North America Endoscopic Hemostasis Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

880.69 Million

USD

1,563.38 Million

2025

2033

USD

880.69 Million

USD

1,563.38 Million

2025

2033

| 2026 –2033 | |

| USD 880.69 Million | |

| USD 1,563.38 Million | |

| % | |

|

تصنيف أسواق أمريكا الشمالية، حسب نوع المنتج (أجهزة ميكانيكية وأجهزة وأجهزة وأجهزة حرارية وعوامل موضوعية وعوامل حقن، وغيرها)، والإجراءات (الانتقال الانسداد المعوي المعوي، الانسداد الاندي المعوي، الانسداد الاندي المعوي المعوي الأسفل، الانسداد المعوي المعوي المعوي المعوي، الانسداد المعوي المعالج، البرونوسكوب البرونيكوسكوبي، الهايمواسيس، وغيرها)، والتطبيقات (المنسوجات المعوية المبرزة، المبرومة، غير المعالجات المعوية، إدارة الصدمات، وآخرون)، والمستعمل النهائي (المستشفى، مراكز الجراحة الإسعافية، العيادات الخاصة، وجهات أخرى)، قناة التوزيع (المبيعات المباشرة والمبيعات غير المباشرة). - الاتجاهات الصناعية والتنبؤات حتى عام 2033

أمريكا الشمالية

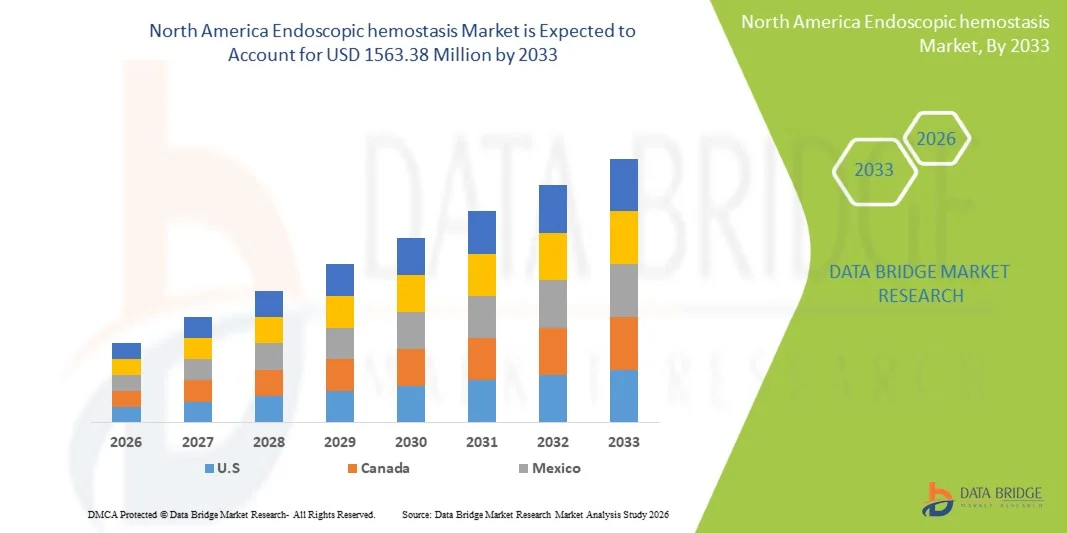

- ومن المتوقع أن تصل سوق أمريكا الشمالية المناظير الداخلية لمدارس الهاوية إلى مبلغ قدره 1563.38 مليون دولار بحلول عام 2033 من 880.69 مليون دولار من دولارات الولايات المتحدة في عام 2025، حيث ستزداد بنسبة 7.9 في المائة في الفترة المتوقعة من 2026 إلى 2033.

- وتشهد سوق أمريكا الشمالية المناظير الداخلية لمعالجة الهاوية نموا مطردا وقويا، مدفوعا بارتفاع انتشار الاضطرابات المعوية المعوية، وتزايد حدوث سرطان القولون، والقرحات الحفازة، والنزيف المعوي المعوي المعوي، وتزايد اعتماد إجراءات داخلية قليلة الإجتياح في جميع أنحاء المنطقة.

- فضلاً عن ذلك فإن التطورات المستمرة في تصميم الأجهزة الداخلية، بما في ذلك تحسين القصاصات، ونظم التخثر، والرش، والعلاجات المركبة، تعمل على تعزيز الدقة، وسهولة الاستخدام، والفعالية السريرية. وعلاوة على ذلك، فإن زيادة الاستثمارات في البحث والتطوير في مجال الأجهزة الطبية، والابتكار التكنولوجي، وإدماج الجيل المقبل من المواد والنظم القائمة على الطاقة، تؤدي إلى دفع ابتكار المنتجات ودعم النمو الطويل الأجل لسوق آسيا والمحيط الهادئ للمكثفات.

أمريكا الشمالية

- إن توسيع البنية الأساسية للرعاية الصحية، وارتفاع أحجام الإجراءات الداخلية، وتزايد تبني نُهج العلاج التي تنطوي على حد أدنى من التوسع، تعمل على تغذية الطلب القوي على الأجهزة المسببة لسرطان الدم في أميركا الشمالية. ويتزايد دمج مقدمي الرعاية الصحية للتكنولوجيات المتقدمة الأكثر تقدماً لتحسين الكفاءة الإجرائية، وخفض معدلات التعقيد، وتقليص فترات الإقامة في المستشفيات، وتعزيز النتائج الشاملة للمريض، وبالتالي دعم نمو السوق المستدام.

- ومن المتوقع أن تسيطر الولايات المتحدة على سوق الهاوية المناظير الداخلية لأمريكا الشمالية، حيث تحصل على 80.24% من حصة السوق في عام 2026، مدفوعة بالهياكل الأساسية القائمة للرعاية الصحية، وارتفاع حجم الإجراءات المناظير الداخلية، والاعتماد القوي للتكنولوجيات الطبية المتقدمة، ووجود كبار صانعي الأجهزة الطبية.

- إن الولايات المتحدة هي البلد الأسرع نمواً في سوق الولايات المتحدة الأمريكية الداخلية لمعالجة مبيدات الآفات، مدعومة بالتبني المبكر للصحة الرقمية ومنصات التنظير الداخلي المتقدمة، وبالتكامل القوي بين التشخيصات التي تساعدها منظمة العفو الدولية والإجراءات الداخلية الموجَّهة إلى الصورة، وبمستوى عال من المشاركة البحثية السريرية في المعالجة المعوية المعوية المعوية والتدخلية. وبالإضافة إلى ذلك، فإن مسارات الإحالة الجيدة التنظيم في البلاد، والتركيز على الرعاية النهارية والعلاجات الداخلية للمرضى الخارجيين، وسرعة الاستيعاب التجاري السريع للجيل المقبل من الأجهزة التي تعمل على معالجة المكثفات من جانب أطباء العيادات، تزيد من تسريع الأحجام الإجرائية. وبالإضافة إلى ذلك، فإن التعاون بين المستشفيات والمؤسسات الأكاديمية وصناع الأجهزة الطبية، إلى جانب تبسيط الأطر الزمنية التنظيمية للموافقة على التكنولوجيات المبتكرة، لا تزال تتخذ من الدانمرك سوقاً رائدة في مرحلة الطفولة المبكرة، تقود نمواً أسرع مقارنة بالبلدان الأخرى في أميركا الشمالية.

- ويسيطر قطاع الأجهزة الميكانيكية لمعالجة الهاوية على سوق أمريكا الشمالية للمساوئ المجهرية، حيث بلغت حصتها في السوق 43.05 في المائة في عام 2025. وترجع هذه الهيمنة إلى الاعتماد السريري الواسع النطاق لمقاطع النظائر الداخلية وأجهزة ربط النطاقات بسبب فعاليتها المثبتة وسهولة نشرها وفعاليتها من حيث التكلفة وملاءمتها لطائفة واسعة من مؤشرات النزف المعوي المعوي المعوي. ولا تزال سماتها القوية في مجال السلامة ومدى توافقها مع الإجراءات الداخلية الموحدة تدعم الطلب المستدام في مختلف بيئات الرعاية الصحية.

تقرير عن النطاق وأمريكا الشمالية

| الصفات الأولى | أمريكا الشمالية |

| المُسَجَّل |

|

| البلدان |

|

| & مفتاح |

|

| ما |

|

| جاري | وبالإضافة إلى الرؤى المتعلقة بسيناريوهات السوق مثل القيمة السوقية، ومعدل النمو، والتجزئة، والتغطية الجغرافية، واللاعبين الرئيسيين، فإن تقارير السوق التي تُقيِّمها بحوث سوق جسر البيانات تشمل أيضاً تحليلاً متعمقاً للخبراء، وعلم وبائيات المرضى، وتحليل خطوط الأنابيب، وتحليل الأسعار، والإطار التنظيمي. |

أمريكا الشمالية

“تكرار اعتماد تكنولوجيات متقدمة للحد الأدنى لتكنولوجيات الان انسداد مغذية متقدمة محفزة للانسداد"

- إن التوسع المطرد في الإجراءات التنظيريّة الباطنية والاجتياحية الدنيا في مختلف أنحاء أميركا الشمالية يشكل عاملاً رئيسياً يدفع إلى زيادة اعتماد أجهزة الشلل المكشوفة الداخليّة. فمع استمرار ارتفاع معدل الإصابة بنزيف معوي معوي معوي، واضطرابات في القولبة، وما يتصل بذلك من ظروف، يعتمد مقدمو الرعاية الصحية بشكل متزايد على الحلول المتقدمة لمعالجة الهاوية لضمان السيطرة الفعالة على النزيف، والسلامة الإجرائية، وتحسين نتائج المرضى عبر البيئات السريرية ذات الحجم المرتفع.

