Middle East And Africa Disposable Spo2 Sensor Market

Размер рынка в млрд долларов США

CAGR :

%

USD

465.10 Million

USD

1,254.05 Million

2025

2033

USD

465.10 Million

USD

1,254.05 Million

2025

2033

| 2026 –2033 | |

| USD 465.10 Million | |

| USD 1,254.05 Million | |

| % | |

|

Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor Market Segmentation, By Connector (Less Than 6 Pins, 6 Pins-10 Pins and More Than 10 Pins), Usage (Adult, Pediatric, Neonate, Animal and Others), Technique (Reflectance and Transflectance), Signal (Analog and Digital), Application (Finger, Ear, Foot, Toe, Multi Position, and Others), End User (Clinical, Hospital, Veterinary and Others), Sales Channel (Offline and Online)- Industry Trends and Forecast to 2033

Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor Market Size

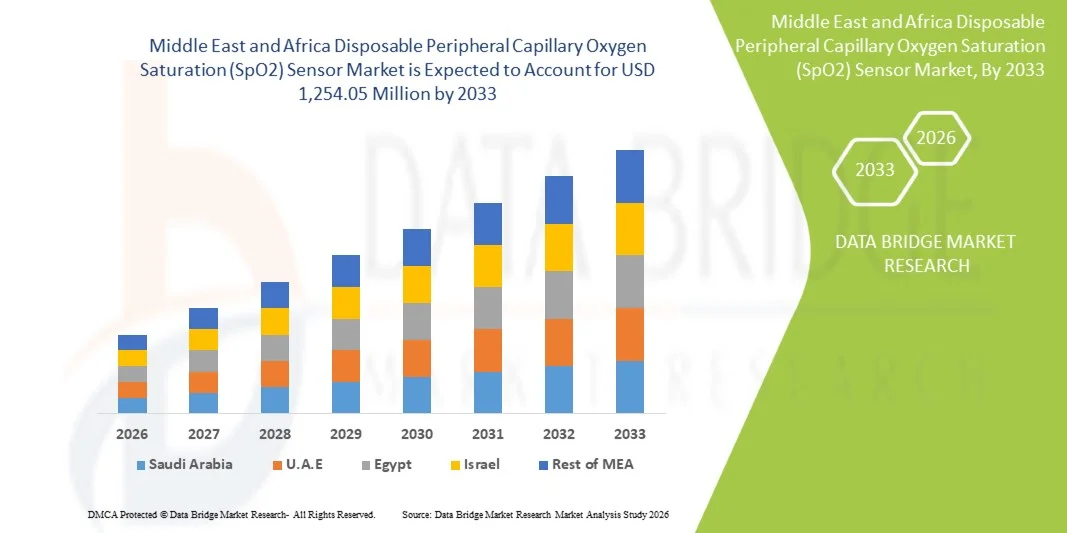

- The Middle East and Africa disposable peripheral capillary oxygen saturation (SpO2) sensor market size was valued at USD 465.10 million in 2025 and is expected to reach USD 1,254.05 million by 2033, at a CAGR of 13.2% during the forecast period

- The market growth is largely driven by the increasing prevalence of respiratory diseases, rising healthcare infrastructure investments, and greater focus on non‑invasive monitoring technologies in the region, which together are enhancing adoption across hospitals and diagnostic centers

- Furthermore, advancements in sensor accuracy and comfort, heightened demand for infection control, and the shift toward continuous patient monitoring solutions are contributing to the expanding uptake of disposable SpO₂ sensors as essential components in respiratory care and patient monitoring ecosystems, thereby supporting significant market growth

Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor Market Analysis

- Disposable peripheral capillary oxygen saturation (SpO₂) sensor market, providing non-invasive monitoring of blood oxygen levels, is increasingly vital in hospitals, clinics, and home care settings due to its ease of use, infection control advantages, and integration with patient monitoring systems

- The escalating demand for the disposable peripheral capillary oxygen saturation (SpO₂) sensor is primarily fueled by the rising prevalence of respiratory diseases, increasing patient safety concerns, and the growing adoption of continuous and real-time monitoring technologies in both clinical and home care environments

- Saudi Arabia dominated the Middle East and Africa disposable peripheral capillary oxygen saturation (SpO₂) sensor market with the largest revenue share in 2025 of 30.7%, supported by significant healthcare infrastructure investments, expansion of intensive care units, and increased access to advanced medical devices, with hospitals and critical care units experiencing substantial adoption driven by government initiatives and private healthcare upgrades

