North America Glyoxal Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

174.79 Million

USD

269.26 Million

2025

2033

USD

174.79 Million

USD

269.26 Million

2025

2033

| 2026 –2033 | |

| USD 174.79 Million | |

| USD 269.26 Million | |

| % | |

|

América del NorteGluthyal Market Segmentation, By Grade (Industrial Grade, Pharmaceutical Grade)

¿Cuál es la tasa de crecimiento y tamaño del mercado Glyoxal de América del Norte

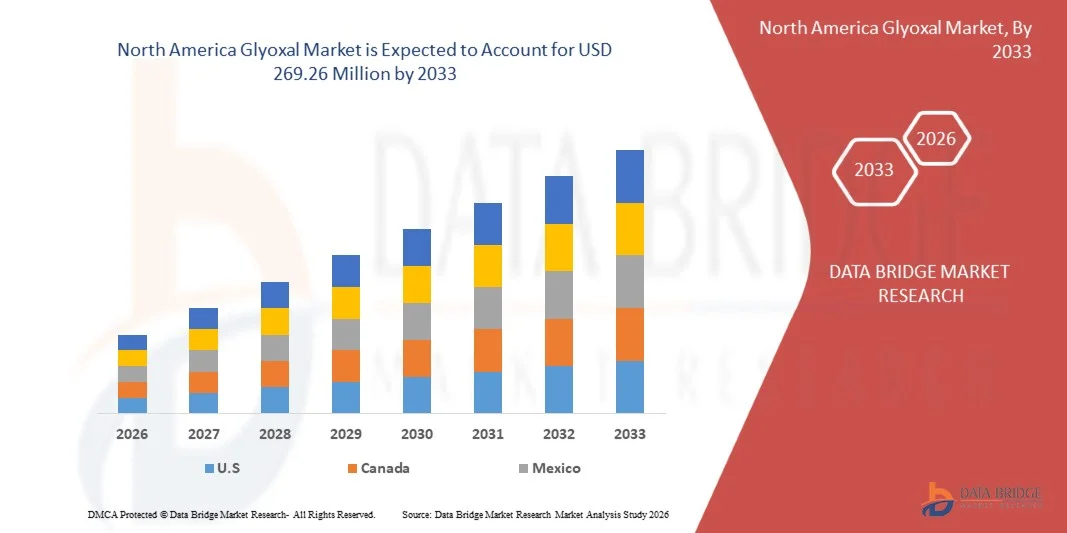

- Según el análisis de investigación del mercado del puente de datos, el tamaño del mercado Glyoxal de América del Norte fue valoradoUSD 174.79 Millones en 2025y se espera que alcanceUSD 269.26 Millones en 2033, aCAGR of 5,6%durante el período previsto

- La creciente utilización del glyoxal como agente de enlace cruzado en el acabado textil es un factor importante que impulsa la demanda en toda la región.

- La creciente adopción en papel y embalaje para las aplicaciones de la fuerza mojada y el tratamiento superficial está fortaleciendo aún más el alcance del mercado.

Tamaño del mercado

- Valor del mercado de América del Norte (2025):USD 174.79 Millones

- Valor de mercado esperado (2033): USD 269,26 Millones

- CAGR prefabricado (2026–2033): 5.6%

North America Glyoxal Market Analysis

- El mercado Glyoxal de América del Norte sirve a diversas industrias, incluyendo textiles, papel, resinas, farmacéuticas, cosméticas y tratamiento de agua. La demanda es impulsada por sus fuertes propiedades y su papel como intermediario clave en las formulaciones químicas de especialidad y rendimiento.

- El aumento de las actividades de acabado textil, el aumento del consumo de envases de papel y el creciente uso de resinas ecológicas son los principales factores de demanda. La expansión de la fabricación farmacéutica y las normas más estrictas de tratamiento de aguas residuales apoyan aún más el consumo glyoxal sostenido en todo el mundo.

- El mercado cuenta con una mezcla de productores químicos multinacionales y fabricantes regionales. La competencia se basa en la pureza de productos, las calificaciones específicas para aplicaciones, la fijación de precios, la fiabilidad de la oferta y el cumplimiento de las normas ambientales y de seguridad en las principales industrias de uso final.

- En 2025, se proyecta que Estados Unidos dominará el mercado Glyoxal de América del Norte, con un 77,25% de la cuota total del mercado. Este dominio se apoya en la capacidad de fabricación a gran escala, los bajos costos de producción y la abundante disponibilidad de materias primas. La fuerte demanda descendente de textiles, resinas, papel y industrias de cuero, junto con una cadena de suministro químico bien establecida, refuerza aún más la dirección del mercado del país.

- Se espera que el Mercado Glyoxal de América del Norte crezca en una CAGR de alrededor del 5,9% de 2026 a 2033, impulsada por la creciente demanda de las industrias textiles y agroquímicas y el creciente uso en resinas y revestimientos para aplicaciones industriales. La expansión de la industrialización y la urbanización en la región aumenta el crecimiento del mercado de combustible.

- En 2025, se espera que el segmento de grado industrial domine el mercado Glyoxal de América del Norte con una cuota de 81,11% debido a su uso generalizado en resinas de fabricación, adhesivos y productos químicos de tratamiento de papel. El segmento se beneficia de la alta demanda en aplicaciones industriales a gran escala y la eficacia en función de los costos para la producción a granel, por lo que es la opción preferida en otras categorías.

Report Scope and North America Glyoxal Market Segmentation

|

Atributos |

North America Glyoxal Key Market Insights |

|

Segmentos cubiertos |

|

|

Países cubiertos |

América del Norte

|

|

Principales jugadores del mercado |

|

|

Oportunidades de mercado |

|

|

Valor añadido Data Infosets |

Además de las ideas sobre escenarios de mercado como el valor de mercado, la tasa de crecimiento, la segmentación, la cobertura geográfica y los principales actores, los informes de mercado comisariados por el Data Bridge Market Research también incluyen análisis de exportaciones de importaciones, visión general de la capacidad de producción, análisis de consumo de producción, escenario de cambio climático, análisis de la cadena de suministro, análisis de la cadena de valor, visión general de materias primas/consumibles, criterios de selección de proveedores, análisis PESTLE Analysis, análisis, análisis de PESTLE, análisis de valores y análisis de valores. |

¿Cuál es la tendencia clave en el mercado Glyoxal de América del Norte

“El aumento de la utilización de glyoxal como agente de enlace cruzado en el acabado textil.”

- Glyoxal se utiliza cada vez más como agente de enlace cruzado en acabado textil debido a su capacidad para mejorar el rendimiento de tela sin afectar la textura o comodidad.

- Mejora la resistencia a las arrugas, estabilidad dimensional, recuperación de pliegues y propiedades de cuidado fácil, especialmente en tejidos de algodón y celulosa.

- Glyoxal es compatible con los procesos de acabado existentes y rentable, por lo que es una opción preferida en la fabricación textil a gran escala

- Informes de la industria (nbinno.com, Silver Fern Chemical, AlphaChem.biz, Ataman Chemicals, 2025) destacan su papel en mejorar la fuerza de la tela, la resistencia a la humedad y la durabilidad en textiles y cuero.

- Su adopción refleja la demanda de tejidos duraderos, resistentes a las arrugas y fáciles de cuidar de la industria del prenda, soportando acabados con valor añadido y calidad de producto consistente.

- Se espera que Glyoxal siga siendo un componente esencial en las formulaciones de acabado textil, sosteniendo la demanda en el mercado Glyoxal de América del Norte.

North America Glyoxal Market Dynamics

Conductor

Demanda creciente del sector de la alimentación "

- La adopción Glyoxal en papel y embalaje está creciendo debido a su capacidad para mejorar la fuerza mojada, la durabilidad de la superficie y el rendimiento general de los productos basados en papel.

- Mejora la resistencia a la humedad, estabilidad dimensional, imprimibilidad e integridad estructural, lo que lo hace valioso para los papeles de embalaje, cartón y productos de papel especial.

- Informes de la industria (ChemCeed, NBINNO.com, ivySCI, 2025) resaltan el papel de glyoxal en la mejora de la fuerza húmeda y seca, la reducción de la absorción de agua y la mejora de la fuerza de tracción en las formulaciones de tamaño de papel y almidón.

- Su compatibilidad con diversos grados de papel y tratamientos superficiales permite a los fabricantes producir papeles de embalaje de alta calidad, duraderos y funcionales que resisten condiciones húmedas o húmedas.

- Con la creciente demanda de envases fiables en alimentos, bienes de consumo y sectores industriales, se espera que el glyoxal siga siendo un agente clave para la mejora de la fuerza húmeda y el tratamiento de la superficie en el mercado mundial de papel y embalaje.