- إن الأجهزة المكشوفة المكشوفة المكشوفة التي تعمل على معالجة المكشوفة تلعب دوراً حاسماً في ضمان الفعالية السريرية، وسلامة المرضى، والموثوقية الإجرائية في كل مراحل التشخيص والعلاج. ومن خلال التمكين من السيطرة السريعة على النزيف، والحد من مخاطر التعقيد، ودعم نُهج العلاج الغازية إلى الحد الأدنى، تساعد هذه الأجهزة على تحسين تدفق العمل الإجرائي إلى أقصى حد، مع تحسين أوقات التعافي والجودة العامة للرعاية في مختلف مرافق الرعاية الصحية.

- إن تبني تكنولوجيات داخلية متقدمة بشكل متزايد، بما في ذلك التصوير عالي الدقة، والتنقيح العلاجي، وتقنيات المزج بين علاج المحار، أدى إلى زيادة الطلب على حلول متسارعة عالية الأداء. والواقع أن الابتكارات في المقاطع الميكانيكية، ونظم التخثر الحراري، وعلاجات الحقن، والعوامل الساخنة المواضيعية تعمل على تعزيز الدقة الإجرائية، ومعدلات نجاح العلاج، والثقة الطبية في الوقت الذي تدعم فيه الممارسات السريرية المتطورة.

- إن مقدمي الرعاية الصحية في مختلف مراحل الرعاية يعتمدون بشكل متزايد على أجهزة محرقة داخلية مجهرية لتلبية معايير الأداء التنظيمية والأمنية والإكلينيكية المتزايدة. والواقع أن المبادئ التوجيهية السريرية الصارمة، والتركيز المتزايد على سلامة المرضى والرعاية القائمة على النتائج، وتزايد الطلب على التدخلات التي لا تنطوي إلا على الحد الأدنى من الضغوط، تشجع المستشفيات والعيادات على دمج تكنولوجيات التصعيد المتقدمة التي تضمن الاتساق والامتثال وتقديم الرعاية ذات الجودة العالية.

- وعلى وجه الإجمال، فإن اتساع نطاق الإجراءات الداخلية، والإبداع السريري، وتطوير البنية الأساسية للرعاية الصحية، يضع أجهزة الهادافات التناظرية التنظيرية الداخلية باعتبارها عنصراً أساسياً في الرعاية الهضمية الهضمية الحديثة. وتدعم هذه الحلول الكفاءة الإجرائية، وسلامة المرضى، والامتثال التنظيمي، والنمو المستدام عبر المناظر الطبيعية المتطور للنظير الداخلي في أميركا الشمالية، الأمر الذي يجعل هذه البصيرة قابلة لإعادة الاستخدام بسهولة عبر المناطق من خلال تكييف ديناميات نظام الرعاية الصحية وأنماط تبنيها.

أمريكا الشمالية

سائق

“النقص في حالات الإصابة بعجز معمّاً معمّاً في الجهاز الهاتري المعوي”

- وقد ثبت أن ارتفاع معدل الإصابة بنزيف غذائي معوي هو قوة أساسية للنمو في سوق أمريكا الشمالية، ومع تزايد معدلات الإصابة بنزيف غذائي غذائي أعلى وأدني على نطاق العالم، اشتد الطلب على التدخلات العلاجية القائمة على أساس التكرير الداخلي التي لا تؤدي إلا إلى الحد الأدنى من الاضمحلال. وتوفر الشللات الداخلية مزايا سريرية حاسمة، بما في ذلك السيطرة السريعة على النزيف، وانخفاض الحاجة إلى التدخل الجراحي، وانخفاض متطلبات نقل الدم، وقصر فترات الإقامة في المستشفيات، مما يجعلها بمثابة وسيلة أولى للعلاج في حالات النزيف الحادة والمزمنة، مما يجعلها بمثابة وسيلة علاجية في حالات النزيف المعوي المعوي الحادة والمزمنة. ونتيجة لذلك، فإن التصاعد في حالات النزيف المعوي - التي تحركها شيوخة السكان، وارتفاع معدل انتشار أمراض الكبد، واستخدام مضادات التخثر، وتأخر الحصول على الرعاية أثناء الاضطرابات الصحية المنهجية - قد ترجم إلى أحجام إجرائية أعلى وإلى اعتماد أوسع نطاقاً لأجهزة متقدمة للواسم البطينية في المستشفيات ومراكز التنظيف الرحمي في شمال أمريكا.

بالنسبة لحالات،

- وفي أيلول/سبتمبر 2021، أفادت مجلة Medscape أن نزيفاً غذائياً غذائياً في الأعلى حدث بمعدل 100 حالة تقريباً لكل 000 100 نسمة سنوياً، وظل واحداً من أكثر أسباب دخول المستشفيات الطارئة شيوعاً، مما يؤكد استمرار ارتفاع عبء الأمراض التي تتطلب تدخلاً من المنظار.

- وفي حزيران/يونيه 2023، أفادت مجلة بحوث علم النفس الفائق أن الوفيات ذات الصلة بنزيف الجهاز الهضمي المعوي العلوي في الولايات المتحدة زادت بين عامي 2012 و2021، مع ملاحظة زيادات أكبر في السنوات الأخيرة، مما يشير إلى تدهور النتائج السريرية ومتطلبات العلاج المكثفة.

- وفي حزيران/يونيه 2023، ذكرت شركة StatPearls للنشر أن النزيف المعوي المعوي المعوي لا يزال يمثل حالة طوارئ طبية متكررة في أمريكا الشمالية، حيث لا يزال التشخيص العاجل للتنظير الباطني والعلاج المتصاعد عاملا حاسما في الحد من الوفيات والاعتلال.

- وفي كانون الثاني/يناير 2025، أفادت مجلة الطب الإكلينيكي أن المرضى المصابين بأمراض كبدية متقدمة قد أظهروا زيادة كبيرة في عدد حالات النزيف المعوي المعوي الهائل، مما يعزز الصلة بين انتشار الأمراض المزمنة وازدياد الحاجة إلى التصلب المعوي.

- وفي أيلول/سبتمبر 2025، أبرز مركز باوبميد أن النزيف المعوي المعوي المعوي العلوي لا يزال يشكل مشكلة تهدد حياة السكان المصابين بأمراض الكبد المزمنة، مما يؤدي إلى استمرار ارتفاع الطلب على الإجراءات العلاجية الداخلية.

- ويجري ترسيخ التصعيد في حالات النزيف المعوي المعوي في أمريكا الشمالية باعتباره محركاً دائماً للنمو الهيكلي لسوق الشلل البطيني، والارتفاع المستمر في حالات النزيف الحاد، إلى جانب تزايد عدد السكان المتأثرين بأمراض الكبد المزمنة، واستخدام الأدوية المضادة للتشنج، والأمراض المعوية المعوية المعوية المتصلة بالعمر، يخلق مطلباً مستمراً وغير دوري لمكافحة النزف الداخلي، ومع تزايد إعطاء الأولوية للمعالجة الباطنية كإدارة الخط الأول للمبادئ التوجيهية السريرية، فإن الاعتماد على تكنولوجيات التسارع للتدخل في حالات الطوارئ والوقاية من التكرار وإدارة التعقيدات يجري تعزيزه هيكلياً، فضلاً عن ذلك، فإن تحسين معدلات البقاء يوسع من نطاق دورات رصد المرضى وتكرار التدخل، مما يضاعف الطلب الإجرائي مدى الحياة، وهذا الديناميك يرسّخ الاعتماد على فرط الودوبات الداخلية بشكل وثيق مع الاتجاهات الوبائية في أمريكا الشمالية، مما يجعل من هذا المحرك ركيزة أساسية طويلة الأجل لتوسيع الأسواق عبر نظم الرعاية الصحية المتقدمة والناشئة.

