North America Polyolefin Market

Market Size in USD Billion

CAGR :

%

USD

48.84 Billion

USD

155.75 Billion

2025

2033

USD

48.84 Billion

USD

155.75 Billion

2025

2033

| 2026 –2033 | |

| USD 48.84 Billion | |

| USD 155.75 Billion | |

| % | |

|

North America Polyolefin Market Size

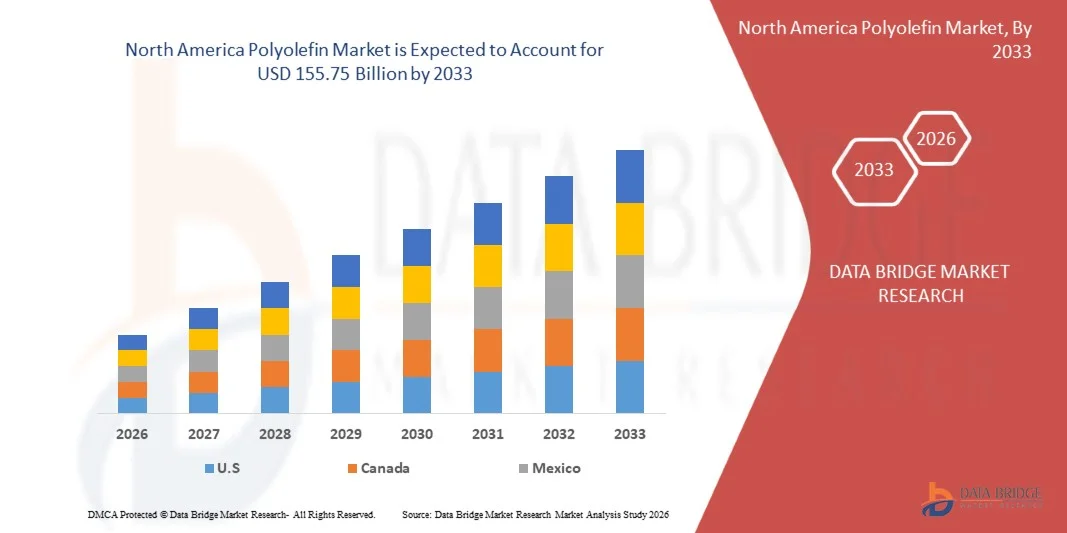

- The North America polyolefin market size was valued at USD 48.84 billion in 2025 and is expected to reach USD 155.75 billion by 2033, at a CAGR of 15.60% during the forecast period

- The market growth is largely fuelled by the increasing demand for lightweight, durable, and cost-effective materials across packaging, automotive, and construction industries

- Rising consumption of plastic packaging, particularly in food and beverage and e-commerce sectors, is further driving the demand for polyolefins globally

North America Polyolefin Market Analysis

- The market is witnessing strong growth driven by the rising demand for versatile polymer materials that offer high strength, flexibility, and chemical resistance across multiple industries

- Increasing focus on sustainability, recyclability, and development of bio-based polyolefins is influencing innovation and shaping long-term growth opportunities in the market

- U.S. dominated the polyolefin market with the largest revenue share in 2025, fueled by strong demand from packaging, automotive, and healthcare industries. Industries are increasingly adopting polyolefins due to their lightweight properties, durability, and cost efficiency across a wide range of applications

- Canada is expected to witness the highest compound annual growth rate (CAGR) in the North America polyolefin market due to rising industrialization, increasing adoption of polyolefin-based packaging solutions, and strategic expansions by key manufacturers. Growing demand from automotive, medical, and consumer goods sectors is also accelerating market growth in the country

- The polyethylene segment held the largest market revenue share in 2025 driven by its widespread usage in packaging, films, and consumer goods due to its flexibility, durability, and cost-effectiveness. Polyethylene is extensively used across industries for its excellent moisture resistance and ease of processing, making it a preferred material for large-scale applications

Report Scope and North America Polyolefin Market Segmentation

|

Attributes |

North America Polyolefin Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

• Exxon Mobil Corporation (U.S.) |

|

Market Opportunities |

• Increasing Demand From Sustainable And Recyclable Packaging Solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Polyolefin Market Trends

