North America Surgical Sutures Market

Marktgröße in Milliarden USD

CAGR :

%

USD

15.18 Billion

USD

25.21 Billion

2025

2033

USD

15.18 Billion

USD

25.21 Billion

2025

2033

| 2026 –2033 | |

| USD 15.18 Billion | |

| USD 25.21 Billion | |

| % | |

|

Marktsegmentierung für chirurgisches Nahtmaterial in Nordamerika nach Produkt (Nahtfäden und automatische Nahtgeräte), Typ (Multifilament- und Monofilament-Nahtmaterial), Anwendung (Herz- und Gefäßchirurgie, Allgemeinchirurgie, Gynäkologische Chirurgie, Orthopädische Chirurgie, Augenchirurgie, Kosmetische und Plastische Chirurgie sowie Sonstige Anwendungen) und Endnutzer (Krankenhäuser, ambulante Operationszentren, Kliniken und Arztpraxen) – Branchentrends und Prognose bis 2033

Marktgröße für chirurgisches Nahtmaterial in Nordamerika

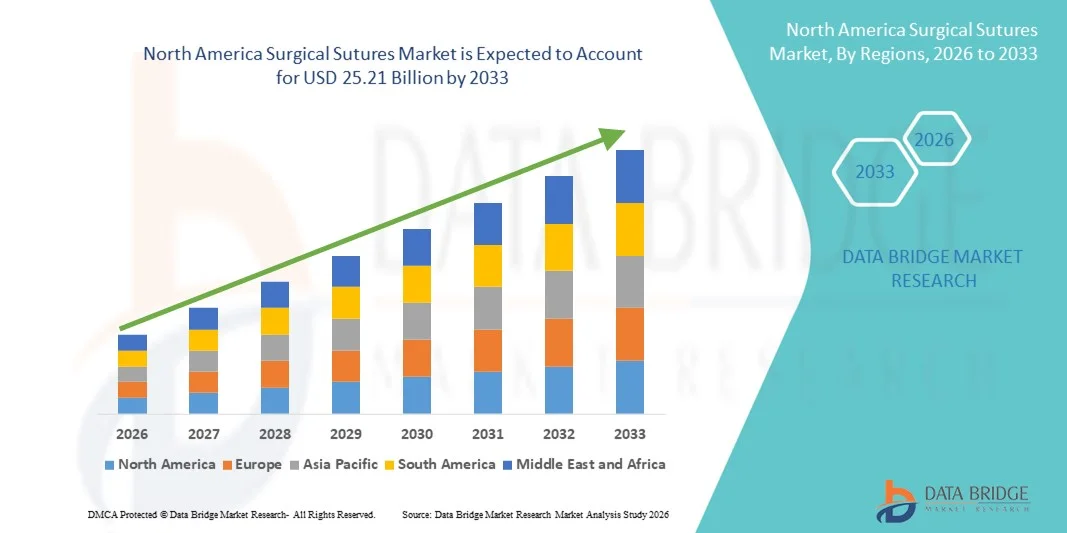

- Der nordamerikanische Markt für chirurgisches Nahtmaterial hatte im Jahr 2025 einen Wert von 15,18 Milliarden US-Dollar und wird voraussichtlich bis 2033 auf 25,21 Milliarden US-Dollar anwachsen , was einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 6,55 % im Prognosezeitraum entspricht.

- Das Marktwachstum wird maßgeblich durch die weltweit steigende Anzahl chirurgischer Eingriffe und die kontinuierlichen technologischen Fortschritte bei Wundverschlussmaterialien angetrieben, was zu verbesserten Operationsergebnissen in Krankenhäusern und Gesundheitseinrichtungen führt.

- Darüber hinaus tragen die steigende Nachfrage nach effektiven Wundversorgungslösungen, die zunehmende Verbreitung chronischer Erkrankungen und die wachsende Beliebtheit minimalinvasiver Eingriffe dazu bei, dass chirurgisches Nahtmaterial zu einem unverzichtbaren Instrument in modernen chirurgischen Verfahren wird. Diese zusammenwirkenden Faktoren beschleunigen die Akzeptanz von chirurgischen Nahtmaterialien und fördern so das Wachstum der Branche erheblich.

Marktanalyse für chirurgisches Nahtmaterial in Nordamerika

- Chirurgisches Nahtmaterial, das zum Wundverschluss bei chirurgischen Eingriffen verwendet wird, ist aufgrund seiner Wirksamkeit bei der Förderung einer ordnungsgemäßen Wundheilung, der Minimierung des Infektionsrisikos und der Unterstützung einer Vielzahl chirurgischer Anwendungen ein zunehmend wichtiger Bestandteil moderner Gesundheitssysteme in Krankenhäusern und chirurgischen Zentren.

- Die steigende Nachfrage nach chirurgischem Nahtmaterial wird in erster Linie durch die zunehmende Anzahl chirurgischer Eingriffe, die steigende Verbreitung chronischer Krankheiten und die wachsende Anwendung fortschrittlicher Wundverschlusstechniken in der modernen Gesundheitsversorgung angetrieben.

