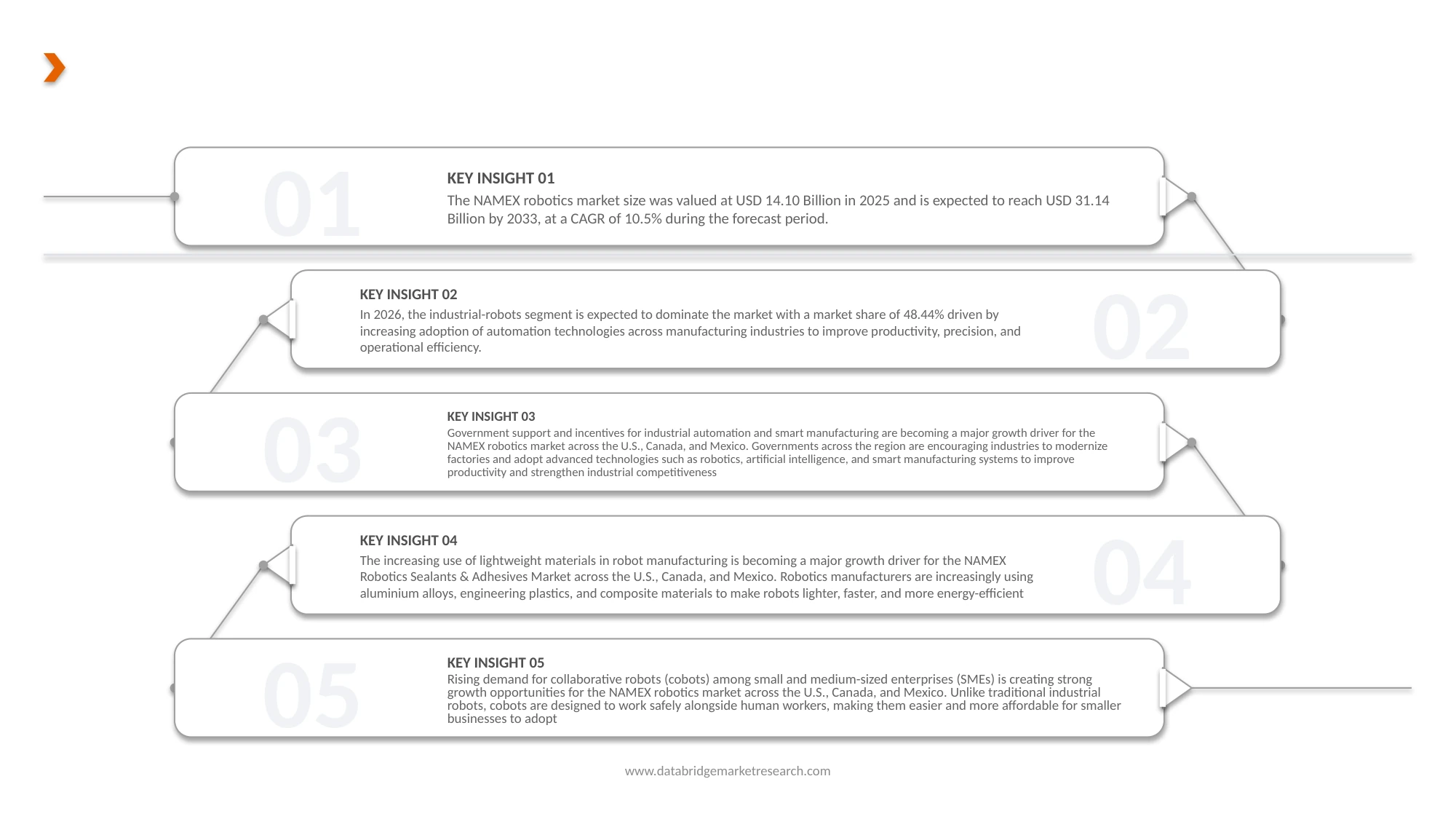

Government support and incentives for industrial automation and smart manufacturing are becoming a major growth driver for the NAMEX robotics market across the U.S., Canada, and Mexico. Governments across the region are encouraging industries to modernize factories and adopt advanced technologies such as robotics, artificial intelligence, and smart manufacturing systems to improve productivity and strengthen industrial competitiveness. In the U.S., initiatives led by the Department of Energy, Manufacturing USA, and the CHIPS and Science Act are supporting investments in automation, semiconductor production, and smart factory development. These programs are helping manufacturers improve operational efficiency, reduce production costs, and strengthen domestic manufacturing capabilities.

