Global Wet Pet Food Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

25.20 Billion

USD

37.50 Billion

2025

2033

USD

25.20 Billion

USD

37.50 Billion

2025

2033

| 2026 –2033 | |

| USD 25.20 Billion | |

| USD 37.50 Billion | |

| % | |

|

Global Wet Pet Food Market Segmentation, By Pet (Dogs and Cats), Distribution Channel (Pet Specialty Stores, Supermarkets/Hypermarkets, Convenience Stores, and Online), Source (Animal-based, Plant Derivatives, and Synthetic) - Industry Trends and Forecast to 2033

Tamaño del mercado de alimentos húmedos

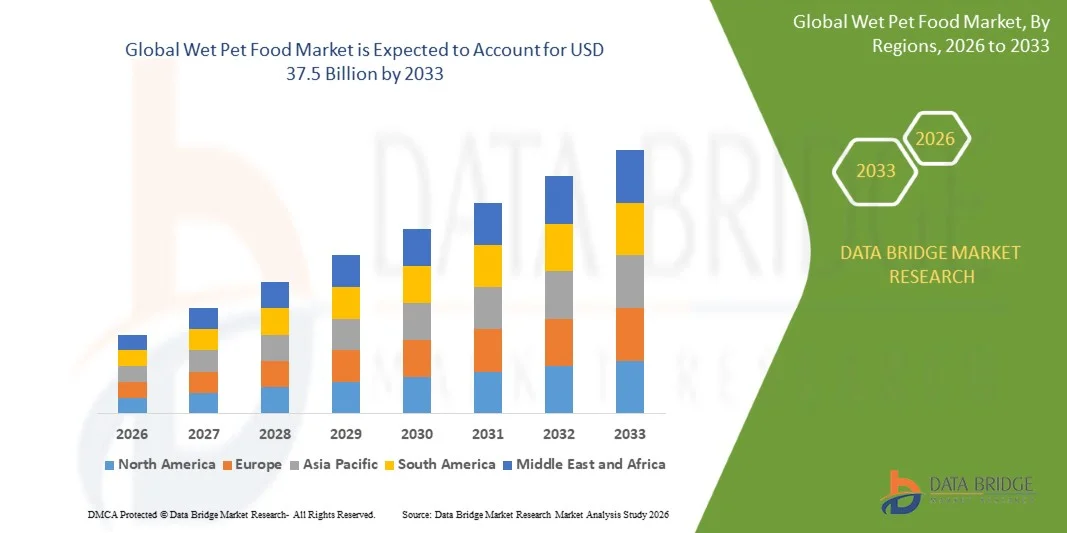

- El tamaño global de los alimentos húmedos para mascotas fue valoradoUSD 25.2 billion in 2025y se espera que alcanceUSD 37,5 billion by 2033, aCAGR of 5.10%durante el período previsto

- El crecimiento del mercado está impulsado en gran medida por el aumento de la humanización de las mascotas y el aumento de la conciencia de la nutrición de las mascotas, lo que lleva a los propietarios a priorizar dietas ricas en humedad y alta calidad para sus mascotas en mercados tanto desarrollados como emergentes

- Además, el aumento de la demanda de productos alimenticios de mascotas de primera, funcionales y específicos para condiciones, con el apoyo de mayores ingresos desechables y la ampliación de la disponibilidad al por menor y el comercio electrónico, está acelerando la adopción y fortaleciendo la expansión general del mercado

Análisis del mercado de alimentos húmedos

- Comida húmeda para mascotas, que ofrece alta palatabilidad, hidratación mejorada y digestibilidad mejorada, se ha convertido en un componente crucial de la nutrición moderna de mascotas para perros y gatos, especialmente entre las mascotas de envejecimiento y las que tienen necesidades específicas de salud

- La creciente demanda de alimentos mojados para mascotas se alimenta principalmente por el aumento de la propiedad de las mascotas, el cambio de la preferencia de los consumidores hacia las formulaciones premium y naturales, y la innovación continua de los productos por los fabricantes líderes centrados en la salud, el bienestar y la comodidad