التعرّض/التحديي

"التكلفة العالية والتعقّد التقني لأجهزة معالجة مظلات التنظير"

- وعلى الرغم من الاعتماد السريري المتزايد، لا تزال سوق أمريكا الشمالية للتنظير الداخلي لمبيدات الآفات تواجه قيودا هيكلية بسبب ارتفاع تكلفة الأجهزة المتطورة للوسائد الداخلية وتعقدها التقني، وكثيرا ما تتطلب هذه التكنولوجيات استثمارات رأسمالية أولية كبيرة لشراء المعدات، والإنفاق المستمر على الأصناف الاستهلاكية، والصيانة المتخصصة، وبالإضافة إلى ذلك، يتطلب الاستخدام الفعال للأجهزة المجهرية الداخلية المكشوفة، تدريبا متقدما من الأطباء، وموظفي دعم مهرة، وهياكل أساسية متطورة في المستشفيات، مما يحد من الاعتماد في نظم الرعاية الصحية التي تراعي التكاليف، والمستشفيات العامة في البلدان المنخفضة والمتوسطة الدخل، بل وحتى المرافق المقيدة في الميزانية في المناطق المتقدمة النمو، كثيرا ما تواجه حواجز تتعلق بالقدرة على تحمل التكاليف، والثغرات في السداد، والاستعداد للقوة العاملة، ونتيجة لذلك، يستمر عدم تكافؤ فرص الحصول على التكنولوجيات المتقدمة لمعالجة الحساسيات الداخلية وانتشارها بشكل أبطأ، مما يعوق توسع الأسواق على نطاق أوسع.

في حالة ما إذا حدث

- وفي تشرين الثاني/نوفمبر 2022، ووفقاً لارتفاع تكلفة إجراءات ومعدات النسخ الانسيابي المعوي المعوي المعوي المعوي، تشكل هذه الإجراءات والمعدات قيداً رئيسياً، فعلى سبيل المثال، تتكلف شركة TNE 12590 يورو لكل إجراء، في حين تتكلف تكاليف النسخ الانكليسي الفموي 184.10 يورو وتكاليف شركة MACE 407.10 يورو، وإضافة إلى ذلك، تضيف صيانة المعدات وإعادة معالجتها إلى التكلفة، حيث تبلغ تكلفة المناظير الداخلية المرنة نحو 330 79 يورو، مما يجعل الإجراءات مكلفة إجمالاً.

- وفي حزيران/يونيه 2024، أبرزت منظمة العلم المباشر أن التكلفة المرتفعة للتنظير المعوي المعوي المعوي المعوي في البلدان المنخفضة الدخل والبلدان المتوسطة الدخل تتفاقم بسبب عدم وجود مرافق محلية للصيانة والإصلاح، ويجب شحن النطاقات التي تتطلب الإصلاح إلى الخارج، مما ينطوي على تكاليف كبيرة وتأخيرات كبيرة، وبالإضافة إلى ذلك، كثيراً ما تفتقر المناظير الذاتية المستعملة والأرخص تكلفة والمصنعة صينياً إلى ما يكفي من الخدمات والدعم في مجال الصيانة.

- وفي تشرين الأول/أكتوبر 2025، نشرت وزارة العدل في المملكة المتحدة دراسة عن الانسدادات الفهرسية المفتوحة، أظهرت أن إجمالي تكلفة المناظير المعوية المعوية المعوية المعوية القابلة لإعادة الاستخدام في مستشفى وطني للخدمات الصحية في المملكة المتحدة، في كل إجراء، يقدر بـ 107.34 جنيهات استرلينية، مع اعتبار تكاليف رأس المال والصيانة من العوامل الرئيسية المحركة للتكاليف، مما يبرز الحواجز الاقتصادية التي تحول دون اعتماد معدات الانتساب على نطاق واسع في بيئات الصحة العامة.

- وفي آب/أغسطس 2024، أفاد استعراض سردي لدليل العلوم بأن شراء معدات النسخ الداخلي وصيانتها وما يرتبط بها من تكاليف لوجستية لا تزال تشكل عائقا رئيسيا أمام تطوير خدمات النسخ الداخلي والمحافظة عليها في البلدان المنخفضة والمتوسطة الدخل، بسبب ارتفاع تكلفة الأجهزة والافتقار إلى الهياكل الأساسية.

- وفي شباط/فبراير 2025، يتضح من الدراسات المختلفة، ولا سيما لأغراض الفرز والمراقبة، أن التكلفة المرتفعة للتنظير داخل الرحم المعوي المعوي المعوي، كما يشير العلم إلى ذلك، يتضح في دراسات مختلفة، ولا سيما فيما يتعلق بالفرز والمراقبة، فعلى سبيل المثال، في حين أن عمليات فرز السكان عموماً قد لا تكون فعالة من حيث التكلفة في المناطق الغربية، فإن المراقبة المحددة الهدف للفئات الشديدة التعرض للخطر، مثل الفئات التي تعاني من التسارع المعوي المعوي المعوي، يمكن أن تظل فعالة من حيث التكلفة، حيث تتراوح وحدات خفض الانبعاثات المعتمدة المتكاملة بين 739.1 20 دولاراً من دولارات الولايات المتحدة و402 98 دولاراً من دولارات الولايات المتحدة لكل وحدة من وحدات خفض الانبعاثات المعتمدة المعتمدة.

- وتشير الأدلة المجمعة بوضوح إلى أن ارتفاع التكلفة والتعقيد التقني المرتبطين بجهازي التنظير المعوي المعوي المعوي والمعالجة المعوي المعوي والمعالجة الانثويتين لمعالجة المظلات يشكلان قيداً مستمراً على نمو السوق، والاستثمار الرأسمالي الكبير في شراء المعدات، وارتفاع تكاليف كل إجراء على حدة، والنفقات الجارية المتصلة بالصيانة، وإعادة المعالجة، والإصلاح، يزيدان بشكل كبير من عبء التكلفة الإجمالية على نظم الرعاية الصحية، وهذه التحديات تزداد حدة في المناطق المنخفضة والمتوسطة الدخل حيث تؤخر الهياكل الأساسية التقنية المحدودة والافتقار إلى قدرات الخدمة المحلية الاعتماد وتقيد القدرة الإجرائية، وحتى في نظم الرعاية الصحية المتقدمة، تؤثر اعتبارات فعالية التكلفة على استراتيجيات الفرز وتحد من التنفيذ الواسع النطاق.

أمريكا الشمالية

وتصنف سوق مظلات أمريكا الشمالية المجهرية الداخلية في خمسة قطاعات رئيسية: نوع المنتج، والإجراء، والتطبيق، والمستعمل النهائي، وقناة التوزيع.

• حسب نوع المنتج

واستناداً إلى نوع المنتج، فإن سوق أمريكا الشمالية لأجهزة مبيدات الحشرات مقسمة إلى أجهزة ميكانيكية، وأجهزة حرارية، وعوامل قابلة للحقن، وغير ذلك. وفي عام 2026، يتوقع أن يهيمن قطاع الأجهزة الميكانيكية على سوق أمريكا الشمالية لمعالجة الرضوض الداخلية بأكبر حصة سوقية تبلغ 43.08 في المائة، نظراً لتفضيلها السريري الواسع النطاق لتحقيق وقف فوري ومتحكم ودائم للنزيف أثناء التدخلات الداخلية. وتحبذ الحلول الميكانيكية، مثل المقاصات وأجهزة التضميد، بصورة روتينية، قدرتها على توفير إغلاق دقيق للسفن دون إحداث ضرر في الأنسجة الحرارية، وبالتالي خفض معدلات إعادة التشويش والمضاعفات اللاحقة للجراحة. وقد أدى الاعتماد القوي على الميكانيكية كنهج علاجي من الدرجة الأولى إلى زيادة إسهامها الكبير في إيرادات السوق العامة وتعزيز موقعها المهيمن في إطار نوع المنتج خلال الفترة المشمولة بالتنبؤ.

إن قطاع العوامل الموضوعية والحقن هو القطاع الأسرع نمواً في سوق محرقة المحارم المجهرية الداخلية، حيث يبلغ المعدل الإجمالي الإجمالي لمعدلات النمو الإجمالي 8.3 في المائة. ويعزى النمو إلى تزايد حالات النزيف المعوي المعوي، واتساع نطاق اعتماد الإجراءات الداخلية المجهرية التي لا تؤدي إلا إلى الحد الأدنى من الاجتياح، وقوة الطلب الإكلينيكي على حلول سريعة التأثير، وسهلة الفهم، وأقصى درجاتها. ومن المتوقع أن يؤدي التقدم المستمر في فعالية الصياغة، والسلامة، والكفاءة الإجرائية إلى دعم نمو القطاعات أثناء الفترة المتوقعة.

• الإجراء

واستناداً إلى الإجراءات المتبعة، فإن السوق مقسمة إلى فصائل في شكل نسخ من الشرائط المعوية المعوية العليا، ونظيرات من الشرائط المعوية المعوية المعوية العليا، وغير ذلك. وفي عام 2026، من المتوقع أن يهيمن قطاع المكهنات المعوية المعوية المعوية العليا على سوق أمريكا الشمالية لمعالجة الشلل المعوي الداخلي بحصة سوقية تبلغ 42.81 في المائة، بسبب اعتماده السريري الواسع النطاق باعتباره النهج الإجرائي في الجبهة الأمامية لإدارة النزيف المعوي المعوي الحاد والمتكرر. وفي عام 2026، يعتمد المنظير المعوي المعوي العلوي على نطاق واسع في تشخيص القرحات النزفية، والنزيف في المفاصل، والآفات في الديوية، والسيطرة العلاجية الفورية عليها، حيث يكون التدخل السريع في القلب أمراً خطيراً سريرياً. ومن المتوقع أن يؤدي التواتر الإجرائي المرتفع في أقسام الطوارئ ومستشفيات الرعاية الجامعية، إلى جانب الدعم التوجيهي القوي للتدخل الانسيابي المبكر، إلى الحفاظ على مركزها الرئيسي في السوق. وينعكس استمرار هيمنة السوق في حصتها الكبيرة ومسار نموها المطرد خلال عام 2033، مما يشير إلى الطلب المستمر على نظم الرعاية الصحية المتقدمة والناشئة على حد سواء.

