Global Sjgrens Syndrome Market

Размер рынка в млрд долларов США

CAGR :

%

USD

220.26 Million

USD

313.23 Million

2025

2033

USD

220.26 Million

USD

313.23 Million

2025

2033

| 2026 –2033 | |

| USD 220.26 Million | |

| USD 313.23 Million | |

| % | |

|

Global Sjögren’s Syndrome Market Segmentation, By Type (Primary Sjögren’s Syndrome and Secondary Sjögren’s Syndrome), Symptoms (Dry Eyes, Dry Mouth, and Others), Diagnosis (Blood Tests, Eye Tests, Lip Biopsy, and Others), Treatment (Medication, Surgery, and Others), Drugs (Salagen, Evoxac, Plaquenil, and Others), End Users (Hospitals, Homecare, Specialty Clinics, and Others), Distribution Channel (Hospital Pharmacy, Online Pharmacy, Retail Pharmacy, and Others)- Industry Trends and Forecast to 2033

Sjögren’s Syndrome Market Size

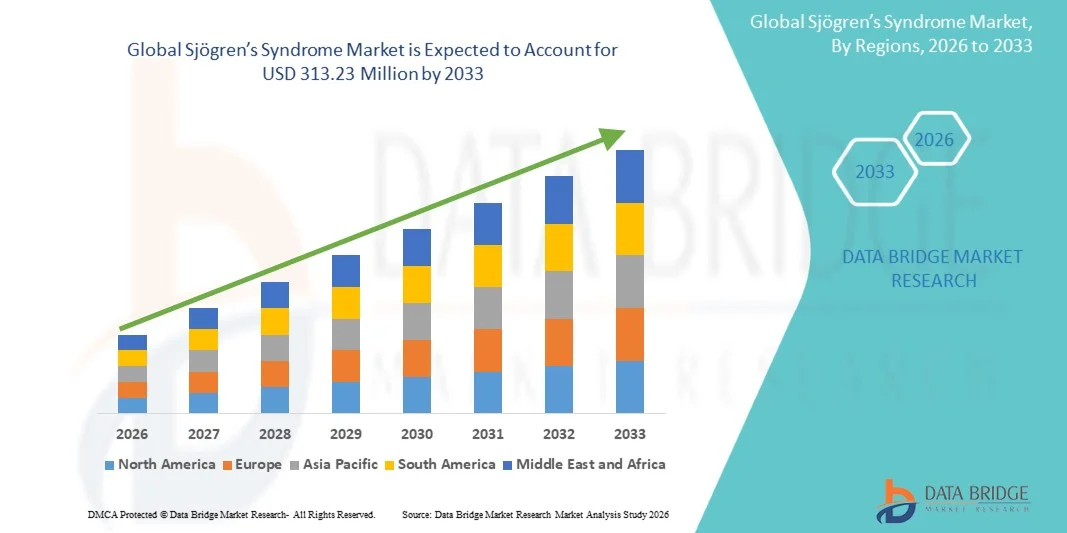

- The global Sjögren’s Syndrome market size was valued at USD 220.26 million in 2025 and is expected to reach USD 313.23 million by 2033, at a CAGR of 4.50% during the forecast period

- The market growth is largely driven by increasing prevalence of autoimmune disorders, rising awareness and improved diagnostic rates, and advancements in targeted therapies and immunomodulatory treatments that improve patient outcomes

- Furthermore, expanding R&D efforts, growing investment in novel biologics and immunotherapies, and enhanced healthcare infrastructure globally are encouraging better disease management approaches boosting adoption of Sjögren’s Syndrome therapies and expanding market opportunities across key regions

Sjögren’s Syndrome Market Analysis

- Sjögren’s Syndrome, a chronic autoimmune disorder primarily affecting exocrine glands and causing dry eyes and dry mouth, is increasingly vital in healthcare due to its impact on patient quality of life and potential systemic complications