Restraint/Challenge

Manejo de complejidad debido a alta reactividad y sensibilidad de estabilidad

- El manejo de glyoxal plantea retos importantes debido a su alta reactividad química y sensibilidad al almacenamiento y las condiciones ambientales. El almacenamiento incorrecto, las fluctuaciones de temperatura o la exposición prolongada al aire y la luz pueden conducir a la polimerización o degradación, lo que requiere protocolos de seguridad estrictos, soluciones especializadas de almacenamiento y métodos de transporte controlados. Estas necesidades aumentan los costos operacionales y exigen personal calificado, en particular en las instalaciones de fabricación pequeñas y medianas.

- Por ejemplo, como reportó Amzole India Pvt. Ltd. en julio de 2025, la hoja de datos de seguridad para el 40% glyoxal enfatiza su naturaleza altamente reactiva y la necesidad crítica de manejo especializado para prevenir la polimerización, la exposición irritante y las reacciones con sustancias incompatibles como óxidos fuertes y bases. Del mismo modo, la documentación de ChemSpider en abril de 2025 destaca que el glyoxal puede reaccionar violentamente con agentes de aire, agua y químicos como hidroxido de sodio, haciendo almacenamiento controlado, transporte cuidadoso y medidas de seguridad estrictas esenciales durante el manejo.

- Estas complejidades de manejo afectan directamente los costos de almacenamiento, transporte y funcionamiento, planteando problemas particulares para los fabricantes más pequeños. A pesar de estas limitaciones, el glyoxal sigue siendo ampliamente utilizado en textiles, papel, adhesivos e intermedios químicos debido a sus aplicaciones versátiles y beneficios funcionales.

- En consecuencia, la gestión cuidadosa de las propiedades reactivas de glyoxal es esencial para una utilización segura y eficiente, asegurando que las industrias puedan aprovechar sus ventajas a la vez que mitigar los riesgos en el mercado mundial.

North America Glyoxal Market Scope

El mercado se segmenta sobre la base del grado, pureza, proceso de producción, aplicación de embalaje, productos químicos de uso final y la industria de uso final.

Por Grado

Basado en el grado, el Mercado Glyoxal de América del Norte se segmenta principalmente en Grado Industrial y Grado Farmacéutico.

Para 2026, se proyecta que el segmento de Grado Industrial dominará el mercado, con un 81.02% de la cuota total. Esta dominación se atribuye a sus extensas aplicaciones en diversas industrias, incluyendo textiles, procesamiento de papel, resinas, tratamiento de cuero y tratamiento de agua. El consumo de alto volumen de glyoxal de grado industrial está respaldado además por su eficacia en función de los costos y su eficiencia en las operaciones a gran escala. Además, la rápida expansión de los sectores industriales y manufactureros en la región de América del Norte está impulsando una demanda fuerte y sostenida. Como resultado, se espera que la glyoxal de grado industrial siga siendo el principal factor de crecimiento dentro del mercado regional.

Se espera que el segmento de Grado Farmacéutico en el mercado Glyoxal de América del Norte crezca más rápido de 2026 a 2033, impulsado por la creciente demanda en síntesis farmacéutica, requisitos regulatorios estrictos para productos químicos de alta pureza, y la expansión de aplicaciones avanzadas de fabricación y especialidad de drogas. Estos factores aumentan la adopción de glyoxal de alta calidad en las API y formulaciones innovadoras de drogas.

Por la pureza

Sobre la base de la pureza, el mercado Glyoxal de América del Norte se segmenta en 90% –9%, 40%–60% y otros.

Para 2026, se espera que el segmento de pureza del 40% al 60% domine el mercado, con un 72,07% de la cuota total. La prominencia de este segmento se atribuye a su rendimiento superior, mayor reactividad y idoneidad para aplicaciones avanzadas en productos farmacéuticos, resinas especiales, textiles y cosméticos. Su calidad constante, junto con la adhesión a los estrictos estándares de la industria, impulsa aún más la demanda fuerte y sostenida. Además, el equilibrio entre la eficacia y la rentabilidad hace que este rango de pureza sea altamente preferido por los fabricantes. Como resultado, se prevé que el segmento de pureza del 40% al 60% seguirá siendo el principal contribuyente al crecimiento en el mercado Glyoxal de América del Norte.

Se espera que el segmento de pureza del 90%-99% en el mercado Glyoxal de América del Norte sea testigo del crecimiento más rápido del 2026 al 2033, impulsado por su uso generalizado enfarmacéuticay aplicaciones químicas especializadas que requieren glyoxal de alta pureza, junto con la creciente demanda de formulaciones avanzadas de drogas y procesos de producción regulados.

Por proceso de producción

Sobre la base del proceso de producción, el Mercado Glyoxal de América del Norte se segmenta en oxidación catalítica de Etileno Glycol, oxidación de acetileno y otros.

Para 2026, se prevé que la oxidación catalítica del segmento Etileno Glycol dominará el mercado, con un 89,45% de la cuota total. El dominio de este segmento es impulsado por su mayor eficiencia de producción, mejor control de rendimiento y menor nivel de impureza en comparación con los procesos basados en acetileno. Además, ofrece una seguridad mejorada y es más compatible con el medio ambiente, por lo que es muy adecuado para la fabricación a gran escala. La eficacia en función de los costos y la escalabilidad de este método refuerzan aún más su preferencia entre los fabricantes. Como resultado, la ruta de oxidación catalítica está preparada para seguir siendo el principal impulsor del crecimiento en el mercado Glyoxal de América del Norte.

Se espera que el segmento de producción “Oxidación de Acetileno” en el mercado Glyoxal de América del Norte sea testigo del crecimiento más rápido de 2026 a 2033, impulsado por su capacidad de producir glyoxal de alta pureza adecuado para aplicaciones farmacéuticas y químicas especializadas, junto con la creciente demanda de formulaciones avanzadas de drogas y el cumplimiento de normas estrictas de calidad y regulación.

Por embalaje

Sobre la base del embalaje, el mercado Glyoxal de América del Norte se segmenta en tambores, IBC compuesto, Bulk, Jerrycans y Bottles.

Para 2026, se espera que el segmento Bottles domine el mercado, con un 37,35% de la cuota total. Este dominio se atribuye a su versatilidad, facilidad de manejo y almacenamiento seguro, especialmente para aplicaciones de pequeña calidad. Las botellas son especialmente adecuadas para usos farmacéuticos, cosméticos y químicos especializados, donde la precisión y la seguridad son críticas. Además, su amplia disponibilidad y producción eficaz en función de los costos impulsan aún más la adopción firme en todas las industrias. La comodidad y fiabilidad de los envases de botella hacen que sea una opción preferida para los fabricantes y usuarios finales por igual.

Se espera que el segmento de embalaje “Composite IBC” en el mercado Glyoxal de América del Norte sea testigo del crecimiento más rápido de 2026 a 2033, impulsado por su eficiencia en el almacenamiento y transporte de productos químicos a granel, mayor seguridad y resistencia química, y la creciente demanda de usuarios farmacéuticos, químicos especializados e industriales que requieren soluciones de embalaje fiables y de gran capacidad.

By Application

Sobre la base del embalaje, el mercado Glyoxal de América del Norte se segmenta en tambores, IBC compuesto, Bulk, Jerrycans y Bottles.

Para 2026, se espera que el segmento Bottles domine el mercado, con un 63,77% de la cuota total. Este dominio se atribuye a su versatilidad, facilidad de manejo y almacenamiento seguro, especialmente para aplicaciones de pequeña calidad. Las botellas son especialmente adecuadas para usos farmacéuticos, cosméticos y químicos especializados, donde la precisión y la seguridad son críticas. Además, su amplia disponibilidad y producción eficaz en función de los costos impulsan aún más la adopción firme en todas las industrias. La comodidad y fiabilidad de los envases de botella hacen que sea una opción preferida para los fabricantes y usuarios finales por igual.

Se espera que el segmento de aplicación de Intermedios Químicos en el mercado Glyoxal de América del Norte sea el segmento de más rápido crecimiento de 2026 a 2033, impulsado por la creciente demanda de resinas, polímeros y productos químicos especializados, la expansión de la industria manufacturera química, y el uso de glyoxal como un intermedio versátil y reactivo en aplicaciones industriales y especiales.

Por productos químicos de uso final

Gluthyal Gluthyal

Para 2026, se espera que el segmento de la Urea de Dihidroxietileno (DHEU) domine el mercado, con un 16,56% de la cuota total. Su dominio es impulsado por su amplia aplicabilidad en acabado textil, tratamiento de papel y fabricación de resina. El segmento se beneficia de una alta reactividad, un rendimiento coherente y la compatibilidad con diversos procesos industriales. Además, la creciente demanda de textiles de alta calidad y productos químicos especializados en la región de América del Norte apoya su fuerte posición de mercado. La eficacia y eficiencia de DHEU refuerzan aún más su preferencia entre fabricantes y usuarios finales.

