Market Analysis and Insights : North America Spinal Implants Market

Market Analysis and Insights : North America Spinal Implants Market

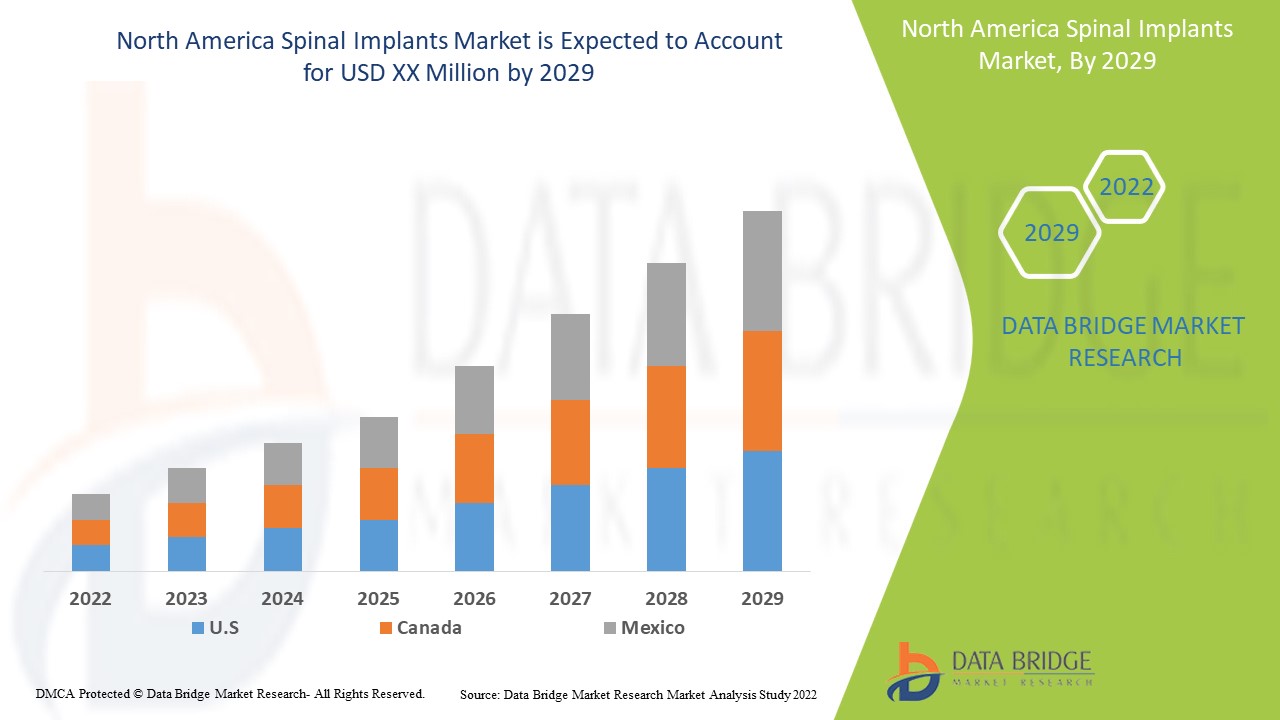

Data Bridge Market Research analyses that the North America spinal implants market to be grow at a CAGR of 5.30% in the forecast period of 2022-2029.

Spinal implants are tools used during spinal surgery to help with stabilization, fusion, correction of abnormalities, and strengthening the spine. The spinal implants are constructed of metals like stainless steel or titanium and come in a variety of sizes to meet the needs of the patient. Hooks, pedicles screws, cages, plates, and rods are some of the other categories. A significant amount of research has done into refining implants in order to enhance patient outcomes.

One of the significant reasons likely to boost the growth and demand of the spinal implants market is the surging demand for minimally invasive spine surgery techniques. The rise in the geriatric population and technological improvements in healthcare sector are expected to propel the global spinal implants market forward. Similarly, the increase in the prevalence of lifestyle related diseases such as obesity is expected to boost market growth. Furthermore, the rising incidences of spinal disorders and launch of advanced bone grafting products are projected to contribute to the market's growth.

Moreover, increase in research and development activities, emerging new markets, and the number of hospitals and surgical centers are boosting plenty of beneficial opportunities that will propel the spinal implants market forward over the projection period.