- Nigeria is expected to be the fastest growing country in the Middle East and Africa disposable peripheral capillary oxygen saturation (SpO₂) sensor market during the forecast period due to rising healthcare expenditures, expanding hospital networks, and growing awareness of non-invasive patient monitoring solutions

- The Finger segment dominated the Middle East and Africa disposable peripheral capillary oxygen saturation (SpO₂) sensor market with the largest share of 44.9% in 2025, driven by their portability, ease of use, and established reputation for reliable monitoring across hospitals, clinics, and home care settings

Report Scope and Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor Market Segmentation

|

Attributes |

Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor Market Trends

“Enhanced Convenience Through Non-Invasive and Connected Monitoring”

- A significant and accelerating trend in the Middle East and Africa disposable peripheral capillary oxygen saturation (SpO₂) sensor market is the integration of non-invasive, connected monitoring solutions with hospital and home care systems, enhancing patient convenience, continuous monitoring, and data management

- For instance, fingertip pulse oximeters with Bluetooth connectivity allow seamless transfer of patient oxygen saturation readings to mobile applications or hospital information systems, enabling real-time monitoring by healthcare providers

- Integration with digital monitoring platforms allows sensors to track trends, set personalized alerts, and generate automated reports, improving clinical decision-making and reducing manual errors in patient management

- The use of connected SpO₂ sensors also enables remote patient monitoring, allowing clinicians to supervise oxygen saturation levels for high-risk patients at home, reducing hospital visits while maintaining quality care

- This trend towards more intelligent, patient-friendly, and connected monitoring systems is fundamentally reshaping clinical workflows, leading companies such as Nonin Medical and Masimo to develop devices with enhanced connectivity, automated reporting, and data integration capabilities

- The demand for Middle East and Africa disposable peripheral capillary oxygen saturation (SpO₂) sensor solutions that provide connected, real-time monitoring is growing rapidly across hospitals and home care settings as healthcare providers increasingly prioritize efficiency, patient safety, and continuous monitoring

- Healthcare providers are also leveraging AI-driven analytics alongside connected SpO₂ sensors to detect early signs of deterioration, particularly in COVID-19 and chronic respiratory patients, enhancing preventive care and resource allocation

Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (Spo2) Sensor Market Dynamics

Driver

“Growing Need Due to Rising Respiratory Disorders and Continuous Monitoring Adoption”

- The increasing prevalence of respiratory diseases, coupled with the rising focus on patient safety and adoption of continuous monitoring systems, is a significant driver for the heightened demand for Middle East and Africa disposable peripheral capillary oxygen saturation (SpO₂) sensor solutions

- For instance, in March 2025, Masimo announced the launch of its new Bluetooth-enabled fingertip pulse oximeter in UAE hospitals, designed for seamless integration with electronic health records and remote monitoring platforms, which is expected to boost market adoption

- As healthcare providers seek more accurate and non-invasive methods to monitor patients, SpO₂ sensors provide continuous oxygen saturation tracking, early warning alerts, and automated logging, offering a compelling improvement over traditional spot-check devices

- Furthermore, the expansion of hospitals, ICU facilities, and home healthcare services in countries such as Saudi Arabia, Egypt, and South Africa is increasing the demand for reliable SpO₂ sensors across multiple care settings

- The convenience of real-time monitoring, data sharing with clinicians, and compatibility with mobile applications are key factors propelling adoption of Middle East and Africa disposable peripheral capillary oxygen saturation (SpO₂) sensor devices in both urban and remote healthcare facilities

- The trend towards integrating continuous monitoring into standard patient care routines and the increasing availability of user-friendly SpO₂ sensor devices are further supporting sustained market growth

- Rising awareness among patients and caregivers about early detection of hypoxia and respiratory complications is also driving demand for disposable SpO₂ sensors in home care and outpatient settings

- Government initiatives and hospital programs promoting remote patient monitoring and telehealth solutions are increasingly encouraging adoption of connected SpO₂ sensors across the Middle East and Africa

Restraint/Challenge

“Sensor Accuracy Variability and Regulatory Compliance Hurdle”