- The escalating demand for Sjögren’s Syndrome therapies is primarily fueled by the rising prevalence of autoimmune diseases, growing patient awareness, improved diagnostic capabilities, and advancements in targeted medications and biologics that manage symptoms and systemic manifestations

- North America dominated the Sjögren’s Syndrome market with the largest revenue share of 39.5% in 2025, characterized by advanced healthcare infrastructure, high patient awareness, and a strong presence of key pharmaceutical and biotech players, with the U.S. experiencing substantial growth in therapy adoption, particularly in Primary Sjögren’s Syndrome cases, driven by innovations in drugs such as Salagen, Evoxac, and Plaquenil

- Asia-Pacific is expected to be the fastest-growing region in the Sjögren’s Syndrome market during the forecast period due to increasing healthcare access, rising disposable incomes, expanding awareness programs, and the growing prevalence of autoimmune disorders in countries such as China and India

- Primary Sjögren’s Syndrome dominated the market with a 65.4% share in 2025, driven by higher prevalence compared to secondary forms, increasing patient awareness, and the growing adoption of targeted therapies that effectively manage its symptoms and systemic complications

Report Scope and Sjögren’s Syndrome Market Segmentation

|

Attributes |

Sjögren’s Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Sjögren’s Syndrome Market Trends

“Rising Adoption of Targeted Biologics and Immunotherapies”

- A significant and accelerating trend in the global Sjögren’s Syndrome market is the increasing adoption of targeted biologics and immunotherapies that focus on managing systemic manifestations and improving patient outcomes

- For instance, the biologic drug Belimumab has shown promise in clinical studies for reducing disease activity in patients with systemic involvement, leading to growing physician preference for such therapies

- Advanced therapies enable better symptom control and improved quality of life, including reductions in fatigue, dry eyes, and dry mouth, which are the most common complaints among patients

- The seamless integration of these therapies into established treatment protocols allows clinicians to offer more personalized and effective management of Sjögren’s Syndrome, reducing complications and hospitalizations

- This trend towards more precise, patient-centric treatment approaches is fundamentally reshaping physician expectations and treatment standards. Consequently, pharmaceutical companies are focusing on developing next-generation biologics with improved efficacy and safety profiles

- The demand for therapies that provide systemic relief and targeted immunomodulation is growing rapidly across both developed and emerging markets, as patients increasingly prioritize comprehensive disease management

- Telemedicine and digital health platforms are emerging as important enablers for disease monitoring, patient education, and therapy adherence, driving broader adoption of treatment solutions

Sjögren’s Syndrome Market Dynamics

Driver

“Increasing Prevalence of Autoimmune Disorders and Awareness”

- The rising prevalence of autoimmune disorders worldwide, coupled with increasing patient and physician awareness, is a significant driver for the heightened demand for Sjögren’s Syndrome therapies

- For instance, in 2025, multiple awareness campaigns and clinical trial expansions in the U.S. and Europe helped identify previously undiagnosed cases, thereby increasing therapy adoption rates

- As patients and healthcare providers become more aware of the disease, early diagnosis and treatment adoption improve, reducing complications and enhancing long-term outcomes

- Furthermore, increasing investment in R&D for targeted therapies and biologics is making treatment more effective, safe, and accessible to patients across different age groups

- The growing preference for personalized medicine and therapies that address both symptoms and systemic effects are key factors propelling market expansion in North America and Europe, as well as emerging growth in Asia-Pacific

- Rising government initiatives and funding to support autoimmune disease research and patient assistance programs are creating additional growth opportunities

- Expansion of diagnostic centers and specialized autoimmune clinics is improving accessibility to treatment, driving higher therapy adoption in underserved region

Restraint/Challenge

“Limited Awareness, High Cost, and Diagnostic Complexity”

- Limited awareness of Sjögren’s Syndrome among general practitioners and patients, along with the complex nature of its diagnosis, poses a significant challenge to broader market penetration

- For instance, the reliance on multiple diagnostic procedures such as blood tests, eye tests, and lip biopsies can delay diagnosis, affecting early treatment adoption and patient outcomes

