North America Topical Skin Adhesive Market

Market Size in USD Billion

CAGR :

%

USD

236.50 Billion

USD

330.95 Billion

2025

2033

USD

236.50 Billion

USD

330.95 Billion

2025

2033

| 2026 –2033 | |

| USD 236.50 Billion | |

| USD 330.95 Billion | |

| % | |

|

North America Topical Skin Adhesive Market Size

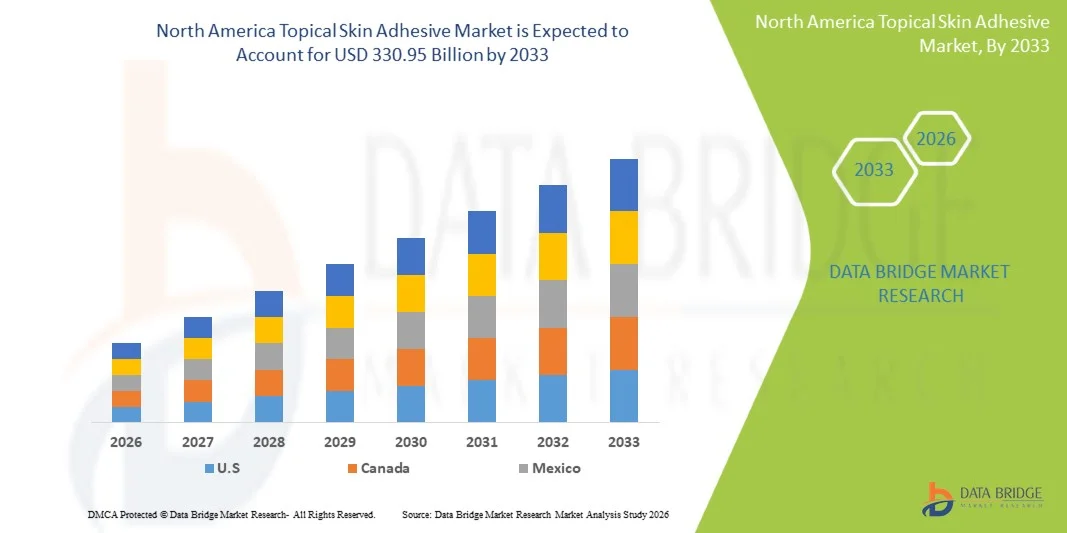

- The North America Topical Skin Adhesive Market size was valued at USD 236.50 billion in 2025 and is expected to reach USD 330.95 billion by 2033, at a CAGR of 4.29% during the forecast period

- The market growth is largely fueled by the increasing number of surgical procedures, rising prevalence of traumatic injuries, and growing adoption of minimally invasive wound closure techniques across hospitals and ambulatory surgical centers

- Furthermore, rising demand for faster wound closure, reduced infection risks, and improved cosmetic outcomes is establishing topical skin adhesives as an effective alternative to traditional sutures and staples. These converging factors are accelerating the uptake of Topical Skin Adhesive solutions, thereby significantly boosting the industry's growth

North America Topical Skin Adhesive Market Analysis

- Topical skin adhesives, offering advanced wound closure solutions for surgical incisions and minor lacerations, are increasingly vital components of modern surgical and emergency care in both hospitals and ambulatory surgical centers due to their ability to provide rapid wound sealing, reduce infection risks, and improve cosmetic outcomes

- The escalating demand for topical skin adhesives is primarily fueled by the rising number of surgical procedures, increasing prevalence of traumatic injuries, and growing preference for minimally invasive wound closure techniques that enable faster healing and reduced hospital stays

- The U.S. dominated the North America Topical Skin Adhesive Market with the largest revenue share of approximately 41.8% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative wound closure technologies, and the strong presence of leading medical device manufacturers. Hospitals, ambulatory surgical centers, and emergency care units across the country are increasingly adopting topical skin adhesives for minimally invasive surgical procedures, trauma care, and outpatient wound management

- Canada is expected to be the fastest-growing region in the North America Topical Skin Adhesive Market during the forecast period, registering a CAGR of approximately 8.3%, driven by increasing healthcare expenditure, rising surgical procedure volumes, expanding access to modern wound care technologies, and growing awareness of advanced wound closure solutions across hospitals and specialty clinics

- The 2-Octyl Cyanoacrylate Adhesive segment dominated the largest market revenue share of 46.8% in 2025, driven by its superior flexibility, strength, and biocompatibility for wound closure applications