Access Full Report @ https://www.databridgemarketresearch.com/reports/namex-robotics-market

Data Bridge market research analyzes that the NAMEX Robotics Market is expected to reach USD 14.11 billion by 2033 from USD 31.14 billion in 2025, growing at a substantial CAGR of 10.5% in the forecast period of 2026 to 2033.

Key Findings of the Study

Increasing Labor Shortages Pushing Companies Toward Robotic Automation.

Increasing labor shortages across the U.S., Canada, and Mexico are becoming a major driver for the growth of the NAMEX robotics market. Many industries, including manufacturing, automotive, warehousing, logistics, and food processing, are facing difficulties in finding skilled workers for repetitive and physically demanding jobs. Rising wage costs and high employee turnover are further encouraging companies to adopt robotic automation systems to maintain productivity and reduce long-term labor expenses. In the U.S. and Canada, aging workforce challenges and growing demand for skilled labor are increasing investments in industrial robots, AI-based automation, and smart manufacturing technologies. Companies are also using robotics to improve workplace safety by reducing human involvement in hazardous and repetitive tasks. Meanwhile, in Mexico, the rapid expansion of automotive and electronics manufacturing, along with increasing nearshoring investments, is driving strong demand for automated production systems and industrial robots.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2018-2023)

|

|

Quantitative Units

|

Revenue in USD billion

|

|

Segments Covered

|

By Robot Type (Industrial Robots, Service Robots, Mobile Robots, and Others), By Payload Capacity (Light Payload Robots, Medium Payload Robots, Heavy Payload Robots, and Ultra-Heavy Payload Robots), By Degree of Freedom (6 to 7 DOF Robots, 8 and Above DOF Robots, and 3 to 5 DOF Robots), By Mobility Type (Wheeled Robots, Mobile Robots, Fixed Robots, Tracked Robots, Hybrid Mobility Robots, and Legged Robots), By Level of Autonomy (Fully Autonomous Robots, Semi-Autonomous Robots, Teleoperated/Remote Controlled Robots, and Manual Robots with Assistance), By End-Effector / Tooling (Grippers, Welding Tools, Sensor and Vision Systems as End-Effectors, Cutting Tools, Dispensing Systems, Painting Sprayers, and Specialized End-Effectors), By Core Technology (Actuation, Artificial Intelligence & Machine Learning, Sensing, Control Systems, Navigation & Mapping, Power Source, Connectivity, and Software & Platform), By Industry Vertical (Automotive, Manufacturing, Logistics & Warehousing, Healthcare & Medical, Defense & Security, Consumer & Household, Agriculture, Retail & Hospitality, Construction, Education & Research, and Others), By Deployment Mode (On-Premise Deployment, Cloud-Based Deployment, and Hybrid Deployment)

|

|

Countries Covered

|

North America

· U.S.

· Canada

· Mexico

|

|

Market Players Covered

|

· ABB Ltd. (Switzerland)

· FANUC Corporation (Japan)

· KUKA AG (Germany)

· Yaskawa Electric Corporation (Japan)

· Universal Robots A/S (Teradyne Inc.) (Denmark)

· Rockwell Automation, Inc. (U.S.)

· Locus Robotics (U.S.)

· Intuitive Surgical, Inc. (U.S.)

· iRobot Corporation (U.S.)

· Boston Dynamics, Inc. (U.S.)

· Figure AI, Inc. (U.S.)

· Seegrid Corporation (U.S.)

· DENSO Corporation (Japan)

· Stäubli International AG (Switzerland)

· Ghost Robotics Corporation (U.S.)

· Symbotic Inc. (U.S.)

· Agility Robotics (U.S.)

· Aethon, Inc. (U.S.)

· GreyOrange Pte. Ltd. (U.S.)

· L3Harris Technologies, Inc. (U.S.)

· OMRON Corporation (Japan)

· Epson Robots (Seiko Epson Corporation) (Japan)

· Zebra Technologies Corporation (U.S.)

· AutoGuide Mobile Robots (U.S.)

· Vecna Robotics, Inc. (U.S.)

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

The NAMEX robotics market is categorized into nine notable segments based on the robot type, payload capacity, degree of freedom, mobility type, level of autonomy, end-effector / tooling, core technology, industry vertical, and deployment mode.

- On the basis of robot type, the market is segmented into industrial robots, service robots, mobile robots, and others.

