Us China Europe Surgical Visualization Systems Market

Market Size in USD Million

CAGR :

%

USD

1.00 Million

USD

2.32 Million

2025

2033

USD

1.00 Million

USD

2.32 Million

2025

2033

| 2026 –2033 | |

| USD 1.00 Million | |

| USD 2.32 Million | |

| % | |

|

Europe Surgical Visualization Systems Market Size

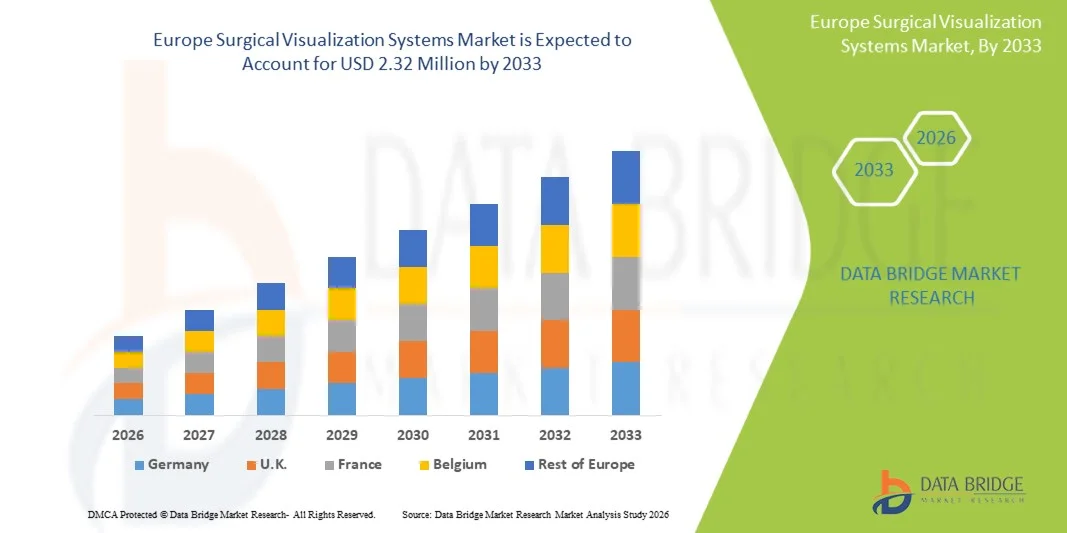

- The Europe Surgical Visualization Systems Market size was valued at USD 1.00 Million in 2025and is expected to reach USD 2.32 Million by 2033, at a CAGR of 11.10% during the forecast period

- The market growth is largely fueled by the increasing adoption of minimally invasive and image-guided surgical procedures, along with rapid advancements in high-definition imaging technologies, 3D visualization, and augmented reality, leading to improved surgical precision and clinical outcomes across healthcare settings

- Furthermore, rising demand for enhanced surgical accuracy, growing preference for real-time intraoperative imaging, and continuous technological innovation in endoscopic and robotic-assisted surgeries are establishing surgical visualization systems as essential tools in modern operating rooms. These converging factors are accelerating the uptake of Surgical Visualization Systems solutions, thereby significantly boosting the industry's growth

Europe Surgical Visualization Systems Market Analysis

- Surgical visualization systems, including endoscopic imaging systems, 3D visualization platforms, and advanced surgical microscopes, are increasingly vital components of modern operating rooms due to their ability to enhance surgical precision, improve visualization of anatomical structures, and support minimally invasive procedures

- The escalating demand for surgical visualization systems is primarily fueled by the rising adoption of minimally invasive and robotic-assisted surgeries, increasing prevalence of chronic diseases requiring surgical intervention, and continuous advancements in high-definition imaging and augmented reality technologies

- K. dominated the Europe Surgical Visualization Systems Market with the largest revenue share of 39.6% in 2025, driven by strong healthcare infrastructure, early adoption of advanced surgical technologies, and significant investments in digital operating rooms, with widespread deployment across NHS hospitals supporting advanced surgical procedures

- Germany is expected to be the fastest growing region in the Europe Surgical Visualization Systems Market during the forecast period due to rapid technological innovation in medical imaging, increasing hospital investments in advanced surgical equipment, and strong focus on precision surgery and healthcare digitization

- The laparoscopy segment accounted for the largest market revenue share of 31.4% in 2025, driven by the increasing global adoption of minimally invasive abdominal surgeries