Report Scope and North America Topical Skin Adhesive Market Segmentation

|

Attributes |

Topical Skin Adhesive Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

• Johnson & Johnson (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Topical Skin Adhesive Market Trends

“Increasing Preference for Advanced Wound Closure Solutions”

- A significant and accelerating trend in the global North America Topical Skin Adhesive Market is the increasing preference for advanced wound closure solutions that provide faster healing, improved cosmetic outcomes, and reduced risk of infection compared to traditional sutures and staples. Healthcare professionals are increasingly adopting topical skin adhesives in surgical procedures, trauma care, and emergency settings due to their ability to simplify wound closure while minimizing patient discomfort

- For instance, in 2025 several hospitals and ambulatory surgical centers in the United States and Europe expanded the use of cyanoacrylate-based topical skin adhesives in minor surgical procedures and emergency wound management, enabling clinicians to close superficial wounds quickly without the need for sutures. Similarly, dermatology and plastic surgery clinics are increasingly adopting medical skin adhesives to improve aesthetic outcomes and reduce scarring following cosmetic procedures

- Advancements in medical adhesive formulations are also contributing to this trend, with manufacturers developing stronger, flexible, and antimicrobial adhesive products designed to enhance wound healing and reduce complications. Modern topical skin adhesives provide improved bonding strength and durability, allowing them to be used in a wider range of surgical and trauma applications

- The growing adoption of minimally invasive procedures and outpatient surgical treatments is further increasing the demand for topical skin adhesives. These products enable quicker procedures, reduce operating room time, and support faster patient recovery, making them highly attractive to hospitals, ambulatory surgical centers, and specialized clinics

- In addition, the increasing focus on patient comfort and reduced hospital stays is encouraging healthcare providers to adopt alternative wound closure techniques such as topical skin adhesives, particularly in pediatric care and emergency departments

- As healthcare systems worldwide continue to prioritize efficiency and patient-centered treatment approaches, the demand for reliable and easy-to-use wound closure solutions such as topical skin adhesives is expected to expand significantly across hospitals, trauma centers, and outpatient surgical facilities

North America Topical Skin Adhesive Market Dynamics

Driver

“Growing Surgical Procedures and Rising Demand for Minimally Invasive Wound Closure Methods”

- The increasing number of surgical procedures worldwide is a key driver supporting the growth of the North America Topical Skin Adhesive Market. Hospitals and surgical centers are increasingly adopting advanced wound closure solutions that improve efficiency while reducing procedure time and postoperative complications

- For instance, in 2025 several leading hospitals in the United States and Japan reported higher adoption of topical skin adhesives in orthopedic and cosmetic surgeries, allowing surgeons to close surgical incisions more efficiently while improving cosmetic outcomes and reducing infection risks. Emergency departments are also increasingly utilizing skin adhesives to treat minor lacerations and trauma injuries

- The rising prevalence of chronic conditions and injuries that require surgical intervention is further contributing to the demand for advanced wound closure products. Procedures in dermatology, plastic surgery, orthopedics, and general surgery frequently require reliable closure methods that promote faster healing and minimal scarring

- In addition, the expansion of ambulatory surgical centers and outpatient care facilities is driving the demand for topical skin adhesives, as these facilities often prefer quick and efficient wound closure solutions that enable faster patient discharge

- Growing awareness among healthcare professionals about the clinical benefits of skin adhesives, including reduced needle-stick injuries and improved patient comfort, is further supporting market adoption across hospitals and specialty clinics

Restraint/Challenge

“Product Cost Limitations and Risk of Adhesive-Related Complications”

- Despite the advantages of topical skin adhesives, certain challenges continue to limit their widespread adoption in some healthcare settings. One major restraint is the relatively higher cost of advanced medical adhesives compared to traditional wound closure methods such as sutures and staples, which may discourage their use in cost-sensitive healthcare systems

- For instance, several hospitals in developing regions of Asia, Africa, and Latin America continue to rely on conventional suturing techniques due to budget constraints and limited access to advanced wound closure technologies, even though skin adhesives offer faster and less invasive treatment options

- Another challenge involves the potential risk of adhesive-related complications, such as allergic reactions, skin irritation, or reduced bonding effectiveness in areas exposed to moisture or movement. These factors can limit the suitability of topical skin adhesives for certain types of wounds or surgical procedures

- In addition, healthcare providers must ensure proper training and product selection to achieve optimal wound closure results, as incorrect application techniques may affect adhesion strength and healing outcomes

- Regulatory requirements and product approval processes for medical adhesives can also present challenges for manufacturers seeking to introduce new formulations in global markets. Ensuring product safety, biocompatibility, and consistent performance requires rigorous testing and compliance with medical device regulations

- Addressing these challenges through continued product innovation, cost optimization, and improved clinical training programs will be essential to expand the adoption of topical skin adhesives and support long-term market growth

North America Topical Skin Adhesive Market Scope

The market is segmented on the basis of product type, application, end-users, and distribution channel.

