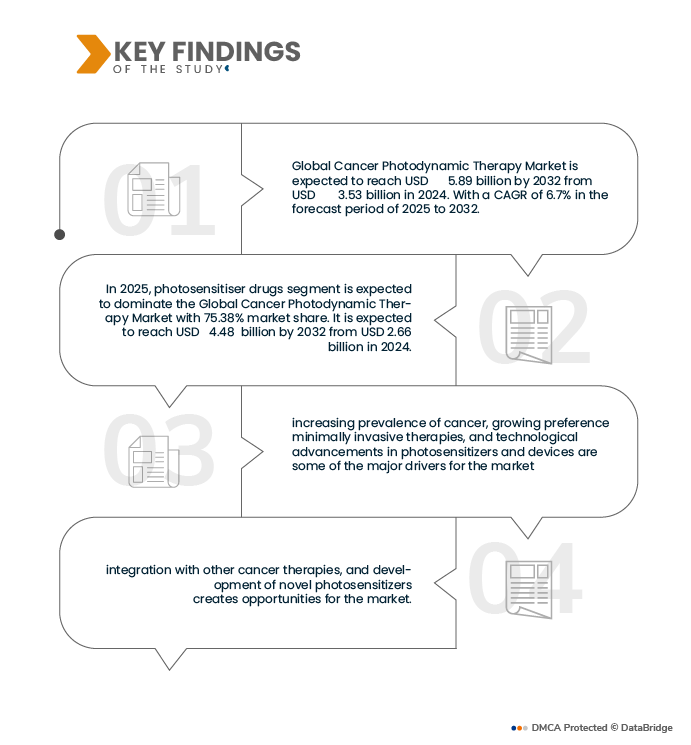

The increasing prevalence of cancer globally is one of the foremost drivers fuelling demand for therapies such as photodynamic therapy (PDT). As populations grow and age, and as diagnostic tools improve, more cancer cases are being detected each year. Higher rates of risk-factors such as tobacco use, obesity, sedentary lifestyles, air pollution, and infections in low- and middle-income countries are also contributing to rising incidence. With more patients requiring effective, less invasive, and cost-efficient localised treatment modalities, PDT becomes more attractive. This rising cancer burden stresses health systems, creating urgent pressure for therapies that can improve outcomes, reduce side effects, and be deployed more widely.

For instances,

- In February 2024, WHO reported that over 35 million new cancer cases are predicted by 2050 globally, a 77 percent increase from the estimated 20 million cases in 2022.

- In April 2024, the American Cancer Society published “Global Cancer Statistics, 2024,” confirming ~20 million newly diagnosed cancer cases in 2022 and 9.7 million cancer deaths worldwide; projected new cancer cases are expected to rise to ~35 million by 2050.

- In April 2025, CDC’s US Cancer Statistics reported rising incidence among women and among younger adults, while also noting that although overall cancer death rate has been falling, increasing incidence in certain populations is a concern

- In May 2024, report published on PubMed by Global Cancer Observatory (GLOBOCAN) estimated nearly 20 million new cancer cases worldwide and 9.7 million deaths.

- In March 2023 report published on Pub Med by India’s National Cancer Registry Programme (ICMR-NCRP) estimated 1,461,427 incident cancer cases in 2022, with projections rising to about 1,570,000 by 2025.

These instances from WHO projections, peer-reviewed cancer registry data, national government registries, and large surveys—paint a clear and recent picture: cancer incidence is rising steadily across many countries and demographic groups. India, for example, shows not only increasing raw numbers but also rising incidence projections. Globally, mortality remains high and the absolute number of new cases is set to nearly double by 2050. This pervasive increase in prevalence underscores the pressing need for treatment modalities that are safe, localised, lower in systemic harm, and adaptable to diverse healthcare settings. In that context, PDT stands out as a market whose growth is logically aligned with rising cancer burden and unmet therapeutic needs.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-cancer-photodynamic-therapy-market

Data Bridge market research analyzes that Global Cancer Photodynamic Therapy Market is expected to reach USD 5.89 billion by 2032 from USD 3.53 billion in 2024, growing with a substantial CAGR of 6.7% in the forecast period of 2025 to 2032.

