Global Truck As A Service Market

Taille du marché en milliards USD

TCAC :

%

USD

41.52 Billion

USD

237.37 Billion

2025

2033

USD

41.52 Billion

USD

237.37 Billion

2025

2033

| 2026 –2033 | |

| USD 41.52 Billion | |

| USD 237.37 Billion | |

| % | |

|

Segmentation du marché mondial du camionnage en tant que service (Tax-as-a-Service), par service (abonnement et paiement à l'usage, location longue durée et gestion de flotte, capacité de fret en tant que service (FaaS), flottes dédiées de poids lourds (HDT) et autres services), par type de camion (poids lourds (HDT), camions moyens (MDT) et camions légers (LDT)), par motorisation (moteur à combustion interne (ICE), véhicule électrique à batterie (BEV), véhicule hybride et véhicule électrique à pile à combustible (FCEV)), par utilisateur final (logistique et transport, commerce de détail et e-commerce, industrie et fabrication, construction et exploitation minière, et autres utilisateurs finaux) - Tendances du secteur et prévisions jusqu'en 2033

Taille du marché du camionnage en tant que service

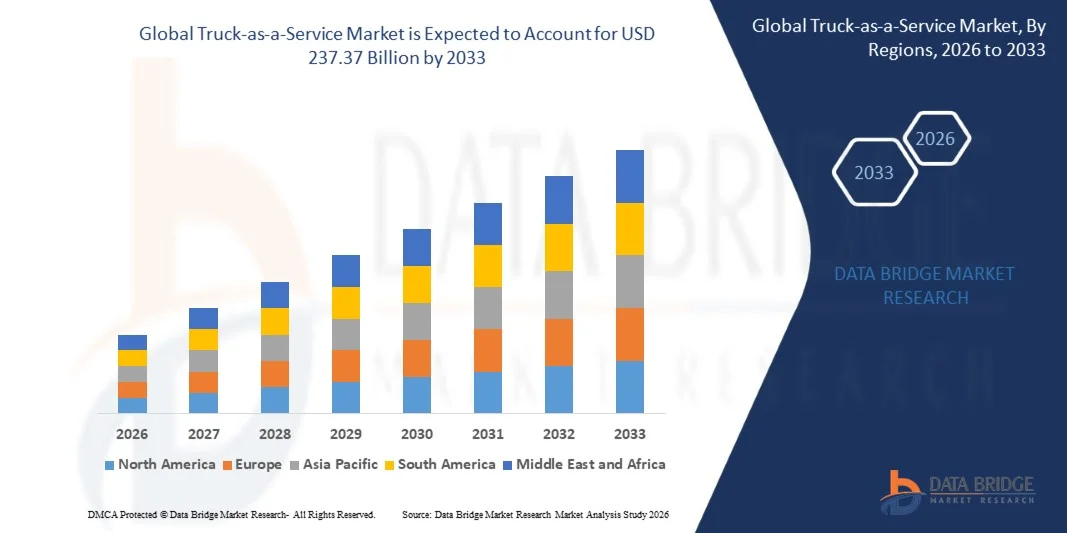

- Le marché mondial du camionnage en tant que service (TaaS) était évalué à 41,52 milliards de dollars américains en 2025 et devrait atteindre 237,37 milliards de dollars américains d'ici 2033 , avec un taux de croissance annuel composé (TCAC) de 24,35 % au cours de la période de prévision.

- La croissance du marché est largement alimentée par l'adoption croissante de modèles logistiques à faible intensité capitalistique et par le besoin accru d'optimisation des coûts dans les opérations de fret et de transport, incitant les gestionnaires de flottes à s'éloigner de la propriété traditionnelle des camions.

- De plus, la demande croissante de solutions de transport routier flexibles, évolutives et basées sur la technologie, conjuguée aux progrès réalisés dans les domaines de la télématique, des plateformes de gestion de flotte et des modèles de mobilité axés sur les services, accélère l'adoption des offres de camionnage en tant que service (Tax-as-a-Service) et soutient l'expansion globale du marché.

Analyse du marché du camionnage en tant que service

- Le modèle « Truck-as-a-Service » (camion en tant que service), qui propose un accès groupé aux véhicules, à la maintenance, à la conformité et à la gestion numérique de flotte, devient une solution essentielle pour les acteurs de la logistique, du commerce de détail et de l'industrie en quête d'efficacité opérationnelle et de réduction des dépenses d'investissement.