• By Product Type

On the basis of product type, the North America Topical Skin Adhesive Market is segmented into 2-Octyl Cyanoacrylate Adhesive, N-Butyl Cyanoacrylate Adhesive, 2-Ethyl Cyanoacrylate Adhesive, and Methyl Cyanoacrylate Adhesive. The 2-Octyl Cyanoacrylate Adhesive segment dominated the largest market revenue share of 46.8% in 2025, driven by its superior flexibility, strength, and biocompatibility for wound closure applications. This adhesive type is widely used in surgical procedures due to its ability to create strong skin bonds while minimizing tissue toxicity. Healthcare professionals prefer 2-octyl cyanoacrylate because it offers longer polymer chains that provide greater durability and resistance to cracking during patient movement. The growing adoption of minimally invasive surgical procedures is further boosting demand for advanced skin adhesives. In addition, the increasing preference for non-invasive wound closure techniques that eliminate the need for sutures or staples supports segment growth. Hospitals and ambulatory surgical centers increasingly utilize these adhesives to reduce procedure time and improve patient comfort. Continuous innovations in medical adhesives and the rising volume of outpatient surgical procedures are also strengthening the demand for 2-octyl cyanoacrylate products globally.

The N-Butyl Cyanoacrylate Adhesive segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by its cost-effectiveness and growing application in trauma and emergency wound closure. N-butyl cyanoacrylate adhesives are widely used for quick wound sealing in emergency departments and trauma centers due to their rapid polymerization and strong adhesive properties. Increasing cases of traumatic injuries, road accidents, and minor lacerations are contributing to the growing use of this adhesive type. In addition, healthcare facilities in emerging economies prefer N-butyl cyanoacrylate adhesives because they offer reliable performance at lower costs compared to other advanced formulations. Rising awareness about infection prevention and faster wound healing is also encouraging the adoption of medical adhesives. Furthermore, advancements in product formulations are improving adhesive strength and safety profiles, further supporting the expansion of this segment during the forecast period.

• By Application

On the basis of application, the North America Topical Skin Adhesive Market is segmented into Surgical Incisions, Trauma-Induced Lacerations, Burn and Skin Grafting, Wound Closure, Chronic Wounds, and Others. The Surgical Incisions segment dominated the largest market revenue share of 41.2% in 2025, driven by the increasing number of surgical procedures performed globally. Topical skin adhesives are widely used for closing surgical incisions due to their ability to provide fast, sterile, and aesthetically favorable wound closure. These adhesives help reduce operation time and eliminate the need for suture removal, thereby improving patient comfort and recovery. The rising adoption of minimally invasive and cosmetic surgical procedures is also increasing the demand for effective wound closure solutions. In addition, topical skin adhesives reduce the risk of infection and scarring compared to traditional sutures or staples. Hospitals and surgeons increasingly prefer these adhesives for small surgical wounds and laparoscopic procedures. Growing healthcare infrastructure and the expansion of surgical facilities worldwide are further driving the demand for skin adhesives in surgical applications.

The Trauma-Induced Lacerations segment is expected to witness the fastest CAGR of 10.3% from 2026 to 2033, fueled by the rising incidence of accidental injuries and emergency trauma cases worldwide. Topical skin adhesives are increasingly used in emergency departments for the rapid closure of minor cuts and lacerations. These adhesives allow healthcare providers to treat wounds quickly without requiring complex surgical procedures. Increasing road accidents, workplace injuries, and sports-related wounds are driving demand for efficient wound management solutions. In addition, topical adhesives reduce the need for anesthesia and shorten treatment time in emergency care settings. Growing awareness among healthcare professionals regarding the clinical benefits of medical adhesives is also contributing to segment growth. The expansion of trauma care facilities and emergency medical services globally is expected to further support the adoption of topical skin adhesives in trauma treatment applications.