- Addressing these challenges through educational initiatives, improved screening protocols, and simplified diagnostic methods is crucial for expanding therapy adoption and market growth

- In addition, the high cost of biologics and advanced therapies compared to conventional symptomatic treatments can limit access, especially in developing regions or among price-sensitive patients

- Overcoming these challenges through patient education, insurance coverage improvements, and development of cost-effective therapeutic options will be vital for sustained growth in the Sjögren’s Syndrome market

- Variability in treatment guidelines across regions and limited standardization of care may hinder consistent therapy adoption and clinical outcomes

- Patient non-adherence due to complex treatment regimens or perceived side effects remains a challenge, requiring enhanced support programs and simplified treatment protocols

Sjögren’s Syndrome Market Scope

The market is segmented on the basis of type, symptoms, diagnosis, treatment, drugs, end users, and distribution channels.

- By Type

On the basis of type, the Sjögren’s Syndrome market is segmented into Primary Sjögren’s Syndrome and Secondary Sjögren’s Syndrome. The Primary Sjögren’s Syndrome segment dominated the market with the largest revenue share of 65.4% in 2025, driven by its higher prevalence compared to secondary forms. Patients with primary Sjögren’s often require long-term management of both systemic and localized symptoms, which increases therapy adoption. The availability of targeted biologics and immunomodulatory medications further supports market dominance. In addition, awareness campaigns and improved diagnostic tools in developed regions have facilitated early detection, driving treatment uptake. Physicians also prefer treating primary cases due to their well-defined symptomatology and established treatment protocols. The dominance of this segment reflects both higher patient population and consistent therapy adoption across geographies.

Secondary Sjögren’s Syndrome is anticipated to witness the fastest growth rate from 2026 to 2033 due to increasing autoimmune comorbidities, particularly in patients with lupus and rheumatoid arthritis. Growing research on the interaction between primary autoimmune disorders and secondary Sjögren’s is driving early diagnosis and treatment. The adoption of combination therapies targeting multiple autoimmune pathways is increasing in emerging markets. Improved awareness among rheumatologists and the launch of new supportive therapies contribute to faster adoption. Expanding healthcare infrastructure in Asia-Pacific and Latin America also supports growth. Patient preference for symptom-specific medications further accelerates this segment’s expansion.

- By Symptoms

On the basis of symptoms, the market is segmented into dry eyes, dry mouth, and others. The Dry Eyes segment dominated the market with a share of 45% in 2025, driven by its high prevalence and impact on daily life. Patients with dry eyes often seek medical attention early, leading to higher adoption of therapies such as artificial tears, topical immunomodulators, and biologics. Healthcare providers focus on symptom management to prevent complications such as corneal damage, increasing treatment frequency. Advances in ophthalmologic diagnostics, including tear film imaging, aid early intervention. Pharmaceutical companies actively target this symptom with new drug formulations, reinforcing market dominance. The widespread availability of OTC and prescription solutions makes dry eyes a central driver of therapy adoption.

The Dry Mouth segment is expected to witness the fastest growth due to rising awareness of oral complications and increasing availability of salivary substitutes and secretagogues. Growing demand for medications such as Salagen and Evoxac is fueling adoption. Increasing research on the link between oral dryness and systemic autoimmune activity is prompting physicians to treat early. The expansion of dental clinics integrated with autoimmune care is further boosting the segment. Patient education on oral health and adherence programs also enhance uptake. Emerging markets are witnessing rapid growth in dry mouth treatments due to increasing healthcare access.

- By Diagnosis

On the basis of diagnosis, the market is segmented into blood tests, eye tests, lip biopsy, and others. The Blood Tests segment dominated the market with a share of 40% in 2025, as it provides a simple, non-invasive method for detecting antibodies associated with Sjögren’s Syndrome. Blood tests allow for early screening, supporting faster treatment initiation and improved patient outcomes. Widespread availability and relatively low cost make them accessible across both developed and emerging markets. Blood tests are often combined with other diagnostic methods, increasing their clinical relevance. Advancements in biomarker detection improve diagnostic accuracy, supporting market leadership. Physicians increasingly rely on these tests for monitoring disease progression and therapy response, reinforcing adoption.