Se espera que el segmento de productos químicos de uso final de 2-Imidazolidinone en el mercado Glyoxal de América del Norte sea el más rápido crecimiento de 2026 a 2033, impulsado por su creciente uso en aplicaciones farmacéuticas, agroquímicas y químicas especializadas. Su crecimiento se alimenta de la creciente demanda de glyoxal de alta pureza como intermediario clave en la sintetización de 2-Imidazolidinone para las formulaciones avanzadas y la producción química compatible con la regulación.

Por Final-User

Sobre la base del usuario final, el mercado Glyoxal de América del Norte se segmenta en Textil, Pulpo y Papel, Cuero, Pinturas y Cubiertas, Tratamiento de Agua, Farmacéuticos, Productos de Hogar, Cosméticos y Cuidado Personal, Embalaje, Electrical y Electrónica, Petróleo y Gas y Otros.

Para 2026, se espera que el segmento Textil domine el mercado, con un 32,55% de la cuota total. Este crecimiento es impulsado por su uso generalizado en acabado de tela, resistencia a las arrugas y tratamientos resistentes a la creasa. La demanda cada vez mayor de textiles duraderos y de alta calidad, junto con la rápida expansión en las industrias de ropa y muebles para el hogar, apoya aún más el crecimiento del mercado. Además, la creciente preferencia de los consumidores por los tejidos premium y duraderos aumenta la adopción de soluciones basadas en glyoxal. Como resultado, el segmento Textil está preparado para seguir siendo el principal contribuyente al mercado Glyoxal de América del Norte.

Se espera que el segmento de usuario final de Pulp y Paper en el mercado Glyoxal de América del Norte sea el más rápido crecimiento de 2026 a 2033, impulsado por la creciente demanda de resinas de fuerza húmeda y aditivos químicos que mejoran la durabilidad y calidad del papel. El crecimiento está respaldado por la expansión de la industria de papel y embalaje y el cambio hacia productos de papel sostenible de alto rendimiento.

North America Glyoxal Market Regional Analysis

- En 2026, se proyecta que Estados Unidos dominará el mercado Glyoxal de América del Norte, con una cuota de ingresos del 77,43%. Este liderazgo está impulsado por una fuerte demanda de las industrias textiles, papel y química, una amplia adopción en recubrimientos y adhesivos, y una infraestructura de fabricación química bien establecida que apoya la producción a gran escala y la innovación continua.

- El Canadá es testigo del crecimiento en el mercado Glyoxal de América del Norte debido al aumento de la demanda del papel, el embalaje y las industrias químicas, el aumento de la adopción en recubrimientos y adhesivos, y el enfoque en aplicaciones industriales de alta calidad, duraderas y funcionales.

- México está experimentando un crecimiento del mercado impulsado por la expansión de la producción de textiles y papel, el aumento de las aplicaciones industriales y las inversiones en la fabricación química y los procesos de valor añadido para satisfacer la demanda regional.

Canada North America Glyoxal Market Insight

El Canadá está experimentando un rápido crecimiento en el mercado Glyoxal de América del Norte debido a la expansión de la producción de textiles y papel y al aumento de las aplicaciones industriales. Aumentar la inversión en procesos de fabricación química y acabados de valor añadido es una mayor adopción. La demanda de telas duraderas y fáciles de cuidar y productos de papel de alto rendimiento está impulsando la expansión del mercado. A medida que las industrias se centran en la eficiencia y la calidad, se espera que el mercado Glyoxal de América del Norte continúe su trayectoria ascendente.

México América del Norte Glyoxal Market Insight

México América del Norte Glyoxal Market es testigo de crecimiento impulsado por tecnologías avanzadas de fabricación química y una fuerte demanda de productos químicos especializados. La adopción de glyoxal en textiles, papel, revestimientos y adhesivos apoya diversas aplicaciones industriales. Enfóquese en productos químicos de alto rendimiento y valor añadido que alimentan aún más el desarrollo del mercado. Se espera que la innovación continua y el avance tecnológico sostengan el crecimiento del mercado de Japón.

Los principales líderes del mercado que operan en el mercado son:

- Amzole India Pvt. Ltd (India)

- Asis Scientific Pty Ltd (Australia)

- Ataman Chemicals (India)

- BASF SE (Alemania)

- Bidvest Chemical (Sudáfrica)

- Bisley Asia (M) Sdn Bhd (Malasia)

- Eastman Chemical Company (Estados Unidos)

- Fluorochem Limited (U.K.)

- Fujifilm Wako Pure Chemical Corporation (Japón)

- Glentham Life Sciences Limited (Reino Unido)

- Get Chef Co., Ltd. (China)

- Hanna Instruments Ltd (U.S.)

- Himedia Laboratories (India)

- Kanto Kagaku (Japón)

- Kemira Oyj (Finlandia)

- Merck KGaA (Alemania)

- Meru Chem Pvt. Ltd (India)

- Muby Chemicals (India)

- Multichem Specialities Private Limited (India)

- Oakwood Products Inc. (U.S.)

- Otto Chemie Pvt. Ltd (India)

- Oxford Lab Fine Chem LLP (India)

- Santa Cruz Biotechnology Inc. (U.S.)

- Sasol (South Africa)

- Silver Fern Chemical, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Univar Solutions LLC (Estados Unidos)

- Weylchem International GmbH (Alemania)

- Zhishang Chemical (China)

Últimas novedades en el mercado Glyoxal de América del Norte

- En junio de 2022, Univar Solutions fue nombrado distribuidor exclusivo de Glyoxal de Intermedios Químicos de BASF en los Estados Unidos y Canadá. Esta asociación tiene como objetivo proporcionar a los clientes en textiles, desinfección, papel, cuero, cosméticos y industrias epoxy acceso confiable a Glyoxal de BASF, un agente de enlace biodegradable que aumenta la flexibilidad, viscosidad, propiedades antirrugas, suavidad y resistencia a la humedad en diversas formulaciones. Esta colaboración ayudará a BASF a fortalecer su presencia de mercado en América del Norte aprovechando la extensa red de distribución y las capacidades de cadena de suministro de Univar Solutions, garantizando un mayor alcance y una entrega fiable de Glyoxal a los clientes.

- En enero, Merck KGaA anunció la finalización de su adquisición del negocio químico de Mecaro, que ahora opera como M Chemicals Inc. Esta adquisición amplió las capacidades de investigación y desarrollo de Merck, así como las instalaciones de producción, fortaleciendo su cartera en materiales precursores semiconductores y productos químicos electrónicos. Si bien representa un crecimiento estratégico en el negocio químico de Merck, la adquisición no está relacionada con los productos glyoxales (glioxil), ya que el enfoque permanece en los materiales avanzados para la industria semiconductora y electrónica en lugar de la química aldehído especial.

- En diciembre de 2025, Thermo Fisher Scientific Inc. anunció el lanzamiento de dos nuevos productos Gibco Bacto CD Supreme FPM Plus y Gibco Bacto CD Supreme Feed (2X) que expanden la línea Gibco Bacto CD de medios definidos químicamente para mejorar y simplificar los flujos de trabajo de biomanufacturación de Escherichia coli (E. coli). Estas formulaciones de definición química de próxima generación están diseñadas para soportar mayores rendimientos, rendimiento constante y producción escalable de ADN plasmido y proteínas recombinantes, especialmente para aplicaciones en terapia génica y desarrollo de vacunas mRNA.