• By End-Users

On the basis of end-users, the North America Topical Skin Adhesive Market is segmented into Hospitals, Clinics, Trauma Centers, Ambulatory Surgical Centers, and Others. The Hospitals segment dominated the largest market revenue share of 48.6% in 2025, driven by the high volume of surgical procedures and trauma treatments conducted in hospital settings. Hospitals serve as primary healthcare centers where a wide range of surgeries and wound management procedures are performed daily. The availability of advanced medical infrastructure and skilled healthcare professionals supports the widespread adoption of topical skin adhesives in hospitals. In addition, hospitals prefer these adhesives because they reduce surgical time and improve patient recovery outcomes. Increasing hospital admissions due to chronic diseases and trauma cases are also contributing to the rising demand for effective wound closure solutions. Furthermore, the expansion of hospital networks and improvements in healthcare infrastructure across emerging economies are strengthening the dominance of this segment.

The Ambulatory Surgical Centers segment is expected to witness the fastest CAGR of 11.1% from 2026 to 2033, driven by the growing preference for outpatient surgical procedures. Ambulatory surgical centers offer cost-effective and convenient treatment options for patients requiring minor surgeries and wound management procedures. Topical skin adhesives are widely used in these centers due to their ability to close wounds quickly and efficiently without requiring prolonged hospitalization. The increasing adoption of minimally invasive surgeries is further boosting the demand for skin adhesives in outpatient settings. In addition, shorter procedure times and faster patient discharge rates make these adhesives highly suitable for ambulatory care facilities. The rising number of ambulatory surgical centers globally and increasing healthcare cost-containment strategies are expected to further accelerate segment growth.

• By Distribution Channel

On the basis of distribution channel, the North America Topical Skin Adhesive Market is segmented into Direct Sales and Retail. The Direct Sales segment dominated the largest market revenue share of 62.4% in 2025, driven by the strong presence of medical device manufacturers supplying products directly to hospitals and healthcare institutions. Direct sales channels allow manufacturers to establish long-term supply contracts with hospitals, clinics, and surgical centers. These agreements ensure consistent product availability and enable healthcare providers to access advanced medical adhesive products. In addition, direct sales provide manufacturers with better control over pricing, distribution logistics, and customer relationships. The increasing demand for bulk procurement of surgical supplies in hospitals is further strengthening the growth of this segment. Medical device companies also provide technical support and training through direct distribution channels, which enhances product adoption in healthcare facilities.

The Retail segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by the growing availability of topical skin adhesives through pharmacies and online medical supply platforms. Retail channels are becoming increasingly popular for minor wound care products used in outpatient and home care settings. Consumers and healthcare professionals are purchasing medical adhesives for small cuts and minor injuries through retail pharmacies and e-commerce platforms. The rising trend of self-care and home healthcare is also contributing to increased retail demand. In addition, expanding digital healthcare marketplaces and improved product accessibility are supporting the growth of this segment globally.

North America Topical Skin Adhesive Market Regional Analysis

- North America dominated the North America Topical Skin Adhesive Market with the largest revenue share of approximately 42.3% in 2025, supported by advanced healthcare infrastructure, strong adoption of innovative wound closure technologies, and the presence of leading medical device manufacturers. The increasing number of surgical procedures, growing demand for minimally invasive treatment methods, and the expansion of ambulatory surgical centers are significantly driving the adoption of topical skin adhesives across hospitals and specialty clinics in the region

- Healthcare providers in North America increasingly prefer topical skin adhesives for wound closure due to their ability to reduce procedure time, minimize infection risk, and improve cosmetic outcomes compared to traditional sutures or staples. These products are widely used in emergency departments, dermatology clinics, and outpatient surgical settings for the management of minor lacerations and surgical incisions

- The strong presence of technologically advanced healthcare facilities, high healthcare expenditure, and continuous product innovation by major medical device companies further support the growth of the North America Topical Skin Adhesive Market in North America. In addition, the rising preference for outpatient surgeries and patient-centered care models is encouraging the use of advanced wound closure solutions such as medical adhesives

U.S. North America Topical Skin Adhesive Market Insight

The U.S. North America Topical Skin Adhesive Market accounted for the largest share within North America in 2025, driven by the country’s advanced healthcare infrastructure and high adoption of minimally invasive surgical technologies. Hospitals, ambulatory surgical centers, and specialized orthopedic and dermatology clinics are increasingly utilizing topical skin adhesives to enhance surgical efficiency and improve patient outcomes. The rising number of cosmetic and reconstructive procedures, along with increasing demand for faster wound closure methods in emergency care units, is further supporting market expansion. In addition, strong research and development activities, continuous product launches, and the presence of leading medical device companies contribute to the growing adoption of topical skin adhesives across the U.S. healthcare system. The **U.S. dominated the North America Topical Skin Adhesive Market with the largest revenue share of approximately 41.8% in 2025**, supported by advanced healthcare infrastructure, high adoption of innovative wound closure technologies, and the strong presence of leading medical device manufacturers. Hospitals, ambulatory surgical centers, and emergency care units across the country are increasingly adopting topical skin adhesives for minimally invasive surgical procedures, trauma care, and outpatient wound management.