The Eye Tests segment is expected to witness the fastest growth due to increasing use of ophthalmologic diagnostics, including Schirmer’s test and tear film analysis. Rising awareness of ocular complications is driving early detection. Clinics are integrating eye tests with telemedicine platforms for remote monitoring. New automated diagnostic tools enhance efficiency and accuracy, boosting patient and physician adoption. Expanding healthcare infrastructure in Asia-Pacific supports faster growth. Patient preference for early symptom monitoring further accelerates adoption.

- By Treatment

On the basis of treatment, the market is segmented into Medication, surgery, and others. The Medication segment dominated the market with 75% share in 2025, driven by the high adoption of symptomatic and systemic therapies including biologics, secretagogues, and immunomodulators. Medications provide non-invasive, effective management of both dry eyes and dry mouth, supporting consistent use. The availability of multiple branded and generic options enhances accessibility. Patients and physicians often prefer pharmacological intervention before considering invasive treatments. Continued R&D in drug development ensures introduction of new therapies. Medications’ dominance is also fueled by growing insurance coverage and reimbursement programs in developed regions.

The Surgery segment is anticipated to witness the fastest growth due to increasing awareness of advanced interventions for severe ocular and salivary complications. Procedures such as salivary duct surgeries and punctal plugs are gaining adoption in specialized clinics. Rising collaborations between hospitals and research institutes promote surgical advancements. Patient preference for long-term symptom relief drives adoption. Increasing number of specialty clinics in emerging markets supports growth. Technological improvements in minimally invasive procedures enhance acceptance.

- By Drugs

On the basis of drugs, the market is segmented into Salagen, Evoxac, Plaquenil, and Others. The Salagen segment dominated the market with 30% share in 2025, driven by its established efficacy in stimulating saliva production and managing dry mouth symptoms. Salagen has long-standing clinical acceptance and availability across major markets. Physicians often prescribe Salagen as a first-line therapy due to its proven safety profile. Patient familiarity and adherence programs enhance its market share. The drug’s inclusion in treatment guidelines reinforces usage. Continued investment in marketing and awareness campaigns strengthens its dominance.

The Evoxac segment is expected to witness the fastest growth due to increasing adoption in newly diagnosed patients and rising awareness of oral health management. Evoxac’s role in improving quality of life and reducing oral complications supports faster uptake. Expanding availability in emerging markets contributes to growth. Physicians are increasingly recommending Evoxac for patients who cannot tolerate other secretagogues. Combination therapies including Evoxac are also gaining traction. Clinical research highlighting systemic benefits further drives adoption.

- By End Users

On the basis of end users, the market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment dominated the market with 50% share in 2025, driven by the availability of multidisciplinary care, access to advanced therapies, and integrated diagnostic services. Hospitals serve as referral centers for complex cases, ensuring higher therapy adoption. Physicians in hospitals have greater access to biologics and clinical trials, further boosting patient treatment uptake. Insurance coverage for hospital-based treatments enhances accessibility. Hospitals also provide patient education programs, improving adherence. The presence of specialized autoimmune units reinforces hospital dominance.

The Specialty Clinics segment is expected to witness the fastest growth due to increasing establishment of clinics focused on autoimmune diseases. These clinics offer personalized care, early diagnosis, and adoption of targeted therapies. Collaboration with hospitals and research institutes improves treatment offerings. Patient preference for focused care drives faster growth. Expansion in urban and semi-urban regions accelerates adoption. Increasing awareness programs and telemedicine support further enhance growth prospects.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, retail pharmacy, and others. The Hospital Pharmacy segment dominated the market with 45% share in 2025, driven by the direct availability of prescribed medications and biologics in hospitals. Patients prefer hospital pharmacies due to the reliability of drug authenticity and integration with clinical care. Hospital pharmacies also provide patient counseling and adherence monitoring. High-value drugs such as biologics are primarily distributed through hospital pharmacies. Insurance reimbursement schemes further support this channel. Physicians often guide patients to hospital pharmacies, ensuring dominance.