- En mayo de 2025, Alpha Chemika amplió su cartera de reactivos de laboratorio y productos químicos finos mediante la introducción de productos adicionales de calidad AR/GR/LR y productos químicos diversificados de laboratorio especializados para apoyar aplicaciones analíticas, farmacéuticas y de investigación de ciencias de la vida, reforzando su compromiso de satisfacer la evolución de la investigación mundial y la demanda industrial.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Tabla de contenido

1 INTRODUCCIÓN

1.1 OBJETIVOS DEL ESTUDIO

1.2 DEFINICIÓN DEL MERCADO

1.3 Visión general del Mar de América del Norte

1.4 LIMITACIONES

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 ÁMBIÉN GEOGRÁFICO

2.3 AÑOS ESTUDIOS PARA EL ESTUDIO

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 TYPE LIFELINE CURVE

2.8 ENTREVISTAS PRIMARÍAS CON LEADRES DE OPINION KEY

2.9 GRID DE POSICIÓN DEL MERCADO

2.1 MARKET END USUER COVERAGE GRID

2.11 FUERZAS SEGUNDARIAS

2.12 ASUNTOS

RESUMEN EJECUTIVO

4 fotos INSIGHTS

4.1 NORTH AMERICA GLYOXAL MARKET: VALUE CHAIN ANALYSIS

4.1.1 MATERIAL DE RAW " FEEDSTOCK SUPPLY (5%–10% VALUE SHARE)

4.1.2 MANUFACTURING " PROCESSING (15%–25% VALUE SHARE)

4.1.3 DISTRIBUCIÓN " LOGISTICS (30%–40% VALUE SHARE)

4.1.4 END-USE INDUSTRIAS " SALES CHANNELS (10%-20% VALUE SHARE)

4.2 ANÁLISIS DE CHAMINIS

4.2.1 EJECUCIÓN MATERIAL DE RECURSOS

4.2.2 PROCESO " MANUFACTURACIÓN DE PRODUCTOS (PRODUCCIÓN)

4.2.3 LOGISTICAS DE LA DISTRIBUCIÓN (TRANSPORTACIÓN)

4.2.4 RETAIL " COMMERCIAL BUYER CHANNELS (DISTRIBUTION " SALES)

4.3 FIVE FORCES ANALISIS DE PORTER

4.3.1 BARGAINING POWER OF BUYERS / CONSUMERS – HIGH

4.3.2 Tres de los nuevos distritos: Cómo avanzar

4.3.3 THREAT OF SUBSTITUTE PRODUCTS – MODERATE TO HIGH

4.3.4 BARGAINING POWER OF SUPPLIERS – MODERATE

4.3.5 INTENSITY OF COMPETITIVE RIVALRY – HIGH

5 MARKET OVERVIEW

5.1 DRIVERS

5.1.1 Impulsar la UTILIZACIÓN DE GLYOXAL como un agente en la terminación TEXTILE.

5.1.2 APROBACIÓN DE LA APROBACIÓN EN PAGO " PACKAGING FOR WET-STRENGTH AND SURFACE TREATMENT APPLICATIONS.

5.1.3 EXPANSION OF INTERMEDIATE CHEMICAL DEMAND IN PHARMACEUTICALS AND AGROCHEMICALS.

5.1.4 INCREASING PREFERENCE FOR LOW-MOLECULAR-WEIGHT ALDEHYDES in RESIN AND ADHESIVE SYSTEMs.

5.2 RESTRAINTS

5.2.1 La COMPLEXIDAD DE MANTENIMIENTO DUE TO HIGH REACTIVITY AND STABILITY SENSITIVITY

5.2.2 AVAILABILIDAD DE SUBSTITUTOS CHEMICOS DE APLICACIÓN-SPECÍFICOS.

5.3 OPORTUNIDAD

5.3.1 VOLATILIDAD EN FEEDSTOCK PRICING AFFECTING COST STRUCTURE

5.3.2 REGULACIONES ENVIRONMENTALES Y OCCUPACIONALES DE SAFETY.

5.3.3 DIFERENCIA DE PRODUCTOS LIMITADOS EN UN MERCADO PRECIO-COMPETIVO

5.4

5.4.1 DESARROLLO DE LOS GRADES GLYOXALES MODIFICADOS Y DE APLICACIÓN

5.4.2 DEMANDAS DE ECONOMÍAS INDUSTRIALES

6 NORTH AMERICA GLYOXAL MARKET, BY GRADE

6.1 Examen general

6.2 GRADE INDUSTRIAL

6.3 GRADE PHARMACEUTICA

6.4 NORTH AMERICA GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS

6.4.1 Grado INDUSTRIAL

Grado PHARMACEUTICA

6.5 NORTH AMERICA INDUSTRIAL GRADE EN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

6.5.1 ASIA-PACIFIC

6.5.2 NORTH AMERICA

6.5.3 EUROPA

6.5.4 MIDDLE EAST " AFRICA

6.5.5 SOUTH AMERICA

6.6 NORTH AMERICA PHARMACEUTICAL GRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

6.6.1 ASIA-PACIFIC

6.6.2 NORTH AMERICA

6.6.3 EUROPA

6.6.4 MIDDLE EAST " AFRICA

6.6.5 SOUTH AMERICA

7 NORTH AMERICA GLYOXAL MARKET, BY PURITY

7.1 Examen general

7.1.1 40%-60%

7.1.2 90%-99%

7.1.3 OTROS

7.2 NORTH AMERICA 40%-60% IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.2.1 ASIA-PACIFIC

7.2.2 NORTH AMERICA

7.2.3 EUROPA

EAST MIDDLE " AFRICA "

7.2.5 SOUTH AMERICA

7.3 NORTH AMERICA 90%-99% in GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.3.1 ASIA-PACIFIC

7.3.2 NORTH AMERICA

7.3.3 EUROPA

7.3.4 EAST MIDDLE " AFRICA

7.3.5 SOUTH AMERICA

7.4 NORTH AMERICA OTHERS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.4.1 ASIA-PACIFIC

7.4.2 NORTH AMERICA

7.4.3 EUROPA

7.4.4 MIDDLE EAST " AFRICA

7.4.5 SOUTH AMERICA

8 NORTH AMERICA GLYOXAL MARKET, BY PRODUCTION PROCESS

8.1 Examen general

8.1.1 OXIDACIÓN CATALÍTICA DE ETHYLENE GLYCOL

8.1.2 OXIDACIÓN DE ACETYLENE

8.1.3 OTROS

8.2 NORTH AMERICA CATALYTIC OXIDATION OF ETHYLENE GLYCOL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.2.1 ASIA-PACIFIC