- Die USA dominierten 2025 mit einem Umsatzanteil von 35,6 % den Markt für chirurgisches Nahtmaterial. Dies ist auf eine fortschrittliche Gesundheitsinfrastruktur, ein hohes Volumen an chirurgischen Eingriffen und die starke Präsenz führender Medizinproduktehersteller zurückzuführen.

- Kanada dürfte im Prognosezeitraum die am schnellsten wachsende Region im Markt für chirurgisches Nahtmaterial sein, mit einer prognostizierten durchschnittlichen jährlichen Wachstumsrate (CAGR) von 8,9 %. Gründe hierfür sind steigende Gesundheitsausgaben, zunehmende Operationszahlen und die wachsende Verwendung moderner Wundverschlussmittel.

- Das Segment der Nahtfäden dominierte 2025 mit einem Marktanteil von 72,8 %, was auf deren breite Anwendung in einer Vielzahl chirurgischer Eingriffe, darunter Herz-Kreislauf-, orthopädische, gynäkologische und allgemeine Chirurgie, zurückzuführen ist.

Berichtsumfang und Marktsegmentierung für chirurgisches Nahtmaterial

|

Attribute |

Chirurgische Nahtmaterialien – Wichtigste Markteinblicke |

|

Abgedeckte Segmente |

|

|

Abgedeckte Länder |

Nordamerika

|

|

Wichtige Marktteilnehmer |

|

|

Marktchancen |

|

|

Mehrwertdaten-Infosets |

Zusätzlich zu den Erkenntnissen über Marktszenarien wie Marktwert, Wachstumsrate, Segmentierung, geografische Abdeckung und Hauptakteure enthalten die von Data Bridge Market Research erstellten Marktberichte auch detaillierte Expertenanalysen, Patientenepidemiologie, Pipeline-Analyse, Preisanalyse und regulatorische Rahmenbedingungen. |

Markttrends für chirurgisches Nahtmaterial in Nordamerika

Zunehmende Verwendung von modernen und biologisch abbaubaren Nahtmaterialien

- Ein bedeutender und sich beschleunigender Trend auf dem globalen Markt für chirurgisches Nahtmaterial ist die zunehmende Verwendung fortschrittlicher Nahtmaterialien, insbesondere bioabbaubarer und antimikrobieller Materialien. Diese wurden entwickelt, um die Wundheilung zu verbessern und das Risiko postoperativer Infektionen zu reduzieren. Im Gesundheitswesen werden vermehrt Nahtmaterialien bevorzugt, die eine höhere Zugfestigkeit, verbesserte Handhabungseigenschaften und ein vorhersagbares Absorptionsprofil aufweisen. Dies optimiert die chirurgische Effizienz und beschleunigt die Genesung der Patienten.

- Ethicon (Johnson & Johnson) hat beispielsweise antibakteriell beschichtete Nahtmaterialien wie Vicryl Plus auf den Markt gebracht, die die bakterielle Besiedlung im Wundbereich hemmen und so Wundinfektionen reduzieren sollen. Auch Medtronic bietet hochentwickelte resorbierbare Nahtmaterialien an, die einen gleichmäßigen Wundverschluss unterstützen und die Notwendigkeit des Nahtwechsels minimieren, was den Patientenkomfort und die klinischen Ergebnisse verbessert.

- Fortschritte in der Nahttechnologie haben es Herstellern ermöglicht, Materialien zu entwickeln, die während der kritischen Heilungsphase ihre Festigkeit beibehalten und sich nach Abschluss der Gewebeheilung allmählich abbauen. Diese Innovationen helfen Chirurgen, einen zuverlässigen Wundverschluss zu erzielen und gleichzeitig Komplikationen zu minimieren, die mit herkömmlichen, nicht resorbierbaren Nahtmaterialien verbunden sind.

- Zudem steigt die Nachfrage nach Spezialnahtmaterialien für minimalinvasive und roboterassistierte Eingriffe, bei denen Präzision, Flexibilität und Haltbarkeit unerlässlich sind. Chirurgen setzen zunehmend auf Hochleistungsnahtmaterialien, die bei heiklen Operationen eine bessere Knotensicherheit und Gewebeverträglichkeit ermöglichen.

- Der kontinuierliche Fokus auf Innovation und verbesserte Operationsergebnisse ermutigt Unternehmen, massiv in Forschung und Entwicklung zu investieren, um Nahtmaterialien mit optimierten Leistungseigenschaften einzuführen. Hersteller entwickeln zudem antimikrobielle und mit Widerhaken versehene Nahtmaterialien, die dazu beitragen, die Operationszeit zu verkürzen und die Wundstabilität zu verbessern.

- Da die Zahl chirurgischer Eingriffe weltweit aufgrund zunehmender chronischer Krankheiten, Traumata und der alternden Bevölkerung weiter steigt, wird ein stetiges Wachstum der Nachfrage nach technologisch fortschrittlichen chirurgischen Nahtmaterialien in Krankenhäusern, ambulanten Operationszentren und Fachkliniken erwartet.