Canada North America Topical Skin Adhesive Market Insight

Canada North America Topical Skin Adhesive Market is expected to be the fastest-growing region in the North America Topical Skin Adhesive Market during the forecast period, registering a CAGR of approximately 8.3%, driven by increasing healthcare expenditure, rising surgical procedure volumes, expanding access to modern wound care technologies, and growing awareness of advanced wound closure solutions across hospitals and specialty clinics. Healthcare providers across Canada are increasingly adopting topical skin adhesives to improve treatment outcomes and reduce recovery times associated with surgical procedures and traumatic injuries. Hospitals and ambulatory surgical centers in provinces such as Ontario, Quebec, and British Columbia are investing in advanced wound closure technologies to support the growing demand for minimally invasive procedures. Furthermore, ongoing improvements in healthcare infrastructure and surgical training programs are enabling wider adoption of topical skin adhesives across hospitals and specialty clinics, thereby supporting continued market growth in the country.

North America Topical Skin Adhesive Market Share

The Topical Skin Adhesive industry is primarily led by well-established companies, including:

• Johnson & Johnson (U.S.)

• Baxter International Inc. (U.S.)

• B. Braun SE (Germany)

• Medtronic plc (Ireland)

• Advanced Medical Solutions Group plc (U.K.)

• Gem S.r.l. (Italy)

• Peter Surgical (France)

• Dermabond (U.S.)

• Adhezion Biomedical, LLC (U.S.)

• 3M Company (U.S.)

• Medline Industries, LP (U.S.)

• Stryker Corporation (U.S.)

• Bioseal, Inc. (U.S.)

• Aesculap, Inc. (Germany)

• Chemence Medical, Inc. (U.K.)

• Henkel AG & Co. KGaA (Germany)

• Glustitch Inc. (Canada)

• Meyer-Haake GmbH (Germany)

• Tissuemed Ltd. (U.K.)

• Sun Medical Co., Ltd. (Japan)

Latest Developments in North America Topical Skin Adhesive Market

- In February 2021, Advanced Medical Solutions Group plc announced the launch of LiquiBand® XL Topical Skin Adhesive, designed to provide strong and flexible wound closure for surgical incisions and traumatic lacerations. The product incorporates advanced cyanoacrylate-based adhesive technology that enables rapid polymerization and creates a microbial barrier to support faster healing and improved cosmetic outcomes in surgical wound management

- In March 2022, Medtronic plc announced the introduction of the V-Loc Wound Closure Device integrated with topical skin adhesive technologies to enhance surgical incision closure. The development was aimed at improving surgical workflow efficiency and reducing the need for traditional sutures and staples while promoting minimally invasive wound closure approaches

- In April 2023, Advanced Medical Solutions Group plc announced the launch of LiquiBandFix8 Mesh Skin Adhesive, a device designed to provide secure mesh fixation and wound closure in surgical procedures. The product combines a medical-grade mesh with topical skin adhesive technology to provide a flexible, waterproof microbial barrier and improved surgical wound support

- In July 2023, Ethicon (Johnson & Johnson MedTech) expanded the clinical adoption of its DERMABOND PRINEO Skin Closure System, a topical skin adhesive combined with a self-adhering mesh for surgical incision closure. The system provides a strong, flexible microbial barrier and has demonstrated improved cosmetic outcomes and reduced hospital stay compared with conventional suturing techniques

- In May 2024, GluStitch Inc. announced the launch of GluStitch® Topical Skin Adhesive for surgical wound closure, developed using medical-grade cyanoacrylate formulations that provide rapid bonding, reduced infection risk, and improved wound healing outcomes in emergency care and surgical applications

- In September 2025, Advanced Medical Solutions Group plc announced the expansion of its LiquiBand topical skin adhesive portfolio, introducing improved formulations designed for faster polymerization and stronger adhesion for use in minimally invasive surgical procedures and emergency wound management

- In November 2025, Chemence Medical announced the development of a next-generation cyanoacrylate-based topical skin adhesive platform designed to enhance wound closure strength and antimicrobial protection, supporting growing demand for advanced wound care solutions and alternatives to sutures and staples in surgical procedure

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.