أما الجزء السفلي للتنظير الانسيابي المعوي المعوي المعوي فهو الجزء التطبيقي الأسرع نمواً في سوق محارس التجويفية الداخلية، حيث سجل معدلاً لمعدلات الخصوبة الإجمالية قدره 8.3 في المائة، وهذا النمو يدعمه ارتفاع معدل انتشار حالات النزيف المعوي المعوي المنخفض، وزيادة حجم إجراءات التشخيص والعلاج في عمليات النسخ القولونية، وتحسين الكشف عن الاضطرابات التكتونية، ومن المتوقع أن يؤدي التقدم التكنولوجي المستمر في الأجهزة التكميلية لمعالجة التصلب الحراري والتركيز المتزايد على التشخيص المبكر إلى زيادة دفع عملية الاعتماد خلال الفترة المتوقعة.

• حسب الطلب

وعلى أساس الطلب، فإن السوق مقسمة إلى نزيف معوي معوي، ونزيف غير معوي، وإدارة الصدمات، وغير ذلك. وفي عام 2026، يتوقع أن يسيطر قطاع النزف المعوي المعوي على سوق أمريكا الشمالية لمعالجة الهاوية الداخلية بحصة سوقية تبلغ 71.16 في المائة، بسبب ارتفاع معدل انتشار القرحات التحفيزية، والجراثيم المرئية، والخصائص اللونية التي تتطلب السيطرة على النزيف من الداخل. وفي عام 2026، يظل النزيف المعوي المعوي أكثر المؤشرات شيوعاً على إجراءات الهاوية الداخلية، مما يؤدي إلى الاستخدام المتسق للحلول الميكانيكية والحرارة والهاوية في المستشفيات وأماكن الرعاية العلاجية. ومن المتوقع أن تؤدي الحاجة الماسة إلى السيطرة السريعة على النزيف إلى الحد من الاعتلال، وطول مدة الإقامة في المستشفيات، والوفيات إلى تعزيز الطلب المستمر في هذا القطاع التطبيقي. ونصيبه الكبير من القيمة السوقية الإجمالية يبرز الدور المركزي للمؤشرات المعوية في تشكيل ديناميات السوق العامة خلال الفترة المتوقعة.

إن الجزء الخاص بمعالجة الصدمات هو الجزء الأسرع نمواً في سوق مفاتح المداخن المجهرية، حيث يبلغ المعدل الإجمالي لمعدلات النمو الإجمالي الإجمالي 8.5%. ويُعزى النمو إلى تزايد حدوث النزيف الحاد المرتبط بالإصابات الناجمة عن الصدمات، وتزايد تفضيل التقنيات الأقل غزواً التي تمكن من السيطرة السريعة على النزيف. ومن المتوقع أن يدعم التوسع المستمر في هذا الجزء خلال الفترة المتوقعة من التوسع المستمر في هذا الجزء. ومن المتوقع أن يؤدي تحسين النتائج السريرية، وخفض معدلات التدخل الجراحي، والتقدم في تكنولوجيات مفاتح القلب المنظارية الداخلية للطوارئ.

• بواسطة المستخدم النهائي

وعلى أساس المستخدم النهائي، ينقسم السوق إلى مستشفيات ومراكز للجراحة الإسعافية وعيادات متخصصة وغيرها. وفي عام 2026، من المتوقع أن يهيمن قطاع المستشفيات على سوق أمريكا الشمالية لمعالجة مبيدات الآفات الداخلية بأكبر حصة سوقية تبلغ 52.06%، وذلك بسبب تركيز البنية التحتية المتقدمة للتنظير الداخلي، وأخصائيين مهرة متخصصين في أمراض الجهاز الهضمي، وقدرات الرعاية الطارئة داخل المستشفيات. وفي عام 2026، تدار حالات النزف المعقدة، بما في ذلك النزف المعوي المعوي المعوي العالي والأدنى الشديد، بشكل رئيسي في المستشفيات العامة والخاصة حيث تتوافر موارد شاملة للتشخيص والتدخل. كما يعمل ارتفاع تدفق المرضى، وزيادة أحجام الإجراءات، ووضع أطر المشتريات على زيادة تعزيز الطلب في المستشفيات على أجهزة المضايقات الداخلية والمواد الاستهلاكية. ومن المتوقع أن يؤدي هذا الاعتماد الهيكلي على الرعاية القائمة على المستشفيات إلى الحفاظ على المركز الرئيسي للقطاع حتى عام 2033 برغم النمو التدريجي في بيئات المرضى الخارجيين.

والواقع أن جزء مراكز الجراحة الإسعافية هو الجزء الأسرع نمواً من أجزاء المستعملين النهائيين في سوق محارم المظلات المنظرية الداخلية، حيث يسجل معدل نمو الناتج المحلي الإجمالي بنسبة 8.3%. ويعزى النمو إلى التحول المتزايد نحو الإجراءات الداخلية للمرضى الخارجيين، والطلب على تقديم الرعاية الصحية بفعالية من حيث التكلفة، وأوقات أقصر لتعافي المرضى. ومن المتوقع أن يؤدي التقدم في أجهزة مبيدات الآفات المضغوطة والكفؤة والملائمة لأوضاع المرضى الخارجيين إلى زيادة تسريع وتيرة الاعتماد أثناء الفترة المتوقعة.

• بواسطة قناة التوزيع

وعلى أساس قناة التوزيع، تنقسم السوق إلى مبيعات مباشرة ومبيعات غير مباشرة، مع زيادة تقسيم المبيعات غير المباشرة إلى قنوات إلكترونية وغير مباشرة. وفي عام 2026، من المتوقع أن يهيمن قطاع المبيعات غير المباشرة على سوق أمريكا الشمالية للمتاجرة بالمساحات المجهرية، حيث تبلغ حصة السوق الأكبر 57.93 في المائة، حيث تتم المشتريات إلى حد كبير من خلال الموزعين، ومنظمات الشراء الجماعي، وشبكات الإمدادات الطبية الإقليمية. وتُفضَّل القنوات غير المباشرة على نطاق واسع بسبب قدرتها على عرض المنتجات المجمعة، ودعم إدارة المخزون، وتوسيع النطاق الجغرافي، وخاصة في الأسواق الناشئة، ونظم الرعاية الصحية اللامركزية. وتعتمد المستشفيات والمراكز الإسعافية في كثير من الأحيان على المصادر التي يقودها الموزعون لضمان توافر أدوات التصعيد الحرجة بشكل متسق مع الاستفادة المثلى من تكاليف المشتريات. ومن المتوقع أن يستمر هيكل التوزيع هذا في دفع زيادة اعتماد قنوات البيع غير المباشرة طيلة الفترة المتوقعة.

أما قطاع المبيعات غير المباشرة فهو قناة التوزيع الأسرع نمواً في سوق مكامن الهاوية المناظير الداخلية، حيث يبلغ المعدل الإجمالي الإجمالي للحصيلة الإجمالية 8.1 في المائة، ويدعم هذا النمو الدور المتزايد للشركاء في التوزيع وشبكات الشراء الجماعي في تعزيز إمكانية الوصول إلى المنتجات وكفاءة العرض. ومن المتوقع أن يؤدي الاعتماد المتزايد على نماذج الشراء المركزية، واتفاقات الشراء المجمعة، والخبرة الفنية للموزعين الإقليميين إلى مواصلة دفع نمو قناة المبيعات غير المباشرة طيلة الفترة المتوقعة.

التحليل الإقليمي للسوق

- وتمثل الولايات المتحدة واحدة من أهم الأسواق لأجهزة الوسائد المعوية الداخلية، تدعمها بنيتها التحتية المتقدمة للرعاية الصحية، وقاعدة قوية لتصنيع الأجهزة الطبية، واعتماد إجراءات تجويفية داخلية عالية الحد الأدنى من الإجهاد.

- وتشهد المكسيك طلباً متزايداً على تكنولوجيات الشلل المعوي الداخلي مثل زيادة انتشار الاضطرابات المعوية المعوية، وشيخوخة السكان، وزيادة التركيز على نُهُج العلاج الحد الأدنى من الاجتياح، وإعادة تشكيل الممارسة السريرية. ويتزايد تركيز مقدمي الرعاية الصحية على تحسين سلامة المرضى، والحد من المضاعفات المرتبطة بالإجراءات، وتعزيز الكفاءة السريرية، الأمر الذي يعجل من اعتماد أجهزة علاجية موثوقة وفعالة من حيث التكلفة عبر بيئات الرعاية الصحية العامة والخاصة.

