Global Liquid Biopsy Tests Market

Taille du marché en milliards USD

TCAC :

%

USD

673.20 Million

USD

2,347.79 Million

2025

2033

USD

673.20 Million

USD

2,347.79 Million

2025

2033

| 2026 –2033 | |

| USD 673.20 Million | |

| USD 2,347.79 Million | |

| % | |

|

Segmentation du marché mondial des tests de biopsie liquide, par type (tests de cellules tumorales circulantes (CTC), tests d'ADN tumoral circulant (ADNtc), tests basés sur les exosomes, tests basés sur les microARN et autres), application (diagnostic du cancer, suivi du traitement, dépistage précoce, évaluation pronostique et médecine personnalisée) - Tendances du secteur et prévisions jusqu'en 2033

Taille du marché des tests de biopsie liquide

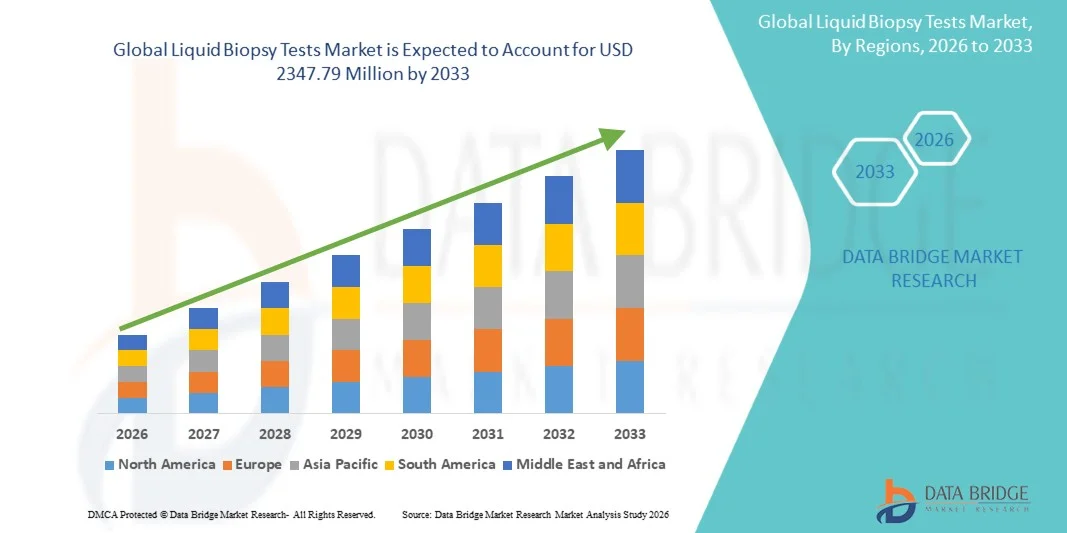

- Le marché mondial des tests de biopsie liquide était évalué à 673,2 millions de dollars américains en 2025 et devrait atteindre 2 347,79 millions de dollars américains d’ici 2033 , avec un TCAC de 16,90 % au cours de la période de prévision.

- La croissance du marché est largement alimentée par l'adoption croissante des techniques de diagnostic minimalement invasives, la prévalence croissante du cancer et la demande grandissante de médecine personnalisée et de dépistage précoce des maladies.

- De plus, la sensibilisation croissante des professionnels de la santé et des patients aux avantages des tests de biopsie liquide — tels que le suivi en temps réel de la maladie, la détection précoce des récidives tumorales et la réduction du recours aux biopsies tissulaires invasives — accélère l'adoption des solutions de biopsie liquide, stimulant ainsi considérablement la croissance du secteur.

Analyse du marché des tests de biopsie liquide

- Les tests de biopsie liquide, qui offrent des solutions de diagnostic minimalement invasives pour la détection et le suivi du cancer et d'autres maladies génétiques, sont des composantes de plus en plus essentielles des soins de santé modernes en raison de leur capacité à fournir des informations en temps réel, à permettre une détection précoce et à réduire le besoin de biopsies tissulaires traditionnelles.