- Concerns surrounding sensor accuracy under varying physiological conditions, as well as stringent regulatory compliance requirements, pose significant challenges to broader adoption of Middle East and Africa disposable peripheral capillary oxygen saturation (SpO₂) sensor devices

- For instance, high-profile reports of inaccurate readings in motion or low-perfusion conditions have made some clinicians hesitant to rely solely on disposable SpO₂ sensors for critical care decisions

- Addressing these concerns through improved sensor technology, calibration protocols, and compliance with FDA, CE, and local regulatory standards is crucial for building trust among healthcare providers. Companies such as Nonin and Masimo emphasize their rigorous testing and certification processes to reassure potential buyers

- In addition, the relatively higher cost of advanced disposable SpO₂ sensors with Bluetooth connectivity and integrated reporting features can be a barrier for budget-conscious hospitals or home care providers in developing countries

- While prices are gradually decreasing and basic models are widely available, the perceived premium for advanced connected devices can still hinder adoption, especially where standard monitoring methods are considered sufficient

- Overcoming these challenges through technological improvements, regulatory compliance, and cost optimization will be vital for sustained growth of the Middle East and Africa disposable peripheral capillary oxygen saturation (SpO₂) sensor market

- Limited awareness of advanced SpO₂ sensor functionalities among smaller clinics and rural healthcare facilities also restrains wider adoption

- Supply chain challenges, including dependency on imported devices and components, may affect timely availability and pricing, further impacting market expansion in certain countries

Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor Market Scope

The market is segmented on the basis of connector, usage, technique, signal, application, end user, and sales channel.

- By Connector

On the basis of connector type, the market is segmented into Less Than 6 Pins, 6 Pins-10 Pins, and More Than 10 Pins. The 6 Pins-10 Pins segment dominated the market with the largest revenue share in 2025, driven by its ability to provide stable connections while supporting both analog and digital signals. Hospitals widely use these connectors for adult and pediatric patient monitoring due to their reliability and compatibility with standard monitoring devices. The segment also benefits from integration with electronic health records and other hospital management systems, enabling efficient data capture. Manufacturers prefer this range as it balances performance and cost-effectiveness, ensuring wide adoption in clinical setups. Hospitals and critical care units often prioritize 6–10 pin connectors for ICU monitoring, surgical procedures, and long-term patient observation. The availability of multiple configurations and durability further supports its dominance in the market.

The Less Than 6 Pins segment is expected to witness the fastest growth from 2026 to 2033, driven by rising demand for portable, wearable, and home-use pulse oximeters. Smaller connectors reduce device size, enhancing comfort for neonates, pediatric, and home care patients. Their lower production cost allows manufacturers to offer affordable solutions without compromising quality. Increasing adoption in telehealth and remote monitoring programs in Egypt, Nigeria, and South Africa is accelerating growth. Compact designs also facilitate integration into multi-parameter monitoring devices. The segment’s simplicity and ease of use make it particularly suitable for rural healthcare and mobile clinics.

- By Usage

On the basis of usage, the market is segmented into adult, pediatric, neonate, animal, and others. The Adult segment dominated the market in 2025 with the largest revenue share due to high hospital and home care adoption. Adult SpO₂ sensors are extensively used in ICUs, surgical wards, and emergency care for accurate oxygen saturation monitoring. Hospitals prefer adult sensors for durability, repeated use, and compatibility with multiple connector and signal types. These sensors are widely integrated with digital platforms for data logging, remote monitoring, and clinical reporting. Manufacturers focus on adult sensors with advanced features such as wireless connectivity and AI-assisted monitoring, further strengthening market dominance. Continuous demand for adult sensors in chronic respiratory care, post-surgery recovery, and outpatient monitoring drives revenue consistently.

The Neonate segment is expected to witness the fastest growth from 2026 to 2033, supported by increasing investments in neonatal intensive care units (NICUs) and growing awareness of infant respiratory health. Neonate sensors are designed for small fingers or toes with soft materials to prevent skin irritation and ensure accurate readings. Government and NGO programs in Egypt and Nigeria to reduce infant mortality are driving adoption. Home healthcare and transport applications for newborns further increase demand. Manufacturers are innovating compact, highly sensitive neonate sensors with wireless and digital connectivity. Rising awareness among parents and caregivers about hypoxia detection is fueling rapid market growth.

