North America Microsurgery Market

Market Size in USD Billion

CAGR :

%

USD

4.83 Billion

USD

8.61 Billion

2025

2033

USD

4.83 Billion

USD

8.61 Billion

2025

2033

| 2026 –2033 | |

| USD 4.83 Billion | |

| USD 8.61 Billion | |

| % | |

|

North America Microsurgery Market Size

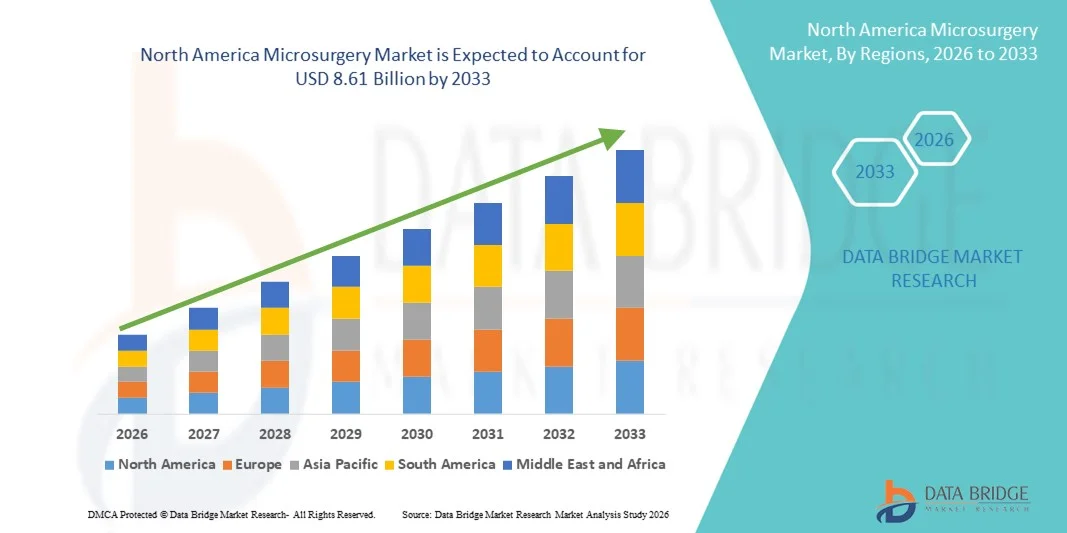

- The North America microsurgery market size was valued at USD 4.83 billion in 2025 and is expected to reach USD 8.61 billion by 2033, at a CAGR of 7.5% during the forecast period

- The market growth is largely driven by the increasing prevalence of chronic diseases, rising demand for minimally invasive procedures, and continuous technological advancements in surgical microscopes and microsurgical instruments across the region

- Furthermore, strong healthcare infrastructure, growing adoption of advanced surgical techniques in specialties such as neurosurgery, ophthalmology, and plastic & reconstructive surgery, and favorable reimbursement frameworks are positioning microsurgery as a preferred approach, thereby significantly accelerating the market’s expansion across North America

North America Microsurgery Market Analysis

- Microsurgery, involving the use of advanced microscopes and precision instruments to operate on delicate anatomical structures such as nerves and small blood vessels, plays a critical role across specialties including neurosurgery, ophthalmology, plastic surgery, and oncology due to its high accuracy, minimal tissue damage, and improved functional outcomes

- The increasing demand for microsurgical procedures is primarily driven by the rising prevalence of chronic diseases, growing cases of trauma and cancer requiring reconstructive and oncologic interventions, and the expanding preference for minimally invasive surgical techniques that support faster recovery and reduced hospital stays

- The United States dominated the North America microsurgery market with the largest revenue share of 78.4% in 2025, supported by advanced healthcare infrastructure, strong reimbursement frameworks, and early adoption of innovative microsurgical technologies, with high procedural volumes recorded across hospitals and academic medical centers

- Canada is expected to witness steady growth during the forecast period owing to improving healthcare investments, increasing adoption of advanced surgical equipment, and rising demand for specialized microsurgical procedures