- L'adoption croissante des modèles de transport par abonnement et à la carte, ainsi que la pression grandissante pour améliorer l'utilisation des flottes et gérer la demande fluctuante de fret, stimulent considérablement la croissance du marché du camionnage en tant que service (Truck-as-a-Service).

- L'Europe a dominé le marché du camionnage en tant que service (TaaS) avec une part de 35 % en 2025, grâce à une forte adoption des modèles de transport à faible intensité capitalistique, à des réglementations strictes en matière d'émissions et à la transition rapide vers des solutions de mobilité durables et partagées.

- La région Asie-Pacifique devrait connaître la croissance la plus rapide sur le marché du camionnage en tant que service (TaaS) au cours de la période de prévision, en raison de l'urbanisation rapide, de l'expansion du commerce électronique et de la demande croissante de solutions logistiques évolutives.

- Le segment de l'abonnement et du paiement à l'usage pour véhicules a dominé le marché en 2025 avec une part de 32,6 %, grâce à sa grande flexibilité et à sa rentabilité pour les gestionnaires de flottes confrontés à une demande de fret fluctuante. Ce modèle permet aux entreprises d'accéder à des camions sans engagement de propriété à long terme, réduisant ainsi les investissements initiaux et améliorant la gestion de leur trésorerie. Son adoption massive par les petites et moyennes entreprises de logistique, ainsi que l'acceptation croissante de la tarification à l'usage, ont conforté sa position de leader sur le marché.

Portée du rapport et segmentation du marché du camionnage en tant que service

|

Attributs |

Principaux enseignements du marché du camionnage en tant que service |

|

Segments couverts |

|

|

Pays couverts |

Amérique du Nord

Europe

Asie-Pacifique

Moyen-Orient et Afrique

Amérique du Sud

|

|

Acteurs clés du marché |

|

|

Opportunités de marché |

|

|

Ensembles d'informations de données à valeur ajoutée |

En plus des informations sur le marché telles que la valeur du marché, le taux de croissance, les segments de marché, la couverture géographique, les acteurs du marché et le scénario du marché, le rapport de marché élaboré par l'équipe de Data Bridge Market Research comprend une analyse approfondie d'experts, une analyse des importations/exportations, une analyse des prix, une analyse de la consommation de production et une analyse PESTEL. |

Tendances du marché du camionnage en tant que service

« Transition vers des modèles de transport routier à faible intensité capitalistique et basés sur l’abonnement »

- Une tendance majeure du marché du Truck-as-a-Service est le passage croissant à des modèles de transport routier allégés en actifs et basés sur l'abonnement, impulsé par les gestionnaires de flottes cherchant à réduire leurs dépenses d'investissement et à améliorer leur flexibilité financière. Les entreprises délaissent de plus en plus la propriété directe des camions au profit d'un accès à des véhicules via un service incluant la maintenance, l'assurance et des outils numériques de gestion de flotte.

- Par exemple, Volvo Trucks a étendu son offre Volvo on Demand afin de proposer aux flottes un accès flexible aux camions, sans engagement de propriété à long terme. Ces modèles permettent aux opérateurs logistiques de gérer les fluctuations des volumes de fret tout en maintenant des coûts d'exploitation prévisibles.

- La demande de transport routier par abonnement est en hausse dans les secteurs de la logistique régionale et du dernier kilomètre, où la variabilité saisonnière de la demande exige des solutions de flotte modulables. Cette tendance favorise une meilleure utilisation des flottes et réduit les risques liés à l'inactivité des véhicules pour les transporteurs.

- Les plateformes numériques permettant de connaître en temps réel la disponibilité des véhicules, leur utilisation et la transparence des coûts renforcent l'attrait des modèles de camionnage à la demande. Ces technologies améliorent la visibilité opérationnelle et facilitent la prise de décision fondée sur les données.

- Les objectifs de développement durable influencent également cette tendance, car les modèles de services simplifient l'accès aux camions électriques et à faibles émissions sans investissement initial important. Cela encourage une adoption plus rapide des flottes plus propres.

- Globalement, la transition vers un transport routier à faible intensité capitalistique remodèle les structures de propriété des flottes et accélère l'adoption du modèle « Truck-as-a-Service » comme stratégie logistique fondamentale.