- By Technique

On the basis of technique, the market is segmented into Reflectance and Transflectance. The Transflectance segment dominated the market in 2025 due to its ability to provide accurate readings even under low perfusion or critical care conditions. Hospitals and clinical setups prefer transfectance sensors for ICUs, surgical wards, and emergency departments where precision is critical. Their higher signal-to-noise ratio ensures reliable data collection for adults and pediatric patients. Integration with electronic health systems and digital monitoring platforms further supports their market dominance. Manufacturers focus on transfectance technology for premium devices that require high accuracy and connectivity features. Hospitals value transfectance sensors for durability, repeatable performance, and compatibility with multiple patient monitoring systems.

The Reflectance segment is expected to witness the fastest growth from 2026 to 2033, driven by the rising adoption of portable, wearable, and home-use pulse oximeters. Reflectance sensors can be applied to non-traditional sites such as the forehead or chest, increasing comfort for neonates and ambulatory patients. Their design facilitates integration with wireless, Bluetooth, and digital platforms. The segment benefits from increasing home care, telehealth, and remote monitoring adoption in Saudi Arabia, Egypt, and South Africa. Lightweight and compact reflectance sensors are cost-effective, driving demand in emerging healthcare markets. Consumer preference for wearable health devices also contributes to rapid growth.

- By Signal

On the basis of signal, the market is segmented into analog and digital. The Digital segment dominated the market in 2025, offering superior accuracy, low interference, and seamless integration with electronic health records. Hospitals prefer digital SpO₂ sensors for critical care, continuous monitoring, and remote patient observation. Digital sensors provide automated alerts, trend analysis, and data logging, increasing patient safety. Manufacturers focus on digital devices for ICU and emergency care due to their reliability and compatibility with hospital monitoring systems. Digital sensors are increasingly integrated with wireless and cloud platforms, supporting telehealth programs. The need for precise readings in adult, pediatric, and neonatal patients reinforces the dominance of digital SpO₂ sensors.

The Analog segment is expected to witness the fastest growth from 2026 to 2033 due to cost-effectiveness and simplicity, making it suitable for basic clinics, veterinary applications, and rural hospitals. Analog sensors are easy to use, maintain, and integrate with standard monitoring devices. Increasing demand for low-cost portable pulse oximeters in emerging Middle East & Africa markets is driving adoption. Clinics in Nigeria, Egypt, and South Africa prefer analog devices for home care and outpatient monitoring. The segment also benefits from rising veterinary applications where affordability and durability are prioritized. Growing awareness of early detection of hypoxia in patients supports fast expansion.

- By Application

On the basis of application, the market is segmented into finger, ear, foot, toe, multi position, and others. The Finger segment dominated the market in 2025, accounting for the largest revenue share of 44.9% due to its wide applicability across hospitals, clinics, and home care. Finger SpO₂ sensors are easy to attach, non-invasive, and provide highly accurate readings, making them the preferred choice for adult and pediatric monitoring. Hospitals and critical care units adopt finger sensors for routine monitoring, ICU use, and emergency situations due to their reliability and repeatability. The segment benefits from compatibility with both analog and digital systems, as well as integration with wireless monitoring platforms. Manufacturers continuously innovate finger sensors with enhanced connectivity, comfort, and portability, reinforcing their dominance. Demand is further boosted by the convenience of rapid measurements and minimal patient discomfort.

The Toe segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing neonatal care and monitoring in NICUs. Toe sensors are specifically designed for small neonates, ensuring accurate readings without causing skin irritation or discomfort. Hospitals and home care providers are adopting toe sensors for continuous monitoring in infants at risk of hypoxia or respiratory complications. Manufacturers are developing compact, wireless, and highly sensitive toe sensors to cater to neonatal monitoring. The segment also benefits from rising home-based neonatal care and telehealth adoption. Increasing awareness of early detection of oxygen desaturation in newborns further supports rapid growth.

- By End User

On the basis of end user, the market is segmented into clinical, hospital, veterinary, and others. The Hospital segment dominated the market in 2025 with the largest revenue share, driven by large-scale adoption in ICUs, surgical wards, emergency departments, and general patient monitoring. Hospitals prefer disposable SpO₂ sensors due to their reliability, accuracy, and infection control benefits. Integration with electronic health records, ICU monitoring systems, and remote patient monitoring platforms further enhances the segment’s dominance. Manufacturers focus on hospital-grade sensors with enhanced durability, connectivity, and data management features. Hospitals across Saudi Arabia, UAE, and South Africa continue to invest in advanced patient monitoring infrastructure, driving sustained revenue. Continuous demand for adult, pediatric, and neonatal monitoring supports this subsegment.

