Global Float Zone Silicon Market

Taille du marché en milliards USD

TCAC :

%

USD

3.84 Billion

USD

7.88 Billion

2024

2032

USD

3.84 Billion

USD

7.88 Billion

2024

2032

| 2025 –2032 | |

| USD 3.84 Billion | |

| USD 7.88 Billion | |

| % | |

|

Marché mondial du silicium à zone flottante, par taille de nœud (10 nm et moins, 12 à 22 nm et 28 nm et plus), collage de plaquettes (collage direct, collage par activation de surface, collage anodique et collage plasma), utilisateur final (télécommunications, instrumentation et recherche scientifique, santé, énergie, défense et surveillance, informatique et divertissement, industrie et automobile, vente au détail et autres) – Tendances du secteur et prévisions jusqu'en 2032.

Taille du marché du silicium de la zone flottante

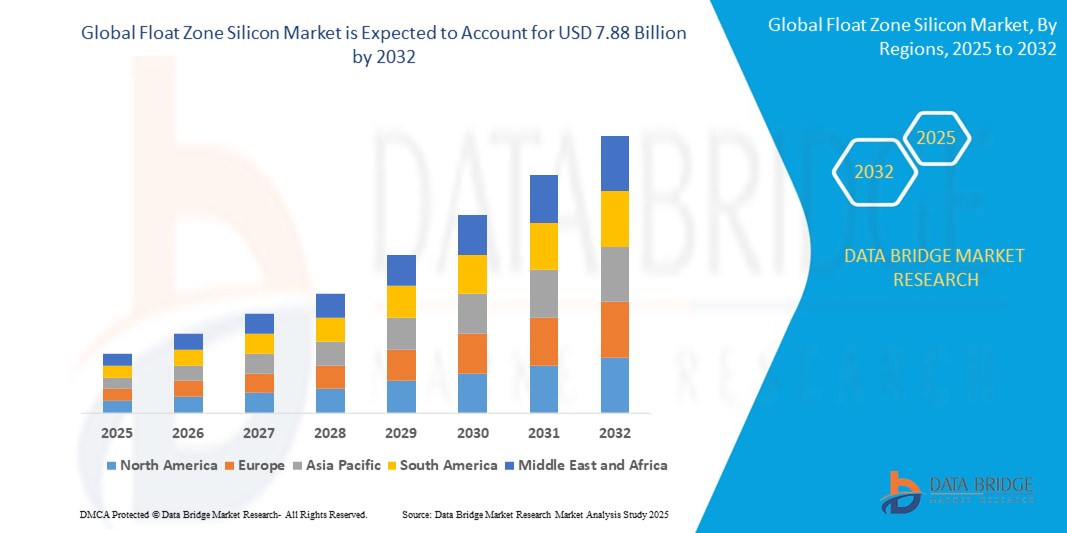

- Le marché mondial du silicium de zone flottante était évalué à 3,84 milliards de dollars en 2024 et devrait atteindre 7,88 milliards de dollars d'ici 2032 , avec un TCAC de 9,40 % au cours de la période de prévision.

- La croissance du marché est principalement tirée par la demande croissante de silicium de haute pureté pour les applications semi-conductrices avancées, notamment dans les secteurs des télécommunications, de l'informatique et de l'énergie, alimentée par les progrès technologiques et la tendance à la miniaturisation des puces.

- L'adoption croissante du silicium de zone flottante dans l'électronique haute performance, associée au besoin de techniques de collage de plaquettes efficaces et fiables, accélère l'expansion du marché, les industries privilégiant la précision et la performance des dispositifs de nouvelle génération.

Analyse du marché du silicium de Float Zone

- Le silicium de zone flottante, reconnu pour sa grande pureté et sa faible densité de défauts, est un matériau essentiel à la production de semi-conducteurs avancés, d'électronique de puissance et de dispositifs hautes performances, offrant des propriétés électriques supérieures à celles du silicium Czochralski.

- Le marché est stimulé par la demande croissante de puces miniaturisées à haut rendement pour des applications telles que les télécommunications 5G, les véhicules électriques et les systèmes d'énergies renouvelables, ainsi que par l'augmentation des investissements dans la fabrication de semi-conducteurs.

- L'Amérique du Nord a dominé le marché du silicium de zone flottante en 2024, avec une part de revenus de 42,5 %, grâce à son industrie des semi-conducteurs de pointe, à d'importants investissements en R&D et à la présence d'acteurs clés aux États-Unis, notamment dans l'innovation des plaquettes de silicium pour les technologies d'IA et de 5G.