- The neurosurgery segment dominated the North America microsurgery market with a market share of 29.7% in 2025, driven by the high incidence of neurological disorders and brain tumors, along with the growing adoption of precision-based microsurgical techniques in complex cranial and spinal procedures

Report Scope and North America Microsurgery Market Segmentation

|

Attributes |

North America Microsurgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Microsurgery Market Trends

Technological Advancements in High-Precision Imaging and Robotic Assistance

- A significant and accelerating trend in the North America microsurgery market is the integration of high-definition visualization systems, fluorescence imaging, and robotic-assisted platforms into microsurgical procedures. This convergence of technologies is significantly enhancing surgical precision, dexterity, and intraoperative decision-making across complex specialties

- For instance, advanced surgical microscope platforms equipped with 3D visualization and fluorescence-guided imaging are increasingly adopted in neurosurgery and oncology to improve tumor margin identification and vascular visualization. Similarly, robotic-assisted microsurgical systems are being utilized in reconstructive and urological procedures to enhance motion control and accuracy

- The incorporation of digital imaging and robotics in microsurgery enables improved ergonomics, tremor filtration, and enhanced visualization of minute anatomical structures, thereby reducing operative fatigue and complication rates. For instance, certain platforms integrate augmented reality overlays and real-time imaging guidance to support precise dissection and suturing in delicate procedures. Furthermore, robotic enhancements allow surgeons to perform intricate free tissue transfers and nerve repairs with greater stability and consistency

- The seamless integration of advanced microscopes and robotic technologies with hospital digital infrastructure facilitates better surgical planning, documentation, and interdisciplinary collaboration. Through centralized surgical suites and imaging systems, clinicians can coordinate complex microsurgical interventions more efficiently, creating a more streamlined and data-driven operative environment

- This trend toward more precise, minimally invasive, and technology-driven microsurgical interventions is fundamentally reshaping surgical standards of care. Consequently, leading medical device manufacturers are developing next-generation microscopes and microsurgical instruments with enhanced optics, digital connectivity, and robotic compatibility to meet evolving clinical demands

- The demand for technologically advanced microsurgical solutions is growing rapidly across hospitals and academic medical centers in North America, as healthcare providers increasingly prioritize improved patient outcomes, reduced recovery times, and operational efficiency

- Growing collaboration between medical device companies and academic institutions is accelerating research and development of next-generation microsurgical tools designed to enhance precision, ergonomics, and digital integration

North America Microsurgery Market Dynamics

Driver

Rising Burden of Chronic Diseases and Demand for Minimally Invasive Procedures

- The increasing prevalence of chronic diseases such as cancer, neurological disorders, and cardiovascular conditions, coupled with the growing preference for minimally invasive surgical approaches, is a significant driver for the heightened demand for microsurgical procedures

- For instance, the growing incidence of brain tumors and complex spinal disorders has led to higher adoption of microsurgical neurosurgical techniques in tertiary care hospitals across the United States and Canada. Such strategic expansion of specialized surgical services by healthcare institutions is expected to drive the microsurgery market growth during the forecast period

- As patients and providers seek procedures associated with reduced tissue trauma, shorter hospital stays, and faster functional recovery, microsurgery offers enhanced precision and improved clinical outcomes compared to conventional open surgeries

- Furthermore, advancements in anesthesia, perioperative care, and surgical training programs are strengthening the adoption of microsurgical techniques across multiple specialties, including plastic surgery, ophthalmology, and gynecology

- The growing emphasis on value-based healthcare and outcome-driven treatment models is encouraging hospitals to invest in advanced microsurgical equipment and skilled professionals, thereby supporting sustained procedural growth across North America

- The increasing availability of specialized microsurgical training and fellowship programs is further accelerating the adoption of complex procedures such as transplantation, replantation, and free tissue transfer in leading medical centers

- Rising trauma cases from road accidents and sports injuries are contributing to greater demand for replantation and reconstructive microsurgical procedures in emergency and specialty hospitals

- Expanding insurance coverage and favorable reimbursement policies for advanced surgical interventions are also supporting higher procedural volumes and equipment adoption rates