The Clinical segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing adoption of outpatient monitoring, diagnostic centers, and home healthcare clinics. Clinical end users require cost-effective, portable, and easy-to-use SpO₂ sensors for continuous monitoring of patients. Integration with telehealth solutions and wearable health devices is accelerating adoption in clinics. Smaller clinics in Egypt, Nigeria, and Kenya are increasingly deploying disposable SpO₂ sensors for chronic respiratory disease management and routine check-ups. Rising awareness among clinicians and patients about early hypoxia detection supports market growth. Manufacturers are innovating compact clinical sensors with reliable performance to meet this growing demand.

- By Sales Channel

On the basis of sales channel, the market is segmented into offline and online. The Offline segment dominated the market in 2025, accounting for the largest revenue share due to hospitals, clinics, and distributors relying on direct purchase channels. Offline distribution allows healthcare providers to physically evaluate sensor quality, receive immediate support, and ensure compliance with regulatory standards. Hospitals in Saudi Arabia, UAE, South Africa, and Egypt prefer offline purchases for bulk orders, warranties, and maintenance agreements. Manufacturers often partner with medical device distributors and wholesalers to strengthen offline presence. The segment benefits from established medical supply chains, trust in local suppliers, and immediate product availability. Ongoing hospital expansions and investments in patient monitoring infrastructure continue to reinforce offline channel dominance.

The Online segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing e-commerce adoption, digital procurement platforms, and direct-to-consumer sales of portable SpO₂ sensors. Online channels provide convenience, access to multiple brands, competitive pricing, and delivery to remote or rural areas. Rising awareness of home healthcare monitoring, telehealth, and wearable health devices contributes to rapid online growth. Manufacturers are increasingly selling sensors through online portals, mobile apps, and B2B platforms for clinics and home care providers. The COVID-19 pandemic accelerated digital sales adoption, which continues to support expansion. Online channels also allow users to compare features, read reviews, and access support, enhancing adoption rates.

Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa disposable peripheral capillary oxygen saturation (SpO₂) sensor market with the largest revenue share in 2025 of 30.7%, supported by significant healthcare infrastructure investments, expansion of intensive care units, and increased access to advanced medical device

- Healthcare providers in the region highly value the accuracy, reliability, and ease of integration offered by disposable SpO₂ sensors with electronic health records, remote monitoring systems, and multi-parameter patient monitoring platforms

- This widespread adoption is further supported by growing awareness of respiratory health, increasing prevalence of chronic and acute respiratory diseases, and government initiatives to enhance patient safety and reduce hospital-acquired infections, establishing disposable SpO₂ sensors as essential monitoring tools in both hospital and home care settings

The Saudi Arabia Disposable Peripheral Capillary Oxygen Saturation (SpO₂) Sensor Market Insight

The Saudi Arabia disposable peripheral capillary oxygen saturation (SpO₂) sensor market captured the largest revenue share in 2025, driven by major investments in healthcare infrastructure, expansion of ICUs, and rising adoption of advanced patient monitoring technologies. Hospitals and clinics increasingly prioritize accurate, reliable, and connected SpO₂ sensors for adult, pediatric, and neonatal monitoring. The growing integration of digital health records, remote monitoring systems, and multi-parameter patient monitoring platforms further boosts market adoption. Government initiatives to improve patient safety, reduce hospital-acquired infections, and enhance telehealth services are also key contributors. The demand spans both hospital and home care settings, with a focus on high-quality disposable sensors for routine and critical care monitoring. Rising awareness among healthcare providers about continuous oxygen saturation tracking strengthens the market's expansion.