Report Scope and Europe Surgical Visualization Systems Market Segmentation

|

Attributes |

Surgical Visualization Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe |

|

Key Market Players |

· Medtronic plc (Ireland) · Stryker Corporation (U.S.) · Johnson & Johnson (U.S.) · Smith+Nephew plc (U.K.) · Karl Storz SE & Co. KG (Germany) · Olympus Corporation (Japan) · CONMED Corporation (U.S.) · B. Braun Melsungen AG (Germany) · Danaher Corporation (Leica Microsystems) (U.S.) · Brainlab AG (Germany) · ZEISS Group (Germany) · Stryker Leibinger (Germany) · Richard Wolf GmbH (Germany) · Arthrex, Inc. (U.S.) · Medtronic Surgical Technologies (U.S.) · Alcon Inc. (Switzerland) · Fujifilm Holdings Corporation (Japan) · Hoya Corporation (Japan) · SonoScape Medical Corp. (China) · Mindray Medical International Limited (China) |

|

Market Opportunities |

· Rising adoption of minimally invasive and robotic-assisted surgeries · Rising Demand in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Surgical Visualization Systems Market Trends

“Advancements in 3D Imaging, 4K Visualization, and AR-Assisted Surgery”

- A significant and accelerating trend in the Europe Surgical Visualization Systems Market is the rapid adoption of high-definition imaging technologies such as 4K, 3D, and augmented reality (AR)-assisted visualization systems that enhance surgical precision and clinical outcomes

- For instance, systems developed by Carl Zeiss Meditec AG provide high-resolution intraoperative imaging platforms that enable surgeons to visualize complex anatomical structures with greater accuracy during minimally invasive procedures

- These advanced visualization tools are improving depth perception, reducing surgical errors, and enabling better decision-making during complex surgeries

- Furthermore, integration of AR overlays is allowing surgeons to visualize real-time anatomical guidance directly on surgical fields, improving procedural efficiency

- The increasing use of minimally invasive and robotic-assisted surgeries is further driving demand for advanced visualization systems in hospitals and surgical centers

- This technological evolution is significantly enhancing surgical precision and transforming operating room workflows across Europe

Europe Surgical Visualization Systems Market Dynamics

Driver

“Rising Demand for Minimally Invasive Surgeries and Growing Surgical Volumes”

- The increasing preference for minimally invasive surgical procedures is a key driver for the growth of the Europe Surgical Visualization Systems Market in Europe

- For instance, the rising number of laparoscopic and endoscopic procedures in countries such as Germany, France, and the UK is significantly boosting demand for high-quality visualization systems in operating rooms

- These procedures require advanced imaging systems that provide clear, magnified, and real-time visuals to ensure surgical accuracy and patient safety

- In addition, the growing prevalence of chronic diseases such as cancer, cardiovascular disorders, and gastrointestinal conditions is increasing surgical intervention rates

- Expansion of hospital infrastructure and investments in modern operating rooms are further supporting market growth

- Moreover, increasing adoption of robotic-assisted surgeries is strengthening the need for integrated visualization platforms in surgical environments

Restraint/Challenge

“High Cost of Advanced Visualization Systems and Limited Adoption in Smaller Healthcare Facilities”

- One of the major challenges in the Europe Surgical Visualization Systems Market is the high cost associated with advanced imaging equipment, including 3D and 4K visualization systems

- For instance, premium surgical visualization platforms require significant capital investment, which can be a limiting factor for smaller hospitals and clinics with constrained budgets

- In addition, the need for regular maintenance, software upgrades, and specialized training adds to the overall operational cost burden

- Limited availability of skilled professionals trained in advanced visualization technologies also restricts widespread adoption

- Variability in healthcare reimbursement policies across European countries further impacts purchasing decisions for high-end surgical systems

- Addressing these challenges through cost-effective innovations, leasing models, and enhanced training programs will be essential for broader market penetration and sustained growth

Europe Surgical Visualization Systems Market Scope

The market is segmented on the basis of product type, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the Europe Surgical Visualization Systems Market is segmented into endoscopic cameras, accessories, light sources, display & monitors, video recorders & processors, camera heads, and video converters. The endoscopic camera segment dominated the largest market revenue share of 28.9% in 2025, driven by its critical role in providing high-resolution visualization during minimally invasive surgeries. Rising adoption of laparoscopic and endoscopic procedures across specialties significantly supports demand. Technological advancements such as 4K and 3D imaging capabilities enhance surgical precision and outcomes. Increasing prevalence of chronic diseases requiring surgical intervention further drives segment growth. Hospitals and surgical centers increasingly prefer advanced camera systems for better diagnostics and intraoperative visualization. Growing investments in operating room modernization also support adoption. The integration of AI-enabled imaging and real-time visualization tools further strengthens demand. Rising geriatric population globally contributes to higher surgical volumes. Expansion of minimally invasive surgery techniques continues to boost this segment.