Key Findings of the Study

Integration With Other Cancer Therapies

The ability of photodynamic therapy (PDT) to produce localized tumour cell killing while stimulating immune responses positions it as an attractive partner for multimodal cancer treatment. Rising evidence shows PDT can increase tumour antigen release, modulate the tumour microenvironment, and enhance infiltration or activation of immune cells — mechanisms that can synergize with immune checkpoint inhibitors, therapeutic cancer vaccines, chemotherapy or radiotherapy. Combining PDT with systemic therapies may convert local control into durable systemic responses, enable dose reductions of toxic agents, and expand indications (for example, unresectable or metastatic disease). As clinical and translational research multiplies, integration with other modalities represents a high-value pathway to broaden PDT’s clinical relevance and commercial uptake.

For instances,

- In April 2021, Department of Respiratory and Critical Care Medicine announced a Phase I pilot study combining intratumoural PDT with PD-1 blockade to evaluate safety and immune activation in thoracic malignancies.

- In July 2023, Scientific Reports published evidence that PDT increased tumour immunogenicity and upregulated costimulatory molecules in murine models, supporting rationale for combining PDT with immune checkpoint inhibitors.

- In February 2024, Frontiers in Immunology reviewed mechanisms by which PDT can synergize with immunotherapies, noting multiple translational studies and recommending combined-modality clinical testing.

- In January 2024, MDPI — International Journal of Molecular Sciences reviewed advances in PDT and documented preclinical and early clinical studies where PDT was combined with chemotherapy or chemoradiation to enhance tumour response and overcome resistance.

- In August 2024, reviews on NIR-activated PSs and photoimmunotherapy highlighted development of photoimmunoconjugates and antibody-targeted PDT agents designed to pair directly with immune checkpoint inhibitors, supporting joint development and regulatory strategies.

PDT is evolving from a stand-alone local therapy into a valuable partner in multimodal cancer care. Preclinical studies show its immunogenic effects can boost systemic responses when combined with immunotherapies, while early clinical trials are testing combinations with chemotherapy, radiotherapy, and surgery. Advances in targeting and light-delivery technologies make these regimens safer and more feasible. For industry, this opens clear opportunities for co-development partnerships, combination trial designs, and differentiated reimbursement strategies. Integration with other cancer therapies is therefore one of the strongest avenues to broaden PDT’s clinical impact and market potential.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2025 to 2032

|

|

Base Year

|

2024

|

|

Historic Years

|

2023 (Customizable to 2018-2022)

|

|

Quantitative Units

|

Revenue in USD billion

|

|

Segments Covered

|

By Product Type (Photosensitizer Drugs, Photodynamic Therapy Devices, Accessories & Consumables), By Cancer Indication (Skin & Cutaneous Oncology, Head & Neck, Esophageal, Lung, Bladder, Cervical, Prostate), By Therapy Modality (Standalone Therapy, Adjunctive Therapy, Palliative Therapy, Combination Therapy, Others), By Procedure Technique (External Beam, Interstitial Delivery, Intracavitary Delivery, Intraoperative Delivery, Others), By Disease Stage (Early-Stage Cancer, Late-Stage Cancer), By Patient Demographics (Pediatric, Adults, Geriatric), By End User (Hospitals, Dermatology & Skin-Cancer Clinics, Ambulatory Surgical Centers, Academic & Research Institutes, Others), By Distribution Channel (Direct Tenders, Third-Party Distributors, Online, Others)

|

|

Countries Covered

|

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

The Global Cancer Photodynamic Therapy Market is segmented into eight notable segments based on product type, cancer indication, therapy modality, procedure technique, disease stage, patient demographics, end user, and distribution channel.

- On the basis of product type, the market is segmented into photosensitiser drugs and photodynamic therapy devices

In 2025, the photosensitiser drugs segment is expected to dominate the market

In 2025, the photosensitiser drugs segment is expected to dominate the market with a market share of 75.38% due to widespread adoption in PDT, technological advancements, rising prevalence of cancer and skin disorders, favourable regulatory approvals, and growing awareness and preference for minimally invasive treatments.

- On the basis of cancer indication, the market is segmented into skin & cutaneous oncology, head & neck, esophageal, lung, bladder, cervical, and prostate.

In 2025, the skin & cutaneous oncology segment is expected to dominate the market

In 2025, the skin & cutaneous oncology segment is expected to dominate the market with a market share of 52.59% due to availability of increasing prevalence of skin cancers and growing adoption of minimally invasive photodynamic therapies.

