North America Surgical Staplers Device Market

Market Size in USD Billion

CAGR :

%

USD

2.29 Billion

USD

4.16 Billion

2025

2033

USD

2.29 Billion

USD

4.16 Billion

2025

2033

| 2026 –2033 | |

| USD 2.29 Billion | |

| USD 4.16 Billion | |

| % | |

|

North America Surgical Staplers Device Market Size

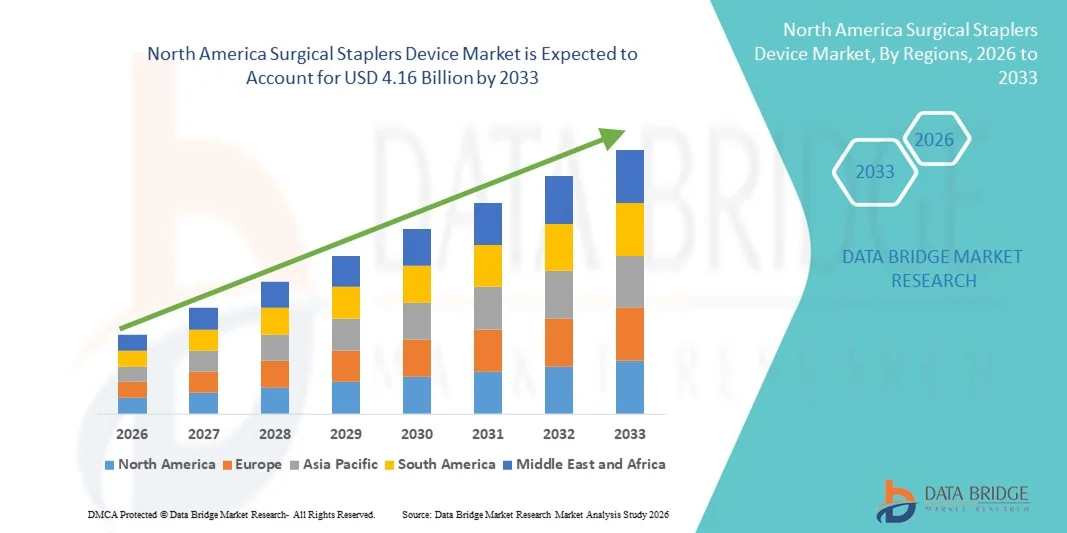

- The North America surgical staplers device market size was valued at USD 2.29 billion in 2025 and is expected to reach USD 4.16 billion by 2033, at a CAGR of7.75% during the forecast period

- The market growth is largely fueled by the increasing number of surgical procedures worldwide and the growing adoption of advanced medical devices that improve surgical efficiency and patient outcomes in both hospitals and ambulatory surgical centers

- Furthermore, rising demand for minimally invasive surgeries and the need for faster wound closure solutions are establishing surgical staplers as a preferred surgical tool. These converging factors are accelerating the uptake of Surgical Staplers Device solutions, thereby significantly boosting the industry's growth

North America Surgical Staplers Device Market Analysis

- Surgical staplers, offering efficient tissue closure and wound management during surgical procedures, are increasingly vital components of modern surgical practices in both hospitals and ambulatory surgical centers due to their precision, reduced operating time, and improved patient recovery outcomes

- The escalating demand for surgical staplers is primarily fueled by the rising number of surgical procedures, increasing preference for minimally invasive surgeries, and continuous advancements in surgical technologies that enhance procedural safety and efficiency

- U.S. dominated the Surgical Staplers Device market with the largest revenue share of 41.2% in 2025, characterized by advanced healthcare infrastructure, high adoption of minimally invasive surgical techniques, and a strong presence of leading medical device manufacturers

- Canada is expected to be the fastest growing region in the Surgical Staplers Device market during the forecast period with a projected CAGR of 8.9%, due to increasing healthcare expenditure, rising surgical volumes, improving hospital infrastructure, and growing adoption of advanced surgical instruments