The Online Pharmacy segment is expected to witness the fastest growth due to the rising trend of e-commerce in pharmaceuticals and home delivery of medications. Convenience, accessibility in remote areas, and competitive pricing drive adoption. Telemedicine consultations paired with online pharmacies enhance patient reach. Expanding internet penetration in emerging markets fuels growth. Online pharmacies also offer subscription-based medication services, ensuring consistent therapy. Awareness campaigns on digital healthcare adoption further support rapid growth.

Sjögren’s Syndrome Market Regional Analysis

- North America dominated the Sjögren’s Syndrome market with the largest revenue share of 39.5% in 2025, characterized by advanced healthcare infrastructure, high patient awareness, and a strong presence of key pharmaceutical and biotech players

- Patients and healthcare providers in the region highly value early diagnosis, access to biologics and immunomodulatory medications, and comprehensive care through hospitals and specialty clinics

- This widespread adoption is further supported by strong R&D presence, government funding for autoimmune disease awareness, and insurance coverage for treatments, establishing North America as a leading market for both primary and secondary Sjögren’s Syndrome therapies

U.S. Sjögren’s Syndrome Market Insight

The U.S. Sjögren’s Syndrome market captured the largest revenue share of 82% in North America in 2025, fueled by the widespread adoption of advanced biologics and immunomodulatory therapies. Patients and healthcare providers increasingly prioritize early diagnosis and effective management of systemic and localized symptoms. The growing availability of specialty clinics, autoimmune centers, and telemedicine platforms further propels market growth. Moreover, high patient awareness campaigns and insurance coverage for therapies significantly contribute to treatment adoption. The trend toward personalized medicine and targeted therapies continues to drive demand for effective and safe treatment options.

Europe Sjögren’s Syndrome Market Insight

The Europe Sjögren’s Syndrome market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by growing awareness of autoimmune disorders and increasing access to healthcare facilities. Rising patient education initiatives and government funding for autoimmune research are fostering adoption of diagnostic and treatment services. European patients are also drawn to the availability of advanced biologics and oral secretagogues for symptom management. The market is witnessing significant growth across hospitals, specialty clinics, and homecare segments, with therapies being incorporated into both newly diagnosed and chronic patient care. Access to multi-disciplinary treatment approaches enhances patient outcomes and reinforces therapy adoption.

U.K. Sjögren’s Syndrome Market Insight

The U.K. Sjögren’s Syndrome market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increased patient awareness and the rising prevalence of autoimmune comorbidities. In addition, early diagnosis programs and availability of targeted therapies are encouraging healthcare providers to adopt biologics and immunomodulatory medications. The U.K.’s focus on integrated care, including specialty clinics and hospital-based autoimmune units, is expected to continue to stimulate market growth. Patient education programs and telehealth adoption further improve treatment adherence. The growing preference for personalized therapy plans is boosting adoption in both primary and secondary Sjögren’s Syndrome cases.

Germany Sjögren’s Syndrome Market Insight

The Germany Sjögren’s Syndrome market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of autoimmune disorders and the demand for advanced diagnostic and therapeutic solutions. Germany’s well-developed healthcare infrastructure, coupled with strong clinical research initiatives, promotes adoption of biologics and supportive treatments. Integration of treatment protocols with specialty autoimmune centers is becoming increasingly prevalent, with a strong preference for evidence-based, patient-centric care. In addition, government-led awareness programs and early diagnosis initiatives align with local patient expectations. The availability of insurance coverage and reimbursement for biologics further enhances market growth.

Asia-Pacific Sjögren’s Syndrome Market Insight

The Asia-Pacific Sjögren’s Syndrome market is poised to grow at the fastest CAGR of 25% during 2026–2033, driven by increasing healthcare access, rising disposable incomes, and growing awareness of autoimmune disorders in countries such as China, Japan, and India. The region's expanding network of specialty clinics and hospitals is supporting early diagnosis and treatment adoption. Furthermore, emerging biologics and affordable medications are improving accessibility to therapies. Government initiatives promoting healthcare modernization and digital health solutions are also accelerating market growth. Increased patient education and expansion of telemedicine platforms further drive adoption across urban and semi-urban regions.