- América del Norte dominaba el mercado de alimentos húmedos para mascotas con una proporción de 42,2%en 2025, debido a altas tasas de propiedad de mascotas y fuerte gasto de consumo en nutrición de mascotas premium

- Se espera que Asia-Pacífico sea la región de más rápido crecimiento del mercado de alimentos mojados durante el período previsto debido a la rápida urbanización, el aumento de los ingresos desechables y el aumento de la adopción de mascotas en las principales economías

- El segmento de perros dominaba el mercado con una cuota de mercado del 62,5% en 2025, debido a la mayor población mundial de perros y mayor consumo de alimentos por mascotas en comparación con gatos. Los propietarios de perros prefieren cada vez más alimentos húmedos debido a su palatabilidad, mayor contenido de humedad y idoneidad para mascotas con problemas dentales o de digestión. La tendencia creciente de la primaización y humanización de los alimentos para perros refuerza aún más la demanda de formulaciones húmedas enriquecidas nutricionalmente adaptadas a diferentes razas y etapas de vida

Report Scope and Wet Pet Food Market Segmentation

| Atributos | Wet Pet Food Key Market Insights |

| Segmentos cubiertos |

|

| Países cubiertos | América del Norte

Europa

Asia y el Pacífico

Oriente Medio y África

América del Sur

|

| Principales jugadores del mercado |

|

| Oportunidades de mercado |

|

| Valor añadido Data Infosets | Además de las ideas sobre escenarios de mercado como el valor de mercado, la tasa de crecimiento, la segmentación, la cobertura geográfica y los principales actores, los informes de mercado comisariados por el Data Bridge Market Research también incluyen análisis de exportaciones de importaciones, visión general de la capacidad de producción, análisis de consumo de producción, escenario de cambio climático, análisis de la cadena de suministro, análisis de la cadena de valor, visión general de materias primas/consumibles, criterios de selección de proveedores, análisis PESTLE Analysis, análisis, análisis de PESTLE, análisis de valores y análisis de valores. |

Tendencias del mercado de alimentos húmedos

“Premiumization of Wet Pet Food Products”

- Una tendencia clave que da forma al mercado de alimentos húmedos para mascotas es la creciente primaización de productos, impulsada por propietarios de mascotas que tratan cada vez más a las mascotas como miembros de la familia y que buscan una nutrición de alta calidad comparable a las normas de alimentos humanos. Este cambio es alentador para los fabricantes centrarse en recetas de alta proteína, ingredientes naturales y formulaciones de etiquetas limpias que enfatizan la transparencia y el valor nutricional

- Por ejemplo, Nestlé Purina PetCare ha ampliado sus carteras Pro Plan y Fancy Feast con ofertas de alimentos húmedos premium que destacan formulaciones sin granos y beneficios funcionales para la salud. Estos lanzamientos refuerzan la confianza del consumidor y fortalecen la posición de la marca en el segmento premium

- Los jugadores líderes están haciendo cada vez más hincapié en las recetas de carne primera, de alta movilidad para mejorar la palatabilidad e hidratación, especialmente para gatos y mascotas mayores. Esta tendencia apoya la demanda de variantes de alimentos húmedos especializados que abordan la digestión, la salud urinaria y la gestión del peso

- La tendencia de la primaización también es evidente en la creciente disponibilidad de comida de mascotas húmedas de estilo gourmet, con nuevas proteínas y recetas centradas en la textura. Estos productos apelan a los consumidores urbanos y de ingresos superiores que buscan experiencias de alimentación diferenciadas para sus mascotas.