- The Disposable Surgical Staplers segment dominated the largest market revenue share of 64.2% in 2025, largely due to their ability to reduce cross-contamination risks and improve patient safety

Report Scope and Surgical Staplers Device Market Segmentation

|

Attributes |

Surgical Staplers Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Surgical Staplers Device Market Trends

Rising Adoption of Minimally Invasive Surgical Procedures

- A significant and accelerating trend in the North America Surgical Staplers Device market is the increasing preference for minimally invasive surgical procedures across multiple medical specialties, including gastrointestinal, thoracic, bariatric, and colorectal surgeries. These procedures require precise wound closure and tissue management, making surgical staplers a critical device in modern operating rooms. Hospitals and surgical centers are increasingly adopting advanced stapling devices that enhance procedural efficiency, reduce operating time, and improve patient recovery outcomes

- For instance, leading medical technology companies such as Medtronic and Ethicon (Johnson & Johnson) have introduced advanced surgical stapling systems designed specifically for laparoscopic and minimally invasive procedures. These devices allow surgeons to perform complex tissue closure with greater precision and consistency, significantly improving surgical outcomes and reducing complication rates

- The growing number of surgical procedures performed across Europe, particularly among the aging population, is also contributing to the increasing demand for surgical stapling devices. Elderly patients are more susceptible to chronic conditions that often require surgical intervention, further strengthening the need for efficient surgical tools such as staplers

- In addition, hospitals and healthcare providers are prioritizing surgical technologies that improve procedural safety and reduce postoperative complications. Surgical staplers provide consistent staple formation and controlled tissue compression, helping to minimize bleeding and enhance wound healing compared to conventional suturing methods

- The expansion of ambulatory surgical centers and specialty clinics across North America is further supporting the adoption of surgical staplers. These facilities rely heavily on efficient surgical devices that help shorten procedure times and enable faster patient turnover

- As healthcare systems continue to modernize their surgical infrastructure, the demand for technologically advanced stapling devices that support precision, efficiency, and improved clinical outcomes is expected to continue rising across the European healthcare landscape

North America Surgical Staplers Device Market Dynamics

Driver

Increasing Surgical Volume and Growing Prevalence of Chronic Diseases

- The rising prevalence of chronic diseases such as colorectal cancer, obesity, gastrointestinal disorders, and cardiovascular conditions is a major driver for the growth of the Surgical Staplers Device market. These conditions often require surgical treatment, which significantly increases the demand for efficient and reliable wound closure devices used during surgical procedures

- For instance, in 2025, several hospitals across North America expanded their surgical departments to address the increasing number of bariatric and gastrointestinal surgeries, leading to higher procurement of advanced surgical stapling devices. Such initiatives by healthcare providers and medical device manufacturers are expected to contribute significantly to the growth of the Surgical Staplers Device industry during the forecast period

- The continuous expansion of healthcare infrastructure, including hospitals, specialty clinics, and ambulatory surgical centers, is further driving the demand for surgical staplers. These facilities require high-precision surgical tools that can enhance operational efficiency while maintaining high standards of patient safety

- In addition, the growing adoption of modern surgical techniques has increased the reliance on specialized surgical instruments. Surgical staplers provide faster wound closure compared to traditional suturing methods, helping surgeons reduce operation time and minimize fatigue during lengthy procedures

- Healthcare providers are also focusing on improving patient recovery times and reducing the risk of postoperative complications. The use of surgical staplers supports better surgical outcomes by ensuring consistent staple formation and reducing the likelihood of tissue trauma

- Furthermore, the increasing investment in medical technology development and the expansion of surgical training programs across North America are contributing to greater familiarity and confidence among surgeons in using advanced stapling devices, thereby strengthening market growth

Restraint/Challenge

High Device Costs and Risk of Surgical Complications

- Despite the growing adoption of surgical staplers, the relatively high cost associated with advanced stapling devices remains a significant challenge for the market. Compared to traditional sutures, surgical staplers require higher upfront investment, which can limit adoption among smaller hospitals and healthcare facilities operating under strict budget constraints