8.2.2 NORTH AMERICA

8.2.3 EUROPA

8.2.4 MIDDLE EAST " AFRICA

8.2.5 SOUTH AMERICA

8.3 NORTH AMERICA OXIDATION OF ACETYLENE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.3.1 ASIA-PACIFIC

8.3.2 NORTH AMERICA

8.3.3 EUROPA

8.3.4 EAST MIDDLE " AFRICA

8.3.5 SOUTH AMERICA

8.4 NORTH AMERICA OTHERS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.4.1 ASIA-PACIFIC

8.4.2 NORTH AMERICA

8.4.3 EUROPA

8.4.4 EAST MIDDLE " AFRICA

8.4.5 SOUTH AMERICA

9 NORTH AMERICA GLYOXAL MARKET, BY PACKAGING

9.1 Examen general

9.2 DRUMS

9.3 IBC COMPOSITE

9.4 BULK

9.5 JERRYCANS

9.6 BOTTLES

9.7 NORTH AMERICA DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.7.1 DRUMS PLASTICOS (HDPE)

9.7.2 TIGHT-HEAD DRUMS

9.7.3 LÍNEAS ENTRADAS

9.7.4 ÁMBOS CON COOTAS DE COMPATIBILIDAD CHEMICA

9.7.5 DRUMS OPEN-TOP

9.8 NORTH AMERICA DRUMS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.8.1 ASIA-PACIFIC

9.8.2 NORTH AMERICA

9.8.3 EUROPA

9.8.4 EAST MIDDLE " AFRICA

9.8.5 SOUTH AMERICA

9.9 NORTH AMERICA COMPOSITE IBC in GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.9.1 IBCS COMPOSITE

9.9.2 IBCS RIGID

9.9.3 IBCS with INSULATION

9.9.4 OTROS

9.1 NORTH AMERICA COMPOSITE IBC in GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.10.1 ASIA-PACIFIC

9.10.2 NORTH AMERICA

9.10.3 EUROPA

9.10.4 EAST MIDDLE " AFRICA

9.10.5 SOUTH AMERICA

9.11 NORTH AMERICA BULK IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.11.1 ASIA-PACIFIC

9.11.2 NORTH AMERICA

9.11.3 EUROPA

9.11.4 EAST MIDDLE " AFRICA

9.11.5 SOUTH AMERICA

9.12 NORTH AMERICA JERRYCANS in GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.12.1 JERRYCANS PLASTICOS

9.12.2 SISTEMAS ESTABLES

9.12.3 METAL JERRYCANS

9.12.4 Otros JERRYCANS

9.13 NORTH AMERICA JERRYCANS in GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.13.1 ASIA-PACIFIC

9.13.2 NORTH AMERICA

9.13.3 EUROPA

9,13,4 MIDDLE EAST " AFRICA

9.13.5 SOUTH AMERICA

9.14 NORTH AMERICA BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.14.1 BOTTLES DE LABORATORIA

9.14.2 ASUNTOS COSMETICOS / PERSONALES DE UTILIZACIÓN

9.14.3 CUESTIONES ESPECIALES

9.14.4 OTROS ASUNTOS

9.15 NORTH AMERICA BOTTLES IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.15.1 ASIA-PACIFIC

9.15.2 NORTH AMERICA

9.15.3 EUROPA

9.15.4 EAST MIDDLE " AFRICA

9.15.5 SOUTH AMERICA

10 NORTH AMERICA GLYOXAL MARKET, BY APPLICATION

10.1 Examen general

10.2 CROSS-LINING

10.3 INTERMEDIATOS CHEMICOS

10.4 OTROS

10.5 NORTH AMERICA CROSS-LINKING in GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

10.5.1 POLYOXALATED POLYACRYLAMIDE (GPAM)

10.5.2 GLYOXALATED STARCH

10.6 NORTH AMERICA CROSS-LINKING IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.6.1 ASIA-PACIFIC

10.6.2 NORTH AMERICA

10.6.3 EUROPA

10.6.4 MIDDLE EAST " AFRICA

10.6.5 SOUTH AMERICA

10.7 INTERMEDIATOS CEMICOS NORTH AMERICA, EN MARCO GLYOXAL, POR TYPE, 2018-2033 (USTED)

10.7.1 MANUFACTURACIÓN DE LAS CHEMICAS BULK

10.7.2 POLYMER PROCESSING

10.8 NORTH AMERICA BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

10.8.1 2-IMIDAZOLIDINONE

10.8.2 ETHYLENE GLYCOL DIFORMATE

10.8.3 QUINOXALINE DERIVATIVES

10.9 NORTH AMERICA POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

10.9.1 GLYOXAL UREA RESIN

10.9.2 GLYOXAL PHENOL RESIN

10.9.3 GLYOXAL-BIS(2-HYDROXYANIL)

10.1 INTERMEDIATOS CEMICOS NORTH AMERICA EN MARCO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

10.10.1 ASIA-PACIFIC

10.10.2 NORTH AMERICA

10.10.3 EUROPA

10.10.4 EAST MIDDLE " AFRICA

10.10.5 SOUTH AMERICA

10.11 NORTH AMERICA OTHERS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

10.11.1 DIHYDROXYETHYLENE UREA (DHEU)

10.11.2 METHYLOL GLYOXAL

10.12 OTROS NORTE AMERICA EN MARCO GLYOXAL, POR REGION, 2018-2033 (USTED)

10.12.1 ASIA-PACIFIC

10.12.2 NORTE AMERICA

10.12,3 EUROPA

10.12.4 EAST MIDDLE " AFRICA

10.12.5 SOUTH AMERICA

11 NORTH AMERICA GLYOXAL MARKET, BY END-USE CHEMICALS

11.1 Examen general

11.2 DIHYDROXYETHYLENE UREA (DHEU)

11.3 2-IMIDAZOLIDINONE

11.4 POLYOXALATED POLYACRYLAMIDE (GPAM)

11.5 ACID GLYOXYLIC

11.6 GLYOXALATED STARCH

11.7 GLYOXAL PHENOL RESIN

11.8 GLYOXAL UREA RESIN

11.9 ETHYLENE GLYCOL DIFORMATE

11.1 CONCENTRO UREA-GLYOXAL

11.11 QUINOXALINE DERIVATIVES

11.12 METHYLOL GLYOXAL

11.13 GLYOXAL-BIS(2-HYDROXYANIL)

11.14 GLYOXAL SODIUM BISULFITE

11.15 QUINOXALINE

11.16 2-METHYLIMIDAZOLE

11.17 IMIDAZOLE

11.18 GLYCOLURIL

11.19 ALLANTOIN

11.2 TETRAMETHYLOL ACETYLENEDIUREA

11.21 NORTH AMERICA DIHYDROXYETHYLENE UREA (DHEU) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.21.1 ASIA-PACIFIC

11.21.2 NORTH AMERICA

11.21.3 EUROPA

11.21.4 MIDDLE EAST " AFRICA

11.21.5 SOUTH AMERICA

11.22 NORTH AMERICA 2-IMIDAZOLIDINONE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.22.1 ASIA-PACIFIC

11.22.2 NORTH AMERICA

11.22.3 EUROPA

11.22.4 MIDDLE EAST " AFRICA

11.22.5 SOUTH AMERICA

11.23 NORTH AMERICA GLYOXALATED POLYACRYLAMIDE (GPAM) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.23.1 ASIA-PACIFIC

11.23.2 NORTH AMERICA

11.23.3 EUROPA

11.23.4 MIDDLE EAST " AFRICA

11.23.5 SOUTH AMERICA

11.24 NORTH AMERICA GLYOXYLIC ACID IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.24.1 ASIA-PACIFIC

11.24.2 NORTH AMERICA

11.24.3 EUROPA

11.24.4 MIDDLE EAST " AFRICA

11.24.5 SOUTH AMERICA

11.25 NORTH AMERICA GLYOXALATED STARCH IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.25.1 ASIA-PACIFIC

11.25.2 NORTH AMERICA

11.25.3 EUROPA

11.25.4 MIDDLE EAST " AFRICA

11.25.5 SOUTH AMERICA

11.26 NORTH AMERICA GLYOXAL PHENOL RESIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.26.1 ASIA-PACIFIC

11.26.2 NORTH AMERICA

11.26.3 EUROPA

11.26.4 MIDDLE EAST " AFRICA

11.26.5 SOUTH AMERICA

11.27 NORTH AMERICA GLYOXAL UREA RESIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.27.1 ASIA-PACIFIC

11.27.2 NORTH AMERICA

11.27.3 EUROPA

11.27.4 MIDDLE EAST " AFRICA

11.27.5 SOUTH AMERICA

11.28 NORTH AMERICA ETHYLENE GLYCOL DIFORMATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.28.1 ASIA-PACIFIC

11.28.2 NORTH AMERICA

11.28.3 EUROPA

11.28.4 MIDDLE EAST " AFRICA

11.28.5 SOUTH AMERICA

11.29 NORTH AMERICA UREA-GLYOXAL CONCENTRATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.29.1 ASIA-PACIFIC

11.29.2 NORTH AMERICA

11.29.3 EUROPA

11.29.4 MIDDLE EAST " AFRICA

11.29.5 SOUTH AMERICA

11.3 NORTH AMERICA QUINOXALINE DERIVATIVES IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.30.1 ASIA-PACIFIC

11.30.2 NORTH AMERICA

11.30.3 EUROPA

11.30.4 MIDDLE EAST " AFRICA

11.30.5 SOUTH AMERICA

11.31 NORTH AMERICA METHYLOL GLYOXAL EN MARKET GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

11.31.1 ASIA-PACIFIC

11.31.2 NORTH AMERICA

11.31.3 EUROPA

11.31,4 MIDDLE EAST " AFRICA

11.31.5 SOUTH AMERICA

11.32 NORTH AMERICA GLYOXAL-BIS(2-HYDROXYANIL) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.32.1 ASIA-PACIFIC

11.32.2 NORTH AMERICA

11.32.3 EUROPA

11.32.4 MIDDLE EAST " AFRICA

11.32.5 SOUTH AMERICA

11.33 NORTH AMERICA GLYOXAL SODIUM BISULFITE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.33.1 ASIA-PACIFIC

11.33.2 NORTH AMERICA

11.33,3 euros

11.33.4 MIDDLE EAST " AFRICA

11.33.5 SOUTH AMERICA

11.34 NORTH AMERICA QUINOXALINE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.34.1 ASIA-PACIFIC

11.34.2 NORTH AMERICA

11.34.3 EUROPA

11.34.4 MIDDLE EAST " AFRICA

11.34.5 SOUTH AMERICA

11.35 NORTH AMERICA 2-METHYLIMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.35.1 ASIA-PACIFIC

11.35.2 NORTH AMERICA

11.35.3 EUROPA

11.35.4 MIDDLE EAST " AFRICA

11.35.5 SOUTH AMERICA

11.36 NORTH AMERICA IMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.36.1 ASIA-PACIFIC

11.36.2 NORTH AMERICA

11.36,3 euros

11.36.4 MIDDLE EAST " AFRICA

11.36.5 SOUTH AMERICA

11.37 NORTH AMERICA GLYCOLURIL EN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.37.1 ASIA-PACIFIC

11.37.2 NORTH AMERICA

11.37.3 EUROPA

11.37.4 MIDDLE EAST " AFRICA

11.37.5 SOUTH AMERICA

11.38 NORTH AMERICA ALLANTOIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.38.1 ASIA-PACIFIC

11.38.2 NORTH AMERICA

11.38,3 euros

11.38.4 MIDDLE EAST " AFRICA

11.38.5 SOUTH AMERICA

11.39 NORTH AMERICA TETRAMETHYLOL ACETYLENEDIUREA IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.39.1 ASIA-PACIFIC