- Se están adoptando innovaciones de embalaje como bandejas de servicio único y paquetes controlados por partes para mejorar la comodidad y la percepción de frescura. Esta evolución en el diseño del producto es reforzar el atractivo de marca premium y fomentar las compras de repetición

- En general, la primaización está remodelando dinámicas competitivas aumentando los precios de venta promedio y los fabricantes de motores para invertir en innovación, garantía de calidad y narración de marca para capturar consumidores centrados en el valor

Dinámica del mercado de alimentos húmedos

Conductor

“Rising Pet Humanization and Focus on Pet Health”

- La humanización creciente de mascotas es un motor primario del mercado de alimentos mojados, ya que los propietarios priorizan cada vez más la nutrición, el bienestar y la atención preventiva de sus mascotas. Este cambio está acelerando la demanda de alimentos mojados debido a sus beneficios de salud percibidos, incluyendo mayor contenido de humedad y mejor digestibilidad

- Por ejemplo, Mars Petcare ha ampliado su cartera de alimentos para mascotas húmedas a través de marcas como Royal Canin y Pedigree para atender necesidades específicas de raza, edad y salud. Estas ofertas apoyan estrategias de nutrición adaptadas a las recomendaciones veterinarias

- Aumentar la conciencia de la obesidad, los problemas dentales y los problemas de salud urinaria en las mascotas es alentar a los propietarios a elegir alimentos húmedos como parte de dietas equilibradas. Los avalados veterinarios y la investigación clínica de nutrición refuerzan aún más esta preferencia

- El conductor se ve fortalecido por el aumento de los ingresos desechables y la voluntad de gastar en productos de atención de mascotas premium, especialmente en América del Norte y Europa. Los consumidores buscan activamente soluciones nutricionalmente completas y funcionales de alimentos húmedos

- Colectivamente, la humanización de las mascotas y la conciencia sobre la salud están transformando los hábitos alimentarios y posicionando los alimentos húmedos como un componente fundamental de la nutrición moderna de las mascotas

Restraint/Challenge

“Sus costos de producción y embalaje de alimentos húmedos para mascotas”

- El mercado de alimentos para mascotas húmedas enfrenta desafíos notables debido a los altos costos de producción y embalaje asociados con formulaciones ricas en humedad y normas estrictas de seguridad. Los alimentos húmedos para mascotas requieren métodos de procesamiento avanzados, incluyendo esterilización y sellado controlado, lo que aumenta la complejidad operacional

- Por ejemplo, Freshpet se basa en la infraestructura de producción y distribución refrigerada para mantener la frescura de productos, aumentando significativamente los costos de fabricación y logística. Estos requisitos limitan la flexibilidad de costos y las estrategias de fijación de precios de impacto

- Materiales de embalaje como latas, bandejas y bolsas añaden a los gastos generales, especialmente en medio de fluctuaciones en los precios de metal y plástico. El cumplimiento de la seguridad alimentaria y las normas de la vida útil de la plataforma eleva aún más las presiones de costos para los fabricantes

- Los pequeños productores tropiezan con dificultades para escalar operaciones manteniendo la calidad y la asequibilidad, creando barreras para la entrada y expansión. Este reto es más pronunciado en mercados sensibles a los precios donde los consumidores pueden preferir alternativas a los alimentos secos

- En general, los elevados costos de producción y embalaje siguen siendo una restricción clave, que influye en los precios, la escalabilidad y la rentabilidad a largo plazo dentro del mercado de alimentos húmedos para mascotas

Mercado de alimentos húmedos

El mercado se segmenta sobre la base de mascotas, canal de distribución y fuente.

• Por mascotas

Sobre la base de mascotas, el mercado de alimentos mojados se segmenta en perros y gatos. El segmento de perros dominaba el mercado con la mayor cuota de ingresos del 62,5% en 2025, impulsada por la mayor población mundial de perros y mayor consumo de alimentos por mascotas en comparación con gatos. Los propietarios de perros prefieren cada vez más alimentos húmedos debido a su palatabilidad, mayor contenido de humedad y idoneidad para mascotas con problemas dentales o de digestión. La tendencia creciente de la primaización y humanización de los alimentos para perros refuerza aún más la demanda de formulaciones húmedas enriquecidas nutricionalmente adaptadas a diferentes razas y etapas de vida.