- For instance, several healthcare institutions in emerging European economies continue to rely on conventional suturing techniques due to the higher procurement cost of advanced surgical stapling systems and disposable cartridges required for each procedure

- In addition to cost concerns, the risk of surgical complications associated with improper stapler usage can also affect adoption rates. Issues such as misfiring, incomplete staple formation, or tissue damage may occur if the device is not used correctly, potentially leading to patient complications and the need for additional medical intervention

- Regulatory requirements for medical devices are also stringent in many regions, requiring extensive clinical validation and compliance with safety standards before new surgical stapling technologies can be introduced into the market. These regulatory processes can delay product approvals and slow down innovation cycles

- Furthermore, limited access to advanced surgical training in certain healthcare facilities may hinder the optimal utilization of modern stapling devices. Surgeons must be properly trained to ensure safe and effective use of these tools during complex surgical procedures

- Addressing these challenges through cost optimization, improved device design, enhanced surgeon training programs, and strong regulatory compliance will be essential for ensuring sustainable growth in the Surgical Staplers Device market over the coming years.

North America Surgical Staplers Device Market Scope

The market is segmented on the basis of product, type, application, and end user.

- By Product

On the basis of product, the Surgical Staplers Device market is segmented into Manual Surgical Staplers and Powered Surgical Staplers. The Manual Surgical Staplers segment dominated the largest market revenue share of 58.4% in 2025, primarily due to their cost-effectiveness and widespread availability across hospitals and surgical centers. Many healthcare facilities, particularly in emerging economies, prefer manual staplers because they are affordable and require minimal maintenance. Surgeons often rely on manual staplers in routine procedures due to their reliability and familiarity in clinical practice. Hospitals benefit from their ease of use and compatibility with various surgical procedures including abdominal and general surgeries. Additionally, manual staplers are widely stocked in hospital procurement systems due to their lower upfront costs compared to powered alternatives. Their simple mechanical design reduces the need for advanced training and technical support. The availability of multiple models and sizes further strengthens their adoption. Surgical teams also value their consistent performance during high-volume procedures. Growing numbers of surgical procedures globally are contributing to sustained demand. Manufacturers continue to introduce ergonomic designs to improve usability and precision. Strong distribution networks and hospital procurement agreements further support the segment’s market leadership.

The Powered Surgical Staplers segment is expected to witness the fastest CAGR of 7.6% from 2026 to 2033, driven by increasing demand for precision-based surgical instruments and minimally invasive procedures. Powered staplers provide enhanced accuracy, consistent staple formation, and reduced tissue trauma, which improves surgical outcomes. Hospitals and advanced surgical centers are increasingly adopting powered staplers to enhance efficiency during complex procedures such as thoracic and colorectal surgeries. Surgeons benefit from reduced hand fatigue and improved control during long surgical procedures. Technological advancements such as battery-powered systems and improved ergonomic designs are further accelerating adoption. Training programs and surgeon familiarity with powered systems are also increasing. The growing trend of robotic-assisted and laparoscopic surgeries supports the demand for powered staplers. Developed healthcare markets are leading the adoption due to better healthcare infrastructure and higher surgical budgets. Manufacturers are investing heavily in product innovation to improve safety features and operational efficiency. The increasing emphasis on patient safety and surgical precision is further encouraging hospitals to upgrade to powered systems.

- By Type

On the basis of type, the Surgical Staplers Device market is segmented into Disposable Surgical Staplers and Reusable Surgical Staplers. The Disposable Surgical Staplers segment dominated the largest market revenue share of 64.2% in 2025, largely due to their ability to reduce cross-contamination risks and improve patient safety. Hospitals and surgical centers increasingly prefer disposable staplers to comply with stringent infection control guidelines. These devices eliminate the need for sterilization after each procedure, saving time and operational costs for healthcare facilities. Disposable staplers are particularly useful in high-volume surgical environments where efficiency and patient safety are priorities. Surgeons also benefit from consistent performance since each device is new and sterile. Growing awareness of hospital-acquired infections has strengthened the adoption of single-use devices. Healthcare regulatory authorities often recommend disposable surgical tools to ensure maximum hygiene standards. Manufacturers are introducing advanced disposable staplers with improved precision and ergonomic features. Increased surgical procedure volumes worldwide further drive demand for disposable devices. Hospitals also find inventory management easier with single-use products. Strong hospital procurement practices and supplier contracts contribute to this segment’s continued dominance.