- La région Asie-Pacifique devrait connaître la croissance la plus rapide au cours de la période de prévision, alimentée par une industrialisation rapide, l'augmentation des installations de fabrication de semi-conducteurs et la demande croissante d'électronique grand public dans des pays comme la Chine, le Japon et la Corée du Sud.

- Le segment des technologies 10 nm et inférieures a dominé la plus grande part de revenus du marché (50 %) en 2024, grâce à la demande croissante de technologies de pointe permettant une densité de transistors plus élevée et des performances améliorées pour les dispositifs électroniques avancés, notamment dans le calcul haute performance et les télécommunications.

Portée du rapport et segmentation du marché du silicium en zone flottante

|

Attributs |

Zone flottante Silicon : Principales informations sur le marché |

|

Segments couverts |

|

|

Pays couverts |

Amérique du Nord

Europe

Asie-Pacifique

Moyen-Orient et Afrique

Amérique du Sud

|

|

Acteurs clés du marché |

|

|

Opportunités de marché |

|

|

Ensembles d'informations de données à valeur ajoutée |

En plus des informations sur les scénarios de marché tels que la valeur du marché, le taux de croissance, la segmentation, la couverture géographique et les principaux acteurs, les rapports de marché élaborés par Data Bridge Market Research comprennent également une analyse approfondie d'experts, la production et la capacité par entreprise représentées géographiquement, les schémas de réseau des distributeurs et des partenaires, une analyse détaillée et mise à jour des tendances des prix et une analyse des déficits de la chaîne d'approvisionnement et de la demande. |

Tendances du marché du silicium en zone flottante

« Adoption croissante des technologies de fabrication de semi-conducteurs avancées »

- Le marché mondial du silicium de zone flottante connaît une tendance notable à l'intégration de technologies de fabrication de semi-conducteurs avancées, stimulée par la demande de plaquettes de silicium de haute pureté.

- Ces technologies, telles que l'amélioration de la purification par zone flottante et les techniques avancées de collage de plaquettes, permettent la production de plaquettes de silicium aux propriétés électriques supérieures et présentant un minimum d'impuretés, ce qui est essentiel pour les applications hautes performances.

- Les procédés de fabrication avancés, notamment pour les tailles de nœud de 10 nm et inférieures, soutiennent le développement des semi-conducteurs de nouvelle génération utilisés dans les technologies d'IA, d'IoT et de 5G.

- Par exemple, les entreprises tirent parti du collage plasma et du collage par activation de surface pour améliorer l'intégration sur plaquette des dispositifs complexes tels que les systèmes microélectromécaniques (MEMS) et les circuits haute fréquence.

- Cette tendance accroît l'attrait du silicium de zone flottante pour des secteurs tels que les télécommunications, l'informatique et l'automobile, où une efficacité et une fiabilité élevées sont primordiales.

- Les innovations dans les techniques de collage de plaquettes, telles que le collage direct, permettent la création d'interconnexions robustes et à haute densité, stimulant ainsi la croissance du marché.

Dynamique du marché du silicium en zone flottante

Conducteur

« Demande croissante de semi-conducteurs haute performance et de solutions d’énergies renouvelables »

- La demande croissante de semi-conducteurs haute performance pour des applications telles que l'infrastructure 5G, les véhicules électriques et l'électronique grand public est un facteur clé du marché mondial du silicium de zone flottante.

- La pureté et les propriétés électriques supérieures du silicium de zone flottante en font un matériau idéal pour la fabrication de puces à haut rendement, d'amplificateurs RF et de cellules solaires, favorisant ainsi le développement des objets connectés et des systèmes d'énergie renouvelable.

- Les initiatives gouvernementales promouvant les énergies propres, notamment en Amérique du Nord et en Europe, stimulent l'adoption du silicium de zone flottante dans la production de cellules solaires à haut rendement.

- La prolifération de l'Internet des objets (IoT) et le déploiement des réseaux 5G facilitent un traitement et une transmission des données plus rapides, augmentant ainsi le besoin en plaquettes de silicium avancées dans les secteurs des télécommunications et de l'informatique.

- Les principaux fabricants de semi-conducteurs intègrent de plus en plus le silicium de zone flottante dans leurs lignes de production afin de répondre aux exigences de performance rigoureuses des dispositifs modernes.