- La demande croissante de tests de biopsie liquide est principalement alimentée par la prévalence accrue du cancer, l'adoption croissante de la médecine personnalisée et la sensibilisation accrue des professionnels de la santé et des patients aux avantages des outils de diagnostic non invasifs.

- L'Amérique du Nord a dominé le marché des tests de biopsie liquide en 2025, représentant 46 % des revenus. Cette domination s'explique par des infrastructures de santé avancées, une forte adoption de la médecine de précision, une activité de recherche clinique soutenue et des investissements croissants de la part des principaux acteurs du marché. Les États-Unis sont en tête de la région, avec une croissance substantielle des tests de biopsie liquide dans les centres d'oncologie, les hôpitaux et les laboratoires de diagnostic.

- La région Asie-Pacifique devrait connaître la croissance la plus rapide sur le marché des tests de biopsie liquide au cours de la période de prévision, avec un taux de croissance annuel composé (TCAC) estimé à 11 % entre 2026 et 2033. Cette croissance est portée par l'augmentation de l'incidence du cancer, l'amélioration des infrastructures de santé, la sensibilisation croissante aux diagnostics avancés et le développement de la recherche médicale dans des pays comme la Chine, l'Inde, le Japon et la Corée du Sud.

- Le segment des tests d'ADN tumoral circulant (ADNtc) a dominé le marché en 2025, représentant 45,8 % des revenus, grâce à sa haute sensibilité, son caractère non invasif et son utilité clinique avérée pour la détection de mutations exploitables en vue d'une thérapie personnalisée.

Portée du rapport et segmentation du marché des tests de biopsie liquide

|

Attributs |

Analyses clés du marché des tests de biopsie liquide |

|

Segments couverts |

|

|

Pays couverts |

Amérique du Nord

Europe

Asie-Pacifique

Moyen-Orient et Afrique

Amérique du Sud

|

|

Acteurs clés du marché |

|

|

Opportunités de marché |

|

|

Ensembles d'informations de données à valeur ajoutée |

En plus des informations sur les scénarios de marché tels que la valeur du marché, le taux de croissance, la segmentation, la couverture géographique et les principaux acteurs, les rapports de marché élaborés par Data Bridge Market Research comprennent également une analyse approfondie par des experts, l'épidémiologie des patients, l'analyse du pipeline, l'analyse des prix et le cadre réglementaire. |

Tendances du marché des tests de biopsie liquide

« Adoption croissante des techniques de diagnostic du cancer minimalement invasives »

- Une tendance clé du marché mondial des tests de biopsie liquide est l'adoption croissante de techniques de diagnostic minimalement invasives, qui permettent la détection précoce du cancer, le suivi de la maladie et l'évaluation de la réponse au traitement sans avoir recours aux biopsies tissulaires traditionnelles.

- Par exemple, en 2024, Guardant Health a lancé son test de biopsie liquide Guardant360, permettant aux cliniciens de détecter plusieurs mutations exploitables à partir d'un seul échantillon de sang, illustrant ainsi l'évolution vers des diagnostics minimalement invasifs.

- Les tests de biopsie liquide fournissent des informations moléculaires rapides et précises à partir d'un simple échantillon de sang, réduisant ainsi l'inconfort et les risques pour le patient par rapport aux biopsies chirurgicales.

- Les progrès réalisés dans le domaine du séquençage de nouvelle génération (NGS), de la PCR numérique et de la microfluidique permettent une détection très sensible et précise de l'ADN tumoral circulant (ADNtc), des exosomes et des cellules tumorales circulantes (CTC).

- Cette tendance est encore accentuée par la préférence croissante des patients pour des interventions moins invasives et des séjours hospitaliers plus courts.

- Les hôpitaux et les centres d'oncologie intègrent de plus en plus les tests de biopsie liquide à leurs protocoles standard afin de compléter les résultats d'imagerie et de biopsie tissulaire. Les entreprises pharmaceutiques exploitent les technologies de biopsie liquide dans les essais cliniques pour l'identification de biomarqueurs et le suivi thérapeutique.

