Global Non 24 Hour Sleep Wake Disorder Drug Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

1.50 Billion

USD

3.20 Billion

2024

2032

USD

1.50 Billion

USD

3.20 Billion

2024

2032

| 2025 –2032 | |

| USD 1.50 Billion | |

| USD 3.20 Billion | |

| % | |

|

Global Non-24-Hour Sleep-Wake Disorder Drug Market Segmentation, By Drug Type (Melatonin Agonists and Others), Route of Administration (Oral and Others), End User (Hospitals, Specialty Clinics, Homecare, and Others), and Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies) - Industry Trends and Forecast to 2032

Non-24-Hour Sleep-Wake Disorder Drug Market Size

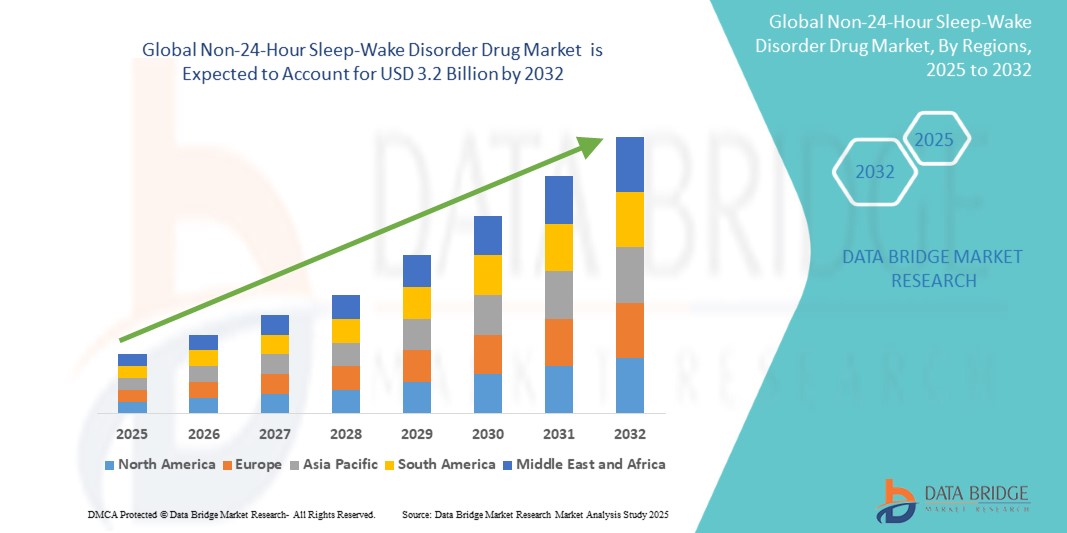

- The Global Non-24-Hour Sleep-Wake Disorder Drug Market size was valued at USD 1.5 billion in 2024 and is expected to reach USD 3.2 billion by 2032, at a CAGR of 9.2% during the forecast period

- This growth is driven by factors such as rising awareness of circadian rhythm disorders, increasing diagnosis among visually impaired individuals, and the growing availability of melatonin-based prescription therapies

Non-24-Hour Sleep-Wake Disorder Drug Market Analysis

- Non-24-Hour Sleep-Wake Disorder (Non-24) is primarily seen in totally blind individuals with no light perception, disrupting their circadian rhythms. The market is growing due to increased healthcare focus on sleep health, FDA approvals of targeted therapies, and patient advocacy efforts improving diagnosis rates

- The demand for these microscopes is significantly driven by the increasing prevalence of age-related eye conditions and advancements in surgical techniques

- North America is expected to dominate the Non-24-Hour Sleep-Wake Disorder Drugs market due to strong clinical infrastructure and availability of drugs like tasimelteon, while developing markets are expanding awareness through neurology and sleep medicine networks

- Asia-Pacific is expected to be the fastest growing region in the Non-24-Hour Sleep-Wake Disorder Drug market during the forecast period due to increasing awareness of sleep disorders and advancements in healthcare infrastructure.

- Melatonin agonists are expected to dominate due to their targeted mechanism of action and minimal side effect profiles

Report Scope and Non-24-Hour Sleep-Wake Disorder Drug Market Segmentation

|

Attributes |

Non-24-Hour Sleep-Wake Disorder Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Non-24-Hour Sleep-Wake Disorder Drug Market Trends

“Integration of Chronotherapy and Personalized Treatment Approaches”

- One prominent trend in the Global Non-24-Hour Sleep-Wake Disorder Drug Market is the growing focus on personalized chronotherapy, which aligns drug administration with an individual’s biological sleep-wake cycle.