Marktdynamik für chirurgisches Nahtmaterial in Nordamerika

Treiber

Zunehmende Anzahl chirurgischer Eingriffe

- Die weltweit steigende Anzahl chirurgischer Eingriffe, bedingt durch die zunehmende Verbreitung chronischer Krankheiten, Traumata und den verbesserten Zugang zur Gesundheitsversorgung, treibt die Nachfrage nach chirurgischem Nahtmaterial maßgeblich an. Da Operationen in verschiedenen medizinischen Fachbereichen immer häufiger durchgeführt werden, wächst auch der Bedarf an zuverlässigen Wundverschlusslösungen stetig.

- So werden beispielsweise laut globalen Gesundheitsschätzungen jährlich weltweit Millionen von chirurgischen Eingriffen durchgeführt, darunter Herz-Kreislauf-Operationen, orthopädische Eingriffe und Kaiserschnitte. Unternehmen wie B. Braun und Smith & Nephew haben ihr Angebot an chirurgischem Nahtmaterial erweitert, um dieser steigenden Nachfrage gerecht zu werden, und bieten eine breite Palette an resorbierbaren und nicht resorbierbaren Fäden für verschiedene chirurgische Disziplinen an.

- Die zunehmende Verbreitung von Erkrankungen wie Herz-Kreislauf-Erkrankungen, Krebs und orthopädischen Störungen erfordert oft chirurgische Eingriffe, was direkt zu einem höheren Verbrauch von Nahtmaterial in Operationssälen weltweit beiträgt.

- Zudem ist die wachsende Zahl älterer Menschen anfälliger für chronische Erkrankungen und chirurgische Eingriffe, was den Bedarf an effektiven Wundverschlussverfahren weiter erhöht. Ältere Patienten unterziehen sich häufig Eingriffen wie Gelenkersatz, Herz-Kreislauf-Operationen und allgemeinen Operationen, die stark auf chirurgische Nähte angewiesen sind.

- Zudem führen der Ausbau der Gesundheitsinfrastruktur in Schwellenländern und der verbesserte Zugang zu chirurgischer Versorgung zu einer steigenden Anzahl von Operationen in Krankenhäusern und ambulanten Operationszentren. Diese Entwicklung verstärkt die weltweite Nachfrage nach chirurgischem Nahtmaterial in verschiedenen Gesundheitseinrichtungen zusätzlich.

Zurückhaltung/Herausforderung

Risiko von Wundinfektionen nach Operationen und Verfügbarkeit alternativer Wundverschlussmethoden

- Eine der größten Herausforderungen für den globalen Markt für chirurgisches Nahtmaterial ist das Risiko von Wundinfektionen (SSI) aufgrund unsachgemäßen Wundverschlusses oder Kontamination während chirurgischer Eingriffe. Diese Komplikationen können die Heilung verzögern, die Gesundheitskosten erhöhen und den Behandlungserfolg negativ beeinflussen.

- Beispielsweise setzen Gesundheitseinrichtungen und Krankenhäuser weltweit kontinuierlich strenge Infektionspräventionsprotokolle um, nachdem Berichte darauf hingewiesen haben, dass Wundinfektionen nach Operationen weiterhin zu den häufigsten Krankenhausinfektionen zählen. Diese Bedenken haben die Anwendung alternativer Wundverschlusstechniken wie chirurgischer Klammergeräte, Gewebekleber und Wundpflaster bei bestimmten Eingriffen gefördert.

- Alternative Wundverschlussmethoden können im Vergleich zu traditionellen Nahttechniken mitunter einen schnelleren Wundverschluss, eine kürzere Operationszeit und ein minimales Gewebetrauma ermöglichen und sind daher in bestimmten chirurgischen Anwendungsbereichen attraktive Optionen.

- Zudem führt die Verfügbarkeit fortschrittlicher Wundverschlusstechnologien, einschließlich resorbierbarer Klammern und bioadhäsiver Klebstoffe, zunehmend zu einem verstärkten Wettbewerb für herkömmliche Nahtmaterialien bei bestimmten Eingriffen wie kosmetischen Operationen und minimalinvasiven Operationen.

- Darüber hinaus könnten die Kostendrucke, denen Gesundheitssysteme und Krankenhäuser in verschiedenen Regionen ausgesetzt sind, Kaufentscheidungen beeinflussen, insbesondere wenn alternative Verschlusslösungen kürzere Eingriffszeiten und eine höhere Effizienz bieten.

- Die Bewältigung dieser Herausforderungen durch verbesserte, infektionsresistente Nahtmaterialien, erhöhte Sterilisationsstandards und kontinuierliche Innovationen in der Nahttechnologie wird entscheidend für das langfristige Wachstum des globalen Marktes für chirurgische Nahtmaterialien sein.