Dynamique du marché du camionnage en tant que service

Conducteur

« Demande croissante d’opérations de flotte rentables et flexibles »

- Le besoin croissant d'opérations de flotte rentables et flexibles est un moteur essentiel du marché du Truck-as-a-Service (Tax-as-a-Service). Les entreprises de logistique et de transport sont confrontées à la hausse des coûts du carburant, des dépenses d'entretien et des exigences de conformité réglementaire, ce qui rend les modèles de propriété traditionnels moins attractifs.

- Par exemple, les grands prestataires logistiques adoptent des solutions de location et de gestion de flotte complètes proposées par des entreprises comme Daimler Truck afin de stabiliser leurs coûts d'exploitation et d'améliorer la disponibilité de leurs véhicules. Ces services réduisent l'incertitude financière et la charge opérationnelle.

- La croissance du commerce électronique et des modèles de livraison à flux tendu exige des flottes capables de s'adapter rapidement aux fluctuations de la demande. Le Truck-as-a-Service permet aux entreprises d'augmenter ou de réduire leur capacité sans engagement financier à long terme.

- Les exploitants de flottes privilégient également l'efficacité opérationnelle, la maintenance prédictive et l'optimisation des itinéraires, des éléments de plus en plus intégrés aux modèles de transport routier axés sur les services. Cela améliore la productivité et réduit les temps d'arrêt.

- Le besoin de dépenses mensuelles prévisibles et d'une meilleure gestion des flux de trésorerie continue de renforcer la demande pour les offres de camionnage à la demande, faisant de la flexibilité et de la maîtrise des coûts les principaux moteurs de croissance.

Retenue/Défi

« Complexité élevée de l’intégration des flottes et de la standardisation des services »

- Le marché du Truck-as-a-Service est confronté à des défis liés à la complexité de l'intégration des véhicules, de la télématique, des services de maintenance et des plateformes numériques dans un modèle opérationnel unifié. La gestion de multiples composantes de service au sein de flottes hétérogènes accroît la difficulté de mise en œuvre pour les fournisseurs et les utilisateurs.

- Par exemple, l'intégration de systèmes télématiques tiers, d'infrastructures de recharge et de logiciels de gestion de flotte au sein de flottes de camions mixtes exige une coordination et une harmonisation technique importantes. Ces difficultés peuvent ralentir l'adoption et allonger les délais de déploiement.

- Les différences de réglementation, d'attentes en matière de services et de pratiques opérationnelles entre les régions compliquent davantage les efforts de normalisation. Les fournisseurs doivent adapter leurs offres, ce qui accroît la complexité opérationnelle.

- Garantir une qualité de service constante pour des flottes importantes et géographiquement dispersées demeure un défi pour les fournisseurs de services de transport routier. La variabilité des réseaux de maintenance et la disponibilité des infrastructures peuvent impacter la fiabilité.

- Ces défis en matière d'intégration et de normalisation incitent les fournisseurs de services à investir dans des plateformes interopérables et des cadres de services évolutifs afin de soutenir une croissance durable du marché.

Étendue du marché du camionnage en tant que service

Le marché est segmenté en fonction du service, du type de camion, de la propulsion et de l'utilisateur final.

- Par service

Le marché du Truck-as-a-Service (Tax-as-a-Service) se segmente, selon le type de service, en abonnement de véhicules et paiement à l'usage, location longue durée et gestion de flotte, capacité de fret à la demande (FaaS), flottes dédiées de poids lourds et autres services. En 2025, le segment de l'abonnement de véhicules et du paiement à l'usage dominait le marché avec une part de 32,6 %, grâce à sa grande flexibilité et à sa rentabilité pour les gestionnaires de flottes confrontés à une demande de fret fluctuante. Ce modèle permet aux entreprises d'accéder à des camions sans engagement de propriété à long terme, réduisant ainsi les investissements initiaux et améliorant la gestion de leur trésorerie. L'adoption rapide par les petites et moyennes entreprises de logistique, ainsi que l'acceptation croissante de la tarification à l'usage, ont conforté la position de leader de ce segment sur le marché.

Le segment de la location et de la gestion de flottes avec services complets devrait connaître la croissance la plus rapide entre 2026 et 2033, portée par la demande croissante de solutions de gestion de flottes intégrées et complètes. Les entreprises privilégient de plus en plus l'externalisation de la maintenance, de la conformité, de la télématique et de la gestion du cycle de vie des véhicules afin d'améliorer leur efficacité opérationnelle et la disponibilité de leurs flottes. La complexité croissante des opérations de flotte et le besoin de maîtriser les coûts d'exploitation accélèrent l'adoption des modèles de services complets par les grandes entreprises de logistique et les industriels.