- لا تزال كندا تبرز باعتبارها مركزاً رئيسياً للنمو بالنسبة لسوق مفاتح الهاوية الداخلية، مدفوعة بخبرة سريرية قوية في علم الانماط المعوية، وتوسيع نطاق الوصول إلى خدمات داخلية متقدمة، وزيادة التركيز على الرعاية التي تركز على المرضى وتقودها النتائج. إن تركيز البلاد على الجودة السريرية، والسلامة، والابتكار التكنولوجي يشجع مؤسسات الرعاية الصحية على تبني حلول متقدمة لأقصى درجات الهاوية من شأنها أن تحسن النتائج الإجرائية، وتدعم التدخلات الأقل غزواً، وتمتثل للمعايير التنظيمية ومعايير الرعاية الصحية المتطورة.

الولايات المتحدة الأمريكية

إن سوق الولايات المتحدة الأمريكية لسوقها للتغلب على المضايقات التي تتعرض لها في الوقت الحاضر تكتسب قوة قوية بسبب ارتفاع حجم الإجراءات الذاتية المعوية المعوية المعوية واعتماد الولايات المتحدة في وقت مبكر لتقنيات التنظير الداخلي المتقدمة. وتركز المستشفيات والعيادات المتخصصة بقوة على الدقة السريرية، والموثوقية الإجرائية، واختيار الأجهزة القائمة على الأدلة، وقيادة الطلب الثابت على الحلول الميكانيكية العالية الأداء والحلول القائمة على الطاقة. وبالإضافة إلى ذلك، فإن وجود كبار مصنعي الأجهزة الطبية، وبرامج التدريب السريري الراسخة، والمعايير التنظيمية والنوعية الصارمة يعزز سرعة استيعاب أجهزة التصعيد المتقدمة تكنولوجياً التي تركز على توحيد المقاييس الإجرائية، وسلامة المرضى، وتحسين النتائج، يعزز من مكانتها باعتبارها سوقاً تقودها التكنولوجيا والابتكار وتقودها داخل أميركا الشمالية..

(ب) أسواق معاين

وما زالت سوق كندا للوساحات الداخلية تتوسع حيث يعطي مقدمو الرعاية الصحية الأولوية لمسارات العلاج الغازية الدنيا، والكفاءة في وحدات النسخ الداخلي، والحد من المضاعفات المرتبطة بالإجراءات. فارتفاع حالات الإصابة بأمراض النزف المعوي المعوي، إلى جانب الطلب المتزايد على خدمات النسخ الداخلي التي تقدمها دائرة الصحة الوطنية، يعجل باعتماد أجهزة الهاوية الفعالة من حيث التكلفة والسهلة الاستخدام التي تدعم الناتج الإجرائي العالي. والتركيز القوي على المبادئ التوجيهية السريرية، والرعاية القائمة على القيمة، وبروتوكولات العلاج الموحدة يشكل قرارات الشراء، في حين يؤدي الاستخدام المتزايد للأجهزة المنضدية الإسعافية ودور الرعاية النهارية إلى زيادة دعم الطلب. وهذه العوامل مجتمعة تضع السوق اليابانية على أنها أداة مدفوعة بالوصول والكفاءة والاعتماد السريري القابل للقياس بدلاً من التركيز على تصنيع الأجهزة..

أمريكا الشمالية

وتتولى شركات راسخة أساساً قيادة صناعة المظلات المغنطيسية الداخلية، ومن بينها:

- مناسخ ميكرو تيك تسي (الصين)

- شركة تايوونغ الطبية المحدودة (كوريا الجنوبية)

- Oveesco اندوسيس ميكروجين AG (الصين)

- (الولايات المتحدة الأمريكية)

- أرغون الأجهزة الطبية (الولايات المتحدة)

- شركة Olimpus Corporation (اليابان)

- شركة Science Corcor (الولايات المتحدة الأمريكية)

- )الولايات المتحدة الأمريكية(

- ميدترونيك (أيرلندا)

- (الولايات المتحدة الأمريكية)

- EERBE Elektromedizin GmbH )الصين(

- KG (الصين)

- إحصاء طبي (اليابان)

- إندوسسكوبي تكنيك غيرهارد (الصين)

- (الولايات المتحدة الأمريكية)

- (الولايات المتحدة الأمريكية)

- (اليابان)

- ب. براون سي (الصين)

- المجموعة الواحدة (بلجيكا)

التطورات الأخيرة في أمريكا الشمالية

- وفي كانون الأول/ديسمبر 2025، ضاعفت أولمبوس التزام صندوق رأس مال الشركات من خلال إطلاق الصندوق الثاني لمغامرات أولمبوس للابتكار بمبلغ إضافي قدره 150 مليون دولار للاستثمار في مشاريع MedTech الناشئة التي تركز على المعالجة الداخلية، والتشخيص، والصحة الرقمية، وما يتصل بها من مجالات الابتكار لتعزيز النمو الطويل الأجل والقيادة التكنولوجية.

- في أكتوبر/تشرين الأول من عام 2025، أعلنت بوسطن سيني العلمية عن اتفاق لاقتناء شركة نالو ميديتش، وهي شركة خاصة للأجهزة الطبية تركز على تكنولوجيات التنشيط العصبي القابل للزرع للألم المزمن. وكان الاقتناء في وضع يسمح بتعزيز حافظة بوسطن العلمية للتعديل العصبي، وتسريع الإبداع في إدارة الألم، وتوسيع خيارات العلاج للمرضى الذين يعانون من ظروف ألم مزمنة.

- في أكتوبر/تشرين الأول، أعلنت شركة كونميد كوربوريشن خروجاً استراتيجياً من أعمالها في مجال علم التغذية، وجردت خطوط منتجاتها من مؤشر جي آي وما يتصل بها من أصول كجزء من عملية إعادة تنظيم الحافظة للتركيز على الحلول الجراحية والتقويمية الأساسية. وكان التحرك في وضع يسمح بتبسيط تركيز الشركة على المنتجات، وصقل الاستثمار في المجالات الإجرائية ذات النمو المرتفع، وتحسين الإيرادات الطويلة الأجل وملامح الهامش من خلال إعادة تخصيص الموارد من أجل منصات الأجهزة الرئيسية والتكنولوجيات الناشئة التي وضعتها اللجنة.

- في أغسطس/آب من عام 2025، وافقت إدارة الأغذية والعقاقير في الولايات المتحدة على الدراسة السريرية الأولى من نوعها للدواء المُعَدَّل للدواء المُعَدَّل للدواء المُعَدَّل للطب المُطَبَّق، وهي الدراسة التي أجريت على قسطرة من بالون PTA المُطَلَّق على مقياس EVEREO 18 من طراز EVERO 18 من طراز ELULImus، مما مكَّن من تقييم سلامته وفعاليته في علاج الأمراض الشريانية العرضية الجانبية. وكان القرار بمثابة معلماً في تكنولوجيا البالونات المُغَلَّبة بالعقاقير، ودعم تقدم كوك في الجيل القادم من العلاجات الوعائية الداخلية الرامية إلى الحد من شفاء الأمراض وتحسين سلامة السفن على المدى البعيد في المرضى الذين يعانون من أمراض شريانية أقل تكاثراً.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