- La disponibilité croissante de kits de diagnostic compagnon pour les thérapies ciblées favorise leur adoption par les cliniciens. Les économies émergentes adoptent rapidement la biopsie liquide grâce à l'expansion des centres d'oncologie et à l'amélioration des infrastructures de santé.

- Les innovations technologiques telles que les panels multigéniques et les affichages numériques améliorent la fiabilité et la rapidité des tests.

Dynamique du marché des tests de biopsie liquide

Conducteur

« Augmentation de la prévalence du cancer et nécessité d’une médecine personnalisée »

- L'augmentation de la prévalence mondiale du cancer est un facteur majeur de croissance du marché des tests de biopsie liquide, car les cliniciens ont besoin de solutions de diagnostic précises, rapides et non invasives pour le dépistage et le suivi précoces.

- Par exemple, en mars 2025, Roche a annoncé l'extension de son test de mutation EGFR Cobas, une solution de biopsie liquide permettant de sélectionner les patients pour des thérapies ciblées, illustrant ainsi la demande croissante de médecine personnalisée.

- L'adoption croissante des approches de médecine personnalisée et de précision stimule davantage la demande, car les biopsies liquides peuvent orienter le choix d'une thérapie ciblée et surveiller la réponse au traitement.

- Les entreprises pharmaceutiques utilisent de plus en plus les biopsies liquides pour le développement de médicaments axé sur les biomarqueurs, le suivi des essais cliniques et les tests compagnons, soutenant ainsi l'expansion du marché.

- Le développement des infrastructures de santé dans les marchés émergents, conjugué à un meilleur accès aux diagnostics de pointe, stimule l'adoption de ces technologies. Les initiatives gouvernementales promouvant les programmes de dépistage précoce du cancer, le soutien au remboursement et les campagnes de dépistage en oncologie renforcent la croissance du marché.

- Les progrès technologiques en matière de séquençage à haut débit, de PCR numérique et de bio-informatique améliorent la précision, la fiabilité et le délai d'obtention des résultats. La sensibilisation des cliniciens et leur préférence pour les procédures moins invasives favorisent l'adoption croissante des biopsies liquides par rapport aux biopsies traditionnelles.

- Les investissements en recherche et développement des principaux acteurs du marché dans les nouveaux panels de biopsie liquide stimulent l'innovation et l'adoption. La disponibilité de tests multiplex pour plusieurs types de cancer en un seul test accroît l'utilité clinique et la demande du marché.

- La préférence des patients pour les procédures minimalement invasives contribue à l'augmentation des taux d'adoption. Les collaborations entre les laboratoires de diagnostic, les hôpitaux et les entreprises de biotechnologie facilitent la pénétration du marché.

Retenue/Défi

« Coûts élevés et problèmes de normalisation technique »

- Le coût élevé des tests de biopsie liquide par rapport aux méthodes de diagnostic conventionnelles constitue un obstacle à leur adoption généralisée, notamment dans les régions sensibles aux prix et en développement.

- Par exemple, en 2023, une étude publiée dans The Lancet Oncology a mis en évidence que le coût moyen des panels de biopsie liquide multigéniques dépasse 1 000 USD par test, ce qui limite l’accessibilité et l’adoption par les cliniciens dans de nombreuses régions.

- De plus, le manque de standardisation dans le prélèvement, le traitement et l'interprétation des échantillons peut entraîner une variabilité des résultats, suscitant des hésitations chez les cliniciens. Les différences de sensibilité de détection et de spécificité des tests entre les différents prestataires peuvent réduire la confiance dans les résultats.

- Les obstacles réglementaires et de remboursement dans certaines régions retardent l'expansion du marché et accroissent la complexité opérationnelle pour les fabricants. La disponibilité de personnel qualifié et de laboratoires certifiés est limitée dans les économies émergentes, ce qui freine l'adoption.

- Les investissements importants nécessaires à la mise en place de plateformes de séquençage avancées dans les hôpitaux et les centres de recherche constituent un frein. Des études de validation clinique sont requises pour garantir la précision des tests et la conformité réglementaire, ce qui ralentit leur commercialisation.