Se espera que el segmento de gatos sea testigo del crecimiento más rápido de 2026 a 2033, apoyado por la creciente adopción de gatos en hogares urbanos y espacios de vida más pequeños. La comida húmeda para mascotas es especialmente favorecida para gatos debido a su alto contenido de proteínas y niveles de humedad que apoyan la salud del tracto urinario. La creciente conciencia de las necesidades nutricionales específicas para felinos y el lanzamiento de variantes gastronómicas y funcionales de alimentos para gatos húmedos siguen acelerando el crecimiento del segmento.

• Canal de distribución

Sobre la base del canal de distribución, el mercado de alimentos húmedos se segmenta en tiendas especializadas para mascotas, supermercados/hipermercados, tiendas de conveniencia y en línea. Las tiendas especializadas en mascotas dominaron el mercado en 2025, debido a su amplio surtido de marcas premium y terapéuticas de alimentos mojados junto con la orientación del personal experto. Estas tiendas son preferidas por los dueños de mascotas que buscan nutrición especializada, productos recomendados por veterinarios y carteras de marcas de confianza. Las relaciones fuertes con los proveedores y las promociones en la tienda refuerzan aún más su posición principal.

Se prevé que el segmento en línea registrará la tasa de crecimiento más rápida de 2026 a 2033, impulsada por el aumento de la penetración del comercio electrónico y la comodidad de la entrega en el hogar. Los modelos de suscripción, los precios competitivos y el acceso a una gama más amplia de marcas internacionales y de nicho atraen a los propietarios de mascotas inteligentes digitalmente. Aumentar el uso de aplicaciones móviles y plataformas directas a consumidor por los fabricantes de alimentos para mascotas también admite una rápida expansión.

• Por Fuente

Sobre la base de la fuente, el mercado de alimentos mojados para mascotas se segmenta en derivados de plantas, animales y sintéticos. El segmento basado en animales representó la mayor cuota de ingresos del mercado en 2025, apoyada por su alto contenido de proteínas y alineación más estrecha con las preferencias dietéticas naturales de perros y gatos. Los consumidores perciben que los alimentos húmedos basados en animales son más nutritivos y agradables, especialmente para las mascotas con mayor energía y necesidades de mantenimiento muscular. El dominio de la carne, el pescado y las formulaciones basadas en la aves a través de categorías premium y masivas sostiene una fuerte demanda.

Se prevé que el segmento de derivados de las plantas crezca a un ritmo más rápido durante el período previsto, alimentado por el creciente interés en opciones de alimentos para mascotas sostenibles y éticamente de origen. Los propietarios de mascotas están adoptando gradualmente formulaciones inclusivas para requisitos dietéticos específicos y gestión de alergias. La innovación en el procesamiento de proteínas vegetales y formulaciones nutricionales equilibradas aumenta aún más la aceptación de este segmento.

Wet Pet Food Market Regional Analysis

- América del Norte dominaba el mercado de alimentos para mascotas húmedas con la mayor cuota de ingresos del 42,2% en 2025, impulsado por altas tasas de propiedad de mascotas y fuerte gasto de consumo en nutrición para mascotas premium

- Los dueños de mascotas de la región priorizan cada vez más productos alimenticios húmedos de alta proteína, naturales y funcionales que apoyan la salud digestiva, la hidratación y el bienestar general

- Esta fuerte adopción está respaldada por una infraestructura bien establecida de cuidado de mascotas, una alta conciencia de las tendencias de humanización de mascotas, y la presencia de las principales marcas mundiales de alimentos para mascotas, posicionando la comida húmeda como opción preferida en los hogares

U.S. Wet Pet Food Market Insight

El mercado de alimentos para mascotas húmedas de EE.UU. representó la mayor cuota de ingresos en América del Norte en 2025, alimentada por una gran población de perros y gatos y la creciente preferencia por dietas premium y especializadas. Los consumidores están optando cada vez más por formular alimentos húmedos sin cereales, orgánicos y recomendados por veterinarios para atender necesidades específicas de salud. La fuerte presencia de plataformas de comercio electrónico, modelos de entrega basados en suscripciones e innovación continua de productos apoya aún más el crecimiento sostenido del mercado.

