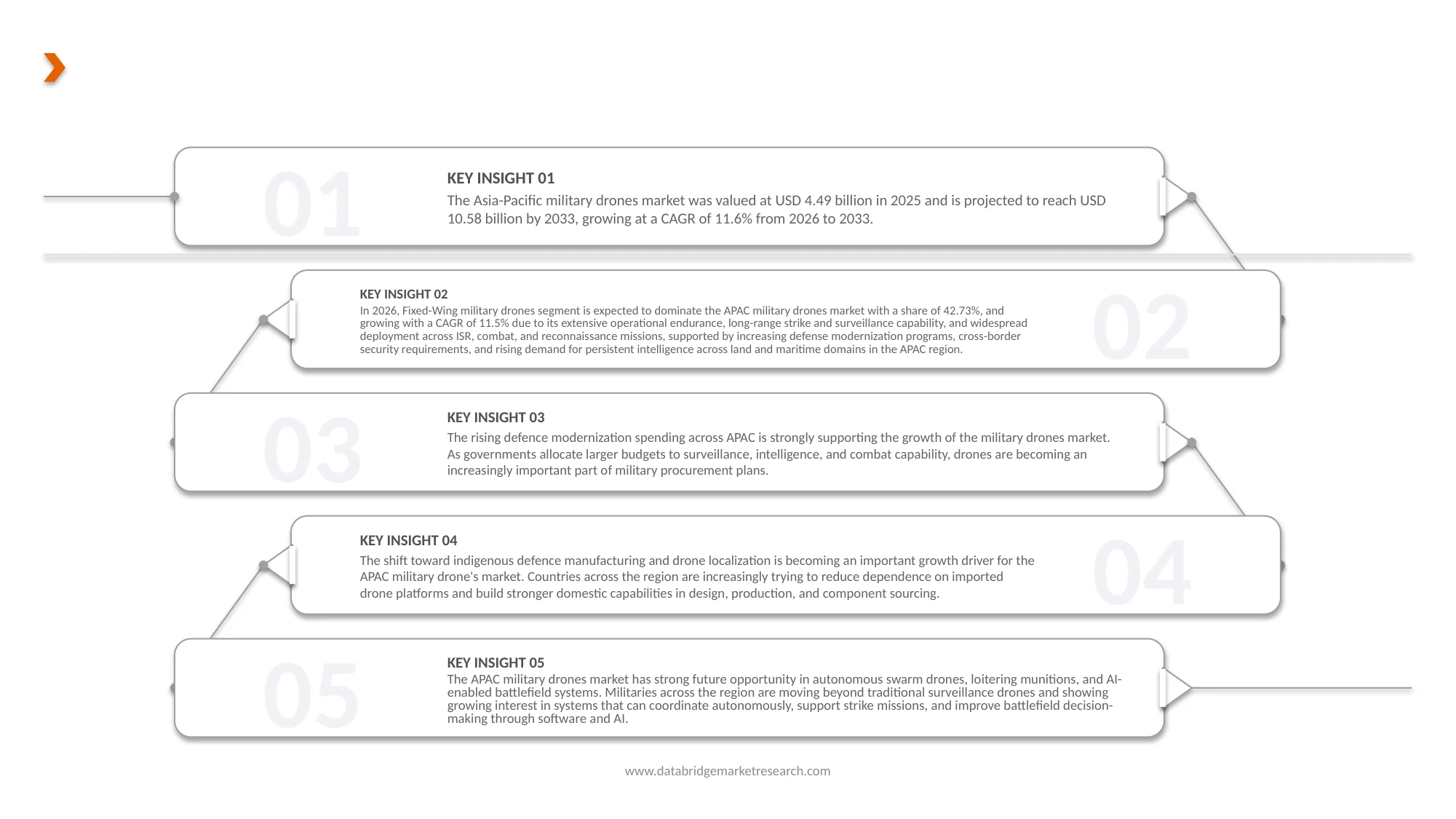

Rising defense modernization spending across major Asia-Pacific countries is driving significant growth in the Asia-Pacific Military Drones Market. Governments across the region are substantially increasing defense budgets to strengthen surveillance capabilities, enhance border security, modernize armed forces, and improve intelligence, reconnaissance, and combat operations. Countries including China, India, Japan, South Korea, and Australia are investing heavily in advanced unmanned aerial systems (UAS) equipped with artificial intelligence, autonomous navigation, high-resolution imaging, and long-endurance capabilities. Leading defense manufacturers such as AVIC, China Aerospace Science and Technology Corporation (CASC), Israel Aerospace Industries, General Atomics, and Boeing are expanding their military drone portfolios to meet the growing demand for technologically advanced defense solutions. The increasing focus on indigenous defense manufacturing and next-generation battlefield capabilities is further supporting market expansion across the Asia Pacific region.

Rising geopolitical tensions, territorial disputes, and evolving security threats are accelerating the procurement of military drones for intelligence, surveillance, target acquisition, and precision strike missions. Defense agencies are integrating unmanned systems with network-centric warfare, satellite communication, and real-time data analytics to improve operational efficiency and mission effectiveness. At the same time, governments are promoting domestic drone production through defense partnerships, technology transfer initiatives, and increased research and development investments to reduce dependence on imports. The continued emphasis on defense modernization, autonomous warfare technologies, and enhanced military preparedness is expected to further strengthen the growth of the Asia Pacific Military Drones Market over the forecast period.

Access Full Report @ https://www.databridgemarketresearch.com/reports/asia-pacific-military-drones-market

As per Data Bridge Market Research analyzes that the Asia-Pacific Military Drones Market is expected to reach USD 10.58 billion by 2033 from USD 4.49 billion in 2025, growing at a substantial CAGR of 11.6% in the forecast period of 2026 to 2033.

Key Findings of the Study

Growth potential in autonomous swarm drones, loitering munitions, and AI-enabled battlefield systems

The growing focus on defense modernization and next-generation warfare capabilities is creating significant growth opportunities in the Asia Pacific Military Drones Market. Rapid adoption of autonomous swarm drones, loitering munitions, AI-enabled battlefield systems, and advanced unmanned combat platforms is driving increased investment in military drone development and deployment across the region.