The Reusable Surgical Staplers segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, supported by the increasing focus on cost optimization and environmental sustainability in healthcare systems. Reusable staplers offer long-term economic benefits for hospitals as the device can be sterilized and used multiple times with replaceable cartridges. Healthcare facilities aiming to reduce medical waste are gradually adopting reusable surgical instruments. Technological improvements have enhanced the durability and reliability of reusable staplers, making them more attractive to surgeons and hospitals. Sterilization technologies and hospital infection control systems have also improved significantly, supporting their safe reuse. Hospitals with well-developed sterilization infrastructure are particularly inclined to adopt reusable staplers. The rising pressure to reduce healthcare expenditure in many countries is encouraging hospitals to shift toward cost-effective solutions. Manufacturers are also designing reusable staplers with improved ergonomics and modular components. Growing sustainability initiatives within healthcare systems are further boosting this segment’s growth. As healthcare providers seek long-term cost savings and waste reduction, reusable staplers are expected to gain greater acceptance globally.

- By Application

On the basis of application, the Surgical Staplers Device market is segmented into Abdominal and Pelvic Surgery, General Surgery, Cardiac and Thoracic Surgery, Orthopedic Surgery, and Other Surgical Applications. The General Surgery segment dominated the largest market revenue share of 36.8% in 2025, driven by the high volume of surgical procedures performed globally. Surgical staplers are extensively used in general surgeries such as gastrointestinal operations, bariatric procedures, and colorectal surgeries. Hospitals rely on stapling devices to ensure efficient wound closure and reduced operating time. Surgeons prefer staplers because they provide consistent staple formation and minimize tissue trauma compared to traditional sutures. Increasing prevalence of gastrointestinal disorders and obesity-related surgeries also contributes to higher procedure volumes. Healthcare facilities are increasingly adopting minimally invasive surgical techniques where staplers play a critical role. Technological improvements in stapling devices have enhanced surgical precision and patient outcomes. The growing aging population worldwide is further increasing demand for general surgical procedures. Hospitals also benefit from reduced operating time and improved workflow efficiency. Continuous innovation in stapler design and materials supports the long-term growth of this segment.

The Cardiac and Thoracic Surgery segment is expected to witness the fastest CAGR of 7.3% from 2026 to 2033, driven by rising incidence of cardiovascular and respiratory diseases worldwide. Surgical staplers are increasingly used in thoracic procedures such as lung resections and other complex operations requiring precise tissue closure. Hospitals and specialized cardiac centers are adopting advanced stapling devices to improve surgical accuracy and reduce complications. The growing number of minimally invasive thoracic surgeries is also supporting the demand for stapling devices. Surgeons rely on staplers for reliable closure of blood vessels and tissues during delicate procedures. Technological advancements in powered staplers further enhance their suitability for cardiac and thoracic surgeries. Increasing investments in advanced surgical infrastructure are also contributing to the segment’s growth. The rising prevalence of lung cancer and heart diseases globally is leading to higher surgical volumes. Healthcare systems are focusing on improving surgical outcomes and patient safety, encouraging the use of modern stapling technologies. As thoracic surgery techniques continue to evolve, the adoption of surgical staplers in these procedures is expected to grow significantly.