Restraint/Challenge

High Equipment Costs and Specialized Skill Requirements

- The substantial capital investment required for advanced microsurgical microscopes, precision instruments, and robotic-assisted systems poses a significant challenge to broader adoption, particularly for smaller hospitals and outpatient facilities

- For instance, high acquisition and maintenance costs associated with state-of-the-art surgical microscopes and robotic platforms can limit procurement decisions in budget-constrained healthcare settings, thereby slowing uniform market penetration

- Addressing these cost concerns through flexible financing models, equipment leasing options, and value-based procurement strategies is crucial for expanding access. Companies are increasingly offering service agreements, training support, and bundled solutions to make advanced microsurgical technologies more accessible to healthcare providers. In addition, the need for highly specialized surgical expertise and extensive training can act as a barrier, as not all institutions possess adequately trained microsurgeons or support staff

- While academic and research centers often have structured training programs, community hospitals may face challenges in recruiting and retaining skilled microsurgical professionals, which can limit procedural volumes

- The complexity of microsurgical procedures and the steep learning curve associated with mastering fine motor skills and advanced visualization systems further contribute to adoption constraints in certain facilities

- Overcoming these challenges through cost optimization, expanded surgeon training initiatives, and continuous technological innovation will be vital for sustaining long-term growth in the North America microsurgery market

- Limited availability of skilled microsurgeons in rural and underserved areas can restrict equitable access to advanced microsurgical care, thereby affecting regional market expansion

- Stringent regulatory requirements and lengthy approval timelines for novel microsurgical devices may delay product commercialization and slow technological adoption across healthcare institutions

North America Microsurgery Market Scope

The market is segmented on the basis of application, procedure, equipment type, and end user.

- By Application

On the basis of application, the North America microsurgery market is segmented into general surgery, neurosurgery, ophthalmology, orthopedic surgery, plastic surgery, oncology, gynaecological surgery, oral surgery, and paediatric surgery. The neurosurgery segment dominated the market with the largest revenue share of 29.7% in 2025, primarily driven by the high prevalence of brain tumors, spinal disorders, and neurovascular conditions requiring precision-based interventions. Microsurgical techniques are extensively used in cranial and spinal procedures to enhance visualization and minimize damage to surrounding tissues. The availability of advanced surgical microscopes and high-definition imaging systems in tertiary care hospitals further supports segment dominance. In addition, the strong presence of specialized neurosurgical centers and skilled professionals in the United States contributes significantly to procedural volumes. Favorable reimbursement structures and continuous technological advancements in neuro-navigation systems also strengthen this segment’s leadership position.

The plastic surgery segment is anticipated to witness the fastest growth rate during the forecast period, fueled by increasing demand for reconstructive and cosmetic procedures. Rising trauma cases, post-oncologic breast reconstruction, and complex wound management cases are driving higher adoption of microsurgical free tissue transfer techniques. Growing awareness regarding aesthetic procedures and improved access to specialized care centers are further supporting segment expansion. Technological advancements in micro sutures and precision instruments enhance surgical outcomes, encouraging broader utilization. In addition, the increasing number of outpatient reconstructive procedures in ambulatory surgery centers is accelerating growth. Expanding insurance coverage for reconstructive surgeries is also contributing to rising procedural volumes across North America.

- By Procedure

On the basis of procedure, the North America microsurgery market is segmented into transplantation, replantation, treatment of infertility, and free tissue transfer. The free tissue transfer segment dominated the market in 2025, driven by its widespread application in reconstructive surgeries following trauma, cancer resections, and congenital deformities. This procedure enables the transfer of tissue along with its blood supply, ensuring improved graft survival and functional restoration. The growing incidence of head and neck cancers and breast cancer reconstruction procedures significantly contributes to segment dominance. Advanced microsurgical training programs and improved surgical instruments further enhance procedural success rates. High procedural adoption in specialized hospitals and academic medical centers reinforces its leading market share.