At the same time, rising defense budgets and expanding indigenous defense manufacturing initiatives are encouraging manufacturers to develop highly autonomous, AI-powered unmanned systems for intelligence, surveillance and reconnaissance (ISR), electronic warfare, precision strike, border security, and collaborative combat operations. Major companies such as Aviation Industry Corporation of China (AVIC), China Aerospace Science and Technology Corporation (CASC), Israel Aerospace Industries, General Atomics, and Boeing are investing in next-generation drone technologies and expanding advanced unmanned defense portfolios. Countries such as China, India, Japan, South Korea, and Australia are emerging as key markets for military drones due to increasing defense expenditure, rapid advancements in autonomous technologies, and growing emphasis on strengthening future battlefield capabilities.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Year

|

2024 (Customizable 2018-2023)

|

|

Quantitative Units

|

Revenue in USD Billion

|

|

Segments Covered

|

By Platform Type (Fixed-Wing Military Drones, Rotary-Wing Military Drones, Hybrid VTOL Military Drones, Loitering Munition Systems, and Nano, Micro & Small Military Drones), Mission Type (Intelligence, Surveillance & Reconnaissance (ISR), Combat & Strike Operations, Electronic Warfare Missions, Maritime Operations, Combat Support Missions, and Homeland Security & Border Protection), Component (Hardware, Software, and Services), Autonomy Level (Remotely Piloted Systems, Semi-Autonomous Systems, Highly Autonomous Systems, Fully Autonomous Combat Systems, and Swarm Autonomous Systems), Technology Type (Conventional UAV Systems, AI-Enabled UAV Systems, Swarm Drone Systems, Manned-Unmanned Teaming (MUM-T) Systems, Collaborative Combat Aircraft (CCA), Stealth Drone Systems, and Hypersonic UAV Concepts), Range (Short Range Drones, Medium Range Drones, and Long Range Drones), End User (Army, Air Force, Navy, Marine Forces,) Special Operations Forces, Border Security Forces, Homeland Security Agencies, Intelligence Agencies, Joint Defense Commands, Defense Research Organizations, National Guard & Reserve Forces, Space & Strategic Commands, Coast Guard Organizations, Defense Logistics & Support Commands, Military Training & Education Institutions, Peacekeeping & Multinational Security Forces, Defense Procurement & Acquisition Agencies, and Military Medical & Disaster Response Units), Deployment Architecture (Standalone UAV Platforms, Network-Centric UAV Systems, Swarm Drone Ecosystems, Manned-Unmanned Teaming Platforms, Multi-Domain Command & Control Ecosystems, and AI-Driven Autonomous Battle Networks)