Table of Content

مقدمة ١

هدف الدراسة في

سوق

أولا - لمحة عامة عن السوق

مـا

الاس

ثانيـة

غير

سابعاً -

السنة

حالات الطوارئ وال

٢-٥ مــادة مــادة مــد المــواد

مع رئيسي

المتعددة المتعددة

جـد فـد فـد فـرص

ثانيا - تحليل المخاطر

قاعدة الغطاء

٢-١١ مصادر أخرى

٢-٢-٦-

أولاً - موجز

٤ ناظرا

٤/١ - تحليل

رابعاً -

رابعا -١ تحليل

)الاستعراض الشامل للعلوم الطبية(

٤-٢- عرض عام لفوات فـتات المنتجات - السوق

استعراض عام للنواتج - الأمراض

أولاً - عرض عام للسنــد -

السنة

والنتائـج

رابعاً - النظر في التكاليف وال

رابعاً - المنافسة والتكامل

رابعا -

لجنة

رابعاً - إجراءات التوريد والاتفاقات

استخدام

الاتجاهات

٩-٩ الاستنتاج

٤- تحليل

درجة الجودة والقامة - السوق

٤-٤,٤,٤ في المائة من البلدان

رابعاً - الاستراتيجية والإدارة

الجريمة المنظمة والتعاون

الغلاف الجوي

المكونات المعدنية والمنظومات

المواد الكيميائية والمواد

المواد الطبيعية والبيولوجية

رابعاً - النظـران

رابعاً-

التقدم المحرز فـي

تعزيز

٤-٦-٢ النهوض بالنظم التعاونية

أولاً- البلاغات

التحقيق في التكنولوجيات

تطوير الأدوات العملية المتعددة

نظم جرد الاستخدام المحسنــة ونظـم

الاستنتاج

تحليل

أولا - لمحة عامة

4-7-2 مواد العنف ومكوناتها

4-7-7-3 تحديد وتشـ

الدورة الرابعة

٤,٥ ٤

4/7-6-

الاستنتاج

لجنة الخبراء التابعة

أولا -

الاتحادات والمشتريات المالية

المجموع الكلي للتكلفة

رابعاً -

والدعـم والتدريـب والتعليـم

النظم النوعية والخطوط الإرشادية

رابعاً - التمثيل، وتنسيق الفقر، وأداء ما بعد

التغـوث والتنشـيط

تقييم المخاطر

٤-١

٤-٠١-١ شبكات

٤-٠١-٢ ضمان ضمان الأداء

٤-٠١-٣

٤-٠١-٤ المستقبل

٤-١١ تغير المناخ

الشواغل البيئية

الفريق العامل المعني

دور الجهة

التوصيات

٤-٢١ نظام المعلومات والاتصالات والتحليل الاستراتيجي

أولاً - تحليل

المحتويات

الأشخاص والمعنيون

4-2-1-3 التلوث والشراك

٤-٤-١-١-٤

رابعاً-

من التنمية

ماذا الأشكال

استراتيجيات وأساليب

٤-٢١-٦ تقييم المخاطر وتخفيف

٤-٢١-٧ الميــب

٤-٣١ تحليل الأسعار

رابعاً-

رابعاً-

الأنشطة

٤-١٤

أولا- مقدمة

الفريق العامل المعني

٤-٤/٤-٤ عدد مقدمي الخدمات

٤-٤١-٤ الاستنتاج

٥ - القطـار والتأثيـر علـى السـواقـع

أولاً - لمحة عامة

من أصل صاروخي (ت) جديد في

خامساً/سادساً

لجنة الخبراء الاستشاري

على

5-5-5-1 شراء وسائل

رابعاً -

وما يتصل

رابعاً - مراقبة السوق

ثالثاً - التقدم المحرز في

جدول الأعمال المؤقت

موضــع

لجنة

عملية

أولاً - الحالة

التجارة فيما بين البلدان

اتفاقات التجارة الحرة

المستوطنات

منح الاعتماد )الم

٥-٥-٤ الدورة التدريبية

النماذج الإضافية المقدمة إلى مصادر

إنشاء السـوسات/المراكـس

من المنتجات

أولاً

ثالثاً - معايير ضمانات الأمان

أولاً - مقدمــة وراســع المواد

6-2 النقل التجاري والنقل

التحقق من

استعراض عام

لجنة

في حالات

السكان الذين

ثانياً-

إعلان ووضع برامج

سابعا ما

رابعا - ١-١ التكاليف العالية والتكرار الكبير والتكرار التقني للاجــالات

٧-٢/٢ في البلدان المنخفضة

ماذا

التقدم المحرز في

٧-٣-٢ الاستثمار في الأسواق التجارية )آسيا والمحيط الهادئ، أمريكا اللاتينية(

٧-٣-٣ تعزيز اعتماد الحلول الموطنـة والمحلـلات

الأرقام

قضايا الاجـراءات

في عمليات إعادة التحريج والتكرار

٨ - مركــات نظــم مــرتــب نوع

أولاً - مقدمة

مــس

في سوق الأساس

8-2-1 الشركات الإحصائية

مؤشرات إحصائية في سوق

المبادئ التوجيهية من خلال عمليات حفظ السلم

٨-٢-١-١-١-١-١-١-١-٢ المراقبة )العمليات( للمعاملات

8-2-1-2-1- في المشاريع التجارية، بحسب المواد

٨-٢-١-١-١-١-١

8-8-2-1-2-2 تيتانييوم

8-2-2 الأدوات البديلة

٨-٢-١-١-٢ الأجهزة المستخدمة في سوق

8-8-1-2-1-1- 1-1-1 شهادتي عمل

أوب

٨-٢-١-١

المواد الأخرى

٨-٢ /٢-

٨,٢ في النرويج

8-2-2 أوروبا

٨-٢-٢-٢-٣ آسيا

٨-٢-٢-٢-

أولاً- 8-2-5 الشرق الأوسط

٨/٨٨

٨-٣-١ الأمراض غير المعدية في سوق الأساس

أولا - مقرر بشأن

٨-٨-١-١ مشاكل الصحة

٨-٨-١-١-١-

٨-٣-١-١-١-١-١-١- التعاون في سوق المعدات الخطرة حسب نوع الطاقة

8-8-1-3-1-1

8-81-3-1-2 الشرطة

٨-٣-١--٣-٢ التعاون في مجال الشرطة في سوق المعدات الخطرة، حسب الطلب

٨-٨-١-٣-١

٨-٨-٣-٣-٢-٢ أقل وزن ثاني

المواد الأخرى

٨-٣-٣-

٨-٨-٢ النرويج

8-8-2-2 أوروبا

٨-٨-٢-٣ آسيا والمحيط الهادئ

٨-٢-٢-

٨-٢-٥ الشرق الأوسط

المدنية وما

في السوق الأساسية الأساسية

شركة PPEPI

٨-٤-١-٢ سلف )الرأس(

أولاً -

8-4-1

أولاً- العناصر التي

٨-٤ في المائة من دولارات

٨,٨,٢

8 8-2-2 أوروبا

٨-٤-٢-٣ آسيا الوسطى

٨-٤-٤

٨-٤-٢-٥ الشرق الأوسط

الأخرى

الأشخاص الآخرين في سوق الأساس

8-5-1-1 النرويج

8-8-1-2 أوروبا

٨-٨-١-١-

٨,٨,٨,١ في الجنوب

أولاً- 8-5-1 الشرق الأوسط وأفريقيا 8-8-1

مــرتــب الهيئــة

أولاً- مقدمة

السنة

في سوق الأوراق

تنفيذ إدارة

بيع البضائع

عـد

في السوق الأساسية

تاسعاً -

9-2-2 أوروبا

٩-٢-٢-٢-٢ منطقة آسيا الوسطى

مـن

الشرق الأوسط

السنة

الفقــرات مــن

بالتداولكوليوني

لجنة منع

الفقــرات مــن البلــدان الأعضاء في

أولا - مقدمــة

9-2-2 أوروبا

٩-٢-٢-٣ آسيا الوسطى

في أمريكا الجنوبية

الشرق الأوسط

مؤتمر القمة

في السوق الأساسية

حتى الآن

9/4-1-2 أوروبا

آسيا والمحيط الهادئ

في أمريكا الجنوبية

الشرق الأوسط

جهات أخرى

الأشخاص الآخرين في سوق أساسـي

حتى الآن

9-5-1-2 أوروبا

آسيا والمحيط الهادئ

جنوب افريقيا

أولاً- الشرق الأوسط

مرقــط فــي السياســات

أولا - لمحة عامة

الشامل

في السوق الأساسية

10-2-1-1

أولاً-

١٠-٢-٢-٣-

10-2-2 إطلاق الغازات الاستوائية في السوق الأساسية

الأجهزة

10-2-2-2-2 الأجهزة

المصادر والأروب

10-2-2-4 الجهات الأخرى

الانبعاثات في السوق الأساسية

10-2-3-1 - أمريكا الشمالية

١٠٢-٢-٢ أوروبا

١٠-٢-٣-٣ آسيا والمحيط الهادئ

١٠-٢-٤-٤ في الولايات المتحدة

١٠-٢-٥- الشرق الأوسط وأفريقيا

غير

غير الشامل للاستفـاس فــي مواقــس

10-3-1-1 التلقيف بالهواء

١٠-٣-١-٢

غير الشامل للاسـتاسطـر فـي مركـز

الأجهزة الفضائية

10/3-2-2 الأمراض البرية

أولاً-

المواد الأخرى

10-3-3 عدم انتشار الأسلحة غير الشامل للتجارب النووية في السوق الأساسية

١٠/٣-١ - أمريكا الشمالية

10-3-3/2 أوروبا

١٠-٣-٣-٣-٣ منطقة آسيا الوسطى

١٠-٣-٤-٤ جنوب افريقيا

الشرق الأوسط

الإدارة

10-4-1 الإدارة الثلاثية في سوق الأساس، حسب نوع الإنتاج

الأجهزة

10-4-4-4-1-2 الإصابات

أولاً- المبادئ والمواد المدنية