“Rising Demand for Lightweight, Durable, and Sustainable Materials”

• The growing demand for lightweight and high-performance materials is significantly shaping the polyolefin market, as industries increasingly prefer materials that offer durability, flexibility, and cost efficiency. Polyolefins are gaining traction due to their wide applicability in packaging, automotive, and construction sectors, where they enhance product performance and reduce overall material weight. This trend is encouraging manufacturers to develop advanced polymer formulations that meet evolving industrial requirements

• Increasing awareness regarding sustainability and recyclability has accelerated the demand for polyolefins in packaging and consumer goods applications. Companies are actively seeking materials that support circular economy initiatives, prompting the use of recyclable and bio-based polyolefins. This has also led to collaborations between polymer producers and end-use industries to improve material performance while reducing environmental impact

• Sustainability and regulatory trends are influencing purchasing decisions, with manufacturers emphasizing eco-friendly production processes, reduced carbon emissions, and recyclable product designs. These factors are helping companies differentiate their offerings in a competitive market and build long-term customer trust. Businesses are also focusing on innovation and certification to align with global environmental standards

• For instance, in 2024, leading polymer manufacturers expanded their portfolios by introducing recyclable and bio-based polyolefin products for packaging and automotive applications. These launches were aimed at addressing the rising demand for sustainable materials and were distributed across industrial and consumer markets. The products were also positioned as environmentally responsible alternatives, enhancing brand value and customer adoption

• While demand for polyolefins is growing, sustained market expansion depends on continuous innovation, cost-effective production, and efficient recycling infrastructure. Manufacturers are focusing on improving material properties, enhancing recyclability, and developing sustainable solutions to meet global demand

North America Polyolefin Market Dynamics

Driver

“Growing Demand for Versatile and Cost-Effective Polymer Materials”

• Rising demand for versatile and cost-effective materials is a major driver for the polyolefin market. Industries are increasingly adopting polyolefins due to their excellent mechanical properties, chemical resistance, and ease of processing. These characteristics make them suitable for a wide range of applications, supporting product innovation and industrial efficiency

• Expanding applications in packaging, automotive, construction, and consumer goods are influencing market growth. Polyolefins provide strength, flexibility, and durability, enabling manufacturers to meet performance requirements across various end-use industries. The increasing demand for lightweight materials in automotive and packaging sectors further reinforces this trend

• Manufacturers are actively promoting polyolefin-based solutions through product innovation, technological advancements, and strategic collaborations. These efforts are supported by the growing need for efficient and sustainable materials, encouraging the adoption of advanced polymer solutions across industries

• For instance, in 2023, major polymer producers reported increased adoption of polyolefins in packaging and automotive applications to improve efficiency and reduce costs. This expansion followed rising demand for lightweight and durable materials, driving repeat usage and product differentiation. Companies also emphasized sustainability and recyclability in their strategies to strengthen market positioning

• Although increasing demand supports growth, wider adoption depends on raw material availability, cost optimization, and advancements in recycling technologies. Investment in sustainable production and circular economy initiatives will be critical to meet global demand and maintain competitive advantage

Restraint/Challenge

“Environmental Concerns and Fluctuating Raw Material Prices”

• Environmental concerns associated with plastic waste and disposal remain a key challenge, limiting the widespread acceptance of polyolefins in certain applications. Regulatory restrictions and increasing pressure to reduce plastic usage are influencing market dynamics. Companies are required to invest in sustainable alternatives and recycling solutions to address these concerns

• Fluctuations in raw material prices, particularly crude oil and natural gas, impact production costs and pricing stability of polyolefins. These variations can affect profit margins and create uncertainties for manufacturers and end-users. Managing cost volatility remains a critical challenge for industry participants

• Supply chain and recycling infrastructure limitations also impact market growth, as efficient collection, sorting, and recycling systems are still developing in many regions. This increases operational challenges and limits the reuse of polyolefin materials. Companies must invest in advanced recycling technologies and infrastructure to improve sustainability outcomes

• For instance, in 2024, several manufacturers faced challenges related to regulatory pressures and rising raw material costs, which impacted production and pricing strategies. These factors led to cautious adoption in certain markets and increased focus on developing sustainable alternatives. Some companies also experienced delays in implementing recycling initiatives due to infrastructure constraints

• Overcoming these challenges will require investment in recycling technologies, development of bio-based alternatives, and improved supply chain efficiency. Collaboration between industry stakeholders, policymakers, and recycling organizations can help unlock long-term growth potential. Furthermore, strengthening sustainability initiatives and innovation in material science will be essential for broader market adoption

North America Polyolefin Market Scope

The market is segmented on the basis of type, end user, and application.

