Asia Pacific Foundry Chemicals Market

Taille du marché en milliards USD

TCAC :

%

USD

1.03 Billion

USD

1.53 Billion

2025

2033

USD

1.03 Billion

USD

1.53 Billion

2025

2033

| 2026 –2033 | |

| USD 1.03 Billion | |

| USD 1.53 Billion | |

| % | |

|

Asia-Pacific Foundry Chemicals Market Segmentation, By Type (Benzene, Formaldehyde, Naphthalene, Phenol, Xylene, and Others), Product Type (Binders, Additive Agents, Coatings, Fluxes, and Others), Foundry Type (Ferrous and Non-Ferrous), Foundry Tool Type (Showel, Trowels, Lifter, Hand Riddle, Vent Wire, Rammers, Swab, Sprue Pins and Cutters, and Others), Foundry Process Type (Thermal galvanization and Electro Less Nickel Plating), Foundry System Type (Sand Cast Systems and Chemically Bonded Sand Cast Systems), Application (Cast Iron, Steel, Aluminium, and Others), Distribution Channel (E-Commerce, Specialty Stores, B2B/Third Party Distributors, and Others) - Industry Trends and Forecast to 2033

What is the Asia-Pacific Foundry Chemicals Market Size and Growth Rate?

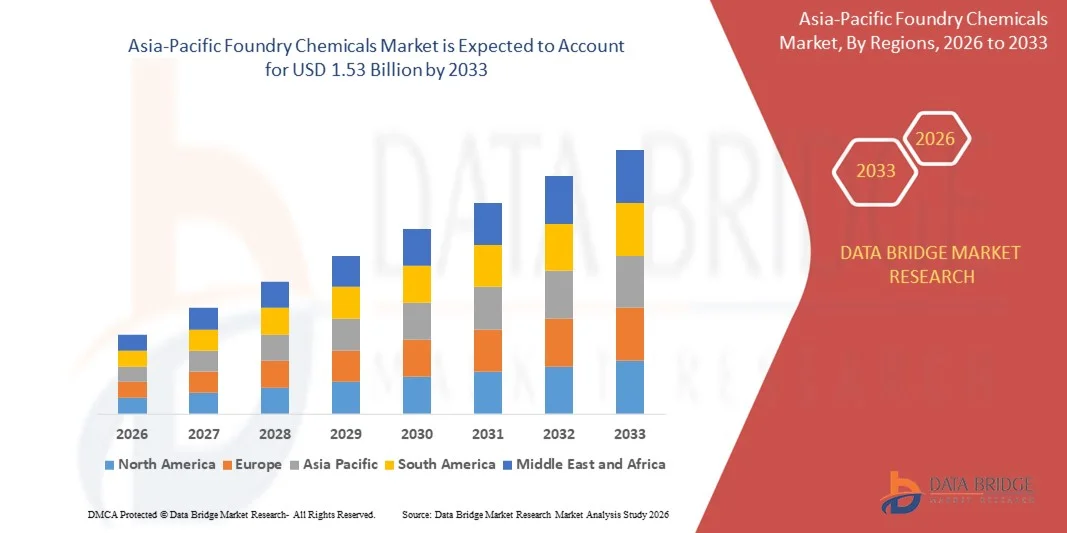

- The Asia-Pacific foundry chemicals market size was valued at USD 1.03 billion in 2025 and is expected to reach USD 1.53 billion by 2033, at a CAGR of 5.1% during the forecast period

- The growing demand for metal casting in the manufacturing of heavy machinery is boosting the foundry chemicals market growth

- Corrodibility of ferrous metals under environmental conditions is hampering the demand for the foundry chemicals market

What are the Major Takeaways of Foundry Chemicals Market?