- On the basis of therapy modality, the market is segmented into standalone therapy, adjunctive therapy, palliation therapy, and others

In 2025, the standalone therapy segment is expected to dominate the market

In 2025, the standalone therapy segment is expected to dominate the market with a market share of 41.67% due to its effectiveness as a primary treatment option and increasing preference for minimally invasive therapies in oncology.

- On the basis of therapy modality, the market is segmented into standalone therapy, adjunctive therapy, palliation therapy, and others

In 2025, the standalone therapy segment is expected to dominate the market

In 2025, the standalone therapy segment is expected to dominate the market with a market share of 41.67% due to its effectiveness as a primary treatment option and increasing preference for minimally invasive therapies in oncology.

- On the basis of procedure technique, the market is segmented into external beam, intracavitary (endoscopic) delivery, interstitial (internal) delivery, and others

In 2025, the external beam segment is expected to dominate the market

In 2025, the external beam segment is expected to dominate the market with a market share of 69.22% due to its widespread use in cancer treatment, high precision in targeting tumors, and increasing adoption of advanced radiotherapy technologies.

- On the basis of disease stage, the market is segmented into early-stage cancer and late-stage cancer.

In 2025, the early-stage cancer segment is expected to dominate the market

In 2025, the early-stage cancer segment is expected to dominate the market with a market share of 81.65% due to its increasing awareness about early detection, growing adoption of minimally invasive therapies, and higher treatment success rates at initial stages of cancer.

- On the basis of patient demographics, the market is segmented into geriatric, adults, and pediatric

In 2025, the geriatric segment is expected to dominate the market

In 2025, the geriatric cancer segment is expected to dominate the market with a market share of 67.66% due to rising aging population, higher cancer prevalence among older adults, and increasing demand for targeted and age-specific oncology treatments.

- On the basis of end user, the market is segmented into hospitals, dermatology & skin-cancer clinics, ambulatory surgical centers (ASCS), academic & research institutes, and others.

In 2025, the hospitals segment is expected to dominate the market

In 2025, the hospitals cancer segment is expected to dominate the market with a market share of 41.80% due to the availability of advanced treatment facilities, access to specialized oncology care, and the ability to provide comprehensive cancer management under one roof.

- On the basis of distribution channel, the market is segmented into direct tender, third party distributors, online and others

In 2025, the direct tender segment is expected to dominate the market

In 2025, the direct tender cancer segment is expected to dominate the market with a market share of 51.18% due to the availability of advanced treatment facilities, access to specialized oncology care, and the ability to provide comprehensive cancer management under one roof.

Major Players

Novartis Pharma AG (Switzerland), Galderma SA (Switzerland), Bausch Health Companies Inc. (Canada), Photocure ASA (Norway), ADVANZ PHARMA Corp. (U.K.), among others.