However, high cost of procedures, less awareness and the dearth of reimbursement in under developed countries are expected to hinder the growth of the spinal implants market. Stringent regulatory guidelines and the lack of adequate physicians are just a few of the challenges that could stymie the spinal implants market's growth.

This North America spinal implants market report provides details of new recent developments, trade regulations, import export analysis, production analysis, value chain optimization, market share, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on North America spinal implants market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

North America Spinal Implants Market Scope and Market Size

The North America spinal implants market is segmented on the basis of procedure, configuration and material. The growth amongst these segments will help you analyse meagre growth segments in the industries, and provide the users with valuable market overview and market insights to help them in making strategic decisions for identification of core market applications.

- On the basis of procedure, spinal implants market is segmented into open surgery, minimally invasive surgery and others.

- Based on configuration, the spinal implants market is segmented into spinal fusion devices, non-fusion devices/motion preservation devices, vertebral compression fracture (VCF) treatment devices, spinal bone stimulators and spine biologics. Spinal fusion devices have been further sub-segmented into thoracolumbar devices, cervical fixation devices and interbody fusion devices. Thoracolumbar devices have been divided into anterior lumbar plates, lumbar plates, pedicle screw, rods, hooks, wires and cables and crosslinks. Cervical fixation devices have been divided into anterior cervical plates, hook fixation systems, plates and screws, clamps and wires. Interbody fusion devices have been divided into non-bone interbody fusion devices and bone interbody fusion devices. Non-fusion devices/motion preservation devices have been further sub-segmented into dynamic stabilization devices, artificial discs, annulus repair devices and nuclear disc prostheses. Dynamic stabilization devices have been divided into interspinous process spacers, pedicle screw-based systems and facet replacement products. Artificial discs have been divided into artificial cervical discs and artificial lumbar discs. Spinal bone stimulators have been further sub-segmented into non-invasive spine bone stimulators and invasive spine bone stimulators. Non-invasive spine bone stimulators have been divided into pulsed electromagnetic field device, capacitive coupling (CC) and combined magnetic field (CMF) devices. Spine biologics have been further sub-segmented into spinal allografts, bone graft substitutes and cell-based matrix. Spinal allografts have been divided into machined bones allograft and demineralized bone matrix. Bone graft substitutes have been divided into bone morphogenetic proteins and synthetic bone grafts.

- The spinal implants market is also segmented on the basis of material into titanium, titanium-alloy, stainless steel, plastic and others.

North America Spinal Implants Market Country Level Analysis

The North America spinal implants market is analysed and market size insights and trends are provided by country, procedure, configuration and material as referenced above.

The countries covered in the North America spinal implants market report are Germany, France, U.K., Italy, Spain, Russia, Netherland, Switzerland, Turkey, Austria, Belgium, and Rest of North America.

Canada is expected to grow during the forecast period of 2022-2029 due to the increasing geriatric population and technological advancement in this region.

The country section of the North America spinal implants market report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points such as consumption volumes, production sites and volumes, import export analysis, price trend analysis, cost of raw materials, down-stream and upstream value chain analysis are some of the major pointers used to forecast the market scenario for individual countries. Also, presence and availability of North America brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

Healthcare Infrastructure growth Installed base and New Technology Penetration

The North America spinal implants market also provides you with detailed market analysis for every country growth in healthcare expenditure for capital equipment, installed base of different kind of products for North America spinal implants market, impact of technology using life line curves and changes in healthcare regulatory scenarios and their impact on the North America spinal implants market. The data is available for historic period 2010 to 2020.

Competitive Landscape and North America Spinal Implants Market Share Analysis

The North America spinal implants market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, North America presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points are only related to the companies’ focus on North America spinal implants market.

Some of the major players operating in the North America spinal implants market are Johnson & Johnson Private Limited, Medtronic, Stryker, SpineGuard, NuVasive, Inc., Zimmer Biomet, Globus Medical, Alphatec Holdings, Inc., Orthofix Medical Inc., RTI Surgical, LDR Holding Corporation, Integra Life Sciences, B. Braun Melsungen AG, and Benvenue Medical, among others.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.