Europe Wet Pet Food Market Insight

Se espera que el mercado de alimentos para mascotas mojados en Europa crezca en un CAGR constante durante el período previsto, impulsado por una mayor conciencia de la nutrición de las mascotas y una mayor adopción de productos alimenticios para mascotas de primera calidad. Los consumidores europeos muestran un fuerte interés en la limpieza, fuente sostenible, y producción ética de alimentos para mascotas húmedas. El crecimiento está respaldado por el aumento de la adopción de mascotas, especialmente entre los hogares más jóvenes, y una fuerte presencia al por menor en los canales en línea y fuera de línea.

U.K. Wet Pet Food Market Insight

Se proyecta que el mercado de alimentos para mascotas húmedas de los Estados Unidos experimente un crecimiento notable durante el período previsto, apoyado por la alta propiedad de las mascotas y la fuerte demanda de alimentos para mascotas naturales y de alto contenido de carne. Las preocupaciones relacionadas con la obesidad de las mascotas y la salud digestiva están alentando a los propietarios a cambiar hacia opciones nutricionalmente equilibradas de alimentos húmedos. El ecosistema minorista maduro del país y la creciente penetración de las marcas de etiquetas privadas premium continúan estimulando la expansión del mercado.

Alemania Wet Pet Food Market Insight

Se prevé que el mercado de alimentos para mascotas mojados de Alemania se expanda en un CAGR considerable, impulsado por el creciente enfoque en la salud de las mascotas, la sostenibilidad y la transparencia de los productos. Los consumidores alemanes favorecen la comida húmeda de alta calidad sin aditivos con etiquetado de ingredientes claros. El mercado se beneficia de una fuerte demanda tanto en perros como en gatos, junto con la creciente aceptación de formulaciones funcionales y recomendadas por veterinarios.

Asia-Pacific Wet Pet Food Market Insight

Se espera que el mercado de alimentos para mascotas húmedas de Asia y el Pacífico registre el CAGR más rápido de 2026 a 2033, impulsado por la rápida urbanización, el aumento de los ingresos desechables y el aumento de la adopción de mascotas en las principales economías. El cambio de estilos de vida y la creciente conciencia de la nutrición de las mascotas están acelerando el cambio de alimentos caseros a alimentos de mascotas húmedas comerciales. Ampliar las redes minoristas y aumentar la penetración de las marcas internacionales de alimentos para mascotas aumentan aún más el crecimiento regional.

Japón Mascotas más húmedo mercado de alimentos

El mercado de alimentos mojados Japón está ganando tracción debido a la población de mascotas envejecidas del país y un fuerte énfasis en la comodidad y la nutrición de calidad. La comida húmeda para mascotas es ampliamente preferida por su facilidad de consumo y idoneidad para mascotas mayores con problemas dentales o de salud. La alta demanda de productos alimenticios mojados premium, controlados por partes y funcionales sigue impulsando el impulso del mercado.

China Wet Pet Food Market Insight

El mercado de alimentos para mascotas mojados de China mantuvo la mayor cuota de ingresos en Asia Pacífico en 2025, impulsada por el rápido crecimiento de la propiedad de mascotas y el aumento de los ingresos desechables entre los hogares urbanos. El aumento de la conciencia sobre la salud de las mascotas y la fuerte influencia de las tendencias occidentales del cuidado de las mascotas están acelerando la adopción de alimentos comerciales para mascotas húmedas. La presencia de fabricantes nacionales, precios competitivos y la rápida expansión de los canales de ventas online apoyan significativamente el crecimiento del mercado en China.