- Certains patients et cliniciens restent sceptiques quant à la fiabilité des résultats de la biopsie liquide par rapport à la biopsie tissulaire, ce qui influence l'adhésion au test. Les limitations techniques dans la détection des mutations peu abondantes dans les cancers de stade précoce constituent un défi.

- Les entreprises s'attaquent à ces contraintes en proposant des solutions rentables, en améliorant la sensibilité des analyses et en fournissant une formation et un soutien aux laboratoires.

Étendue du marché des tests de biopsie liquide

Le marché est segmenté en fonction du type, de la technologie, de l'application et de l'utilisateur final.

• Par type

Le marché des tests de biopsie liquide est segmenté, selon le type de test, en tests de cellules tumorales circulantes (CTC), tests d'ADN tumoral circulant (ADNtc), tests basés sur les exosomes, tests basés sur les microARN et autres. Le segment des tests d'ADN tumoral circulant (ADNtc) a représenté la plus grande part de marché (45,8 %) en 2025, grâce à sa haute sensibilité, son caractère non invasif et son utilité clinique avérée pour la détection de mutations exploitables en vue d'une thérapie personnalisée. Les tests d'ADNtc sont largement utilisés en oncologie pour le choix du traitement, le suivi de la maladie et la détection des récidives. Ce segment bénéficie d'une large adoption dans les laboratoires hospitaliers et les centres de diagnostic privés grâce à la fiabilité des résultats, la large couverture des cancers et l'intégration aux plateformes de séquençage de nouvelle génération (SNG). Les cliniciens privilégient souvent l'ADNtc pour le suivi de la réponse au traitement et de la maladie résiduelle minimale (MRD). Les progrès technologiques constants en matière de sensibilité des tests, de détection multiplex et de bio-informatique renforcent la position de leader des tests d'ADNtc sur le marché. La prévalence croissante du cancer à l'échelle mondiale et la demande accrue de médecine de précision soutiennent la croissance de ce segment. Les acteurs du marché proposent de plus en plus de panels d'ADN tumoral circulant (ADNtc) à un coût avantageux, élargissant ainsi l'accès à ces tests dans les pays développés et émergents. Les collaborations stratégiques entre les entreprises de diagnostic et les centres d'oncologie favorisent une adoption rapide. Par ailleurs, la disponibilité de tests ADNtc approuvés par la FDA a renforcé la confiance des cliniciens. La sensibilisation croissante des patients et des professionnels de santé aux options minimalement invasives stimule également leur adoption. En définitive, les tests ADNtc sont considérés comme la référence en matière de profilage moléculaire par biopsie liquide, conservant leur position dominante en termes de revenus et de choix clinique.

Le segment des tests de cellules tumorales circulantes (CTC) devrait connaître le taux de croissance annuel composé (TCAC) le plus rapide, à 22,4 %, entre 2026 et 2033, grâce à leur utilisation croissante dans la détection précoce des cancers, le pronostic et le suivi des métastases. Les tests CTC permettent un suivi en temps réel de la dynamique tumorale et fournissent des informations sur l'hétérogénéité tumorale, ce qui les rend particulièrement précieux pour la planification de thérapies personnalisées. L'intensification de la recherche clinique sur de nouvelles méthodes d'enrichissement et de détection des CTC favorise leur adoption. La sensibilisation croissante des patients et des oncologues aux diagnostics non invasifs accélère la demande. Les technologies CTC sont intégrées aux essais cliniques pour surveiller l'efficacité thérapeutique et les mécanismes de résistance. Les applications émergentes dans le suivi de la réponse à l'immunothérapie stimulent davantage la croissance du marché. Les partenariats stratégiques et les investissements en R&D permettent le développement de plateformes CTC innovantes, plus sensibles et nécessitant des volumes d'échantillons plus faibles. L'expansion des laboratoires de diagnostic spécialisés en oncologie en Amérique du Nord, en Europe et en Asie-Pacifique contribue à une pénétration rapide du marché. Les initiatives gouvernementales et le soutien au remboursement dans certaines régions encouragent une adoption plus large. L'amélioration continue de la précision, de la reproductibilité et du rapport coût-efficacité des tests garantit leur large adoption par les cliniciens. Les tests CTC complètent les analyses d'ADN tumoral circulant (ADNtc), créant ainsi une approche synergique en diagnostic par biopsie liquide. La croissance de ce marché est soutenue par le développement des programmes de dépistage en oncologie et les collaborations de recherche entre les milieux universitaires. De manière générale, les tests CTC devraient connaître la croissance de revenus la plus rapide grâce à leur pertinence clinique croissante et aux progrès technologiques.