The display & monitors segment is expected to witness the fastest CAGR of 11.8% from 2026 to 2033, driven by increasing demand for high-definition visualization in operating rooms. Surgeons require large, high-resolution displays for better accuracy during complex procedures. Adoption of 4K and 8K surgical monitors is rising rapidly across advanced healthcare facilities. Integration with imaging systems and surgical navigation platforms enhances usability. Growing investments in hybrid operating rooms further support demand. Technological advancements in OLED and LED displays improve image clarity and color accuracy. Increasing number of minimally invasive surgeries boosts requirement for advanced visualization. Rising hospital infrastructure upgrades in emerging economies also contribute to growth.

- By Application

On the basis of application, the market is segmented into arthroscopy, laparoscopy, ENT endoscopy, obstetrics/gynecology endoscopy, urology endoscopy, gastroscopy, and others. The laparoscopy segment accounted for the largest market revenue share of 31.4% in 2025, driven by the increasing global adoption of minimally invasive abdominal surgeries. Laparoscopic procedures offer benefits such as reduced hospital stay, faster recovery, and lower infection risk. Rising prevalence of gallbladder diseases, hernia, and gastrointestinal disorders supports segment dominance. Technological advancements in visualization systems enhance surgical accuracy. Growing preference for minimally invasive procedures among patients and surgeons further drives demand. Increasing healthcare expenditure and surgical volumes globally contribute significantly. Expansion of ambulatory surgical centers also supports adoption. Continuous innovation in laparoscopic instruments strengthens market growth.

The urology endoscopy segment is expected to witness the fastest CAGR of 12.6% from 2026 to 2033, driven by increasing incidence of kidney stones, prostate disorders, and urinary tract diseases. Rising aging population significantly contributes to demand for urological procedures. Technological advancements in endoscopic imaging improve diagnostic accuracy and treatment outcomes. Growing adoption of minimally invasive urology surgeries boosts segment expansion. Increasing awareness of early diagnosis and treatment further supports growth. Expanding healthcare infrastructure in developing regions enhances accessibility. Surgeons are increasingly adopting advanced visualization systems for precision procedures. Rising outpatient urology procedures also contribute to demand.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, diagnostic imaging centers, ambulatory surgical centers, and others. The hospitals segment dominated the largest market revenue share of 57.6% in 2025, driven by high patient inflow, availability of advanced surgical infrastructure, and skilled healthcare professionals. Hospitals perform the majority of complex surgical procedures requiring advanced visualization systems. Increasing investments in hybrid operating rooms and digital surgery suites support dominance. Rising adoption of minimally invasive surgeries further strengthens demand. Hospitals also benefit from strong procurement budgets and reimbursement systems. Continuous technological upgrades enhance surgical efficiency and outcomes. Growing global healthcare expenditure contributes to segment expansion. Increasing prevalence of chronic diseases requiring surgical intervention also supports growth.

The ambulatory surgical centers segment is expected to witness the fastest CAGR of 13.2% from 2026 to 2033, driven by the growing shift toward outpatient surgical procedures. These centers offer cost-effective and efficient surgical care with shorter recovery times. Rising demand for same-day surgeries supports adoption of visualization systems. Increasing preference for minimally invasive procedures boosts growth. Expansion of healthcare infrastructure in urban regions further supports segment development. Technological advancements in compact and portable visualization systems enhance usability. Growing patient preference for outpatient care also drives demand. Rising healthcare privatization in emerging economies accelerates expansion.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and third-party distributors. The direct tender segment held the largest market revenue share of 64.3% in 2025, driven by large-scale procurement by hospitals and government healthcare institutions. Direct tendering ensures cost efficiency, standardized procurement, and long-term supplier agreements. Increasing government investments in healthcare infrastructure support dominance. Hospitals prefer direct procurement for high-value surgical systems to ensure quality assurance. Bulk purchasing for public healthcare systems further strengthens this segment. Strong manufacturer-institution relationships also contribute to growth. Regulatory compliance requirements favor structured procurement channels.