- Increasing demand for steel in the market is acting as an opportunity for the foundry chemicals market. The stringent environmental regulation regarding chemicals released from foundries is acting as a challenge for hampering the demand of the foundry chemicals market

- China dominated the Asia-Pacific foundry chemicals market with an estimated 38.7% revenue share in 2025, driven by rapid industrialization, large-scale automotive and machinery manufacturing, and strong adoption in construction, renewable energy, and heavy equipment sectors

- India is projected to register the fastest CAGR of 8.1% from 2026 to 2033, driven by increasing use in automotive, construction, renewable energy, and industrial machinery applications. Expanding manufacturing hubs, rising EV adoption, and government-backed industrial modernization programs are boosting demand for fiber and metal matrix composite Foundry Chemicals

- The Formaldehyde segment dominated the market with an estimated 41.2% share in 2025, driven by its high reactivity, excellent binding properties, and wide application across ferrous and non-ferrous casting industries

Report Scope and Foundry Chemicals Market Segmentation

|

Attributes |

Foundry Chemicals Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Foundry Chemicals Market?

Rising Adoption of Advanced, Lightweight, and High-Durability Foundry Chemicals

- The foundry chemicals market is experiencing growing demand for lightweight, corrosion-resistant, and high-performance materials used in automotive, aerospace, industrial machinery, and renewable energy sectors

- Manufacturers are increasingly introducing polymer composites, PTFE-coated alloys, and fiber-reinforced metal-ceramic solutions to improve wear resistance, load capacity, and operational reliability

- Emphasis on energy efficiency, reduced maintenance, and longer lifecycle performance is driving adoption in high-stress and continuous operation environments

- For instance, companies such as SKF, Schaeffler, Trelleborg, GGB, and RBC Bearings are expanding their portfolio of advanced composite bearings and friction-reducing coatings for EVs, wind turbines, industrial automation, and heavy equipment

- High uptake of Foundry Chemicals in electric vehicles, industrial robotics, fluid-handling, and aerospace components is sustaining market expansion

- As industries focus on durability, weight optimization, and lifecycle cost reduction, foundry chemicals are expected to remain critical in next-generation mechanical and industrial systems

What are the Key Drivers of Foundry Chemicals Market?

- Rising demand for maintenance-free, lubrication-free, and high-load capable bearings is significantly boosting foundry chemicals adoption across automotive, aerospace, and industrial sectors

- For instance, during 2024–2025, SKF, Schaeffler, and Trelleborg launched advanced composite and polymer-based solutions designed for extreme temperatures, heavy loads, and extended operating life

- Growing deployment of EVs, wind energy systems, automated machinery, and industrial robots is increasing need for lightweight, durable, and energy-efficient bearings

- Advances in polymer engineering, material composites, and precision manufacturing are enhancing friction resistance, wear performance, and load-bearing capabilities

- Increasing focus on sustainability and energy savings is promoting replacement of conventional metal bearings with composite or polymer alternatives

- Supported by industrial automation, renewable energy expansion, and infrastructure growth, the foundry chemicals market is poised for steady long-term growth

Which Factor is Challenging the Growth of the Foundry Chemicals Market?

- Higher costs of advanced polymers, fibers, and precision-fabricated materials limit adoption in price-sensitive applications

- Volatility in raw material prices and supply-chain disruptions during 2024–2025 increased operational costs for key manufacturers

- Performance constraints under extreme shock loads or misalignment conditions may restrict application in certain heavy-duty industrial systems

- Limited awareness among small-scale manufacturers about lifecycle benefits and long-term cost efficiency slows market penetration

- Competition from traditional metal bearings and low-cost substitutes exerts pricing pressure and reduces differentiation

- To overcome these challenges, companies are focusing on cost-efficient designs, targeted applications, and customer education to drive broader adoption of Foundry Chemicals

How is the Foundry Chemicals Market Segmented?

The market is segmented on the basis of type, product type, foundry type, foundry tool type, foundry process type, foundry system type, distribution channel, and application.

- By Type

The Foundry Chemicals market is segmented into Benzene, Formaldehyde, Naphthalene, Phenol, Xylene, and Others. The Formaldehyde segment dominated the market with an estimated 41.2% share in 2025, driven by its high reactivity, excellent binding properties, and wide application across ferrous and non-ferrous casting industries. Formaldehyde-based chemicals are extensively used in resin formulations, coatings, and core binders, providing strength and durability in high-temperature operations.