Japan Sjögren’s Syndrome Market Insight

The Japan Sjögren’s Syndrome market is gaining momentum due to the country’s high awareness of autoimmune diseases, advanced healthcare infrastructure, and preference for early treatment intervention. Adoption is driven by the increasing number of specialty autoimmune clinics and hospital-based diagnostic centers. The integration of telemedicine and digital health platforms enhances monitoring and therapy adherence. Moreover, Japan’s aging population is likely to spur demand for safer, more accessible treatment options. The growing emphasis on quality of life and systemic symptom management is also supporting growth in both residential and clinical care settings.

India Sjögren’s Syndrome Market Insight

The India Sjögren’s Syndrome market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s expanding healthcare access, rising awareness of autoimmune disorders, and increasing adoption of advanced medications. India is witnessing a growing number of specialty clinics and hospitals providing targeted therapies for systemic and localized symptoms. The push toward digital health solutions and telemedicine platforms, along with increasing patient education initiatives, are key factors propelling the market. Affordability of medications and emerging domestic pharmaceutical players further support therapy adoption. Rapid urbanization and increasing disposable incomes enhance access to diagnostics and biologics, driving overall market growth

Sjögren’s Syndrome Market Share

The Sjögren’s Syndrome industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Johnson & Johnson Services, Inc. (U.S.)

- Bristol Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Biogen Inc. (U.S.)

- Sanofi (France)

- GSK plc (U.K.)

- Daiichi Sankyo Co., Ltd. (Japan)

- Amgen Inc. (U.S.)

- Pfizer Inc. (U.S.)

- AstraZeneca (U.K.)

- Takeda Pharmaceutical Company Limited (Japan)

- Otsuka Holdings Co., Ltd. (Japan)

- Hikma Pharmaceuticals plc (U.K.)

- ADVANZ PHARMA Corp. (U.K.)

- Resolve Therapeutics, LLC (U.S.)

- Sylentis, S.A. (Spain)

- Santen Pharmaceutical Co., Ltd. (Japan)

- TearSolutions Inc. (U.S.)

What are the Recent Developments in Global Sjögren’s Syndrome Market?

- In October 2025, telitacicept demonstrated clinically meaningful efficacy in a Phase III clinical trial for primary Sjögren’s syndrome, meeting its primary endpoint by significantly improving disease activity scores in patients and supporting plans for regulatory submissions and further global development of this BLyS/APRIL dual‑target therapy

- In August 2025, Novartis announced that both Phase III clinical trials of ianalumab met their primary endpoint in patients with Sjögren’s disease, demonstrating statistically significant reduction in disease activity and positioning ianalumab to potentially become the first targeted treatment for this autoimmune condition pending regulatory submission

- In July 2025, the U.S. National Institutes of Health (NIH) released its first‑ever NIH‑Wide Strategic Plan for Autoimmune Disease Research, establishing a coordinated federal blueprint to accelerate discovery, improve diagnostics and treatments, and enhance disease understanding across autoimmune diseases including Sjögren’s, marking a pivotal long‑term research commitment for the condition

- In June 2025, argenx presented new data at EULAR 2025 showing positive outcomes for efgartigimod in Sjögren’s disease, highlighting encouraging Phase 2 results and supporting ongoing development of this FcRn‑blocking therapy as a precision approach to treating underlying immunologic drivers of the disease

- In March 2025, Johnson & Johnson’s investigational therapy nipocalimab received U.S. FDA Fast Track designation for the treatment of adults with moderate‑to‑severe Sjögren’s disease, building on its prior Breakthrough Therapy designation and aiming to expedite clinical development and regulatory review of this potential treatment option where none currently directly address underlying disease mechanism

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.