The transplantation segment is projected to witness the fastest growth during the forecast period due to rising cases of organ failure and increasing awareness regarding organ donation programs. Microsurgical techniques are critical in vascular anastomosis and improving graft viability during organ transplants. Expanding transplant infrastructure and improved post-operative care facilities in North America are supporting higher procedural volumes. Continuous innovation in micro suturing materials and surgical microscopes enhances precision in transplant surgeries. Growing government initiatives and funding for organ transplant programs are further accelerating segment expansion. In addition, advancements in immunosuppressive therapies are indirectly supporting the success and growth of transplantation procedures.

- By Equipment Type

On the basis of equipment type, the market is segmented into microsurgical instruments, microscope, and micro sutures materials. The microscope segment dominated the market in 2025 owing to its essential role in providing magnified, high-resolution visualization of delicate anatomical structures. Technological advancements such as 3D imaging, fluorescence guidance, and digital integration significantly enhance surgical accuracy and efficiency. High capital investment by hospitals in advanced operating room infrastructure further drives demand for surgical microscopes. The increasing complexity of neurosurgical and oncologic procedures also reinforces the reliance on advanced visualization systems. Moreover, integration with robotic-assisted platforms strengthens the adoption of high-end microscopes across leading healthcare facilities.

The micro sutures materials segment is expected to witness the fastest growth during the forecast period, driven by increasing volumes of reconstructive and vascular microsurgeries. Continuous innovation in biocompatible and ultra-fine suture materials enhances wound healing and reduces post-operative complications. Rising demand for precision-based anastomosis in transplantation and replantation procedures supports segment expansion. The growing focus on improving surgical outcomes and minimizing scarring further accelerates adoption. In addition, the relatively lower cost compared to capital-intensive equipment enables broader usage across hospitals and clinics. Increasing research activities aimed at developing advanced suture materials also contribute to rapid growth.

- By End User

On the basis of end user, the North America microsurgery market is segmented into hospitals, clinics, research organization, ambulatory surgery centres, and academic and research centres. The hospitals segment dominated the market in 2025 due to the high volume of complex surgical procedures performed in these settings. Hospitals are equipped with advanced operating rooms, high-end microscopes, and multidisciplinary surgical teams necessary for intricate microsurgical interventions. The availability of comprehensive post-operative care and intensive care units further supports segment dominance. Strong reimbursement frameworks and government funding for large healthcare institutions contribute to sustained demand. In addition, hospitals often serve as referral centers for specialized microsurgical cases, ensuring high procedural throughput.

The ambulatory surgery centres segment is anticipated to register the fastest growth during the forecast period owing to the rising preference for cost-effective and minimally invasive outpatient procedures. Increasing advancements in microsurgical instruments and anesthesia techniques make certain procedures feasible in outpatient settings. Shorter recovery times and reduced hospital stays encourage patients to opt for ambulatory facilities. Expanding healthcare infrastructure and favorable regulatory support further promote segment expansion. In addition, the growing number of specialized outpatient surgical centers across the United States and Canada accelerates adoption. The shift toward value-based care models is also contributing to increased utilization of ambulatory surgery centres for selected microsurgical procedures.

North America Microsurgery Market Regional Analysis

- The United States dominated the North America microsurgery market with the largest revenue share of 78.4% in 2025, supported by advanced healthcare infrastructure, strong reimbursement frameworks, and early adoption of innovative microsurgical technologies, with high procedural volumes recorded across hospitals and academic medical centers

- Healthcare providers in the region highly prioritize precision-based surgical interventions, advanced imaging systems, and improved patient outcomes, leading to strong adoption of surgical microscopes, microsurgical instruments, and specialized training programs across leading hospitals and academic centers

- This widespread utilization is further supported by well-established healthcare infrastructure, high healthcare expenditure, the presence of skilled microsurgeons, and favorable reimbursement frameworks, positioning microsurgery as a preferred approach for complex procedures across the United States and Canada

U.S. Microsurgery Market Insight

The U.S. microsurgery market captured the largest revenue share of 78.4% in 2025 within North America, fueled by the high prevalence of chronic diseases and the strong demand for minimally invasive surgical procedures. Healthcare providers are increasingly prioritizing precision-driven interventions supported by advanced surgical microscopes and microsurgical instruments. The presence of leading academic medical centers and specialized surgical training programs further strengthens procedural volumes across neurosurgery, oncology, and plastic surgery. Moreover, substantial healthcare expenditure and favorable reimbursement policies are significantly contributing to sustained market expansion.