In 2026, the industrial robots segment is expected to dominate the market

On the basis of robot type, the market is segmented into industrial robots, service robots, mobile robots, and others. In 2026, the industrial robots segment is expected to dominate with 49.83% % market share, growing with the CAGR of 10.2% in the forecast period of 2026 to 2033, driven by industrial robots segment include strong adoption in automotive and manufacturing industries, where precision, speed, and repeatability are critical. Demand for welding, assembly, and material handling automation is high due to labor shortages and productivity requirements.

In 2026, the light payload robots segment is expected to dominate the market

- On the basis of payload capacity, the market is segmented into light payload robots, medium payload robots, heavy payload robots, and ultra-heavy payload robots. In 2026, the light payload robots segment is expected to dominate with 33.26% market share, growing with the CAGR of 10.8% in the forecast period of 2026 to 2033, driven by their versatility in handling assembly, packaging, welding, and material movement across manufacturing and logistics industries. They offer an optimal balance between strength, precision, and cost-effectiveness, making them suitable for a wide range of industrial applications. Strong adoption in automotive production lines and electronics manufacturing further drives demand.

In 2026, the 6 to 7 DOF robots segment is expected to dominate the market

- On the basis of degree of freedom, the market is segmented into 6 to 7 DOF robots, 8 and above DOF robots, 3 to 5 DOF robots. In 2026, the 6 to 7 DOF robots segment is expected to dominate with 57.59% market share, growing with the CAGR of 10.4% in the forecast period of 2026 to 2033, due to their ability to perform complex, precise, and multi-axis movements required in automotive and industrial manufacturing applications. They provide optimal flexibility for welding, assembly, painting, and material handling tasks. Their proven reliability, ease of integration, and widespread availability make them industry standards.

In 2026, the wheeled robots segment is expected to dominate the market

- On the basis of mobility type, the market is segmented into wheeled robots, mobile robots, fixed robots, tracked robots, hybrid mobility robots, and legged robots. In 2026, the wheeled robots segment is expected to dominate with 36.53% market share, growing with the CAGR of 11.1% in the forecast period of 2026 to 2033, driven by their cost-effectiveness, stability, and efficiency in structured environments like warehouses, factories, and distribution centers. They are widely used for material transport and logistics operations where smooth surfaces and predictable routes exist.

In 2026, the fully autonomous robots segment is expected to dominate the market

- On the basis of level of autonomy, the market is segmented into fully autonomous robots, semi-autonomous robots, teleoperated/remote controlled robots, and manual robots with assistance. In 2026, the fully autonomous robots segment is expected to dominate with 36.41% market share, growing with the CAGR of 10.9% in the forecast period of 2026 to 2033, driven by the advancements in AI, machine learning, and sensor technologies that enable independent decision-making and operation. Industries prefer them for improving efficiency, reducing labor dependency, and enhancing precision in manufacturing and logistics.

In 2026, the grippers segment is expected to dominate the market

- On the basis of end-effector / tooling, the market is segmented into grippers, welding tools, sensor and vision systems as end-effectors, cutting tools, dispensing systems, painting sprayers, and specialized end-effectors. In 2026, the grippers segment is expected to dominate with 32.34% market share, growing with the highest CAGR of 10.9% in the forecast period of 2026 to 2033, driven by their extensive use in pick-and-place operations, assembly lines, and material handling across industries. They are essential for handling a wide variety of objects with precision and speed, making them a core component of industrial automation systems. Their compatibility with different robotic arms and cost-effectiveness further support widespread adoption.

In 2026, the actuation segment is expected to dominate the market

- On the basis of core technology, the market is segmented into actuation, artificial intelligence & machine learning, sensing, control systems, navigation & mapping, power source, connectivity, and software & platform. In 2026, the actuation segment is expected to dominate with 18.27% market share, growing with the highest CAGR of 10.3% in the forecast period of 2026 to 2033, as they are fundamental to enabling movement and physical execution in all robotic systems. They are widely used across industrial robots for tasks such as welding, assembly, and material handling. Their reliability, precision, and ability to support heavy workloads make them essential in manufacturing environments.

In 2026, the automotive segment is expected to dominate the market

- On the basis of industry vertical, the market is segmented into automotive, manufacturing, logistics & warehousing, healthcare & medical, defense & security, consumer & household, agriculture, retail & hospitality, construction, education & research, and others. In 2026, the automotive segment is expected to dominate with 22.80% market share, growing with the highest CAGR of 10.3% in the forecast period of 2026 to 2033, driven by the extensive use of robotics in welding, painting, assembly, and inspection processes. High production volumes, precision requirements, and established automation infrastructure drive strong robot adoption. Continuous investment in electric vehicle manufacturing and smart factory development further strengthens demand.