• Sur demande

Selon l'application, le marché des tests de biopsie liquide est segmenté en diagnostic du cancer, suivi du traitement, dépistage précoce, évaluation pronostique et médecine personnalisée. Le segment du diagnostic du cancer représentait la plus grande part de marché (42,6 %) en 2025, sous l'effet de l'augmentation de la prévalence mondiale du cancer et du besoin urgent d'outils de diagnostic précis et peu invasifs. Les cliniciens s'appuient de plus en plus sur les tests de biopsie liquide pour détecter les mutations exploitables, suivre l'évolution de la maladie et compléter les résultats des biopsies tissulaires. L'adoption des tests d'ADN tumoral circulant (ADNtc) et de cellules tumorales circulantes (CTC) pour diverses tumeurs solides, notamment les cancers du poumon, colorectal, du sein et de la prostate, renforce la position de leader de ce segment sur le marché. Ce dernier bénéficie des avancées technologiques, telles que les panels multiplex et le séquençage à haut débit, qui permettent la détection simultanée de plusieurs biomarqueurs. La multiplication des collaborations entre les hôpitaux, les centres de recherche et les entreprises de diagnostic favorise une adoption généralisée. La préférence des patients pour des procédures moins invasives stimule davantage la demande. Les initiatives gouvernementales et des ONG en faveur du dépistage précoce du cancer créent un environnement de marché favorable. L'augmentation des investissements en recherche et développement en oncologie, conjuguée au développement des infrastructures de santé dans les économies émergentes, stimule davantage la croissance. Dans les régions développées, les applications de diagnostic du cancer sont privilégiées en raison du soutien au remboursement et de leur adoption clinique. Les publications scientifiques et les recommandations cliniques préconisent de plus en plus la biopsie liquide pour le diagnostic, renforçant ainsi sa crédibilité. Globalement, ce segment conserve sa position dominante grâce à son importance clinique cruciale, à son adoption technologique et à sa large applicabilité à différents types de cancers.

Le segment du suivi thérapeutique devrait connaître le taux de croissance annuel composé (TCAC) le plus rapide, à 23,1 %, entre 2026 et 2033, porté par le besoin croissant d'évaluation en temps réel de l'efficacité thérapeutique et de détection précoce de la résistance aux médicaments. Les tests de biopsie liquide permettent aux cliniciens de suivre la dynamique tumorale de manière non invasive, autorisant ainsi des ajustements thérapeutiques sans biopsies tissulaires répétées. L'utilisation croissante des thérapies ciblées et des immunothérapies exige un suivi continu, stimulant la demande. Les progrès technologiques en matière de quantification de l'ADN tumoral circulant (ADNtc) et de caractérisation des cellules tumorales circulantes (CTC) améliorent la précision et la fiabilité. Les entreprises pharmaceutiques intègrent de plus en plus la biopsie liquide dans les essais cliniques pour le suivi des résultats des traitements. L'expansion des laboratoires de diagnostic moléculaire hospitaliers en Amérique du Nord, en Europe et en Asie-Pacifique accélère l'adoption de cette technologie. La sensibilisation croissante des patients aux avantages des traitements personnalisés contribue à la croissance du marché. Le renforcement des collaborations entre les entreprises de biotechnologie et les centres d'oncologie favorise l'innovation dans les tests de suivi. Les économies émergentes adoptent le suivi thérapeutique afin d'optimiser leurs ressources de santé limitées. L'amélioration des politiques de remboursement dans les régions développées encourage une utilisation clinique plus large. La recherche continue sur les biomarqueurs prédictifs renforce la crédibilité du segment. Globalement, les applications de suivi des traitements connaissent la croissance la plus rapide en raison des besoins cliniques, des progrès technologiques et de l'évolution vers des soins oncologiques personnalisés.