Canada Microsurgery Market Insight

The Canada microsurgery market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by growing healthcare investments and increasing adoption of advanced surgical technologies. Rising incidence of cancer, trauma cases, and neurological disorders is fostering demand for precision-based microsurgical procedures. Canadian healthcare institutions are increasingly integrating advanced visualization systems and microsurgical instruments into tertiary care settings. The country is experiencing steady growth across hospital and academic research applications, with microsurgery being incorporated into both reconstructive and specialized surgical programs.

Mexico Microsurgery Market Insight

The Mexico microsurgery market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by improving healthcare infrastructure and increasing access to specialized surgical services. In addition, the rising burden of chronic diseases and trauma-related injuries is encouraging hospitals to adopt advanced microsurgical techniques. Mexico’s expanding private healthcare sector, alongside growing medical tourism activities, is expected to continue stimulating market growth. The gradual integration of advanced surgical microscopes and training programs is further supporting the adoption of microsurgical procedures across key urban centers.

North America Microsurgery Market Share

The North America Microsurgery industry is primarily led by well-established companies, including:

- Stryker (U.S.)

- Medtronic (Ireland)

- Johnson & Johnson Services, Inc. (U.S.)

- Zimmer Biomet (U.S.)

- B. Braun SE (Germany)

- Danaher (U.S.)

- Olympus Corporation (Japan)

- Beaver-Visitec International Inc. (U.S.)

- Global Surgical Corporation (U.S.)

- Microsurgery Instruments, Inc. (U.S.)

- Synovis Micro Companies Alliance, Inc. (U.S.)

- KLS Martin Group (Germany)

- Scanlan International (U.S.)

- Leica Microsystems (Germany)

- Carl Zeiss Meditec AG (Germany)

- Integra LifeSciences Corporation (U.S.)

- Synovis Life Technologies, Inc. (U.S.)

- Checkpoint Surgical, Inc. (U.S.)

- Aesculap, Inc. (U.S.)

- MicroSurgical Technology (U.S.)

What are the Recent Developments in North America Microsurgery Market?

- In December 2025, Medical Microinstruments (MMI) received U.S. FDA 510(k) clearance for its NanoWrist® Scissors and Forceps for robotic microsurgical soft tissue dissection, and completed the first fully robotic microsurgical procedure using these instruments at Tampa General Hospital, marking an evolution in robotic microsurgery beyond traditional anastomosis with full robotic-assisted dissection capabilities

- In October 2025, Medical Microinstruments (MMI) announced the completion of the first robotic microsurgical intracranial procedures using its Symani® surgical system in a U.S. clinical trial (for moyamoya disease), demonstrating robotic precision in intricate brain surgery and expanding potential applications of microsurgical robotics

- In October 2025, Medical Microinstruments (MMI) enrolled the first patient in the landmark PRECISE clinical study in the U.S., marking the largest prospective, multi-center trial focused on evaluating robotic-assisted microsurgery (Symani® Surgical System) for free flap reconstruction and lymphatic repair procedures a significant step in generating clinical evidence to expand robotic microsurgery for complex reconstructive applications

- In April 2024, the FDA granted De Novo classification to MMI’s Symani® Surgical System, making it the only commercially available robotic platform in the U.S. for reconstructive microsurgery, enabling FDA-authorized robotic microsurgery with motion scaling and high-precision wristed instruments

- In June 2023, US Medical Innovations (USMI) received FDA approval for its Canady Flex RoboWrist™, a fully articulating robotic instrument for open, endoscopic, and laparoscopic surgical procedures, representing a significant advancement in articulated robotic tools available to U.S. surgeons

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.