- This approach aims to enhance treatment effectiveness by delivering medications at biologically optimal times, thereby improving sleep regulation and minimizing side effects

- For instance, in 2023, several studies and clinical trials explored circadian-timed melatonin receptor agonists, such as tasimelteon, showing improved outcomes when administered according to individual circadian profiles, paving the way for more precise and targeted therapies.

- These advancements are reshaping sleep disorder management by offering more patient-centric solutions, increasing therapeutic efficacy, and driving innovation in drug development for circadian rhythm disorders

Non-24-Hour Sleep-Wake Disorder Drug Market Dynamics

Driver

“Rising Awareness and Diagnosis of Circadian Rhythm Disorders”

- Growing recognition of circadian rhythm disorders such as Non-24 among both physicians and patients is driving market demand. Health systems are incorporating sleep health screenings and referrals to specialists more proactively

- Growing global awareness of sleep health has led to increased recognition and diagnosis of circadian rhythm disorders, including Non-24-Hour Sleep-Wake Disorder, particularly among blind individuals and those with irregular sleep patterns.

- As more individuals undergo sleep assessments and consult specialists for persistent sleep-wake disruptions, the demand for effective pharmacological treatments continues to rise, supporting market growth and fostering earlier intervention

For instance,

- in 2024, the U.S. National Institutes of Health expanded its sleep disorder research funding, accelerating the availability of diagnostic tools and treatment pathways

- As a result of increasing awareness and improved diagnosis of circadian rhythm disorders—particularly among individuals with vision impairment—there is a significant rise in the demand for Non-24-Hour Sleep-Wake Disorder drugs

Opportunity

“Expansion of Digital Health Tools and Online Pharmacies”

- Patients are increasingly accessing support through mobile health apps and online pharmacies, improving medication adherence and access to information about Non-24

- Digital health tools such as mobile sleep-tracking apps and telemedicine platforms are increasingly being used to monitor sleep patterns and identify symptoms of circadian rhythm disorders, facilitating early diagnosis and timely medical consultation.

- Additionally, the growth of online pharmacies allows patients—especially those with mobility challenges or visual impairments—to easily access Non-24-Hour Sleep-Wake Disorder drugs, improving treatment adherence and expanding market reach.

For instance,

- For example, in 2025, partnerships between sleep clinics and digital platforms in the U.S. and Germany enabled streamlined prescription renewals for melatonin-based drugs

- The integration of digital health tools and online pharmacy services can lead to improved patient outcomes, better treatment adherence, and enhanced quality of life. By leveraging remote monitoring and convenient drug access, healthcare providers can identify at-risk patients earlier and initiate timely interventions to manage Non-24-Hour Sleep-Wake Disorder effectively.

Restraint/Challenge

“High Cost and Limited Awareness in Emerging Economies”

- Despite approval in multiple countries, high cost of therapy and lack of awareness among general practitioners remain major challenges, especially in low- and middle-income markets

- The high cost of Non-24-Hour Sleep-Wake Disorder drugs, combined with limited healthcare infrastructure, can be a significant barrier in emerging economies, where treatment options may be unaffordable for many patients.

- This financial challenge, along with a lack of awareness about circadian rhythm disorders, often results in delayed diagnoses and lower adoption of treatment, limiting the market potential in these regions.

For instance,

- A 2023 study published in the Journal of Sleep Research reported that over 60% of neurologists in Southeast Asia were unaware of Non-24-specific treatment protocols, limiting patient referrals

- Consequently, these limitations can lead to disparities in access to effective treatments and early diagnosis, ultimately hindering the overall growth of the Non-24-Hour Sleep-Wake Disorder drug market in emerging economies

Non-24-Hour Sleep-Wake Disorder Drug Market Scope

The market is segmented on the basis drug type, route of administration, end user, and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Drug Type |

|

|

By Route of Administration |

|

|

By End User |

|

|

By Distribution Channel

|

|

In 2025, the Melatonin Agonists is projected to dominate the market with a largest share in drug type segment

The Melatonin Agonists segment is expected to dominate the Non-24-Hour Sleep-Wake Disorder Drug market with the largest share of 56.22% in 2025 due to its proven efficacy in regulating circadian rhythms and treating sleep-wake cycle disturbances. The growing prevalence of circadian rhythm disorders, particularly among blind individuals, along with the increasing demand for targeted, precision-based therapies, supports this segment's leading position. Additionally, heightened awareness, ongoing clinical research, and favorable regulatory approvals contribute to the strong market outlook for melatonin receptor agonists.