Retenue/Défi

« Coûts de production élevés et processus de fabrication complexes »

- Le coût élevé de production du silicium de zone flottante, dû au processus de purification énergivore et aux équipements spécialisés, constitue un obstacle important à son adoption par le marché, notamment dans les régions sensibles aux coûts.

- La complexité de la fabrication de plaquettes de silicium de haute pureté, notamment pour les technologies de gravure avancées telles que 10 nm et moins, exige des investissements substantiels dans la R&D et les installations de production.

- De plus, les inquiétudes concernant la stabilité de la chaîne d'approvisionnement et la disponibilité des matières premières pour la production de silicium par la méthode de la zone flottante peuvent freiner la croissance du marché.

- La complexité des techniques de collage de plaquettes, telles que le collage anodique et le collage plasma, accroît les difficultés de production et exige un contrôle précis pour obtenir des résultats fiables.

- Ces facteurs peuvent limiter l'expansion du marché dans les économies émergentes où les coûts et les limitations des infrastructures sont des facteurs importants.

Portée du marché du silicium de la zone flottante

Le marché est segmenté en fonction de la taille des nœuds, du collage des plaquettes et de l'utilisateur final.

- Par taille de nœud

Le marché mondial du silicium gravé par la méthode de la zone flottante est segmenté en fonction de la taille des nœuds : 10 nm et moins, 12 à 22 nm et 28 nm et plus. Le segment des 10 nm et moins représentait la plus grande part de marché (50 %) en 2024, grâce à la demande croissante de technologies de pointe permettant une densité de transistors plus élevée et des performances accrues pour les dispositifs électroniques avancés, notamment dans les domaines du calcul haute performance et des télécommunications.

Le segment des technologies 28 nm et supérieures devrait connaître le taux de croissance le plus rapide entre 2025 et 2032, grâce aux progrès réalisés dans les applications hautes performances et à la pertinence continue des applications existantes où la fiabilité et la compatibilité sont primordiales, comme dans les secteurs industriel et automobile.

- Par collage de plaquettes

Le marché mondial du silicium par la méthode de collage de plaquettes est segmenté en collage direct, collage par activation de surface, collage anodique et collage plasma. Le segment du collage direct devrait représenter la plus grande part de marché (40 %) en 2024, grâce à ses nombreuses applications dans la fabrication de semi-conducteurs, notamment pour la production de dispositifs électroniques avancés tels que les circuits intégrés et les systèmes microélectromécaniques (MEMS).

Le segment du collage plasma devrait connaître le taux de croissance le plus rapide entre 2025 et 2032, grâce à sa résistance de collage améliorée, son uniformité et son contrôle des paramètres de collage, ce qui le rend adapté aux applications avancées dans la fabrication de semi-conducteurs, la biotechnologie et la nanotechnologie.

- Par l'utilisateur final

Le marché mondial du silicium de zone flottante est segmenté, selon l'utilisateur final, en télécommunications, instrumentation et recherche scientifique, santé, énergie, défense et surveillance, informatique et divertissement, industrie et automobile, distribution et autres. Le segment des télécommunications a dominé le marché en 2024, représentant 35 % des revenus, grâce au déploiement de l'infrastructure 5G et à la demande de matériaux semi-conducteurs de haute qualité pour les amplificateurs RF et les circuits haute fréquence, tirant parti de la pureté et des propriétés électriques supérieures du silicium de zone flottante.

Le segment industriel et automobile devrait connaître une croissance rapide entre 2025 et 2032, portée par l'adoption croissante du silicium à zone flottante dans les véhicules électriques et l'électronique automobile pour une conversion de puissance efficace, la gestion des batteries et les puces hautes performances, ainsi que dans l'automatisation industrielle pour des solutions fiables et évolutives.

Analyse régionale du marché du silicium de Float Zone

- L'Amérique du Nord a dominé le marché du silicium de zone flottante en 2024, avec une part de revenus de 42,5 %, grâce à son industrie des semi-conducteurs de pointe, à d'importants investissements en R&D et à la présence d'acteurs clés aux États-Unis, notamment dans l'innovation des plaquettes de silicium pour les technologies d'IA et de 5G.

- Les consommateurs et les industries privilégient le silicium de zone flottante pour sa pureté et ses performances exceptionnelles dans les semi-conducteurs à haut rendement, les cellules solaires et l'électronique de puissance, en particulier dans les régions dotées d'infrastructures technologiques avancées.

- La croissance est soutenue par des innovations dans les techniques de purification, telles que le chauffage par induction avancé et le raffinage par zone, ainsi que par une adoption croissante sur les marchés des équipementiers et de l'après-vente dans divers secteurs industriels.