- By End User

On the basis of end user, the Surgical Staplers Device market is segmented into Hospitals, Ambulatory Surgical Centers (ASCs), and Clinics. The Hospitals segment dominated the largest market revenue share of 67.5% in 2025, supported by the high number of complex surgical procedures performed in hospital settings. Hospitals possess advanced surgical infrastructure and specialized surgical teams capable of performing diverse procedures requiring stapling devices. Most high-risk and specialized surgeries such as thoracic, abdominal, and cardiovascular procedures are conducted in hospitals. Hospitals also maintain strong procurement systems ensuring the consistent supply of surgical staplers and related consumables. Government funding and healthcare reimbursement programs further strengthen hospital purchasing capacity. Surgeons working in hospitals often prefer advanced stapling technologies due to their reliability and precision. Hospitals also serve as primary centers for surgical training and clinical trials involving innovative surgical devices. Increasing patient admissions and surgical volumes continue to support demand. Integration of minimally invasive and robotic-assisted surgeries further drives the use of staplers in hospital settings.

The Ambulatory Surgical Centers (ASCs) segment is expected to witness the fastest CAGR of 7.8% from 2026 to 2033, driven by the growing preference for outpatient surgical procedures and cost-effective healthcare services. ASCs provide faster surgical services with shorter patient recovery times compared to traditional hospital settings. Patients increasingly prefer ASCs due to lower costs and reduced hospital stays. Many minimally invasive surgeries are now being performed in ambulatory settings, increasing the use of surgical staplers. Healthcare systems are also encouraging the shift toward outpatient procedures to reduce hospital congestion and operational costs. Technological advancements in surgical equipment have made it easier for ASCs to perform complex procedures safely. Surgeons benefit from efficient operating room workflows and reduced patient turnaround time. Growing investments in ASC infrastructure and expansion of outpatient care facilities further support market growth. As healthcare providers emphasize cost efficiency and patient convenience, ASCs are expected to become a major growth driver in the surgical staplers market.

North America Surgical Staplers Device Market Regional Analysis

- The North America surgical staplers device market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the increasing number of surgical procedures, advancements in medical technology, and the growing preference for minimally invasive surgical techniques across healthcare systems in the region. The rising prevalence of chronic conditions such as gastrointestinal disorders, obesity, and cancer is significantly increasing the demand for surgical interventions, which in turn is supporting the adoption of efficient wound closure devices such as surgical staplers across hospitals and specialty surgical centers

- Surgical staplers have become an essential component in modern operating rooms due to their ability to provide reliable tissue closure, reduce surgical time, and improve clinical outcomes. Their growing use in procedures such as bariatric surgery, colorectal surgery, and thoracic surgery is contributing to increased demand across healthcare facilities. In addition, the shift toward minimally invasive and laparoscopic procedures has further accelerated the adoption of surgical stapling devices that enable greater precision and efficiency during complex surgical operations

- The continuous expansion of hospital infrastructure, along with the presence of well-established healthcare systems and advanced surgical facilities in North America, is further supporting the adoption of modern surgical stapling technologies. Furthermore, increasing investments in healthcare modernization, the expansion of ambulatory surgical centers, and the rising focus on improving surgical efficiency and patient safety are encouraging healthcare providers to incorporate technologically advanced surgical staplers into routine clinical practice

U.S. Surgical Staplers Device Market Insight

The U.S. surgical staplers device market dominated the North American market with the largest revenue share of 41.2% in 2025, supported by the country’s highly developed healthcare infrastructure and the widespread adoption of minimally invasive surgical procedures. Hospitals and specialized surgical centers in the United States increasingly rely on surgical staplers for their precision, reliability, and ability to improve surgical efficiency and patient outcomes. The country also benefits from a strong presence of leading medical device manufacturers and continuous technological advancements in surgical instruments. Additionally, the increasing number of bariatric, gastrointestinal, and cancer-related surgeries is significantly driving demand for surgical stapling devices. Government support for healthcare innovation, combined with rising investments in hospital modernization and surgical training programs, is further strengthening the growth of the surgical staplers device market in the United States.