Analyse régionale du marché des tests de biopsie liquide

- L'Amérique du Nord a dominé le marché des tests de biopsie liquide avec la plus grande part de revenus, soit 46 %, en 2025.

- Soutenu par une infrastructure de soins de santé de pointe

- Forte adoption de la médecine de précision, activité de recherche clinique soutenue et investissements croissants des principaux acteurs du marché

Aperçu du marché américain des tests de biopsie liquide

Le marché américain des tests de biopsie liquide a généré la plus grande part de revenus en Amérique du Nord en 2025, grâce à une forte croissance de ces tests dans les centres d'oncologie, les hôpitaux et les laboratoires de diagnostic. Cette expansion est alimentée par les progrès technologiques dans la détection de l'ADN tumoral circulant (ADNtc) et des cellules tumorales circulantes (CTC), ainsi que par l'utilisation croissante de ces tests pour le dépistage précoce du cancer, le suivi de la réponse au traitement et l'évaluation de la maladie résiduelle minimale. Le cadre réglementaire favorable du pays, l'augmentation des investissements dans la médecine de précision et le développement des collaborations entre les entreprises de diagnostic et les institutions de recherche contribuent également à cette croissance.

Analyse du marché européen des tests de biopsie liquide

Le marché européen des tests de biopsie liquide devrait connaître une croissance annuelle composée (TCAC) importante au cours de la période de prévision, portée par la prévalence croissante du cancer, l'adoption de la médecine de précision et des politiques de santé publique favorisant le diagnostic précoce. Les collaborations entre les entreprises de diagnostic et les instituts de recherche, ainsi que le développement des laboratoires cliniques proposant des solutions de tests moléculaires avancées, contribuent également à cette croissance.

Analyse du marché britannique des tests de biopsie liquide

Le marché britannique des tests de biopsie liquide devrait connaître une croissance annuelle composée remarquable, portée par l'augmentation de l'incidence du cancer, l'adoption croissante des méthodes de diagnostic non invasives et l'accroissement des investissements dans la recherche clinique. La solidité du système de santé britannique et l'accent mis sur le dépistage précoce et les traitements personnalisés continuent de favoriser le développement des technologies de biopsie liquide.

Analyse du marché allemand des tests de biopsie liquide

Le marché allemand des tests de biopsie liquide devrait connaître une croissance soutenue, grâce à un système de santé performant, une activité de recherche clinique intense et l'adoption croissante de plateformes de diagnostic moléculaire avancées. La demande croissante de diagnostics du cancer peu invasifs et de suivi en temps réel de l'évolution de la maladie contribue également à cette croissance.

Aperçu du marché des tests de biopsie liquide en Asie-Pacifique

Le marché des tests de biopsie liquide en Asie-Pacifique devrait connaître la croissance la plus rapide au cours de la période de prévision, avec un taux de croissance annuel composé (TCAC) projeté de 11 % entre 2026 et 2033. Cette croissance est alimentée par l'augmentation de l'incidence du cancer, l'amélioration des infrastructures de santé, la sensibilisation croissante aux diagnostics avancés et le développement de la recherche médicale dans des pays comme la Chine, l'Inde, le Japon et la Corée du Sud. Les initiatives gouvernementales en faveur de la médecine de précision, l'adoption croissante des plateformes de séquençage de nouvelle génération (SNG) et l'expansion des centres de diagnostic en oncologie constituent des facteurs clés de cette croissance.

Analyse du marché japonais des tests de biopsie liquide

Le marché japonais des tests de biopsie liquide connaît une forte croissance, portée par la prévalence élevée du cancer, un système de santé technologiquement avancé et le recours croissant aux tests de diagnostic non invasifs. Les investissements continus en R&D et l'adoption d'outils de diagnostic moléculaire de pointe soutiennent davantage cette croissance, notamment dans les domaines de l'oncologie et de la médecine personnalisée.