Marktumfang für chirurgisches Nahtmaterial in Nordamerika

Der Markt ist segmentiert nach Produkt, Typ, Anwendung und Endnutzer.

- Nebenprodukt

Basierend auf dem Produkt ist der amerikanische Markt für chirurgisches Nahtmaterial in Nahtfäden und automatisierte Nahtgeräte unterteilt. Das Segment der Nahtfäden dominierte 2025 mit einem Marktanteil von 72,8 % und erzielte damit den größten Umsatz. Dies ist auf ihren breiten Einsatz in einer Vielzahl chirurgischer Eingriffe zurückzuführen, darunter Herz-Kreislauf-, orthopädische, gynäkologische und allgemeinchirurgische Eingriffe. Nahtfäden sind aufgrund ihrer Kosteneffizienz, Zuverlässigkeit und einfachen Anwendung nach wie vor die am häufigsten verwendete Methode zum Wundverschluss. Krankenhäuser und chirurgische Zentren setzen sowohl bei Routineeingriffen als auch bei komplexen Operationen weiterhin stark auf traditionelle Nahttechniken. Die steigende Anzahl chirurgischer Eingriffe in Nordamerika trägt maßgeblich zur hohen Nachfrage nach Nahtfäden bei. Kontinuierliche Fortschritte bei resorbierbaren und nicht resorbierbaren Nahtmaterialien verbessern zudem die klinischen Ergebnisse und die Patientensicherheit. Darüber hinaus unterstützt die Verfügbarkeit verschiedener Nahtgrößen, Materialien und Nadelkombinationen ihre breite Anwendung. Chirurgen bevorzugen Nahtfäden häufig, da diese einen präzisen Wundverschluss ermöglichen und das Komplikationsrisiko reduzieren. Der Ausbau der Gesundheitsinfrastruktur und die steigenden Operationszahlen stärken dieses Segment zusätzlich. Produktinnovationen wie antibakteriell beschichtete Nahtmaterialien tragen ebenfalls zur Segmenterweiterung bei. Die zunehmende Zahl älterer Menschen, die sich chirurgischen Eingriffen unterziehen, treibt die Nachfrage weiterhin an. Daher bleiben Nahtmaterialien das dominierende Produktsegment auf dem Markt für chirurgisches Nahtmaterial.

Das Segment der automatisierten Nahtgeräte wird voraussichtlich von 2026 bis 2033 mit einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 8,9 % das schnellste Wachstum verzeichnen. Treiber dieser Entwicklung ist die zunehmende Verbreitung fortschrittlicher chirurgischer Technologien und minimalinvasiver Verfahren. Automatisierte Nahtgeräte ermöglichen einen schnelleren und effizienteren Wundverschluss, verbessern die chirurgische Präzision und verkürzen die Operationszeit. Chirurgen bevorzugen zunehmend automatisierte Geräte bei laparoskopischen und roboterassistierten Eingriffen, bei denen manuelles Nähen schwierig sein kann. Die Nachfrage nach minimalinvasiven Verfahren steigt rasant aufgrund kürzerer Krankenhausaufenthalte und einer schnelleren Genesung der Patienten. Technologische Fortschritte bei automatisierten Nahtinstrumenten verbessern die Benutzerfreundlichkeit und die klinischen Ergebnisse. Krankenhäuser und ambulante Operationszentren investieren verstärkt in fortschrittliche chirurgische Geräte, um die Effizienz zu steigern. Darüber hinaus reduzieren automatisierte Nahtgeräte die Ermüdung des Chirurgen bei langen und komplexen Operationen. Steigende Gesundheitsausgaben und die Integration von Technologie in die chirurgische Praxis fördern das Marktwachstum zusätzlich. Hersteller von Medizinprodukten bringen innovative automatisierte Nahtsysteme mit verbesserter Ergonomie und Sicherheitsmerkmalen auf den Markt. Schulungsprogramme für Chirurgen tragen ebenfalls zur Akzeptanz bei. Da die Zahl der chirurgischen Eingriffe in Nordamerika weiter zunimmt, wird für das Segment der automatisierten Nahtgeräte ein rasantes Wachstum erwartet.