11.39.2 NORTH AMERICA

11.39.3 EUROPA

11.39.4 MIDDLE EAST " AFRICA

11.39.5 SOUTH AMERICA

12 NORTH AMERICA GLYOXAL MARKET, BY END USER

12.1 Examen general

12.2 TEXTILE

12.3 PULP AND PAPER

12.4 LEATHER

12.5 PUNTOS Y COOTAS

12.6 TRATAMIENTO DE AGUA

12.7 PHARMACEUTICAS

12.8 PRODUCTOS DE CASA

12.9 COSMETICS AND PERSONAL CARE

12.1

12.11 ELECTRICALES Y ELECTRONICOS

12.12 OIL Y GAS

12.13 OTROS

12.14 NORTH AMERICA TEXTILE EN MARKET GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

12.14.1 ASIA-PACIFIC

12.14.2 NORTH AMERICA

12.14.3 EUROPA

12.14.4 EAST MIDDLE " AFRICA

12.14.5 SOUTH AMERICA

12.15 NORTH AMERICA PULP AND PAPER in GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.15.1 ASIA-PACIFIC

12.15.2 NORTH AMERICA

12.15.3 EUROPA

12.15.4 EAST MIDDLE " AFRICA

12.15.5 SOUTH AMERICA

12.16 NORTH AMERICA LEATHER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.16.1 ASIA-PACIFIC

12.16.2 NORTH AMERICA

12.16.3 EUROPA

12.16.4 MIDDLE EAST " AFRICA

12.16.5 SOUTH AMERICA

12.17 NORTH AMERICA PAINTS AND COATINGs in GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.17.1 ASIA-PACIFIC

12.17.2 NORTH AMERICA

12.17.3 EUROPA

12.17.4 MIDDLE EAST " AFRICA

12.17.5 SOUTH AMERICA

12.18 NORTH AMERICA WATER TREATMENT IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.18.1 ASIA-PACIFIC

12.18.2 NORTH AMERICA

12.18.3 EUROPA

12.18.4 MIDDLE EAST " AFRICA

12.18.5 SOUTH AMERICA

12.19 NORTH AMERICA PHARMACEUTICALS in GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.19.1 ASIA-PACIFIC

12.19.2 NORTH AMERICA

12.19.3 EUROPA

12.19.4 MIDDLE EAST " AFRICA

12.19.5 SOUTH AMERICA

12.2 NORTH AMERICA HOUSEHOLD PRODUCTS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.20.1 ASIA-PACIFIC

12.20.2 NORTH AMERICA

12.20.3 EUROPA

12.20,4 MIDDLE EAST " AFRICA

12.20.5 SOUTH AMERICA

12.21 NORTH AMERICA COSMETICS AND PERSONAL CARE IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

12.21.1 LOCIONES Y CREAS

12.21.2 PERFUMOS Y DEODORANTES

12.21.3 OTROS

12.22 COSMETICAS NORTH AMERICA Y CARE PERSONAL EN MERCADO GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

12.22.1 ASIA-PACIFIC

12.22.2 NORTH AMERICA

12.22.3 EUROPA

12.22,4 MIDDLE EAST " AFRICA

12.22.5 SOUTH AMERICA

12.23 NORTH AMERICA PACKAGING IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.23.1 ASIA-PACIFIC

12.23.2 NORTH AMERICA

12.23.3 EUROPA

12.23.4 MIDDLE EAST " AFRICA

12.23.5 SOUTH AMERICA

12.24 NORTH AMERICA ELECTRICAL AND ELECTRONICS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.24.1 ASIA-PACIFIC

12.24.2 NORTH AMERICA

12.24.3 EUROPA

12.24.4 MIDDLE EAST " AFRICA

12.24.5 SOUTH AMERICA

12.25 NORTH AMERICA OIL AND GAS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.25.1 ASIA-PACIFIC

12.25.2 NORTH AMERICA

12.25,3 EUROPA

12.25.4 MIDDLE EAST " AFRICA

12.25.5 SOUTH AMERICA

12.26 NORTH AMERICA OTHERS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.26.1 ASIA-PACIFIC

12.26.2 NORTH AMERICA

12.26,3 EUROPA

12.26.4 MIDDLE EAST " AFRICA

12.26.5 SOUTH AMERICA

13 NORTH AMERICA GLYOXAL MARKET, BY REGION

13.1 NORTH AMERICA

13.1.1 Estados Unidos

13.1.2 CANADA

13.1.3 MEXICO

14 NORTH AMERICA GLYOXAL MARKET, COMPANY LANDSCAPE

14.1 COMPANY SHARE ANALISIS: GLOBAL

15 SWOT ANALYSIS

16 EMPRESAS

16.1 BASF

16.1.1 SNAPSHOT

16.1.2 ANÁLISIS REVENIDO

16.1.3 PRODUCTO PORTFOLIO

16.1.4 DESARROLLO RECIENTE

16.2 MERCK KGAA

SNAPSHOT 16.2.1

16.2.2 ANÁLISIS REVENIDO

16.2.3 PRODUCTO PORTFOLIO

16.2.4 DESARROLLO RECIENTE

16.3 THERMO FISHER SCIENTIFIC INC.

16.3.1

16.3.2 ANÁLISIS REVENIDO

16.3.3 PRODUCTO PORTFOLIO

16.3.4 DESARROLLO RECIENTE

16.4 GMBH INTERNACIONAL DE WEYLCHEM

16.4.1 SNAPSHOT

16.4.2 PRODUCTO PORTFOLIO

16.4.3 DESARROLLO RECIENTE

16.5 ALPHA CHEMIKA.

16.5.1 SNAPSHOT

16.5.2 PRODUCTO PORTFOLIO

16.5.3 DESARROLLO RECIENTE

16.6 AMZOLE INDIA PVT. LTD

SNAPSHOT 16.6.1

16.6.2 PRODUCTOS PORTFOLIO

16.6.3 DESARROLLO RECIENTE

16.7 EMCO DYESTUFF

16.7.1

16.7.2 PRODUCTO PORTFOLIO

16.7.3 DESARROLLO RECIENTE

16.8 FLUOROCHEM LIMITED

SNAPSHOT 16.8.1

16.8.2 PRODUCTOS PORTFOLIO

16.8.3 DESARROLLO RECIENTE

16.9 FUJIFILM WAKO PURE CHEMICAL CORPORATION

SNAPSHOT 16.9.1

16.9.2 PRODUCTO PORTFOLIO

16.9.3 DESARROLLO RECIENTE

16.1 GETCHEM CO., LTD.

16.10.1 SNAPSHOT

16.10.2 PRODUCTO PORTFOLIO

16.10.3 DESARROLLO RECIENTE

16.11 GLENTHAM LIFE SCIENCES LIMITED

16.11.1

16.11.2 PRODUCTO PORTFOLIO

16.11.3 DESARROLLO RECIENTE

16.12 HANNA EQUIPMENTS (INDIA) PVT. LTD.

SNAPSHOT 16.12.1

16.12.2 PRODUCTOS PORTFOLIO

16.12.3 DESARROLLO RECIENTE

16.13 HEZE RUNQUAN CHEMICAL CO., LTD.

16.13.1

16.13.2 PRODUCTO PORTFOLIO

16.13.3 DESARROLLO RECIENTE

16.14 HIMEDIA LABORATORIA

16.14.1

16.14.2 PRODUCTO PORTFOLIO

16.14.3 DESARROLLO RECIENTE

16.15 HUBEI SHUNHUI BIO-TECHNOLOGY CO., LTD.

16.15.1

16.15.2 PRODUCTO PORTFOLIO

16.15.3 DESARROLLO RECIENTE

16.16 KANTO KAGAKU

16.16.1

16.16.2 PRODUCTO PORTFOLIO

16.16.3 DESARROLLO RECIENTE

16.17 KEMIRA

16.17.1

16.17.2 ANÁLISIS REVENIDO

16.17.3 PRODUCTO PORTFOLIO

16.17.4 DESARROLLO RECIENTE

16.18 LOBACHEMIE PVT. LTD.

16.18.1 SNAPSHOT

16.18.2 PRODUCTO PORTFOLIO

16.18.3 DESARROLLO RECIENTE

16.19 MERU CHEM PVT.LTD.

16.19.1

16.19.2 PRODUCTO PORTFOLIO

16.19.3 DESARROLLO RECIENTE

16.2 Especialidades MULTICHEM PRIVADAS

16.20.1

16.20.2 PRODUCTO PORTFOLIO

16.20.3 DESARROLLO RECIENTE

16.21 OTTO CHEMIE PVT. LTD

16.21.1

16.21.2 PRODUCTO PORTFOLIO

16.21.3 DESARROLLO RECIENTE

16.22 OXFORD LAB FINE CHEM LLP.

16.22.1 SNAPSHOT

16.22.2 PRODUCTO PORTFOLIO

16.22.3 DESARROLLO RECIENTE

16.23 SANTA CRUZ BIOTECHNOLOGY INC.

16.23.1 SNAPSHOT

16.23.2 PRODUCTO PORTFOLIO

16.23.3 DESARROLLO RECIENTE

16.24 SHANDONG ZHISHANG CHEMICAL CO.LTD,

16.24.1 SNAPSHOT

16.24.2 PRODUCTOS PORTFOLIO

16.24.3 DESARROLLO RECIENTE

16.25 SIHAULI CHEMICALS PRIVATE LIMITADA

16.25.1

16.25.2 PRODUCTO PORTFOLIO

16.25.3 DESARROLLO RECIENTE

16.26 SILVER FERN CHEMICAL LLC

16.26.1 SNAPSHOT

16.26.2 PRODUCTO PORTFOLIO

16.26.3 DESARROLLO RECIENTE

16.27 SIMSON PHARMA LIMITED

16.27.1

16.27.2 PRODUCTO PORTFOLIO

16.27.3 DESARROLLO RECIENTE

16.28 TOKYO CHEMICAL INDUSTRY UK LTD.

16.28.1 SNAPSHOT

16.28.2 PRODUCTO PORTFOLIO

16.28.3 DESARROLLO RECIENTE

16.29 UNIVAR SOLUTIONS LLC

16.29.1 SNAPSHOT

16.29.2 PRODUCTO PORTFOLIO

16.29.3 DESARROLLO RECIENTE

16.3 WUXI LANSEN CHEMICALS CO., LTD.

16.30.1

16.30.2 PRODUCTO PORTFOLIO

16.30.3 DESARROLLO RECIENTE

17 CUESTIÓN

18 INFORMES CONEXOS

Lista de Tablas

CUADRO 1 PRODUCTOS FINANCIEROS PARA GLYOXAL

CUADRO 2 NORTH AMERICA GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

CUADRO 3 NORTH AMERICA GLYOXAL MARKET, POR GRADE, 2018-2033 (THOUSAND TONS )

CUADRO 4 NORTH AMERICA INDUSTRIAL GRADE EN MARCO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 5 NORTH AMERICA PHARMACEUTICAL GRADE EN MARKET GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 6 NORTH AMERICA GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