In 2026, the on-premise deployment segment is expected to dominate the market

- On the basis of deployment mode, the market is segmented into on-premise deployment, cloud-based deployment, and hybrid deployment. In 2026, the on-premise deployment segment is expected to dominate with 52.24% market share, growing with the highest CAGR of 10.2% in the forecast period of 2026 to 2033, due to strong demand for data security, operational control, and integration with existing industrial infrastructure. Enterprises prefer on-site systems for reliability, low latency, and compliance with regulatory standards. Manufacturing and automotive industries rely heavily on on-premise robotics systems to ensure uninterrupted operations.

Major Players

- ABB Ltd. (Switzerland)

- FANUC Corporation (Japan)

- KUKA AG (Germany)

- Yaskawa Electric Corporation (Japan)

- Universal Robots A/S (Teradyne Inc.) (Denmark)

- Rockwell Automation, Inc. (U.S.)

- Locus Robotics (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- iRobot Corporation (U.S.)

- Boston Dynamics, Inc. (U.S.)

- Figure AI, Inc. (U.S.)

- Seegrid Corporation (U.S.)

- DENSO Corporation (Japan)

- Stäubli International AG (Switzerland)

- Ghost Robotics Corporation (U.S.)

- Symbotic Inc. (U.S.)

- Agility Robotics (U.S.)

- Aethon, Inc. (U.S.)

- GreyOrange Pte. Ltd. (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- OMRON Corporation (Japan)

- Epson Robots (Seiko Epson Corporation) (Japan)

- Zebra Technologies Corporation (U.S.)

- AutoGuide Mobile Robots (U.S.)

- Vecna Robotics, Inc. (U.S.)