- Nach Typ

Basierend auf dem Nahtmaterialtyp ist der Markt in Multifilament- und Monofilament-Nahtmaterialien unterteilt. Monofilament-Nahtmaterialien erzielten 2025 mit 58,4 % den größten Marktanteil, was auf ihre überlegene Infektionsresistenz und das geringere Gewebetrauma im Vergleich zu Multifilament-Nahtmaterialien zurückzuführen ist. Sie bestehen aus einem einzigen Materialstrang, wodurch die bakterielle Besiedlung minimiert und das Risiko von Wundinfektionen reduziert wird. Diese Nahtmaterialien werden häufig in der Herz-, Augen- und Plastischen Chirurgie eingesetzt, wo Präzision und minimale Gewebereaktion entscheidend sind. Chirurgen bevorzugen Monofilament-Nahtmaterialien, da diese reibungslos durch das Gewebe gleiten und so die Reibung beim Wundverschluss verringern. Der zunehmende Fokus auf Infektionsprävention und Patientensicherheit trägt ebenfalls zur Verbreitung von Monofilament-Nahtmaterialien bei. Krankenhäuser und OP-Zentren verwenden diese Nahtmaterialien vermehrt bei heiklen Eingriffen. Technologische Fortschritte bei Polymermaterialien haben die Festigkeit und Flexibilität von Monofilament-Nahtmaterialien weiter verbessert. Darüber hinaus trägt die steigende Anzahl minimalinvasiver Operationen zum Wachstum dieses Segments bei. Gesundheitsdienstleister legen Wert auf hochwertige Nahtmaterialien, um die Operationsergebnisse zu verbessern und Komplikationen zu reduzieren. Die Verfügbarkeit resorbierbarer Monofilament-Nahtmaterialien erweitert deren Anwendungsmöglichkeiten zusätzlich. Da die Anzahl chirurgischer Eingriffe in Nordamerika weiter zunimmt, behaupten Monofilament-Nahtmaterialien ihre Marktführerschaft.

Für das Segment der Multifilament-Nahtmaterialien wird von 2026 bis 2033 mit einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 7,6 % das schnellste Wachstum erwartet. Treiber dieser Entwicklung sind die hohe Knotensicherheit und Flexibilität der Materialien, die sie für verschiedene chirurgische Eingriffe geeignet machen. Multifilament-Nahtmaterialien bestehen aus mehreren geflochtenen Strängen und bieten Chirurgen hervorragende Handhabungseigenschaften. Sie werden häufig in der Orthopädie, Allgemeinchirurgie und Gynäkologie eingesetzt, wo ein sicherer Wundverschluss unerlässlich ist. Chirurgen bevorzugen Multifilament-Nahtmaterialien oft bei Eingriffen, die eine starke Gewebeadaptation erfordern. Die geflochtene Struktur verbessert die Knotenfestigkeit und -stabilität und reduziert das Risiko eines Nahtverrutschens. Steigende Operationszahlen und der Ausbau der Gesundheitsinfrastruktur tragen zur wachsenden Nachfrage bei. Fortschritte in der Beschichtungstechnologie haben die Glätte und die antibakteriellen Eigenschaften von Multifilament-Nahtmaterialien verbessert. Darüber hinaus bringen Hersteller innovative Produkte auf den Markt, um das Infektionsrisiko zu reduzieren. Die zunehmende Verwendung moderner Nahtmaterialien unterstützt das Marktwachstum zusätzlich. Schulungsprogramme und Initiativen zur chirurgischen Weiterbildung verbessern ebenfalls die Vertrautheit der Chirurgen mit Multifilament-Nahtmaterialien. Steigende Investitionen im Gesundheitswesen und die zunehmende Anzahl chirurgischer Eingriffe in Nordamerika treiben dieses Segment weiterhin an. Daher wird erwartet, dass Multifilament-Nahtmaterialien im Prognosezeitraum ein stetiges Wachstum verzeichnen werden.

- Durch Bewerbung

Basierend auf den Anwendungsgebieten ist der Markt in Herz-Kreislauf-Chirurgie, Allgemeinchirurgie, Gynäkologie, Orthopädie, Augenchirurgie, ästhetische und plastische Chirurgie sowie weitere Anwendungsgebiete unterteilt. Das Segment Allgemeinchirurgie erzielte 2025 mit 36,9 % den größten Marktanteil, bedingt durch die hohe Anzahl allgemeinchirurgischer Eingriffe in Krankenhäusern und Gesundheitseinrichtungen. Chirurgisches Nahtmaterial wird häufig bei Eingriffen wie Blinddarmentfernungen, Hernienoperationen, gastrointestinalen und abdominalen Operationen eingesetzt. Die zunehmende Verbreitung chronischer Erkrankungen, die chirurgische Eingriffe erfordern, trägt maßgeblich zum Wachstum dieses Segments bei. Krankenhäuser und chirurgische Zentren nutzen Nahtmaterial als unverzichtbare Instrumente zum Wundverschluss und zur Gewebereparatur. Die verbesserte Gesundheitsversorgung und die optimierte chirurgische Infrastruktur in Nordamerika stützen die Nachfrage zusätzlich. Chirurgen bevorzugen moderne Nahtmaterialien, die die Heilung fördern und das Infektionsrisiko minimieren. Technologische Fortschritte bei Nahttechniken und -materialien tragen ebenfalls zu besseren klinischen Ergebnissen bei. Darüber hinaus erhöht die alternde Bevölkerung, die sich chirurgischen Behandlungen unterzieht, den Bedarf an Nahtmaterial. Staatliche Gesundheitsausgaben und die Kostenübernahme für Operationen durch die Krankenversicherung steigern ebenfalls die Anzahl der Eingriffe. Kontinuierliche Produktinnovationen von Medizintechnikunternehmen fördern das Marktwachstum zusätzlich. Da die Zahl der chirurgischen Eingriffe weiter zunimmt, bleibt die Allgemeinchirurgie der dominierende Anwendungsbereich im Markt für chirurgisches Nahtmaterial.