Analyse du marché chinois des tests de biopsie liquide

En 2025, le marché chinois des tests de biopsie liquide représentait la plus grande part de revenus en Asie-Pacifique, porté par la hausse de la prévalence du cancer, le développement des infrastructures de santé, les initiatives gouvernementales favorisant le dépistage précoce et l'adoption croissante des technologies de diagnostic moléculaire. La présence d'entreprises de diagnostic locales proposant des solutions économiques et les progrès technologiques rapides des plateformes de biopsie liquide sont des facteurs clés de cette expansion.

Part de marché des tests de biopsie liquide

Le secteur des tests de biopsie liquide est principalement dominé par des entreprises bien établies, notamment :

- Guardant Health (États-Unis)

- Roche (Suisse)

- Illumina (États-Unis)

- Exact Sciences (États-Unis)

- Thermo Fisher Scientific (États-Unis)

- Médecine de base (États-Unis)

- Sysmex Corporation (Japon)

- Natera (États-Unis)

- F. Hoffmann-La Roche (Suisse)

- Sophia Genetics (Suisse)

- Cancer Genetics, Inc. (États-Unis)

- Singlera Genomics (Chine)

- Diagnostic génomique personnel (États-Unis)

- Freenome (États-Unis)

- ArcherDX (États-Unis)

- Chronix Biomedical (Allemagne)

- Guardant Health (États-Unis)

- Laboratoires Bio-Rad (États-Unis)

- Burning Rock Biotech (Chine)

Dernières évolutions du marché mondial des tests de biopsie liquide

- En juillet 2024, Guardant Health, Inc. a annoncé le lancement d'une mise à jour majeure de son test de biopsie liquide Guardant360, leader sur le marché, avec un panel élargi de 739 gènes permettant une évaluation plus large des biomarqueurs et une sensibilité améliorée pour la caractérisation avancée du cancer, renforçant ainsi sa position dans le diagnostic de précision en oncologie.

- En octobre 2024, Guardant Health a obtenu l'approbation de la FDA américaine pour son test de biopsie liquide Guardant360 CDx en tant que test compagnon pour l'identification des mutations de l'EGFR dans le cancer du poumon non à petites cellules (CPNPC), ce qui constitue l'une des premières approbations de la FDA pour un test compagnon de biopsie liquide basé sur le séquençage de nouvelle génération (NGS) dans une indication de tumeur solide.

- En mai 2024, Mercy BioAnalytics, Inc. a reçu la désignation de dispositif révolutionnaire de la FDA américaine pour son test de dépistage du cancer de l'ovaire Mercy Halo — une biopsie liquide à base de vésicules extracellulaires conçue pour la détection précoce du cancer chez les femmes ménopausées asymptomatiques — soulignant le soutien réglementaire aux diagnostics non invasifs innovants.

- En août 2024, Labcorp a annoncé avoir reçu l'autorisation de mise sur le marché De Novo de la FDA américaine pour PGDx elio plasma focus Dx, le premier test de biopsie liquide en kit autorisé par la FDA pour les tumeurs solides, permettant aux cliniciens d'identifier les patients éligibles à une thérapie ciblée pour de nombreux types de cancer.

- En mars 2025, Belay Diagnostics s'est associé à GenomOncology pour intégrer GO Pathology Workbench à son test d'analyse de biopsie liquide « Summit », optimisant ainsi les flux de travail d'interprétation des variants et facilitant le traitement à haut débit des échantillons pour la prise de décision clinique en cancérologie.

- En mai 2025, le National Health Service (NHS) d'Angleterre a déployé un test novateur d'ADN tumoral circulant (ADNtc) basé sur la biopsie liquide comme outil de diagnostic de première intention pour les patients suspectés de cancer du poumon et du sein avancé, fournissant un profilage génomique non invasif pour guider une thérapie personnalisée et réduire le besoin de biopsies tissulaires invasives.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.