Market Developments

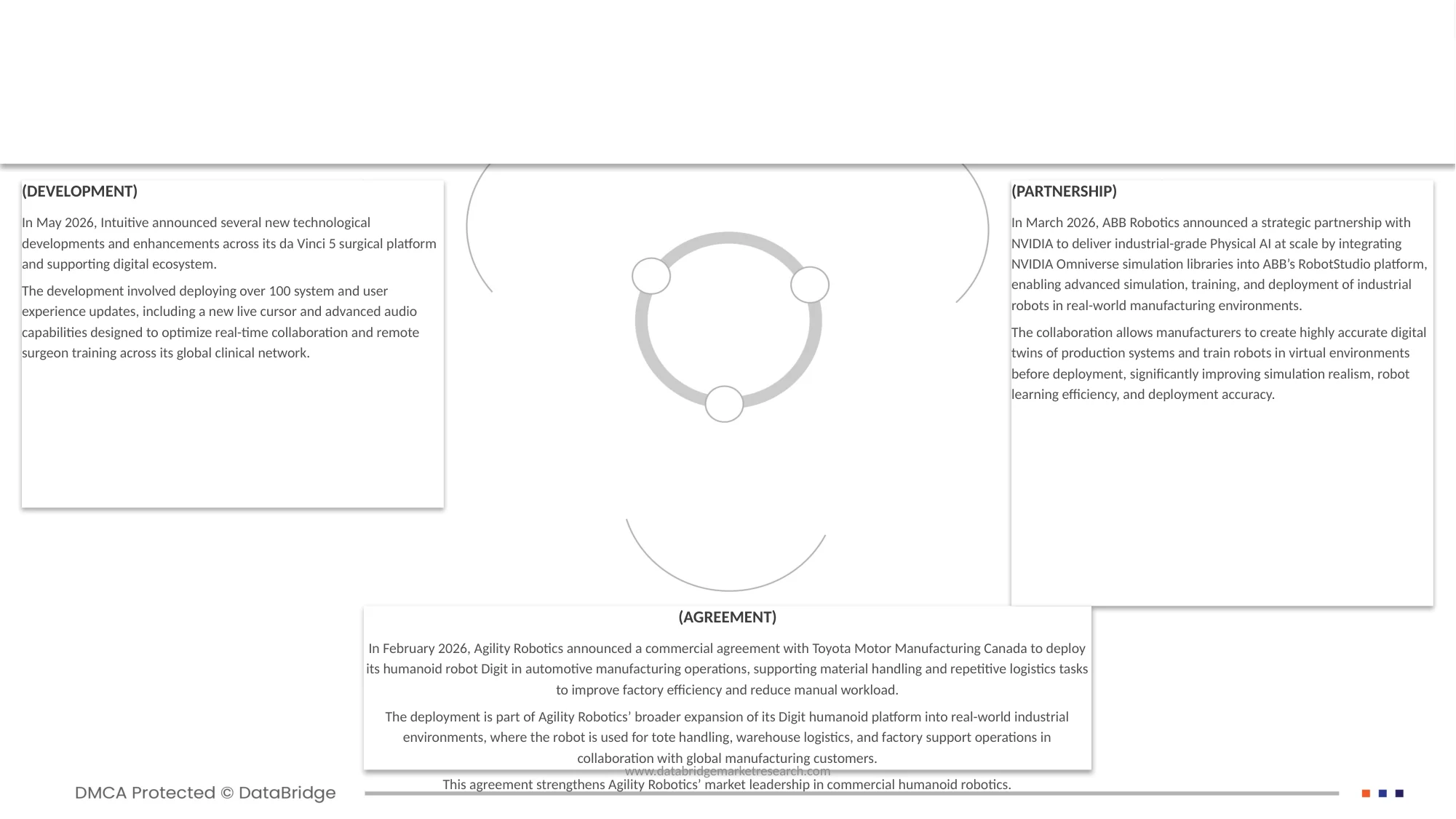

- In March 2026, Intuitive announced the completion of its commercial acquisition and direct operational expansion across Southern Europe. The expansion involved taking full ownership of the da Vinci and Ion robotic-assisted surgery businesses previously managed by ab medica, Abex, and Excelencia Robótica, directly integrating operations across Italy, Spain, Portugal, Malta, and San Marino to scale regional customer support.

- In March 2026, ABB Robotics announced a strategic partnership with NVIDIA to deliver industrial-grade Physical AI at scale by integrating NVIDIA Omniverse simulation libraries into RobotStudio platform, enabling advanced simulation, training, and deployment of industrial robots in real world manufacturing environments. The ABB’s collaboration allows manufacturers to create highly accurate digital twins of production systems and train robots in virtual environments before deployment, significantly improving simulation realism, robot learning efficiency, and deployment accuracy.

- In February 2026, Agility 2026 Agreement Robotics announced a commercial agreement with Toyota Motor Manufacturing Canada to deploy its humanoid robot Digit in automotive manufacturing operations, supporting material handling and repetitive logistics tasks to improve factory efficiency and reduce deployment is part of Agility Robotics’ manual workload. The broader expansion of its Digit humanoid platform into real-world industrial environments, where the robot is used for tote handling, warehouse logistics, and factory support operations in collaboration with global manufacturing customers. This agreement strengthens Agility Robotics’ market leadership in commercial humanoid robotics.

- In August 2025, Symbotic Inc. announced the launch of its next-generation storage system for its warehouse automation platform, designed to significantly improve warehouse performance by increasing storage density and improving overall system efficiency. The new storage architecture enables a more compact warehouse footprint while increasing product capacity, allowing faster movement of goods within the system and improving case-handling speed across automated fulfillment operations. This development strengthens Symbotic’s position in warehouse automation.

- In March 2025, Boston Dynamics accelerated its humanoid processing intelligence by deploying the NVIDIA Jetson Thor computing platform on its Atlas architecture, allowing developers to run complex, multimodal AI models and learned dexterity policies via the Isaac Lab framework.

As per Data Bridge Market Research analysis:

Geographically, the countries covered in the NAMEX robotics market report are U.S., Canada, and Mexico.

U.S. is the dominating country in NAMEX robotics market

U.S. is expected to dominate the robotics market in the NAMEX, due to its strong industrial base, advanced technological ecosystem, and early adoption of automation across key sectors such as automotive, electronics, logistics, and healthcare. The country benefits from the presence of leading robotics manufacturers, AI innovators, and research institutions that continuously drive innovation in robotic hardware, software, and intelligent systems. High labor costs and ongoing labor shortages further accelerate the adoption of robotics to improve productivity, efficiency, and operational consistency across industries.

Mexico NAMEX Robotics Market Insight

Mexico shows steady growth in the NAMEX robotics market due to rapid expansion of e-commerce and warehouse automation is boosting demand for autonomous mobile robots and fulfillment systems. Strong venture capital funding, supportive government policies, and increasing integration of AI, machine learning, and cloud robotics technologies further reinforce the country’s leadership position in the NAMEX robotics market.

For more detailed information about theNAMEX robotics market report, click here – https://www.databridgemarketresearch.com/reports/namex-robotics-market