Analyse du marché américain du silicium flottant

Le marché américain du silicium de zone flottante a représenté la plus grande part de revenus (87,7 %) en Amérique du Nord en 2024, porté par une forte demande dans les secteurs des semi-conducteurs et de l'énergie solaire, ainsi que par une prise de conscience croissante des propriétés électriques supérieures de ce matériau. La tendance vers des générations de semi-conducteurs plus avancées et l'augmentation des investissements dans les technologies d'énergies renouvelables stimulent davantage la croissance du marché. La présence de fabricants clés tels que GlobalWafers et Siltronic, associée à des initiatives de R&D performantes, crée un écosystème de marché robuste.

Aperçu du marché européen du silicium flottant

Le marché européen du silicium de zone flottante devrait connaître une croissance significative, portée par une forte volonté d'innovation technologique et d'efficacité énergétique. Les industries recherchent du silicium de haute pureté pour les applications semi-conductrices avancées et les solutions d'énergies renouvelables, notamment pour les cellules solaires. La croissance est marquée tant dans les nouveaux procédés de fabrication que dans les applications de modernisation, avec des pays comme l'Allemagne et la France affichant une forte progression grâce à leur orientation vers les industries de haute technologie et les objectifs de développement durable.

Analyse du marché britannique du silicium flottant

Le marché britannique du silicium de zone flottante devrait connaître une croissance rapide, portée par la demande croissante d'électronique haute performance et d'applications d'énergies renouvelables en milieux urbains et industriels. La prise de conscience croissante des avantages de ce matériau en matière de réduction de la consommation d'énergie et d'amélioration des performances des dispositifs favorise son adoption. L'évolution des réglementations en faveur des technologies écoénergétiques influence les choix de l'industrie, qui doit concilier performance et conformité.

Analyse du marché du silicium de la zone flottante en Allemagne

L'Allemagne devrait connaître l'un des taux de croissance les plus rapides sur le marché du silicium de zone flottante, grâce à son secteur de fabrication de semi-conducteurs de pointe et à son engagement fort en faveur de l'efficacité énergétique. Les industries allemandes privilégient le silicium de zone flottante, technologiquement avancé, pour des applications dans le calcul haute performance et les énergies renouvelables, contribuant ainsi à réduire la consommation d'énergie. L'intégration de ces matériaux dans les solutions électroniques haut de gamme et les solutions de rechange soutient la croissance durable du marché.

Aperçu du marché du silicium flottant en Asie-Pacifique

La région Asie-Pacifique devrait connaître la croissance la plus rapide, portée par l'expansion de la production de semi-conducteurs et la hausse des investissements dans des pays comme la Chine, le Japon et la Corée du Sud. La demande croissante de silicium de haute pureté pour l'électronique, les cellules solaires et l'automobile stimule la croissance du marché. Les initiatives gouvernementales en faveur de l'efficacité énergétique et de l'adoption des technologies de pointe encouragent également l'utilisation du silicium de zone flottante.

Aperçu du marché japonais du silicium flottant

Le marché japonais du silicium de zone flottante devrait connaître une croissance rapide, portée par la forte préférence des consommateurs et des industriels pour un silicium de haute qualité et de haute pureté, qui améliore les performances des semi-conducteurs et des applications solaires. La présence de grands fabricants tels que Shin-Etsu Chemical et SUMCO, ainsi que l'intégration du silicium de zone flottante dans les produits OEM, accélèrent la pénétration du marché. L'intérêt croissant pour l'électronique de pointe et les solutions d'énergies renouvelables contribue également à cette croissance.

Aperçu du marché du silicium flottant en Chine

La Chine détient la plus grande part du marché du silicium de zone flottante en Asie-Pacifique, portée par une urbanisation rapide, une demande croissante en électronique de pointe et un fort intérêt pour les énergies renouvelables. Le développement du secteur technologique chinois et les investissements dans la fabrication de semi-conducteurs favorisent l'adoption du silicium de zone flottante. De solides capacités de production nationales et des prix compétitifs facilitent l'accès au marché et contribuent à une croissance significative.