The Phenol segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by rising demand for phenolic resins in advanced casting processes, aerospace, and automotive applications. Its superior heat resistance, chemical stability, and ability to produce low-emission cores are accelerating adoption. Increasing focus on sustainable production and improved casting quality further reinforces growth opportunities for phenol-based Foundry Chemicals globally.

- By Product Type

On the basis of product type, the market is segmented into Binders, Additive Agents, Coatings, Fluxes, and Others. The Binders segment dominated with 38.5% share in 2025, supported by strong demand in sand casting, core making, and chemically bonded sand systems. Binders enhance mold strength, reduce defects, and improve surface finish across automotive, construction, and industrial applications.

The Coatings segment is expected to register the fastest CAGR from 2026 to 2033, driven by increasing adoption of heat-resistant and protective coatings in high-precision castings, aerospace, and industrial machinery. Technological advancements in coating formulations that improve thermal insulation, wear resistance, and defect reduction are further strengthening market expansion globally.

- By Foundry Type

Based on foundry type, the market is segmented into Ferrous and Non-Ferrous. The Ferrous segment dominated the market with a 56.7% share in 2025, attributed to its extensive use in steel, iron, and alloy castings for automotive, construction, and heavy machinery sectors. Ferrous foundries require robust chemical solutions for high-temperature molding, binder performance, and surface finish quality.

The Non-Ferrous segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by rising aluminum, copper, and specialty alloy casting in electronics, aerospace, and lightweight automotive applications. Growing industrialization and demand for precision, lightweight components further support non-ferrous Foundry Chemicals adoption.

- By Foundry Tool Type

On the basis of tool type, the market is segmented into Shovel, Trowels, Lifter, Hand Riddle, Vent Wire, Rammers, Swab, Sprue Pins & Cutters, and Others. The Rammers segment dominated with 33.4% share in 2025, widely used for compacting molds and cores in high-quality casting operations. Rammers ensure uniform density, reduced defects, and better mold strength, particularly in heavy-duty industrial and automotive foundries.

The Swab segment is projected to grow at the fastest CAGR from 2026 to 2033 due to rising use in core coating, precision cleaning, and defect-free mold preparation in ferrous and non-ferrous casting. Increasing automation and demand for high-quality castings accelerate swab adoption.

- By Foundry Process Type

On the basis of process type, the market is segmented into Thermal Galvanization and Electro Less Nickel Plating. The Thermal Galvanization segment dominated with a 59.1% share in 2025, driven by strong application in corrosion protection, surface hardening, and high-temperature resistance for industrial components.

The Electro Less Nickel Plating segment is expected to grow at the fastest CAGR from 2026 to 2033, due to its uniform deposition, enhanced wear resistance, and wide adoption in aerospace, automotive, and precision engineering castings. Regulatory emphasis on sustainability and improved coating technologies further supports growth.

- By Foundry System Type

The market is segmented into Sand Cast Systems and Chemically Bonded Sand Cast Systems. The Sand Cast Systems segment dominated with 52.6% share in 2025, owing to its widespread use in ferrous and non-ferrous metal casting, cost-effectiveness, and compatibility with traditional foundries.

The Chemically Bonded Sand Cast Systems segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for high-precision, low-defect castings in automotive, aerospace, and industrial machinery. Advanced binder technologies and high-performance chemicals are accelerating adoption.

- By Application

Based on application, the market is segmented into Cast Iron, Steel, Aluminium, and Others. The Cast Iron segment dominated with a 44.3% share in 2025, driven by extensive use in automotive engines, industrial machinery, and heavy equipment. Cast iron foundries require high-performance binders, coatings, and fluxes for precision, thermal stability, and defect-free output.

The Aluminium segment is expected to grow at the fastest CAGR from 2026 to 2033 due to increasing lightweight automotive and aerospace components, rising industrial automation, and demand for sustainable, high-precision castings.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into E-Commerce, Specialty Stores, B2B/Third Party Distributors, and Others. The B2B/Third Party Distributors segment dominated with 61.8% share in 2025, owing to strong supplier relationships, bulk procurement by industrial users, and customized solutions for high-volume foundries.