10-4-4-4 المصادر الأخرى

١٠-٤ الإدارة الثلاثية في سوق الأساس

١٠/٤-١ - أمريكا الشمالية

١٠-٤-٢ أوروبا

١٠-٤-٢-٣ آسيا الوسطى

١٠-٤/٤/٤ في أمريكا الجنوبية

١٠-٤-٢-٥ الشرق الأوسط وأفريقيا

(10) مواد أخرى

٠١-١-١ الأشخاص الآخرين في سوق الأساس

١٠-٥-

10-5-1-2 أوروبا

١٠-٥-١-١-

١٠-١-١-

٥-١-

١١ بــاء فــي الســنــة

أولا - لمحة عامة

١١-٢ المستشفيات

١١-١ المستشفيات في سوق التأمين على ظهر السفن، حسب نوع

١١/٢-١ المنشورات

١١-٢-٢-

١١-٢-٢ المستشفيات في سوق الأساس

١١/٢-١-

11-2-2-2 أوروبا

١١-٢-٢-٣ منطقة آسيا والمحيط الهادئ

١١-٢-٢-٤-

١١-٢-٥- الشرق الأوسط وأفريقيا

١١-٣ مراكز

مركزــات مراكــب مـن مراكـب مـن مراكـب مراكـب

١١-٣-١-

١١-٣-١-٢ أوروبا

١١-٣-٣-٣- آسيا والمحيط الهادئ

١١-٣-١-٤- جنوب افريقيا

١١-١-١-٥-

أولاً -

في معايير المحاسبة المتعلقة بالخصيـات

١١-٤-١-

١١-٤-١-٢ أوروبا

١١-٤-١-٣ آسيا والمحيط الهادئ

١١-٤-٤-٤-

١١-٤-١-٥- الشرق الأوسط والجنوب

١١-٥ مواد أخرى

١١-٥-١-

١١-٥-

11-5-1-2 أوروبا

١١-٥-١-١-

١١-١-١-

أولاً-

في أمريكا الشمالية

أولا - لمحة عامة

١٢-٢

12-2-1 المبيعات المباشرة في شكل أساس افتراضي، حسب نوع

٢-٢-١ ـ

ثانيا - ٢ - ٢ -

12-2-2 المبيعات المباشرة في سوق الأساس

12-2-2-1 أمريكا الشمالية

12-2-2-2 أوروبا

١٢-٢-٢-٣ منطقة آسيا والمحيط الهادئ

١٢-٢-٢-٤ - جنوب افريقيا

12-2-2-5 الشرق الأوسط وأفريقيا

١٢-٣

١٢/١- مبيعــات فــي مواقــع

12/3-1-1 - أمريكا الشمالية

12/3-1-2 أوروبا

١٢-٣-١-٣-

١٢-٣-١-٤-

مجموعـان

مــن

١٣/١

13-1-1 الولايات المتحدة الأمريكية

٣١-٢ كندا

المكسيك

في أمريكا الشمالية

تحليل مخاطر

١٥ ١٥ تحليل المخاطر

ستة عشر

أولاً - مقدمــة

١٦-١/١ر مراجعة حسابات الشركة

٦١/٢

161-3 تحليل المخاطر

1 -1 - 1 - 1 - 1

التنمية في

١٦-٢ الصندوق العلمي

16-2-1 خسار الشركة

16-2-2

حل مشكلة

16-2-4 البولي البولي البوليفي

التنمية

٦١ - ٣

١٦-٣/١ مراجعة حسابات الشركة

٦١-٣

16-3 تحليل مخاطر

البوليفيا

التنمية في

٦١-٤

16-4/1 تقييم الممتلكات

٦١-٤

16-4-4 تحليل مخاطر العمل

١٦-٤-٤ بروميد البولي البولي البولي

التنمية

٦

16-5-1 خدمات

٦١-٥/٢ تحليل

16-5 البولي البوليفي

١٦-٤ التنمية

٦١ -

١٦-٦-١- فحص الممتلكات

١٦-٦-٢ البولي البوليفي

وضع وضع

باء -

١٦-١- ١-

16-7-2 البولي البوليفي

١٦-٧-٣-

16-8

١٦-٨-١ فحص

١٦-٨-٢ البولي البوليفي

التنمية

16-9 تاريخ الاجتمـاع، التوجـيـة

١٦-٩-١- ١ر٦١-

16-9-2 البولي البولي البوليفي

١٦-٩-٩-٣-

الفريق العامل

١٦-١٠-١-

١٦-١٠-٢ البولي البوليفي

١٦-١٠-٣-

16-11 نقطة البداية، إضافة.

١٦-١١-١-

١٦-١١-٢ بروميد المنتجات

٦١-١١-٣-٣ -

للسياسـة

١٦-١٢/١- فحص الممتلكات

١٦-١٢-٢ البولي البولي البوليفي

١٦-١٢-٣ التنمية

٦١-٣١

١٦-١٣-١ فحص

٦١-٣١-٢

١٦-١٣-٣ البولي البوليفي

١٦-١٣-٤ التنمية

16- 14 كانون الثاني/يناير 1992(ب)

١٦-١٤-١-

٦١-٤١-٢

١٦-١٤-١-٣ البولي البوليفي

١٦-١٤-٤ -

ك. ك. ك. ك.

١٦-١٥-١ فحص مرتبات الموظفين

١٦-١٥-٢ البولي البوليفي

١٦-١٥-٣-٣ -

٦١-٦١ مـديـتـالـيا سـرل

١٦-١٦-١٦-١ فحص

16-16-16-2 البولي البوليفي

١٦-١٦-٦-٣ التنمية

١٦-١٧ مؤتمر الأمم المتحدة

١٦-١٧-١ مراجعة حسابات الشركة

١٦-١٧-٢ البولي البوليفي

١٦-١٧-٣ التنمية

16-18 - مـتـو

١٦-١٨-١ فحص

١٦-١٨-٢ البولي البوليفي

١٦-١٨-٣-

سادساً -

١٦-١٩-١ فحص

١٦-٩١-٢ بروميد المنتجات

١٦-١٩-٣-

١٦-٢

١٦-٢٠-١-

١٦-٢٠-٢-

التنمية

٦١/٦١

١٦-٢١-١ فحص

٦١-١٢-٢

١٦-٢١-٣ البولي البولي البوليفي

١٦-٢١-٤ التنمية

١٧

١٧-١

17/1

17-1-2 البوليفي

التنمية

الصحة الأساسية

17/2/1

17-2-2

17-17-2-3 البولي البوليفي

أولاً - مقدم من

17-3 هنري شاين، المؤكّد

17-3/1

هذا المبلغ

17-3-3 البوليفي

تقرير

١٧-٤ - الأضــاف الطبيــة للسمــاك

17-4/1 جواز الشراء

17-4/4 البوليفيا

١٧٤/٤

١٧-٥

١٧-١- ١-١ خدمات

17/5 البوليفي

١٧ تموز/

تقرير

سابعاً

List of Table

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

الجدول ٣ الكهنيات الإحصائية في سوق أسعار الفائدة للأنواع، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٤ الأدلة الاحصائية العليا في سوق سوق المواد، حسب المادة، ٢٠٨/٢٠٣٣ )بالآلاف(

(بآلاف دولارات الولايات المتحدة)

الجدول ٦ - الأجهزة الهيدروهادمية المساعدة في سوق أساســات الاستعــداد

الجدول ٧ - الأمراض غير المعدية في سوق الأساس الافتراضي، حسب نوع الجنس، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٨

الجدول 9

الجدول ٠١ - الأمراض غير المعدية في سوق الأساس

الجدول ١١ المئـة ١١ المئـات والآثـاث التعويضـات الأساسيـة والمستحقـات فـي مـرتـكـشـات الأساسـات

)بآلاف دولارات الولايات المتحدة(

الجدول ٣١ - التبرعات الأخرى في سوق الأساس

(بآلاف دولارات الولايات المتحدة)

جدول الأعمال الخامس عشر

جدول الأعمال 16

)بآلاف دولارات الولايات المتحدة(

الجدول ٨١

في السوق السوقية في مرحلة ما بعد

الجدول ٠٢

(بآلاف دولارات الولايات المتحدة)

)بآلاف دولارات الولايات المتحدة(

الجدول ٣٢

الجدول ٤٢

الجدول ٥٢

الجدول ٦٢ تصنيف فئات المنتجات، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٧٢

الجدول ٨٢ الإدارة التاريخية في السوق الأساسية

الجدول ٩٢ الإدارة التاريخية في سوق الأساس

الجدول ٠٣

)بآلاف دولارات الولايات المتحدة(

الجدول ٣٢ مستشفيات الصحة العامة في السوق السوقية لمستواس التخطيطي، حسب النوع، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٣٣ مــن محاضــر الاســعار فــي مواقــع المقــر فــي ٣١

مراكز

في السوق القياسية لمستواســط الاستعــداد، حسب المنطقة، ٢٠٨٨/٢٠٣٣، )بالآلاف(

الثاني - البلاغات المقدمة من الدول الأطراف الأخرى في سوق الأساس

(بآلاف دولارات الولايات المتحدة)

الجدول ٣٨

الجدول ٣٩

الجدول ٤٠ بيــد بيــان بيــع فــي مواقــع المقــر فــي

(بآلاف دولارات الولايات المتحدة)

الجدول ٤٢ المستوى الأساســي

(بآلاف دولارات الولايات المتحدة)

الجدول ٤٤ الكهنية الاحصائية في سوق المواد الكيميائية للكيميــات، ٢٠١٨-٢٠٣٣ )بالآلاف(

في سوق أسعار الفائدة على المعدات، بحسب المواد، ٢٠٨/٢٠٣٣ )بالآلاف(

)بآلاف دولارات الولايات المتحدة(

الجدول ٤٧ - الأمراض غير المعدية في سوق الأساس الاستوائية، حسب نوع الجنس، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٤٨

الجدول ٤٩

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

جدول الأعمال 52

الجدول ٣٥ الجدول ٥٣

(بآلاف دولارات الولايات المتحدة)