- Par type de camion

Le marché est segmenté selon le type de camion : poids lourds (PL), poids moyens (PM) et poids légers (PL). Le segment des poids lourds a généré la plus grande part de revenus en 2025, grâce à son utilisation intensive dans le transport de marchandises longue distance, la logistique interurbaine et le transport industriel. Les PL sont privilégiés pour leur capacité de charge utile élevée et leur robustesse, ce qui les rend indispensables aux grands réseaux logistiques. Les modèles de camions à la demande (TaaS) permettent aux opérateurs de déployer des PL sans investissement initial important, optimisant ainsi leur rentabilité. La forte demande liée au commerce transfrontalier et au transport de marchandises, dépendant des infrastructures, soutient leur position dominante. Les gestionnaires de flottes bénéficient également d'une maintenance intégrée et d'une garantie de disponibilité pour les PL.

Le segment des camions moyens devrait connaître la croissance la plus rapide au cours de la période de prévision, portée par l'expansion des réseaux de distribution urbains et régionaux. Les camions moyens sont de plus en plus utilisés pour la logistique du dernier kilomètre et du moyen kilomètre grâce à leur équilibre entre capacité de charge utile et maniabilité. La croissance rapide des plateformes logistiques régionales pour le commerce électronique favorise l'adoption de modèles de services basés sur les camions moyens. Les entreprises privilégient les abonnements aux camions moyens pour pallier les contraintes de livraison en milieu urbain et optimiser leurs coûts. La demande croissante de flottes de livraison flexibles dans les villes de taille moyenne et les petites villes contribue également à accélérer cette croissance.

- Par propulsion

Le marché du Truck-as-a-Service (Tax-as-a-Service) est segmenté, selon le type de propulsion, en véhicules à moteur thermique (ICE), véhicules électriques à batterie (BEV), véhicules hybrides et véhicules électriques à pile à combustible (FCEV). Le segment des ICE dominait le marché en 2025, grâce à son infrastructure de ravitaillement bien établie et à sa large familiarité avec les flottes de véhicules. Les camions ICE restent la solution privilégiée pour le transport de marchandises longue distance et le transport de charges lourdes, notamment lorsque l'infrastructure de recharge est limitée. Leurs coûts d'acquisition réduits et leur fiabilité éprouvée contribuent à leur adoption continue. De nombreux gestionnaires de flottes s'appuient sur des modèles de service basés sur les ICE pour garantir la continuité de leurs opérations dans différentes zones géographiques. La disponibilité de réseaux de maintenance qualifiés renforce encore leur position dominante.

Le segment des véhicules électriques à batterie (VEB) devrait connaître la croissance la plus rapide entre 2026 et 2033, sous l'effet du durcissement des réglementations sur les émissions et de la hausse des prix des carburants. Les offres de camions à la demande (TaaS) basées sur les VEB permettent aux entreprises d'opérer une transition vers un développement durable sans investissements initiaux importants. Les incitations gouvernementales et les objectifs de décarbonation des entreprises accélèrent l'adoption des VEB dans la logistique urbaine et régionale. La réduction des coûts d'exploitation et de maintenance renforce les avantages économiques à long terme. Le développement des infrastructures de recharge et les progrès en matière d'autonomie des batteries contribuent également à cette croissance rapide.

- Par l'utilisateur final

En fonction de l'utilisateur final, le marché est segmenté en logistique et transport, distribution et e-commerce, industrie et production, construction et exploitation minière, et autres utilisateurs finaux. Le segment de la logistique et du transport détenait la plus grande part de chiffre d'affaires en 2025, porté par des exigences élevées en matière d'utilisation des flottes et la demande de solutions de transport de marchandises économiques. Les entreprises de logistique adoptent de plus en plus le modèle « Truck-as-a-Service » (TaaS) pour améliorer leur capacité d'adaptation et réduire les temps d'arrêt. L'externalisation des flottes permet aux opérateurs de mieux gérer les pics de demande et la variabilité des itinéraires. L'intégration de la télématique et des outils d'optimisation des itinéraires renforce encore l'efficacité opérationnelle. La croissance continue du fret national et international consolide la position dominante de ce segment.