Der Bereich der kosmetischen und plastischen Chirurgie wird voraussichtlich von 2026 bis 2033 mit einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 9,4 % das schnellste Wachstum verzeichnen. Treiber dieser Entwicklung ist die steigende Nachfrage nach ästhetischen Eingriffen und rekonstruktiven Operationen. Kosmetische Operationen wie Facelifts, Nasenkorrekturen und Brustvergrößerungen erfordern hochpräzise Nähte, um minimale Narbenbildung und optimale Heilung zu gewährleisten. Der wachsende Einfluss sozialer Medien und das steigende Bewusstsein der Verbraucher für ästhetische Eingriffe tragen maßgeblich zur Nachfrage bei. Chirurgen bevorzugen moderne Nahtmaterialien, die bessere kosmetische Ergebnisse erzielen und sichtbare Narben reduzieren. Technologische Innovationen bei resorbierbaren und feinen Fäden haben deren Wirksamkeit in der plastischen Chirurgie verbessert. Der zunehmende Medizintourismus und die Verfügbarkeit spezialisierter Kliniken für kosmetische Chirurgie fördern das Wachstum dieses Segments zusätzlich. Steigende verfügbare Einkommen und sich wandelnde Schönheitsideale bewegen immer mehr Menschen dazu, sich für ästhetische Eingriffe zu entscheiden. Auch rekonstruktive Operationen nach Traumata oder Erkrankungen erfordern spezielle Nahttechniken. Krankenhäuser und Fachkliniken investieren in fortschrittliche chirurgische Materialien, um die Patientenzufriedenheit zu steigern. Die wachsende Akzeptanz kosmetischer Eingriffe bei Männern und Frauen unterstützt ebenfalls die Marktexpansion. Da die ästhetische Medizin weiter an Bedeutung gewinnt, wird erwartet, dass das Segment der kosmetischen und plastischen Chirurgie das schnellste Wachstum verzeichnen wird.

- Vom Endbenutzer

Basierend auf den Endnutzern ist der Markt in Krankenhäuser, ambulante Operationszentren (AOZ), Kliniken und Arztpraxen unterteilt. Das Segment der Krankenhäuser dominierte 2025 mit einem Marktanteil von 61,7 %, was auf die hohe Anzahl chirurgischer Eingriffe in Krankenhäusern zurückzuführen ist. Krankenhäuser verfügen über eine moderne chirurgische Infrastruktur und spezialisierte medizinische Fachkräfte, die komplexe chirurgische Fälle behandeln können. Die Verfügbarkeit von Operationssälen, Sterilisationseinrichtungen und postoperativen Überwachungseinheiten macht Krankenhäuser zum primären Ort für Operationen. Darüber hinaus führen Krankenhäuser ein breites Spektrum an Eingriffen durch, darunter kardiovaskuläre, orthopädische und allgemeinchirurgische Eingriffe, die das Nähen von Gewebe erfordern. Staatliche Gesundheitsfinanzierung und Versicherungsschutz tragen zusätzlich zu den hohen Operationszahlen der Krankenhäuser bei. Große Krankenhäuser setzen häufig moderne Nahttechnologien und -materialien ein, um die klinischen Ergebnisse zu verbessern. Die Präsenz multidisziplinärer OP-Teams unterstützt ebenfalls komplexe Eingriffe. Steigende Krankenhauseinweisungen aufgrund chronischer Erkrankungen tragen zur Nachfrage nach chirurgischem Nahtmaterial bei. Medizinische Ausbildungseinrichtungen innerhalb von Krankenhäusern fördern den Einsatz moderner Nahttechniken zusätzlich. Kontinuierliche Investitionen in die Gesundheitsinfrastruktur stärken die Marktführerschaft der Krankenhäuser. Da die Anzahl chirurgischer Eingriffe weiter zunimmt, bleiben Krankenhäuser das größte Endnutzersegment.

Das Segment der ambulanten Operationszentren (AOZ) wird voraussichtlich von 2026 bis 2033 mit einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 10,1 % das schnellste Wachstum verzeichnen. Treiber dieser Entwicklung ist die zunehmende Verlagerung hin zu ambulanten chirurgischen Eingriffen. AOZ bieten kostengünstige und effiziente Alternativen zu stationären Operationen. Patienten bevorzugen AOZ zunehmend aufgrund kürzerer Wartezeiten, geringerer Kosten und schnellerer Genesungszeiten. Minimalinvasive Operationstechniken haben es zudem ermöglicht, viele Eingriffe ambulant durchzuführen. AOZ expandieren in Nordamerika rasant, um der steigenden Nachfrage nach chirurgischen Eingriffen gerecht zu werden. Diese Zentren benötigen zuverlässige Nahtmaterialien, um einen effizienten Wundverschluss während der Eingriffe zu gewährleisten. Gesundheitsdienstleister investieren verstärkt in AOZ, um Krankenhäuser zu entlasten. Fortschritte in der Operationstechnik und Anästhesie fördern ebenfalls ambulante Operationen. Staatliche Maßnahmen zur Förderung einer kosteneffizienten Gesundheitsversorgung tragen zum Wachstum der AOZ bei. Darüber hinaus unterstützen eine verbesserte Gesundheitsinfrastruktur und ein steigendes Gesundheitsbewusstsein der Patienten die Expansion ambulanter Einrichtungen. Da ambulante chirurgische Eingriffe weiter zunehmen, wird erwartet, dass AOZ das schnellste Wachstum im Markt für chirurgisches Nahtmaterial verzeichnen werden.