Latest Developments in Asia-Pacific Cancer Photodynamic Therapy Market

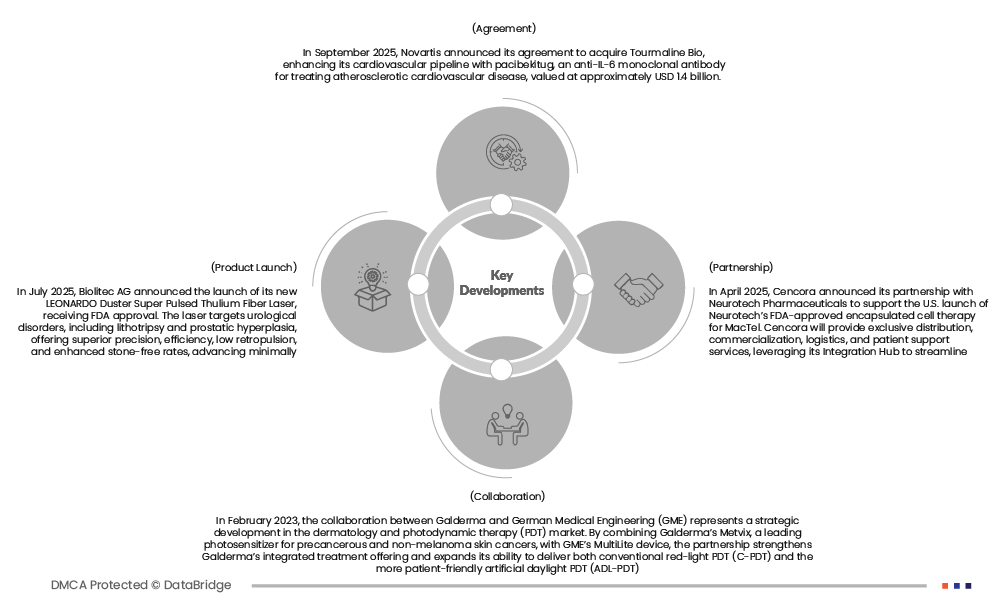

- In September 2025, Novartis announced its agreement to acquire Tourmaline Bio, enhancing its cardiovascular pipeline with pacibekitug, an anti-IL-6 monoclonal antibody for treating atherosclerotic cardiovascular disease, valued at approximately USD 1.4 billion.

- In July 2025, Biolitec AG announced the launch of its new LEONARDO® Duster Super Pulsed Thulium Fiber Laser, receiving FDA approval. The laser targets urological disorders, including lithotripsy and prostatic hyperplasia, offering superior precision, efficiency, low retropulsion, and enhanced stone-free rates, advancing minimally invasive urology treatments globally

- In June 2025, Photocure launched direct sales, marketing, and distribution of Hexvix® in Spain, strengthening its European presence. With reimbursement approval and expert support, Spain’s high bladder cancer incidence offers significant growth potential for Hexvix-driven Blue Light Cystoscopy adoption.

- In April 2025, Cencora announced its partnership with Neurotech Pharmaceuticals to support the U.S. launch of Neurotech’s FDA-approved encapsulated cell therapy for MacTel. Cencora will provide exclusive distribution, commercialization, logistics, and patient support services, leveraging its Integration Hub to streamline market access and care coordination.

- In February 2023, the collaboration between Galderma and German Medical Engineering (GME) represents a strategic development in the dermatology and photodynamic therapy (PDT) market. By combining Galderma’s Metvix, a leading photosensitizer for precancerous and non-melanoma skin cancers, with GME’s MultiLite device, the partnership strengthens Galderma’s integrated treatment offering and expands its ability to deliver both conventional red-light PDT (C-PDT) and the more patient-friendly artificial daylight PDT (ADL-PDT).

As per Data Bridge Market Research analysis:

Geographically, the countries covered in the Global Cancer Photodynamic Therapy Market report are North America, Euorpe, Asia-Pacific, Middle East and Africa, South America. Europe is further segmented into Germany, U.K., Italy, France, Spain, Switzerland, Russia, Turkey, Belgium, Netherlands, Denmark, Norway, Finland, Sweden, Rest of Europe. The Asia-Pacific is further segmented into China, Japan, South Korea, India, Thailand, Singapore, Malaysia, Hong Kong, Indonesia, Australia, New Zealand, Philippines, Taiwan, rest of Asia-Pacific. The North America is further segmented into U.S., Canada, and Mexico. The South America is further segmented into Brazil, Argentina, Bolivia, Chile, Columbia, Ecuador, Paraguay, Peru, Uruguay, Venezuela, and rest of South America. The Middle East and Africa is further segmented into South Africa, Egypt, Saudi Arabia, U.A.E, Israel, Bahrain, Kuwait, Oman, Qatar, Rest of Middle East and Africa.

North America is the dominating country in Global Cancer Photodynamic Therapy Market

North America leads the Global Cancer Photodynamic Therapy Market, driven by the advanced healthcare infrastructure, high adoption of innovative treatments, strong R&D investments, favorable reimbursement policies, and awareness of minimally invasive therapies.

Asia-Pacific is expected to be the fastest growing country in Global Cancer Photodynamic Therapy Market

Japan is expected to witness significant growth in the Global Cancer Photodynamic Therapy Market, driven by rising cancer prevalence, increasing healthcare expenditure, and growing awareness of advanced treatment options. Rapid improvements in healthcare infrastructure, expansion of specialized cancer treatment centers, and government initiatives promoting early diagnosis and innovative therapies are driving adoption.

For more detailed information about the Global Cancer Photodynamic Therapy Market report, click here – https://www.databridgemarketresearch.com/reports/global-cancer-photodynamic-therapy-market