Le secteur du commerce de détail et du e-commerce devrait connaître la croissance la plus rapide au cours de la période prévisionnelle, portée par l'essor fulgurant des achats en ligne et des modèles de distribution omnicanaux. Les acteurs du e-commerce s'appuient sur des solutions de transport routier flexibles pour gérer la livraison du dernier kilomètre et la logistique inverse. Le modèle « Truck-as-a-Service » permet aux détaillants d'adapter leurs flottes lors des périodes promotionnelles sans engagement de propriété à long terme. La demande croissante de délais de livraison plus courts accélère l'adoption de ce modèle. L'essor des centres de distribution urbains renforce encore ces perspectives de forte croissance.

Analyse régionale du marché du camionnage en tant que service

- L'Europe a dominé le marché du camionnage en tant que service (TaaS) avec la plus grande part de revenus (35 %) en 2025, grâce à une forte adoption des modèles de transport à faible intensité capitalistique, à des réglementations strictes en matière d'émissions et à la transition rapide vers des solutions de mobilité durables et partagées.

- Les gestionnaires de flottes de la région privilégient de plus en plus le modèle « Truck-as-a-Service » pour réduire leurs dépenses d'investissement, garantir la conformité réglementaire et accélérer la transition vers des camions à faibles émissions et électriques.

- Cette domination est renforcée par des réseaux logistiques transfrontaliers bien développés, une forte pénétration des services de location de flottes et l'adoption de solutions télématiques et de gestion de flottes avancées, positionnant l'Europe comme un marché mature et axé sur l'innovation.

Analyse du marché allemand du camionnage en tant que service

En 2025, le marché allemand du Truck-as-a-Service (Tax-as-a-Service) représentait la plus grande part de marché en Europe, grâce à la solidité de son tissu industriel et à son leadership en matière de logistique et d'innovation automobile. Les gestionnaires de flottes allemands privilégient l'efficacité opérationnelle, la maintenance prédictive et le développement durable, ce qui stimule la demande de solutions de location longue durée et de gestion de flottes. La présence d'importantes plateformes logistiques et la volonté de réduire les émissions de carbone contribuent également à l'expansion du marché.

Analyse du marché britannique du camionnage en tant que service

Le marché britannique du camionnage à la demande devrait connaître une croissance annuelle composée stable au cours de la période de prévision, portée par la demande croissante de solutions de transport de marchandises flexibles et l'adoption grandissante des modèles de transport routier à la demande et par abonnement. L'essor du commerce électronique et des réseaux de livraison urbains incite les entreprises à éviter la possession d'une flotte de véhicules sur le long terme. Les pressions réglementaires visant à réduire les émissions et la congestion favorisent également le développement du camionnage à la demande.

Analyse du marché nord-américain du camionnage en tant que service

Le marché nord-américain du transport routier à la demande (Truck-as-a-Service) détient une part de marché importante, soutenue par des volumes de fret élevés, une forte demande en transport longue distance et une adoption généralisée des modèles d'externalisation de flottes. Les prestataires logistiques de la région tirent parti du transport routier à la demande pour maîtriser leurs coûts d'exploitation et optimiser l'utilisation de leurs flottes. Une infrastructure numérique performante et des outils d'analyse de données de pointe contribuent également à la croissance du marché.

Analyse du marché du camionnage en tant que service en Asie-Pacifique

Le marché du transport routier à la demande en Asie-Pacifique devrait connaître le taux de croissance annuel composé le plus rapide entre 2026 et 2033, porté par l'urbanisation rapide, l'essor du commerce électronique et la demande croissante de solutions logistiques évolutives. Les entreprises des économies émergentes adoptent le transport routier à la demande pour éviter les coûts initiaux élevés liés à l'acquisition de véhicules. Les investissements publics dans les infrastructures logistiques et la mobilité intelligente accélèrent la croissance régionale.