Regionale Analyse des nordamerikanischen Marktes für chirurgisches Nahtmaterial

- Nordamerika dominierte 2025 den Markt für chirurgisches Nahtmaterial mit dem größten Umsatzanteil. Dies ist auf die hochentwickelte Gesundheitsinfrastruktur der Region, die hohe Anzahl chirurgischer Eingriffe und die starke Präsenz führender Medizintechnikhersteller zurückzuführen, die kontinuierlich innovative Wundverschlussprodukte auf den Markt bringen. Die Region profitiert von etablierten Krankenhausnetzwerken, qualifizierten Chirurgen und einem breiten Zugang zu modernen Medizintechnologien. All dies trägt zum umfangreichen Einsatz von chirurgischem Nahtmaterial bei einer Vielzahl von Eingriffen bei, darunter Herz-Kreislauf-, orthopädische und allgemeine Chirurgie.

- Die Gesundheitsdienstleister der Region schätzen die Zuverlässigkeit, Präzision und Wirksamkeit moderner chirurgischer Nahtmaterialien für einen sicheren Wundverschluss und optimale Heilungsergebnisse. Die Verfügbarkeit technologisch fortschrittlicher Nahtmaterialien wie resorbierbarer, antimikrobiell beschichteter und Spezialnähte trägt zu einer verbesserten Patientenrehabilitation bei und reduziert das Risiko postoperativer Komplikationen. Diese Produkte werden in Krankenhäusern, ambulanten Operationszentren und Fachkliniken häufig eingesetzt, um die Effizienz chirurgischer Eingriffe und die Patientensicherheit zu erhöhen.

- Diese weitverbreitete Anwendung wird zusätzlich durch hohe Gesundheitsausgaben, solide Erstattungsstrukturen und kontinuierliche Fortschritte in der Operationstechnik begünstigt. Darüber hinaus verstärken die zunehmende Verbreitung chronischer Krankheiten, eine wachsende ältere Bevölkerung, die chirurgische Eingriffe benötigt, und laufende Investitionen in Innovationen im Gesundheitswesen die Nachfrage nach chirurgischem Nahtmaterial in ganz Nordamerika.

Einblick in den US-Markt für chirurgisches Nahtmaterial

Der US-amerikanische Markt für chirurgisches Nahtmaterial dominierte 2025 mit einem Umsatzanteil von 35,6 % den Gesamtmarkt für chirurgisches Nahtmaterial. Dies ist auf eine fortschrittliche Gesundheitsinfrastruktur, ein hohes Volumen an chirurgischen Eingriffen und die starke Präsenz führender Medizintechnikhersteller wie Johnson & Johnson, Medtronic und B. Braun zurückzuführen. Krankenhäuser und ambulante Operationszentren in den USA führen jährlich eine große Anzahl von Eingriffen durch, darunter Herz-Kreislauf-Operationen, orthopädische Eingriffe und minimalinvasive Verfahren, die alle zuverlässige Wundverschlusslösungen erfordern. Kontinuierliche Produktinnovationen wie antibakterielle und mit Widerhaken versehene Fäden sowie resorbierbare Materialien verbessern die Effizienz von Operationen und die Behandlungsergebnisse. Der zunehmende Fokus auf Patientensicherheit, Infektionsprävention und verbesserte Operationsergebnisse treibt die Einführung moderner chirurgischer Nahtmaterialien in Krankenhäusern und ambulanten Operationszentren in den USA weiter voran.

Einblick in den kanadischen Markt für chirurgisches Nahtmaterial

Der kanadische Markt für chirurgisches Nahtmaterial wird im Prognosezeitraum voraussichtlich das schnellste Wachstum verzeichnen, mit einer prognostizierten durchschnittlichen jährlichen Wachstumsrate (CAGR) von 8,9 %. Treiber dieses Wachstums sind steigende Gesundheitsausgaben, ein zunehmendes Operationsvolumen und die verstärkte Anwendung fortschrittlicher Wundverschlusstechnologien. Das kanadische Gesundheitssystem investiert kontinuierlich in die Modernisierung von Krankenhäusern und die Verbesserung der chirurgischen Infrastruktur, wodurch der Zugang zu chirurgischen Behandlungen in den wichtigsten Provinzen verbessert wird. Darüber hinaus führt die steigende Prävalenz chronischer Erkrankungen wie Herz-Kreislauf-Erkrankungen, Krebs und orthopädischen Beschwerden zu einer Zunahme der jährlich durchgeführten chirurgischen Eingriffe. Gesundheitsdienstleister setzen zudem vermehrt auf innovative resorbierbare und antimikrobielle Nahtmaterialien, um die Operationsergebnisse zu verbessern und das Infektionsrisiko zu reduzieren. Dies dürfte das Wachstum des Marktes für chirurgisches Nahtmaterial in Kanada im Prognosezeitraum weiter fördern.