|

|

Countries Covered

|

China, India, Japan, South Korea, Australia, Malaysia, Taiwan, Thailand, Singapore, Indonesia, New Zealand, Philippines, Hong Kong, and Rest of Asia-Pacific.

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis.

|

Segment Analysis

The Asia Pacific military drones market is segmented into eight notable segments based on the platform type, mission type, component, autonomy level, technology type, range, end user, and deployment architecture.

- On the basis of Platform Type, the market is segmented into Fixed-Wing Military Drones, Rotary-Wing Military Drones, Hybrid VTOL Military Drones, Combat UAVs (UCAVs), Loyal Wingman / Collaborative Combat Aircraft (CCA), Loitering Munition Systems, and Nano, Micro & Small Military Drones

In 2026, the Fixed-Wing Military Drones segment is expected to dominate the Asia Pacific military drones market

In 2026, the Fixed-Wing Military Drones segment is expected to dominate the market with a market share of 42.73% due to its extensive operational endurance, long-range strike and surveillance capability, and widespread deployment across ISR, combat, and reconnaissance missions, supported by increasing defense modernization programs, cross-border security requirements, and rising demand for persistent intelligence across land and maritime domains in the Asia Pacific region.

- On the basis of Mission Type, the market is segmented into Intelligence, Surveillance & Reconnaissance (ISR), Combat & Strike Operations, Electronic Warfare Missions, Maritime Operations, Combat Support Missions, and Homeland Security & Border Protection

In 2026, the Rapeseed (Canola) Oil segment is expected to dominate the Asia Pacific Military Drones Market

In 2026, the Intelligence, Surveillance & Reconnaissance (ISR) segment is expected to dominate the market with a market share of 34.49% due to the increasing demand for real-time battlefield intelligence, rising cross-border security tensions, expanding maritime monitoring requirements, and growing deployment of UAVs for continuous surveillance across strategic and high-risk regions in the Asia Pacific landscape.

- On the basis of Component, the market is segmented into Hardware, Software, and Services. In 2026, the Hardware segment is expected to dominate the market with a market share of 72.85%

- On the basis of Autonomy Level, the market is segmented into Remotely Piloted Systems, Semi-Autonomous Systems, Highly Autonomous Systems, Fully Autonomous Combat Systems, and Swarm Autonomous Systems. In 2026, Remotely Piloted Systems segment is expected to dominate the market with a market share of 58.75%

- On the basis of Technology Type, the market is segmented into Conventional UAV Systems, AI-Enabled UAV Systems, Swarm Drone Systems, Manned-Unmanned Teaming (MUM-T) Systems, Collaborative Combat Aircraft (CCA), Stealth Drone Systems, and Hypersonic UAV Concepts. In 2026, Conventional UAV Systems segment is expected to dominate the market with a market share of 53.07%

- On the basis of Range, the market is segmented into Short Range Drones, Medium Range Drones, and Long Range Drones. In 2026, the Long Range Drones segment is expected to dominate the market with a market share of 47.53%