Mercado de alimentos húmedos

La industria de alimentos para mascotas húmedas está dirigida principalmente por empresas bien establecidas, incluyendo:

- VAFO Group a.s. (República Checa)

- Freshpet Inc. (U.S.)

- Tiernahrung Deuerer GmbH (Alemania)

- Blue Buffalo Co. Ltd. (U.S.)

- Harringtons Pet Food (Reino Unido)

- Darling Ingredients Inc. (U.S.)

- Champion Petfoods Holding Inc. (Canadá)

- Phelps Pet Products (U.S.)

- Nestle SA (Suiza)

- De Haan Petfood (Países Bajos)

- Mars Inc. (U.S.)

- FirstMate Pet Foods (Canadá)

- Schell and Kampeter Inc. (Estados Unidos)

- Beaphar Beheer BV (Países Bajos)

- Spectrum Brands Inc. (U.S.)

- C and D Foods Ltd. (Irlanda)

- Simmons Foods Inc. (U.S.)

- Evangers Dog and Cat Food Co. Inc. (Estados Unidos)

- Colgate Palmolive Co. (U.S.)

- Clearlake Capital Group L.P. (U.S.)

Novedades en el mercado mundial de alimentos húmedos

- En febrero de 2025, Royal Canin completó la adquisición de Aguas Frescas, productor de alimentos mojados en México, fortaleciendo significativamente su huella en América Latina. Este movimiento permite a Royal Canin localizar la producción, mejorar la eficiencia de la cadena de suministro y responder mejor a la creciente demanda regional de alimentos mojados para mascotas. La adquisición mejora su posición competitiva ampliando el acceso a las nuevas bases de consumo y reforzando su liderazgo en la nutrición de mascotas de primera calidad en los mercados en desarrollo

- En enero de 2024, Nestlé Purina PetCare lanzó una nueva gama de alimentos mojados sin grano, de alta proteína bajo su etiqueta Pro Plan, abordando el creciente cambio hacia dietas de mascotas premium y centradas en la salud. Esta expansión de productos refuerza la presencia de Purina en el segmento de alimentos mojados de primera calidad apelando a los propietarios de mascotas que buscan soluciones de nutrición funcional. El lanzamiento apoya el crecimiento del mercado impulsando la innovación y reforzando las tendencias de primaización dentro de la categoría de alimentos húmedos para mascotas

- En julio de 2023, Champion Petfoods, bajo Marte, Incorporated, introdujo la línea de alimentos mojados de ACANA Premium Pâté, destacando los beneficios de nutrición e hidratación basados en presas. Este lanzamiento amplía la cartera de alimentos húmedos de la empresa y mejora su atractivo entre los consumidores priorizando las dietas naturales y biológicamente apropiadas. El desarrollo fortalece la posición competitiva de Champion Petfoods ampliando la elección en el mercado de alimentos de gatos mojados premium y apoyando la diferenciación de marca a largo plazo

- En abril de 2023, Mars Petcare amplió su cartera de SHEBA con la introducción de PORTIONS Wet Kitten Food, orientada a las necesidades nutricionales de la primera vida. Esta introducción del producto permite a la empresa capturar la demanda en diferentes etapas de la vida del gato y reforzar la lealtad de la marca entre los nuevos propietarios de mascotas. El movimiento apoya la expansión del mercado aumentando la profundidad del producto en el segmento de nutrición gatito y fortaleciendo la oferta general de alimentos húmedos de Mars Petcare

- En marzo de 2023, Hill’s Pet Nutrition, subsidiaria de Colgate-Palmolive, lanzó Prescription Diet ONC Care, una línea de alimentación húmeda especializada para mascotas diagnosticadas con cáncer. Este desarrollo mejora la presencia de Hill en el segmento de alimentos húmedos recomendado por veterinarios y terapéuticos, reforzando su papel en la nutrición clínica. La progresiva expansión global de esta gama fortalece la posición de mercado de la empresa abordando las necesidades de nutrición médica no satisfechas y profundizando las relaciones con canales veterinarios en todo el mundo

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.