Marktanteil von chirurgischen Nahtmaterialien in Nordamerika

Die Branche für chirurgisches Nahtmaterial wird hauptsächlich von etablierten Unternehmen dominiert, darunter:

- Johnson & Johnson (USA)

- Medtronic (Irland)

- B. Braun SE (Deutschland)

- Smith & Nephew (UK)

- Boston Scientific (USA)

- Teleflex Incorporated (USA)

- Stryker Corporation (USA)

- Conmed Corporation (USA)

- Apollo Endosurgery (USA)

- DemeTECH Corporation (USA)

- Sutures India Pvt. Ltd. (Indien)

- Healthium Medtech (Indien)

- Internacional Farmacéutica SA de CV (Mexiko)

- Peters Surgical (Frankreich)

- Mani Inc. (Japan)

- Delfinnaht (Indien)

- Lotus Surgicals (Indien)

- Riverpoint Medical (USA)

- WL Gore & Associates (USA)

- Zimmer Biomet (USA)

Neueste Entwicklungen auf dem nordamerikanischen Markt für chirurgisches Nahtmaterial

- Im Februar 2021 gab Corza Medical, ein globaler Anbieter chirurgischer Lösungen, die Übernahme der Surgical Specialties Corporation bekannt, einem Unternehmen, das für sein Portfolio an chirurgischem Nahtmaterial und ophthalmologischen Messern bekannt ist. Durch die Übernahme konnte Corza Medical seine Position auf dem globalen Markt für Wundverschluss stärken, indem das Produktangebot an chirurgischem Nahtmaterial und das Vertriebsnetz in mehreren Regionen erweitert wurden.

- Im August 2023 brachte Healthium Medtech TRUMAS™ auf den Markt, eine spezialisierte Produktreihe chirurgischer Nahtmaterialien für minimalinvasive Eingriffe. Ziel ist die Verbesserung der Nahteffizienz bei laparoskopischen und minimalinvasiven Operationen. Die neue Produktlinie wurde entwickelt, um die Herausforderungen in Operationsumgebungen mit eingeschränktem Zugang zu bewältigen und die chirurgische Präzision sowie die Patientenergebnisse zu verbessern.

- Im September 2023 erhielt Genesis MedTech von der chinesischen Arzneimittelbehörde (NMPA) die Zulassung für seine antibakteriellen Nahtmaterialien, die zur Reduzierung von Wundinfektionen nach Operationen und zur Verbesserung der postoperativen Heilung entwickelt wurden. Die Markteinführung erweiterte die Verfügbarkeit fortschrittlicher, infektionsresistenter Nahtmaterialien in der Region Asien-Pazifik.

- Im Mai 2023 entwickelten Forscher des Massachusetts Institute of Technology (MIT) intelligente Nahtmaterialien, die Entzündungen erkennen und therapeutische Medikamente direkt in die Wunde abgeben können. Dies stellt einen Durchbruch in der Wundverschlusstechnologie der nächsten Generation dar und ermöglicht die Echtzeitüberwachung chirurgischer Heilungsprozesse.

- Im Juni 2023 schloss Samyang Holdings Corp., ein globaler Hersteller von biologisch abbaubaren Nahtmaterialien, den Bau einer 21,9 Millionen US-Dollar teuren Produktionsstätte für chirurgische Materialien in Ungarn ab. Ziel der Anlage ist die Erweiterung der Produktionskapazität und die Stärkung der Marktpräsenz auf dem europäischen Markt für Medizinprodukte.

- Im März 2024 gaben Private-Equity-Gesellschaften wie Mankind Pharma und ChrysCapital Gebote zur Übernahme von Healthium Medtech ab, einem weltweit führenden Hersteller von chirurgischem Nahtmaterial, der zuvor im Besitz von Apax Partners war. Dieses strategische Interesse unterstreicht die zunehmende Konsolidierung und Investitionstätigkeit in der globalen Branche für Wundverschluss und chirurgisches Nahtmaterial.

- Im April 2024 eröffnete Samyang Holdings in Ungarn eine neue, 22 Millionen US-Dollar teure Produktionsstätte für chirurgisches Nahtmaterial. Dadurch wurde die Produktionskapazität deutlich erweitert und das Unternehmen konnte die Versorgung der europäischen Gesundheitsmärkte mit biologisch abbaubaren Nahtmaterialien stärken.

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.