The E-Commerce segment is expected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing digitalization, online access to standard and specialty chemicals, and adoption by small and medium-scale foundries. Faster delivery, competitive pricing, and wider product availability support market expansion globally.

Which Region Holds the Largest Share of the Foundry Chemicals Market?

- China dominated the Asia-Pacific foundry chemicals market with an estimated 38.7% revenue share in 2025, driven by rapid industrialization, large-scale automotive and machinery manufacturing, and strong adoption in construction, renewable energy, and heavy equipment sectors

- Rising demand for lightweight, durable, and low-maintenance foundry chemicals in high-load applications reinforces China’s market leadership

- Robust OEM collaborations, advanced manufacturing capabilities, and continuous R&D investments further strengthen long-term market growth.

Japan Foundry Chemicals Market Insight

In Japan, growth is fueled by advanced automotive, aerospace, and industrial machinery sectors. Foundry Chemicals are extensively used in robotics, wind turbines, and precision equipment due to low friction, high wear resistance, and maintenance-free performance. Focus on energy-efficient and lightweight solutions, coupled with strong domestic manufacturing and OEM partnerships, supports steady adoption and ensures long-term market expansion in high-precision applications.

India Foundry Chemicals Market Insight

India is projected to register the fastest CAGR of 8.1% from 2026 to 2033, driven by increasing use in automotive, construction, renewable energy, and industrial machinery applications. Expanding manufacturing hubs, rising EV adoption, and government-backed industrial modernization programs are boosting demand for fiber and metal matrix composite foundry chemicals. Strong focus on energy efficiency and precision casting solutions is accelerating regional market penetration.

South Korea Foundry Chemicals Market Insight

South Korea’s growth is supported by automotive, electronics, and industrial equipment sectors, where Foundry Chemicals are preferred for high-load, low-maintenance, and wear-resistant operations. Increasing deployment in EV components, robotics, and renewable energy installations accelerates adoption. Strong OEM partnerships, technological innovation, and R&D investments reinforce the country’s competitive market position.

Australia Foundry Chemicals Market Insight

Australia shows steady growth driven by construction, mining, and renewable energy sectors. Foundry Chemicals are increasingly used in heavy machinery, industrial equipment, and wind turbines to enhance durability, load performance, and service life. Government-supported industrial upgrades, infrastructure development, and renewable energy initiatives encourage adoption. Expanding local manufacturing capabilities and industrial exports support long-term market expansion in the region.

Which are the Top Companies in Foundry Chemicals Market?

The foundry chemicals industry is primarily led by well-established companies, including:

- Vesuvius (U.K.)

- Imerys (France)

- Saint Gobain Performance Ceramics & Refractories (France)

- Georgia Pacific Chemicals (U.S.)

- DuPont (U.S.)

- ASK Chemicals (U.S.)

- Shandong Crownchem Industries Co., Ltd (China)

- Compax Industrial Systems Pvt. Ltd (India)

- CS ADDITIVE GMBH (Germany)

- CAGroup (U.A.E.)

- Ultraseal India Pvt. Ltd. (India)

- Hüttenes Albertus (Germany)

- CERAFLUX INDIA PVT.LTD. (India)

- Forace Polymers (P) Ltd. (India)

- Scottish Chemical (U.K.)

What are the Recent Developments in Global Foundry Chemicals Market?

- In August 2025, Vesuvius acquired Morgan Advanced’s Molten Metal Systems to strengthen its non-ferrous revenue to 27%, focusing on expansion in India with cost synergies expected to deliver over 50% EBITDA uplift, reinforcing the company’s global market position

- In March 2025, ASK Chemicals launched a new range of low-emission cold-box binders, reducing VOC outputs by 30% to promote sustainable foundry operations in automotive applications, supporting environmentally responsible production practices

- In January 2024, Hüttenes-Albertus International developed bio-based release agents in alignment with EU green directives, targeting growth in the construction sector, further enhancing the company’s commitment to sustainable and eco-friendly solutions

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.