Canada Surgical Staplers Device Market Insight

The Canada surgical staplers device market is expected to grow at the fastest CAGR of 8.9% during the forecast period, driven by increasing healthcare expenditure, rising surgical volumes, and ongoing improvements in hospital infrastructure across the country. Canada’s healthcare system continues to expand its surgical capacity through the development of modern hospitals and specialized surgical centers, which is encouraging the adoption of advanced surgical instruments including stapling devices. The growing prevalence of chronic diseases and the aging population are also contributing to a higher demand for surgical procedures, particularly in gastrointestinal and cardiovascular treatments. Furthermore, healthcare providers in Canada are increasingly adopting technologically advanced surgical tools to improve surgical precision, reduce procedure time, and enhance patient recovery outcomes. Continuous investments in healthcare modernization and medical technology adoption are expected to support sustained growth of the surgical staplers device market in Canada during the forecast period.

North America Surgical Staplers Device Market Share

The Surgical Staplers Device industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- B. Braun S.E. (Germany)

- 3M Company (U.S.)

- CONMED Corporation (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- Purple Surgical (U.K.)

- Grena Ltd. (U.K.)

- Frankenman International Ltd. (China)

- Victor Medical Instruments Co., Ltd. (China)

- Welfare Medical Ltd. (U.K.)

- Surgnova Healthcare Technologies (India)

- Meril Life Sciences Pvt. Ltd. (India)

- Reach Surgical, Inc. (China)

- Stapleline Medizintechnik GmbH (Germany)

- Smith & Nephew (U.K.)

- Cardinal Health (U.S.)

- Teleflex Incorporated (U.S.)

- Zhejiang Geyi Medical Instrument Co., Ltd. (China)

- LocaMed Ltd. (U.K.)

Latest Developments in North America Surgical Staplers Device Market

- In March 2021, Ethicon, a Johnson & Johnson MedTech company, announced the launch of the ECHELON+ Stapler with Gripping Surface Technology (GST) Reloads, designed to improve staple-line security and reduce surgical complications. The powered surgical stapler incorporates dynamic firing technology and enhanced compression capabilities to deliver consistent staple formation and improved tissue management during surgical procedures. This launch highlighted Ethicon’s commitment to advancing surgical stapling technologies that improve clinical outcomes and surgeon confidence

- In June 2021, Intuitive Surgical introduced the SureForm robotic-assisted surgical stapler integrated with SmartFire technology for use with robotic surgical systems. The device allows surgeons to control the stapler directly from the surgical console during robotic-assisted procedures, enabling improved precision and workflow efficiency. This development represented a significant advancement in robotic-enabled surgical stapling solutions

- In August 2022, Teleflex Incorporated announced the acquisition of Standard Bariatrics, Inc. for approximately USD 170 million, with additional milestone payments possible. The acquisition brought a novel powered surgical stapling technology specifically designed for bariatric procedures into Teleflex’s portfolio, strengthening the company’s position in advanced surgical technologies and minimally invasive surgery solutions

- In May 2024, Ethicon, part of Johnson & Johnson MedTech, announced the U.S. launch of the ECHELON LINEAR Cutter, a surgical stapler integrating both 3D-Stapling Technology and Gripping Surface Technology. Clinical evaluations indicated the device delivered approximately 47% fewer leaks at the staple line, supporting improved surgical safety and outcomes in colorectal and other complex procedures

- In July 2024, Ethicon launched the next-generation ECHELON™ 3000 Stapler, a digitally enabled surgical stapler designed with powered articulation and an expanded jaw aperture to improve surgical access and control during open and minimally invasive procedures. The device enables surgeons to position and operate the stapler with greater precision, reflecting ongoing innovation in surgical stapling systems

- In June 2025, Johnson & Johnson MedTech announced the U.S. launch of the ETHICON™ 4000 Stapler, an advanced surgical stapling system incorporating proprietary 3D Staple Technology and enhanced reload design to improve staple-line integrity and reduce the risk of leaks and bleeding complications across multiple surgical specialties. The system is also designed for future integration with the company’s OTTAVA robotic surgical platform

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.