Part de marché du silicium de Float Zone

L'industrie du silicium de zone flottante est principalement dominée par des entreprises bien établies, notamment :

- Topsil GlobalWafers A/S (Danemark)

- Sino-American Silicon Products Inc. (Taïwan)

- Shanghai Simgui Technology Co., Ltd. (Chine)

- Shin-Etsu Chemical Co., Ltd. (Japon)

- SUMCO CORPORATION (Japon)

- Siltronic AG (Allemagne)

- SK Siltron Co., Ltd. (Corée du Sud)

- Okmetic Oy (Finlande)

- Microchip Technology Inc. (États-Unis)

- JRH ELECTRONICS INC. (États-Unis)

- RS Technologies Co., Ltd. (Chine)

- Groupe technologique TCL (Chine)

- Plaquette pure (États-Unis)

- Matériaux électroniques MEMC (États-Unis)

- Société des matériaux Mitsubishi (Japon)

- Ferrotec Holdings Corporation (Japon)

Quels sont les développements récents sur le marché mondial du silicium de zone flottante ?

- En juin 2024, une étude de marché a mis en lumière la forte croissance du marché des plaquettes de silicium de zone flottante (FZ), portée par la demande croissante de substrats de haute pureté pour la fabrication de semi-conducteurs. Évalué à environ 5 milliards de dollars en 2025, ce marché devrait atteindre près de 9 milliards de dollars d'ici 2033, grâce à ses applications dans le calcul haute performance, l'électronique de puissance et les capteurs avancés. Les plaquettes FZ, reconnues pour leur pureté et leurs propriétés électriques exceptionnelles, sont de plus en plus prisées dans les secteurs exigeant précision et fiabilité, tels que l'aérospatiale, l'automobile et les énergies renouvelables.

- En mai 2024, de nouvelles données ont révélé une augmentation notable de la demande de plaquettes de silicium de zone flottante (FZ) dans le secteur de l'intégration MEMS et de capteurs, notamment pour l'électronique grand public. Cette forte croissance est alimentée par l'utilisation croissante des montres connectées, des capteurs médicaux et des dispositifs de surveillance environnementale, qui requièrent tous des substrats à haute sensibilité et à faible défaut. La pureté cristalline et les caractéristiques électriques supérieures du silicium FZ en font un matériau idéal pour améliorer la précision et la fiabilité des capteurs, en particulier dans les dispositifs compacts et performants où même des défauts mineurs peuvent impacter leur fonctionnement.

- En mars 2024, l'industrie des semi-conducteurs a poursuivi sa transition vers des plaquettes de silicium de zone flottante (FZ) de plus grand diamètre, notamment au format 300 mm, afin d'accroître l'efficacité de la production et de réduire les coûts unitaires. Cette évolution est motivée par le besoin croissant de dispositifs électroniques compacts et performants dans des secteurs tels que l'intelligence artificielle, l'électronique de puissance et les capteurs avancés. Les fabricants explorent également de nouvelles techniques de dopage et des traitements de surface innovants pour améliorer le rendement, les performances électriques et la stabilité thermique des plaquettes. Ces avancées visent à répondre aux exigences strictes de pureté et d'absence de défauts des applications de nouvelle génération, tout en favorisant la mise à l'échelle de la production en grande série.

- En janvier 2024, les données industrielles ont mis en évidence la forte demande de plaquettes de silicium de zone flottante (FZ) pour l'électronique de puissance, notamment dans les secteurs des véhicules électriques (VE) et de l'automatisation industrielle. Avec plus de 7 millions de VE utilisant des modules de puissance à base de plaquettes FZ, l'importance de ce matériau est soulignée par sa résistivité uniforme, sa tension de claquage élevée et sa faible densité de défauts – autant de caractéristiques essentielles pour les onduleurs et les modules IGBT à haut rendement. Ces propriétés permettent des performances supérieures dans des environnements à haute tension et haute température, faisant du silicium FZ une pierre angulaire de l'évolution des systèmes de mobilité et d'énergie de nouvelle génération.

- En octobre 2023, les principaux acteurs du marché des plaquettes de silicium de zone flottante (FZ), dont Shin-Etsu Chemical, SUMCO CORPORATION et Siltronic, ont intensifié leurs investissements dans la production de silicium de haute pureté et les technologies de traitement avancées des plaquettes. Ces initiatives stratégiques visent à répondre à la demande croissante de substrats ultra-purs, indispensables aux composants semi-conducteurs de nouvelle génération utilisés dans l'électronique de puissance, le calcul haute performance et les capteurs avancés. L'accent est mis sur l'augmentation de la production de plaquettes FZ de 300 mm, l'amélioration des techniques de croissance cristalline et le perfectionnement des procédés de traitement de surface afin de satisfaire aux exigences de qualité strictes des applications émergentes.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.