CUADRO 7 NORTH AMERICA 40%-60% EN MERCADO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 8 NORTH AMERICA 90%-99% EN MARCO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 9 OTROS NORTE AMERICA EN MARCO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 10 NORTH AMERICA GLYOXAL MARKET, POR PROCESO DE PRODUCCIÓN, 2018-2033 (US$ THOUSAND)

CUADRO 11 NORTH AMERICA OXIDACIÓN CATALÍTICA DE ETHYLENE GLYCOL EN MERCADO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 12 OXIDACIÓN NORTH AMERICA DE ACETYLENE EN MARCHA GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 13 OTROS NORTE AMERICA EN MARCO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 14 NORTH AMERICA GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

CUADRO 15 NORTH AMERICA DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 16 NORTH AMERICA DRUMS EN MARKET GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 17 NORTH AMERICA COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 18 NORTH AMERICA COMPOSITE IBC IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

CUADRO 19 NORTH AMERICA BULK IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

CUADRO 20 NORTH AMERICA JERRYCANS EN GLYOXAL MARKET, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 21 NORTH AMERICA JERRYCANS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

CUADRO 22 NORTH AMERICA BOTTLES EN MARKET GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 23 NORTH AMERICA BOTTLES EN MARKET GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 24 NORTH AMERICA GLYOXAL MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)...

CUADRO 25 NORTH AMERICA CROSS-LINING EN MARKET GLYOXAL, POR TYPE, 2018-2033 (USD THOUSAND)

CUADRO 26 NORTH AMERICA CROSS-LINING EN MARCO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 27 INTERMEDIATOS CEMICOS NORTH AMERICA, EN MARCHA GLYOXAL, POR TYPE, 2018-2033 (USTED)

CUADRO 28 NORTH AMERICA BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 29 NORTH AMERICA POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 30 INTERMEDIATOS AMÉRICOS NORTE EN MARCHA GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 31 OTROS NORTE AMERICA EN MARCO GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 32 OTROS NORTE AMERICA EN MARCO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 33 NORTH AMERICA GLYOXAL MARKET, POR END-USE CHEMICALS, 2018-2033 (USD THOUSAND)

CUADRO 34 NORTH AMERICA DIHYDROXYETHYLENE UREA (DHEU) EN GLYOXAL MARKET, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 35 NORTH AMERICA 2-IMIDAZOLIDINONE EN MERCADO GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 36 NORTH AMERICA GLYOXALATED POLYACRYLAMIDE (GPAM) EN MERCADO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 37 NORTH AMERICA GLYOXYLIC ACID EN MARKET GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 38 NORTH AMERICA GLYOXALATED STARCH IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

CUADRO 39 NORTH AMERICA GLYOXAL PHENOL RESIN EN GLYOXAL MARKET, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 40 NORTH AMERICA GLYOXAL UREA RESIN EN GLYOXAL MARKET, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 41 NORTH AMERICA ETHYLENE GLYCOL DIFORMATE EN GLYOXAL MARKET, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 42 NORTH AMERICA UREA-GLYOXAL CONCENTRATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

CUADRO 43 NORTH AMERICA QUINOXALINE DERIVATIVES IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

CUADRO 44 NORTH AMERICA METHYLOL GLYOXAL EN MARKET GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 45 NORTH AMERICA GLYOXAL-BIS(2-HYDROXYANIL) EN MERCADO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 46 NORTH AMERICA GLYOXAL SODIUM BISULFITE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

CUADRO 47 NORTH AMERICA QUINOXALINE EN MARKET GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 48 NORTH AMERICA 2-METHYLIMIDAZOLE EN MARKET GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 49 NORTH AMERICA IMIDAZOLE EN MARCO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 50 NORTH AMERICA GLYCOLURIL EN MARKET GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 51 NORTH AMERICA ALLANTOIN EN GLYOXAL MARKET, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 52 NORTH AMERICA TETRAMETHYLOL ACETYLENEDIUREA IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

CUADRO 53 NORTH AMERICA GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

CUADRO 54 TEXTO NORTH AMERICA EN MARCO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 55 NORTH AMERICA PULP AND PAPER EN GLYOXAL MARKET, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 56 NORTH AMERICA LEATHER EN GLYOXAL MARKET, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 57 NORTH AMERICA PAINTS AND COATINGS IN GLYOXAL MARKET, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 58 NORTH AMERICA WATER TREATMENT IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

CUADRO 59 PHARMACEUTICAS NORTH AMERICAS EN MARCO GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 60 PRODUCTOS NORTH AMERICA EN MARCO GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 61 COSMETICOS NORTH AMERICA Y CARE PERSONAL EN MARCHA GLYOXAL, POR TYPE, 2018-2033 (USTED)

CUADRO 62 COSMETICOS NORTH AMERICA Y CARE PERSONAL EN MARCHA GLYOXAL, POR REGION, 2018-2033 (USTED)

CUADRO 63 NORTH AMERICA PACKAGING EN MARKET GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 64 NORTH AMERICA ELECTRICAL AND ELECTRONICS EN MARKET GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 65 NORTH AMERICA OIL Y GAS EN MARCO GLYOXAL, POR REGION, 2018-2033 (US$ THOUSAND)

CUADRO 66 NORTH AMERICA OTHERS EN MARKET GLYOXAL, POR REGION, 2018-2033 (USD THOUSAND)

CUADRO 67 NORTH AMERICA GLYOXAL MARKET, POR PAÍS, 2018-2033 (US$ THOUSAND)

CUADRO 68 NORTH AMERICA GLYOXAL MARKET, POR PAÍS, 2018-2033 (THOUSAND TONS )

CUADRO 69 USD

CUADRO 70 NORTH AMERICA GLYOXAL MARKET, POR GRADE, 2018-2033 (US$ THOUSAND)

CUADRO 71 NORTH AMERICA GLYOXAL MARKET, POR GRADE, 2018-2033 (THOUSAND TONS )

CUADRO 72 NORTH AMERICA GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

CUADRO 73 NORTH AMERICA GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND)

CUADRO 74 NORTH AMERICA GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

CUADRO 75 NORTH AMERICA DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 76 NORTH AMERICA COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 77 JERRYCANS NORTH AMERICA EN MARCO GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 78 NORTH AMERICA BOTTLES EN MARKET GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 79 NORTH AMERICA GLYOXAL MARKET, POR APLICACIÓN, 2018-2033 (USD THOUSAND)..