The third-party distributor segment is expected to witness the fastest CAGR of 10.9% from 2026 to 2033, driven by increasing demand from smaller healthcare facilities and private clinics. Distributors help expand market reach in emerging and remote regions. They provide logistics support, installation services, and after-sales assistance. Rising healthcare access in developing economies supports segment expansion. Growing number of specialty clinics and ambulatory centers further boosts demand. Distributors enable faster product availability and flexibility. Increasing manufacturer reliance on channel partners accelerates growth.

Europe Surgical Visualization Systems Market Regional Analysis

- The Europe Surgical Visualization Systems Market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing demand for minimally invasive surgical procedures, rising adoption of advanced imaging technologies, and continuous modernization of operating rooms across hospitals

- Growing emphasis on surgical precision, improved patient outcomes, and integration of high-definition visualization systems with robotic-assisted surgical platforms are further supporting market expansion

- In addition, increasing healthcare digitization and investments in smart operating theaters are strengthening the adoption of surgical visualization systems across the region

U.K. Europe Surgical Visualization Systems Market Insight

The U.K. Europe Surgical Visualization Systems Market captured the largest revenue share of 39.6% in 2025 within Europe, supported by strong healthcare infrastructure, early adoption of advanced surgical technologies, and significant investments in digital operating rooms. The widespread deployment of high-resolution imaging systems across NHS hospitals, along with increasing use of laparoscopic and robotic-assisted surgeries, is driving strong demand for surgical visualization solutions. Continuous focus on improving surgical efficiency and patient safety is further reinforcing market growth in the country.

Germany Europe Surgical Visualization Systems Market Insight

The Germany Europe Surgical Visualization Systems Market is expected to be the fastest growing in Europe during the forecast period, driven by rapid advancements in medical imaging technologies, increasing investments in hospital infrastructure, and strong focus on precision and image-guided surgeries. Germany’s emphasis on healthcare innovation and digital transformation of surgical suites is accelerating the adoption of advanced visualization platforms. Growing preference for minimally invasive procedures and integration of AI-enabled imaging solutions are further contributing to market expansion.

Europe Surgical Visualization Systems Market Share

The Surgical Visualization Systems industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- Stryker Corporation (U.S.)

- Johnson & Johnson (U.S.)

- Smith+Nephew plc (U.K.)

- Karl Storz SE & Co. KG (Germany)

- Olympus Corporation (Japan)

- CONMED Corporation (U.S.)

- Braun Melsungen AG (Germany)

- Danaher Corporation (Leica Microsystems) (U.S.)

- Brainlab AG (Germany)

- ZEISS Group (Germany)

- Stryker Leibinger (Germany)

- Richard Wolf GmbH (Germany)

- Arthrex, Inc. (U.S.)

- Medtronic Surgical Technologies (U.S.)

- Alcon Inc. (Switzerland)

- Fujifilm Holdings Corporation (Japan)

- Hoya Corporation (Japan)

- SonoScape Medical Corp. (China)

- Mindray Medical International Limited (China)

Latest Developments in Europe Surgical Visualization Systems Market

- In March 2021, Stryker Corporation advanced its surgical visualization portfolio through continued global expansion of its 1688 4K Imaging Platform, supporting high-definition visualization for minimally invasive and open surgeries and improving intraoperative precision in operating rooms

- In May 2021, Karl Storz strengthened its surgical visualization systems lineup with expanded deployment of 4K and 3D endoscopic visualization technologies, supporting improved depth perception and image clarity in laparoscopic and robotic-assisted surgeries

- In December 2021, ClaroNav received regulatory clearance in Canada for its Navient surgical navigation and visualization system, designed to enhance real-time imaging guidance and improve surgical accuracy in ENT and cranial procedures

- In May 2022, Olympus Corporation received FDA clearance for its EZ1500 series endoscopes, incorporating extended depth-of-field imaging technology to enhance surgical visualization precision during minimally invasive procedures

- In July 2023, Fujifilm Holdings expanded its surgical visualization portfolio with enhanced endoscopic imaging systems designed for minimally invasive surgery, strengthening adoption of high-definition visualization platforms in global operating rooms

- In September 2024, Stryker Corporation launched an advanced surgical visualization camera system in India, designed to improve image clarity, color accuracy, and real-time visualization for complex surgical procedures

- In May 2025, Olympus Corporation announced FDA 510(k) clearance for its EZ1500 endoscope series, featuring Extended Depth of Field (EDOF) technology to improve visualization depth and diagnostic accuracy during surgical procedures

- In May 2025, EIZO Corporation launched its CuratOR SC431 surgical camera system, offering high-performance imaging and enhanced visualization capabilities for operating room environments

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.