Analyse du marché chinois du camionnage en tant que service

En 2025, la Chine dominait le marché du Truck-as-a-Service (TaaS) en Asie-Pacifique, grâce à son vaste réseau logistique, son important secteur manufacturier et l'adoption rapide des plateformes numériques de fret. La tendance vers une logistique intelligente et des solutions de transport économiques alimente une forte demande pour les modèles TaaS. L'accent croissant mis sur la réduction des émissions et la modernisation des flottes contribue également à l'expansion du marché.

part de marché du camionnage en tant que service

Le secteur du transport routier à la demande est principalement dominé par des entreprises bien établies, notamment :

- Daimler Truck AG (Allemagne)

- AB Volvo (Suède)

- TRATON SE (Allemagne)

- Tata Motors Limited (Inde)

- Einride AB (Suède)

- BYD Company Limited (Chine)

- Volta Trucks (Suède)

- Xos, Inc. (États-Unis)

- Nikola Corporation (États-Unis)

- Hyliion Holdings Corp. (États-Unis)

- Convoy Inc. (États-Unis)

- Trimble Transport (États-Unis)

- Omnitracs LLC (États-Unis)

- OCTO Telematics Ltd. (Italie)

- Microlise Limited (Inde)

- Masternaut Limited (Royaume-Uni)

- Transfix (États-Unis)

- Fleet Advantage LLC (États-Unis)

Dernières évolutions du marché mondial du camionnage en tant que service

- En septembre 2024, Volvo Trucks a renforcé le marché du « camion en tant que service » (TaaS) en livrant 70 camions électriques Volvo VNR dans le cadre de l'initiative SWITCH-ON. Cette initiative a permis à plusieurs flottes du sud de la Californie d'adopter des camions zéro émission pour leurs opérations régionales de transport de marchandises. Soutenu par l'EPA et le South Coast AQMD, ce programme réduit les obstacles financiers et opérationnels à l'électrification. L'intégration de Volvo on Demand accélère encore l'adoption par le marché en permettant aux flottes d'accéder à des camions électriques via un modèle de service avec un investissement initial minimal, renforçant ainsi la transition vers des solutions de transport de marchandises durables et à faible intensité capitalistique.

- En novembre 2023, Hydrogen Vehicle Systems Limited (HVS) s'est associée à Zeti et à Gravis Capital pour lancer un modèle de transport en tant que service (TasaS) pour les camions à pile à combustible hydrogène, étendant ainsi la mobilité basée sur les services au secteur de l'hydrogène. Cette collaboration favorise une commercialisation plus large des camions à hydrogène en regroupant véhicules, financement et services opérationnels au sein d'une offre unique. Cette initiative renforce la confiance du marché dans les solutions de camions à hydrogène de type « TasaS » en répondant aux défis liés aux coûts, au financement et à l'adoption rencontrés par les gestionnaires de flottes.

- En août 2023, le partenariat de Webfleet avec VEV, fournisseur de solutions pour flottes électriques, a contribué de manière significative à l'écosystème du « Truck-as-a-Service » en soutenant la transition complète des flottes vers l'électrique. Cette collaboration permet aux gestionnaires de flottes de gérer l'approvisionnement en véhicules, l'infrastructure de recharge, l'électrification des sites et les opérations courantes grâce à des données télématiques. Cette évolution améliore l'efficacité opérationnelle et l'optimisation énergétique, renforçant ainsi la proposition de valeur des modèles de camions basés sur le service et accélérant l'adoption des flottes commerciales de véhicules électriques.

- En juin 2022, WattEV a annoncé son intention d'exploiter 12 000 camions électriques dans le cadre de son modèle « Truck-as-a-Service » d'ici 2030, témoignant ainsi de sa grande confiance dans le transport de marchandises électrifié à la demande. S'appuyant sur un réseau de recharge d'une puissance de plusieurs gigawatts, cette initiative comble les lacunes critiques en matière d'infrastructures qui freinent l'adoption des camions électriques. L'inauguration de la station-service pour camions électriques de Bakersfield, équipée de panneaux solaires, de batteries de stockage et de bornes de recharge de plusieurs mégawatts, confirme l'évolutivité et la viabilité à long terme des plateformes « Truck-as-a-Service » électriques.

- En mars 2022, la start-up américaine WattEV a commandé 50 camions électriques Volvo VNR pour son modèle de camionnage à la demande, marquant ainsi une première étape vers le transport de marchandises électrifié. Parallèlement au déploiement des véhicules, le développement de stations de recharge haute capacité en Californie renforce l'efficacité opérationnelle du transport routier électrique. Cette initiative a soutenu la dynamique initiale du marché en démontrant comment l'intégration des véhicules et des infrastructures de recharge permet des opérations de transport de marchandises électriques concrètes et axées sur les services.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.