CUADRO 80 NORTH AMERICA CROSS-LINING EN MARKET GLYOXAL, POR TYPE, 2018-2033 (USD THOUSAND)

CUADRO 81 INTERMEDIATOS AMÉRICOS NORTE, EN MARCO GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

TABLE 82 NORTH AMERICA BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 83 NORTH AMERICA POLYMER PROCESSING IN GLYOXAL MARKET, POR TYPE, 2018-2033 (USD THOUSAND)

CUADRO 84 OTROS NORTE AMERICA EN MARCO GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 85 NORTH AMERICA GLYOXAL MARKET, POR END-USE CHEMICALS, 2018-2033 (USD THOUSAND)

CUADRO 86 NORTH AMERICA GLYOXAL MARKET, POR FIN USUARIO, 2018-2033 (USD THOUSAND)

CUADRO 87 COSMETICOS NORTH AMERICA Y CUIDADO PERSONAL EN MARCHA GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 88 MERCADO GLYOXAL, POR GRADE, 2018-2033 (US$ THOUSAND)

CUADRO 89 MARKET GLYOXAL, POR GRADE, 2018-2033 (THOUSAND TONS )

CUADRO 90 MARKET GLYOXAL, POR PURITY, 2018-2033 (US$ THOUSAND)

CUADRO 91 MARKET GLYOXAL, POR PROCESO DE PRODUCCIÓN, 2018-2033 (US$ THOUSAND)

CUADRO 92 U.S. GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

CUADRO 93 DRUMS U.S. EN MARKET GLYOXAL, POR TYPE, 2018-2033 (USTED)

CUADRO 94 U.S. COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 95 U.S. JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 96 U.S. BOTTLES EN MARKET GLYOXAL, POR TYPE, 2018-2033 (USD THOUSAND)

CUADRO 97 MERCADO GLYOXAL, POR APLICACIÓN, 2018-2033 (US$ THOUSAND)

CUADRO 98 U.S. CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 99 INTERMEDIATOS U.S. CHEMICAL, EN MARCHA GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 100 U.S. BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 101 PROCESO DE POLYMER EN MARKET GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 102 U.S. OTHERS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 103 U.S. GLYOXAL MARKET, BY END-USE CHEMICALS, 2018-2033 (USD THOUSAND)

CUADRO 104 MARKET GLYOXAL, POR FIN USUARIO, 2018-2033 (US$ THOUSAND)

CUADRO 105 COSMETICOS Y CUIDADO PERSONAL EN MERCADO GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 106 CANADA GLYOXAL MARKET, POR GRADE, 2018-2033 (US$ THOUSAND)

CUADRO 107 CANADA GLYOXAL MARKET, POR GRADE, 2018-2033 (THOUSAND TONS )

CUADRO 108 CANADA GLYOXAL MARKET, BY PURITY, 2018-2033 (US$ THOUSAND)

CUADRO 109 CANADA GLYOXAL MARKET, POR PROCESO DE PRODUCCIÓN, 2018-2033 (US$ THOUSAND)

CUADRO 110 CANADA GLYOXAL MARKET, POR PACKAGING, 2018-2033 (US$ THOUSAND)

CUADRO 111 DROMAS CANADAS EN MERCADO GLYOXAL, POR TYPE, 2018-2033 (USTED)

CUADRO 112 CANADA COMPOSITE IBC EN MARKET GLYOXAL, POR TYPE, 2018-2033 (USTED)

CUADRO 113 CANADA JERRYCANS EN MARCHA GLYOXAL, POR TYPE, 2018-2033 (USTED)

CUADRO 114 BOTTLES CANADA EN MARKET GLYOXAL, POR TYPE, 2018-2033 (USD THOUSAND)

CUADRO 115 CANADA GLYOXAL MARKET, POR APLICACIÓN, 2018-2033 (US$ THOUSAND)

CUADRO 116 CANADA CROSS-LINING EN MARKET GLYOXAL, POR TYPE, 2018-2033 (USD THOUSAND)

CUADRO 117 INTERMEDIATOS CANADÁTICOS, EN MARCO GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 118 CANADA BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 119 POLYMER PROCESSING CANADA EN MARKET GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 120 CANADÁ OTROS EN MERCADO GLYOXAL, POR TYPE, 2018-2033 (USD THOUSAND)

CUADRO 121 CANADA GLYOXAL MARKET, BY END-USE CHEMICALS, 2018-2033 (USD THOUSAND)

CUADRO 122 CANADA GLYOXAL MARKET, POR FIN USUARIO, 2018-2033 (US$ THOUSAND)

CUADRO 123 COSMETICOS CANADAS Y CUIDADO PERSONAL EN MARCHA GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 124 MÉXICO GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

CUADRO 125 MÉXICO GLYOXAL MARKET, POR GRADE, 2018-2033 (THOUSAND TONS )

CUADRO 126 MÉXICO GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

CUADRO 127 MÉXICO GLYOXAL MARKET, POR PROCESO DE PRODUCCIÓN, 2018-2033 (US$ THOUSAND)

CUADRO 128 MÉXICO GLYOXAL MARKET, POR PACKAGING, 2018-2033 (US$ THOUSAND)

CUADRO 129 MÉXICOS EN MARKET GLYOXAL, POR TYPE, 2018-2033 (USTED)

CUADRO 130 MÉXICO COMPOSITE IBC EN MARKET GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 131 MÉXICO JERRYCANS EN MARKET GLYOXAL, POR TYPE, 2018-2033 (US$ THOUSAND)

CUADRO 132 MÉXICO BOTTLES EN MARKET GLYOXAL, POR TYPE, 2018-2033 (USD THOUSAND)

CUADRO 133 MÉXICO GLYOXAL MARKET, POR APLICACIÓN, 2018-2033 (US$ THOUSAND)

CUADRO 134 MÉXICO CROSS-LINING EN MARKET GLYOXAL, POR TYPE, 2018-2033 (USD THOUSAND)

CUADRO 135 MÉXICO INTERMEDIATES, EN MARCO GLYOXAL, POR TYPE, 2018-2033 (USTED)

CUADRO 136 MÉXICO BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 137 MÉXICO POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

CUADRO 138 MÉXICO OTROS EN MARCHA GLYOXAL, POR TYPE, 2018-2033 (USTED)

CUADRO 139 MÉXICO GLYOXAL MARKET, POR END-USE CHEMICALS, 2018-2033 (USD THOUSAND)

CUADRO 140 MÉXICO GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

CUADRO 141 MÉXICO COSMETICS AND PERSONAL CARE IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

Lista de figuras

FIGURE 1 NORTH AMERICA GLYOXAL MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA GLYOXAL MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA GLYOXAL MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA GLYOXAL MARKET: PHILIPPINES VS REGIONAL ANALYSIS

FIGURE 5 NORTH AMERICA GLYOXAL MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA GLYOXAL MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 NORTH AMERICA GLYOXAL MARKET: DBMR MARKET POSITION GRID

FIGURE 8 DBMR VENDOR SHARE ANALISIS

FIGURE 9 NORTH AMERICA GLYOXAL MARKET: SEGMENTATION

RESUMEN 10

FIGURE 11 DECISIONES STRATEGIC

FIGURE 12 SIX SEGMENTS COMPRISE THE NORTH AMERICA GLYOXAL MARKET, BY PRODUCT (2025)

FIGURE 13 RISING UTILIZATION OF GLYOXAL AS A CROSSLINING AGENT IN TEXTILE FINISHING IS EXPECTED TO DRIVE THE NORTH AMERICA GLYOXAL MARKET DURING THE FORECAST PERIOD of 2026 to 2033

FIGURE 14 SEGMENTO DE GRADE INDUSTRIAL se presenta para ajustarse a la mayor parte del NORTE MERCADO GLYOXAL AMERICA EN 2026 & 2033

FIGURE 15 VALUE CHAIN ANALISIS

FIGURE 16 SUPPLY CHAIN ANALYSIS

FIGURE 17 FIVE FORCES DE PORTER ANALISIS

FIGURE 18 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF NORTH AMERICA GLYOXAL MARKET

FIGURE 19 GLYOXAL MARKET: BY GRADE, 2025

FIGURE 20 GLYOXAL MARKET: BY PURITY, 2025

FIGURE 21 GLYOXAL MARKET: BY PRODUCTION PROCESS, 2025

FIGURE 22 NORTH AMERICA GLYOXAL MARKET: BY PACKAGING, 2025

FIGURE 23 NORTH AMERICA GLYOXAL MARKET: BY APPLICATION, 2025

FIGURE 24 NORTH AMERICA GLYOXAL MARKET: BY END-USE CHEMICALS, 2025

FIGURE 25 NORTH AMERICA GLYOXAL MARKET: BY END USER, 2025

FIGURE 26 NORTH AMERICA GLYOXAL MARKET: GEOGRAPHICAL ANALYSIS

FIGURE 27 NORTH AMERICA GLYOXAL MARKET: COMPANY SHARE 2025 (%)

FIGURE 28 NORTH AMERICA GLYOXAL MARKET, SNAPSHOT (2025)

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.