UAE Disposable Peripheral Capillary Oxygen Saturation (SpO₂) Sensor Market Insight

The UAE disposable peripheral capillary oxygen saturation (SpO₂) sensor market is expected to expand at a significant CAGR during the forecast period, fueled by widespread hospital modernization, growing private healthcare investments, and the increasing prevalence of respiratory diseases. Healthcare facilities are adopting connected SpO₂ sensors compatible with electronic health records and mobile monitoring applications. The region also benefits from advanced telemedicine and home care programs that utilize portable and Bluetooth-enabled devices. Rising government initiatives supporting digital healthcare adoption and patient safety measures are driving the market. Adoption spans adult, pediatric, and neonatal monitoring across clinical, hospital, and home care settings. Integration with multi-parameter monitoring platforms further reinforces the UAE’s market growth trajectory.

Egypt Disposable Peripheral Capillary Oxygen Saturation (SpO₂) Sensor Market Insight

The Egypt disposable peripheral capillary oxygen saturation (SpO₂) sensor market is anticipated to grow at a robust CAGR, driven by expanding hospital networks, increasing government healthcare initiatives, and rising awareness of oxygen monitoring for chronic respiratory patients. Hospitals and clinics are increasingly deploying disposable SpO₂ sensors for ICU and emergency applications. Portable devices for home-based care and outpatient monitoring are contributing to market expansion. Rising prevalence of respiratory disorders, including COPD and COVID-related conditions, supports sustained demand. Manufacturers are introducing cost-effective, high-accuracy devices to cater to both urban and rural healthcare facilities. Integration with electronic health systems and telehealth solutions strengthens the adoption rate.

Nigeria Disposable Peripheral Capillary Oxygen Saturation (SpO₂) Sensor Market Insight

The Nigeria disposable peripheral capillary oxygen saturation (SpO₂) sensor market is projected to grow at a rapid CAGR during the forecast period, fueled by expanding access to hospital facilities, rising home healthcare adoption, and increasing awareness of early detection of hypoxia. Hospitals and clinics are investing in portable and disposable SpO₂ sensors for adult and pediatric monitoring. Telehealth and remote patient monitoring programs in urban and semi-urban areas are accelerating adoption. Government initiatives to improve neonatal and respiratory care are also driving market expansion. Cost-effective devices suitable for emerging healthcare setups are increasingly available. Rising awareness among caregivers and patients about the importance of continuous oxygen monitoring further supports rapid market growth.

Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor Market Share

The Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor industry is primarily led by well-established companies, including:

- Masimo (U.S.)

- Medtronic (Ireland)

- Nonin (U.S.)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- NIHON KOHDEN CORPORATION (Japan)

- Contec Medical Systems Co., Ltd. (China)

- Beurer GmbH (Germany)

- BPL Medical Technologies (India)

- Mindray Medical International Limited (China)

- Heal Force Bio Meditech (China)

- Smiths Medical (U.S.)

- Vyaire Medical (U.S.)

- Drägerwerk AG & Co. KGaA (Germany)

- Edan Instruments, Inc. (China)

- ChoiceMMed Technologies Inc. (China)

- Opto Circuits (India)

- Spacelabs Healthcare (U.S.)

- CAS Medical Systems (U.S.)

- Avante Health Solutions (U.S.)

What are the Recent Developments in Middle East and Africa Disposable Peripheral Capillary Oxygen Saturation (SpO2) Sensor Market?

- In June 2025, GE Healthcare announced a strategic distribution partnership in the UAE to improve accessibility of its pulse oximeter devices for healthcare providers across the Middle East & Africa. This collaboration is aimed at increasing market penetration and device availability in clinical settings throughout the region

- In February 2024, Philips partnered with a telehealth provider to integrate pulse oximeters into remote patient monitoring solutions, enhancing the use of SpO₂ data in telemedicine care, which is increasingly relevant to MEA telehealth expansion

- In October 2023, GE Healthcare released a Bluetooth‑enabled fingertip pulse oximeter designed for real‑time data sharing with healthcare providers, improving SpO₂ monitoring in both clinical and home healthcare settings. This launch reflects growing demand for connected oxygen saturation monitoring tools that support telehealth and remote patient tracking

- In August 2023, Smiths Medical launched a pulse oximeter with improved sensor technology to deliver more accurate SpO₂ readings in low perfusion conditions, addressing clinical accuracy concerns especially relevant in critical care and emergency monitoring

- In January 2023, Philips Healthcare announced the launch of a new portable pulse oximeter for home use in the Middle East with advanced connectivity that allows patients to share SpO₂ readings with healthcare professionals seamlessly. This initiative aims to enhance remote patient monitoring capabilities and improve outcomes in respiratory care across the region

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.