- On the basis of End User, the market is segmented into Army, Air Force, Navy, Border Security Forces, Special Operations Forces, Marine Forces, Homeland Security Agencies, Intelligence Agencies, Joint Defense Commands, Coast Guard Organizations, Defense Research Organizations, Military Medical & Disaster Response Units, National Guard & Reserve Forces, Space & Strategic Commands, Defense Procurement & Acquisition Agencies, Defense Logistics & Support Commands, Military Training & Education Institutions, and Peacekeeping & Multinational Security Forces. In 2026, the Army segment is expected to dominate the market with a market share of 34.95%

- On the basis of deployment architecture, the market is segmented into standalone uav platforms, network-centric uav systems, swarm drone ecosystems, manned-unmanned teaming platforms, multi-domain command & control ecosystems, and ai-driven autonomous battle networks. In 2026, standalone uav platforms segment is expected to dominate the market with a market share of 42.75%

Major Players

Data Bridge Market Research analyzes Aviation Industry Corporation of China, Ltd. (AVIC) (China), General Atomics (U.S.), Lockheed Martin Corporation (U.S.), Elbit Systems Ltd (Israel), Boeing (U.S.)) as the major market players of the Asia Pacific Military Drones Market.

Market Developments

- In June 2025, Taiwan signed a deal with Auterion to bring battlefield-tested drone software into its defence ecosystem. Reuters said the software could eventually support millions of drones, showing strong APAC opportunity in AI-enabled battlefield systems, autonomous mission control, and smart drone coordination. The value was not disclosed, but the scale shows rising demand for software-led military drone capability.

- In October 2025, South Korea’s Seoul ADEX 2025 showcased AI-powered suicide drones and advanced unmanned combat systems. Reuters also reported that South Korea’s 2026 defence budget would rise by 8.2% to around USD 47.1 billion. This creates a clear opportunity for loitering munitions and AI-enabled battlefield drones, as growing defence budgets can support procurement, testing, and future deployment of autonomous military systems.

- In December 2025, the U.S. approved an USD 11.1 billion arms package for Taiwan that included Altius loitering munition drones. Reuters noted that the package supports Taiwan’s asymmetric warfare strategy, which focuses on smaller, mobile, and cost-effective weapons. This is a strong opportunity signal for APAC because it shows growing regional interest in loitering munitions and smart strike drones for future battlefield use

- In March 2022, Anduril Industries announced its expansion into Australia through the establishment of Anduril Australia, an independent subsidiary headquartered in Sydney. The company stated plans to design, develop, manufacture, and market major defense technologies in Australia, including autonomous systems, artificial intelligence solutions, and next-generation defense capabilities, while creating engineering and manufacturing jobs across the country. The expansion strengthened Anduril's presence in the Asia-Pacific region

- In July 2025, BAE Systems successfully demonstrated a major advancement in drone warfare by launching APKWS laser-guided rockets from its TRV-150 unmanned aerial system and destroying both air and ground targets during trials in the United States. The demonstration marked the first time an APKWS-guided munition had been used in an air-to-air engagement from a drone, showcasing a low-cost solution for countering unmanned aerial threats while maintaining strike capabilities against ground targets. The successful trial strengthens BAE Systems' position in the rapidly growing autonomous defense market

Regional Analysis

Geographically, the countries covered in the Asia Pacific Military Drones Market report are the China, India, Japan, South Korea, Australia, Malaysia, Taiwan, Thailand, Singapore, Indonesia, New Zealand, Philippines, Hong Kong, and Rest of Asia-Pacific.

As per Data Bridge Market Research analysis:

Germany is expected to be the dominant and the fastest-growing country in the Europe steel for data centers construction market

China is expected to dominate the Asia Pacific Military Drones Marketdue to its strong industrial manufacturing base, advanced automotive sector, well-established chemical and lubricant industries, and increasing adoption of sustainable bio-based products. The country’s focus on environmental compliance, renewable energy expansion, industrial automation, and high demand for bio-lubricants, transformer fluids, and specialty esters continues to support significant market growth and consumption.

For more detailed information about the Europe steel for data centers construction market report, click here – https://www.databridgemarketresearch.com/reports/asia-pacific-military-drones-market