• By Type

On the basis of type, the North America polyolefin market is segmented into polyethylene, polypropylene, and functional polyolefins. The polyethylene segment held the largest market revenue share in 2025 driven by its widespread usage in packaging, films, and consumer goods due to its flexibility, durability, and cost-effectiveness. Polyethylene is extensively used across industries for its excellent moisture resistance and ease of processing, making it a preferred material for large-scale applications.

The polypropylene segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its superior strength, lightweight properties, and high chemical resistance. It is increasingly used in automotive, medical, and industrial applications where performance and durability are critical. The growing demand for lightweight materials and sustainable alternatives is further supporting its rapid adoption.

• By End User

On the basis of end user, the global polyolefin market is segmented into packaging, consumer goods, building and construction, automotive, medical and pharmaceuticals, and others. The packaging segment held the largest market revenue share in 2025 driven by the rising demand for flexible and rigid packaging solutions in food, beverage, and e-commerce industries. Polyolefins are widely used in packaging due to their versatility, strength, and cost efficiency, supporting their dominant position.

The automotive segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for lightweight and fuel-efficient vehicles. Polyolefins are extensively used in automotive components to reduce vehicle weight and improve performance. Growing adoption of electric vehicles and advancements in material technology are further accelerating demand in this segment.

• By Application

On the basis of application, the global polyolefin market is segmented into films and sheet, blow molding, injection molding, and tapes and fibers. The films and sheet segment held the largest market revenue share in 2025 driven by extensive use in packaging, agriculture, and industrial applications. These materials offer flexibility, durability, and moisture resistance, making them highly suitable for a wide range of end uses.

The injection molding segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its ability to produce complex and high-precision components efficiently. It is widely used in automotive, consumer goods, and medical industries due to its cost-effectiveness and scalability. Increasing demand for mass production of plastic components is further supporting the growth of this segment.

North America Polyolefin Market Regional Analysis

- U.S. dominated the polyolefin market with the largest revenue share in 2025, fueled by strong demand from packaging, automotive, and healthcare industries. Industries are increasingly adopting polyolefins due to their lightweight properties, durability, and cost efficiency across a wide range of applications

- The growing demand for flexible packaging, combined with advancements in polymer processing technologies, further supports market growth

- Moreover, increasing focus on recycling initiatives and sustainable material development is significantly contributing to the expansion of the polyolefin market in the U.S.

Canada Polyolefin Market Insight

The Canada polyolefin market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand from the automotive, packaging, and construction sectors. Manufacturers are adopting polyolefins due to their durability, lightweight properties, and cost-effectiveness, which align with industry needs for performance and sustainability. Growing consumer focus on recyclable and eco‑friendly materials is further supporting the uptake of polyolefins in packaging applications. In addition, investments in advanced manufacturing and infrastructure development are contributing to market expansion and strengthening Canada’s position in the global polyolefin landscape.

North America Polyolefin Market Share

The North America polyolefin industry is primarily led by well-established companies, including:

• Exxon Mobil Corporation (U.S.)

• Dow Inc. (U.S.)

• Chevron Phillips Chemical Company LLC (U.S.)

• Phillips 66 Company (U.S.)

• Marathon Petroleum Corporation (U.S.)

• Westlake Chemical Corporation (U.S.)

• Eastman Chemical Company (U.S.)

• Celanese Corporation (U.S.)

• Huntsman Corporation (U.S.)

• Kraton Corporation (U.S.)

• Inter Pipeline Ltd. (Canada)

• Pembina Pipeline Corporation (Canada)

• Nova Chemicals Corporation (Canada)

• Methanex Corporation (Canada)

• Supresta Chemical (U.S.)

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Polyolefin Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Polyolefin Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Polyolefin Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.