الجدول ٥٥

الجدول 56 تصنيف المنتجات، 2018-2033 (بالآلاف)

جدول الأعمال ٥٧

الجدول ٥٨ تصنيف المنتجات، ٢٠٨/٢٠٣٣ )بالآلاف(

الجدول ٥٩ الإدارة التاريخية في سوق الأساس الافتراضي، حسب نوع المنتج، ٢٠٨/٢٠٣٣ )بالآلاف(

)بآلاف دولارات الولايات المتحدة(

الجدول ٦١ المستشفيات الرئيسية في سوق التأمين الأساسي للاحصاء، حسب النوع، ٢٠٨/٢٠٣٣ )بالآلاف(

)بآلاف دولارات الولايات المتحدة(

الجدول ٦٣

الجدول ٦٤ - أسعار السوق الأساسية للأساس القياسي، حسب نوع المنتج، ٢٠١٨-٢٠٣٣ )بالآلاف من دولارات الولايات المتحدة(

الجدول ٥٦ الأجهزة الهيدروهنية القياسية المستخدمة في الولايات المتحدة في السوق الأساسية للانتاج، حسب نوع الجنس، ٢٠١٨-٢٠٣٣ )بالآلاف(

)بآلاف دولارات الولايات المتحدة(

الجدول ٧٦ المنشورات المصرفية الأمريكية في سوق أسعار الفائدة على المعدات، حسب المادة، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٦٨ المعدات المستخدمة في تقييم المعدات في سوق أسعار أسعار الصرف للأنواع، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٦٩ الأجهزــة الفئــة فــي مواقــط الاستعــراضيــات فــي مركــز الاستعــداديــة

الجدول ٠٧ الجدول ٠٧ الجدول ١ - التنسيق بين الببولارات في سوق أسعار الصرف في مجال الاصابـات الأرضيـة، حسب نوع الطاقة، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٧١

الجدول ٧٢ المُعد َّات والمُحَتَّات الكيميائية في الولايات المتحدة في السوق الأساسية الأساسية للكربون، حسب نوع الجنس، ٢٠١٨-٢٠٣٣ )بآلاف دولارات الولايات المتحدة(

(بآلاف دولارات الولايات المتحدة)

الجدول ٤٧ الجدول ٤٧ الدراسات التي أعدتها الولايات المتحدة الأمريكية في مجال الدراسات المتعلقة بالأخلاقيات في السوق التخطيطية الأساسية، حسب نوع الجنس، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٥٧ الجدول ٥٧ الجدول ١ - الجدول ٧٥

الجدول ٧٦ المستوى السوقي للأساسي القياسي للأساسي القياسي للولايات المتحدة، حسب الطلب، ٢٠١٨-٢٠٣٣ )بالآلاف من دولارات الولايات المتحدة(

الجدول ٧٧ الجدول ١١٨-٢٠٣٣ )بآلاف دولارات الولايات المتحدة(

الجدول ٨٧ الجدول ٧٨ الجامستـين الاستـنستـاء الـمـتـحـدة مـن الرسـاطـات فـي مـواعـد الأساسـي للديمـات

الجدول ٩٧ الولايات المتحدة الأمريكية

الجدول ٨٠ الولايات المتحدة الأمريكية، التي تُدفع في السوق الأساسية

الجدول ٨١ الإدارة الفنية للولايات المتحدة في السوق القياسية للأسعار الأساسية، حسب نوع المنتج، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٢٨ الجدول ٢٨

الجدول ٨٣ المستشفيات الأمريكية في السوق السوقية للمستوى الافتراضي، حسب النوع، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٤٨ الجدول ٤٨

الجدول ٨٥ المبيعــات غيــر المبالــغ المبالــغ المتجــرات غيــر المباشرــة فــي نظــام النظــر الأساســي فــي

الجدول ٨٦ مركز الدراسات العليا في كندا، حسب نوع المنتج، ٢٠١٨-٢٠٣٣ )بالآلاف(

)بآلاف دولارات الولايات المتحدة(

قائمة بمنشورات الأمم المتحدة، حسب النوع، 2018-2033 (بالآلاف)

مؤشرات كانانـا الإحصائية في سوق أسعار الفائدة على المواد، بحسب المواد، ٢٠٨/٢٠٣٣ )بالآلاف(

قائمة بالوسائل الممكن استخدامها في سوق أسعار الفائدة على المواد

الجدول ٩١ - الأمراض السرطانية في سوق الأساس الاستوائية، حسب نوع الجنس، ٢٠١٨-٢٠٣٣ )بالآلاف(

الجدول ٢٩ كانـان الأول/ديسمبـر - الاجـادة التعويضيـة فـي سـكـتـيـك الأسـرة فـي الأسكـان، حسب نوع الطاقة، ٢٠١٨-٢٠٣٣ )بآلاف دولارات الولايات المتحدة(

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

جدول الأعمال 96 كندا في إطار خطة العمل الأساسية في مرحلة ما بعد

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

)بآلاف دولارات الولايات المتحدة(

(بآلاف دولارات الولايات المتحدة)

الجدول ١٠١ كندا غير

الجدول ١٠٢ كندا التي تُدفع في السوق السوقية الأساسية

الجدول 103 إدارة كندا في سوق الأساس

)بآلاف دولارات الولايات المتحدة(

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

الجدول ١٠٧

(بالآلاف)

(بآلاف دولارات الولايات المتحدة)

)بآلاف دولارات الولايات المتحدة(

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

الجدول ٣١١ - الأمراض الوراثية في سوق الأساس

(بآلاف دولارات الولايات المتحدة)

الجدول ٥١١ - التقييم المكسيكي للفوائد الأولية في سوق المواد الخطرة، حسب الطلب، ٢٠١٨-٢٠٣٣ )بالآلاف من دولارات الولايات المتحدة(

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

المكسيك في سوق الأوراق المالية، حسب نوع الجنس، 2018-2033 (بالآلاف)

)بآلاف دولارات الولايات المتحدة(

(بآلاف دولارات الولايات المتحدة)

(بدولارات الولايات المتحدة)

الجدول ٢٢١ - المكسيك

الجدول ٣٢١ الميسكيــس المكسيكيــن غير الشاملين لمـن الاستسـتراتستـان الـمـتخـدم فـي مـرتـكـسـات فـي مـواعـد

الجدول ٤٢١ الميسكيـس المكسيكيـن غير الغازيـة الاستـنستـياس الاستـرقالـي الـمـتـرك فـي مـرتـكـسـاتـسـاسـاسـاسـاسـاسـمـاً

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

(بآلاف دولارات الولايات المتحدة)

الجدول ٩٢١

List of Figure

أولاً - مـرتـكـشـسـسـسـسـسـاسـسـدخطـس فـاء

ثانياً - في أمريكا الشمالية

في شمال الولايات المتحدة الأمريكية

في ٤ شمالي الولايات المتحدة

في أمريكا الشمالية ٥ - مخطــط فــي

ثانيا - النظر في

في أمريكا الشمالية ٧

ثانياً - مقدمة 8 -

ثانياً - تحليل

سوق سوق الأوراق العاملة في السوق

في أمريكا الشمالية

ثانياً - الاجزاء الثاني عشر من الاجزاء التي تُعِدُّ على أساس السوق، بحسب نوع المنتج

سادساً - موجز تنفيذ

في أمريكا الشمالية

القضايا الأساسية التي من المتوقع أن تؤدي إلى تحيـل نغـر

الفصلان الثاني والنوع الثاني من الجزء الأول من الجزء الأول من الجزء المتعلق بالهيد

تقييم الأصول

تحليل

مُعَدَّة 19 من دولارات الولايات المتحدة الأمريكية

الشكل ٢٠ - سوق السوق: حسب نوع المنتج، كجر )٢٠٢٥-٢٠٣٢(

المصدر: حسب نوع المنتج، كَر (2025-2032)

المصدر: نوع المنتج، مصــروف الفــلاد )٢٠٢٥-٢٠٣٢(

مـرتـكـيـت فـي سـنـاء المـرتـب فـي سـنـة ٢٣

الشكل ٢٤ - خط أساس

المصدر: حسب الإجراء، 2026-2033 (بآلاف دولارات الولايات المتحدة)

مرقــم فــي أمريكا الشمالية، حسب الطلب،

الشكل ٢٧ - خط أساســة الأساســية

الشكل ٢٨ - خط أساســة

المصدر: حسب الطلب، 2026-2033 (بآلاف دولارات الولايات المتحدة)

مُعَدّة 30 سُنْة سُنْطَسَسْطَس، مُسَمَّمًا،

(بآلاف دولارات الولايات المتحدة)

المصدر: حسب الاستخدام، 2026-2033 (بآلاف دولارات الولايات المتحدة)

المصدر: حسب الاستخدام، 2026-2033 (بآلاف دولارات الولايات المتحدة)

مرقــم فــي أمريكا الســاء الســكان

)بآلاف دولارات الولايات المتحدة(

)بآلاف دولارات الولايات المتحدة(

)بآلاف دولارات الولايات المتحدة(

في أمريكا الشمالية 38

المصدر: الشركة )نسبة مئوية(

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.