The oral is expected to account for the largest share during the forecast period in route of administration market

In 2025, the oral segment is expected to dominate the market with the largest market share of 51.31% due to the convenience, patient compliance, and widespread availability of oral formulations. Oral drugs, such as melatonin receptor agonists, are preferred for long-term management of circadian rhythm disorders due to ease of administration and consistent therapeutic outcomes. The growing patient population, especially among individuals with limited access to specialized care, further drives the demand for oral treatments, reinforcing this segment's market leadership.

Non-24-Hour Sleep-Wake Disorder Drug Market Regional Analysis

“North America Holds the Largest Share in the Non-24-Hour Sleep-Wake Disorder Drug Market”

- North America dominates the Non-24-Hour Sleep-Wake Disorder Drug market, driven by its advanced healthcare infrastructure, high awareness of sleep disorders, and strong presence of leading pharmaceutical companies.

- The U.S. holds a significant share due to growing recognition of circadian rhythm disorders among both blind and sighted populations, increasing diagnosis rates, and greater access to specialized sleep medicine.

- Well-established reimbursement frameworks and substantial investment in clinical research and development by key industry players further support market growth.

- Additionally, the rising use of digital health platforms and telemedicine in sleep disorder management is accelerating treatment accessibility and fueling market expansion across the region

“Asia-Pacific is Projected to Register the Highest CAGR in the Non-24-Hour Sleep-Wake Disorder Drug Market”

- Se espera que la región de Asia y el Pacífico sea testigo de la mayor tasa de crecimiento en el mercado de medicamentos para trastornos del sueño y la vigilia no relacionados con las 24 horas , impulsada por las rápidas mejoras en la infraestructura de atención médica, la creciente conciencia pública sobre los trastornos del sueño y del ritmo circadiano y el creciente acceso a los servicios de diagnóstico.

- Países como China, India y Japón están surgiendo como mercados clave debido a sus grandes poblaciones y al creciente reconocimiento de la salud del sueño, particularmente entre las personas con discapacidad visual que tienen un mayor riesgo de sufrir el trastorno del sueño-vigilia no de 24 horas.

- Japón, con su sistema de atención sanitaria progresista y su énfasis en la investigación neurológica y del sueño, desempeña un papel crucial en el avance de la adopción del tratamiento en toda la región.

- Mientras tanto, China y la India están experimentando un aumento de las inversiones tanto del sector gubernamental como del privado para ampliar el acceso a la medicina del sueño, promover campañas de concientización y mejorar la disponibilidad de tratamientos especializados, lo que contribuye a una fuerte expansión del mercado.

Cuota de mercado de medicamentos para el trastorno del sueño-vigilia no regulado por 24 horas

El panorama competitivo del mercado ofrece detalles por competidor. Se incluye información general de la empresa, sus estados financieros, ingresos generados, potencial de mercado, inversión en investigación y desarrollo, nuevas iniciativas de mercado, presencia global, plantas de producción, capacidad de producción, fortalezas y debilidades de la empresa, lanzamiento de productos, alcance y variedad de productos, y dominio de las aplicaciones. Los datos anteriores se refieren únicamente al enfoque de mercado de las empresas.

Los principales líderes del mercado que operan en el mercado son:

- Vanda Pharmaceuticals (Estados Unidos)

- Takeda Pharmaceutical Company Limited (Japón)

- Teva Pharmaceuticals (Israel)

- Productos farmacéuticos Glenmark (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Torrent Pharmaceuticals Ltd. (India)

- Apotex Inc. (Canadá)

- Cipla Ltd. (India)

Últimos avances en el mercado mundial de fármacos para el tratamiento de trastornos del sueño y la vigilia no regulados por las 24 horas

- En enero de 2025, Vanda Pharmaceuticals lanzó un portal educativo directo al paciente para mejorar la conciencia y facilitar las consultas en línea para Non-24.

- En febrero de 2025, Takeda anunció los resultados de ensayos clínicos de un nuevo agonista del receptor de melatonina que mostraban parámetros de sueño mejorados en pacientes No-24.

- En marzo de 2025, Glenmark Pharmaceuticals celebró un acuerdo de licencia para distribuir terapias Non-24 en América Latina.

- En abril de 2025, Apotex inició un ensayo clínico para una formulación genérica de tasimelteón para ampliar el acceso en los mercados emergentes.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.