Middle East And Africa Health Insurance Market

Taille du marché en milliards USD

TCAC :

%

USD

160.90 Billion

USD

215.17 Billion

2025

2033

USD

160.90 Billion

USD

215.17 Billion

2025

2033

| 2026 –2033 | |

| USD 160.90 Billion | |

| USD 215.17 Billion | |

| % | |

|

Middle East and Africa Health Insurance Market Segmentation, By Type (Products, and Solutions), Services (Inpatient Treatment, Outpatient Treatment, Medical Assistance, and Others), Level of Coverage (Bronze, Silver, Gold, and Platinum), Service Providers (Public Health Insurance Providers, and Private Health Insurance Providers), Health Insurance Plans (Point of Service (POS), Exclusive Provider Organization (EPOS), Indemnity Health Insurance, Health Savings Account (HSA), Qualified Small Employer Health Reimbursement Arrangements (QSEHRAS), Preferred Provider Organization (PPO), Health Maintenance Organization (HMO), and Others), Demographics (Adults, Minors, and Senior citizens), Coverage Type (Lifetime Coverage and Term Coverage), End User (Corporates, Individuals, and Others), Distribution Channel (Direct Sales, Financial Institutions, E-commerce, Hospitals, Clinics, and Others)- Industry Trends and Forecast to 2033

Quelle est la taille et l'aperçu du marché de l'assurance maladie au Moyen-Orient et en Afrique

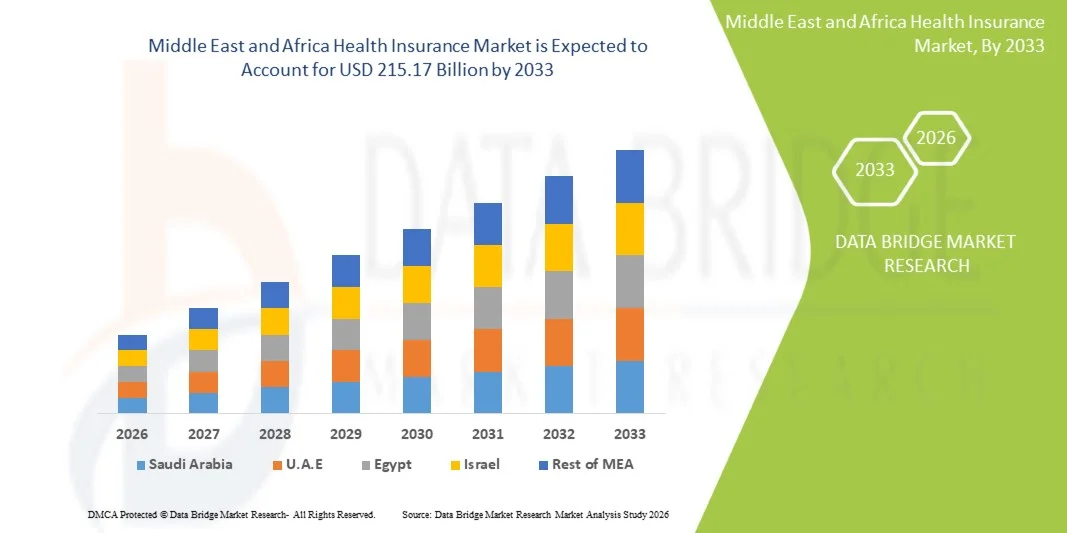

- Selon Data Bridge études de marché Analyse La taille du marché de l'assurance maladie au Moyen-Orient et en Afrique a été évaluée à160,90 milliards de dollars en 2025et devrait atteindre215,17 milliards de dollars en 2033, à unTCAC de 3,70 %pendant la période de prévision

- La croissance du marché est largement alimentée par une prise de conscience accrue de la couverture sanitaire, une augmentation des coûts des soins de santé et des initiatives gouvernementales favorisant la pénétration de l'assurance dans toute la région, ce qui conduit à une plus grande adoption de solutions d'assurance maladie dans les populations urbaines et rurales.

- En outre, la demande croissante de services complets, abordables et numériquesassurance maladieLes plans incitent les assureurs à innover et à élargir leurs offres. Ces facteurs convergents accélèrent l'adoption des produits d'assurance maladie, ce qui stimule considérablement la croissance de l'industrie.

Taille du marché et prévisions

- Valeur de marché (2025): 160,90 milliards de dollars

- Valeur marchande prévue (2033): 215,17 milliards de dollars

- Prévisions CAGR (2026-2033): 3.70%

Moyen-Orient et Afrique Analyse du marché de l'assurance maladie

- L'assurance maladie, qui assure une couverture financière pour les dépenses médicales et l'accès aux services de santé, devient de plus en plus critique au Moyen-Orient et en Afrique en raison de l'augmentation des coûts des soins de santé, de l'expansion des établissements de soins privés et de la prise de conscience croissante des avantages de l'assurance pour atténuer les dépenses hors de portée

- L'accélération de la demande d'assurance maladie est principalement motivée par des initiatives gouvernementales visant à élargir la couverture, à accroître la prévalence des maladies chroniques et à accroître la préférence des consommateurs pour des solutions d'assurance complètes, abordables et numériques

- Les Emirats arabes unis ont dominé le marché de l'assurance maladie au Moyen-Orient et en Afrique avec la plus grande part des revenus de 38,5 % en 2025, caractérisée par des dépenses élevées en soins de santé, des règlements d'assurance obligatoires et une forte présence d'assureurs de premier plan, avec une forte croissance de l'adoption de politiques en raison de la couverture médicale obligatoire pour les résidents et les employés des entreprises

- L ' Afrique du Sud devrait être le pays qui connaît la croissance la plus rapide sur le marché de l ' assurance maladie au cours de la période de prévision en raison de l ' augmentation des régimes d ' assurance subventionnés par l ' État, de l ' augmentation de la population de la classe moyenne et de l ' amélioration des infrastructures de soins de santé.

- Le segment des prestataires privés d'assurance maladie a dominé le marché avec une part de 46,8 % en 2025, en raison de ses options de couverture complètes, de sa flexibilité et de ses partenariats croissants entre les assureurs et les prestataires de soins de santé.

Portée du rapport et segmentation du marché de l'assurance maladie au Moyen-Orient et en Afrique

|

Attributs |

Moyen-Orient et Afrique Assurance maladie Principales perspectives du marché |

|

Segments couverts |

|

|

Pays couverts |

Moyen-Orient et Afrique

|

|

Principaux acteurs du marché |

|

|

Possibilités de marché |

|

|

Infos sur la valeur ajoutée |

En plus des renseignements sur les scénarios du marché comme la valeur du marché, le taux de croissance, la segmentation, la couverture géographique et les principaux intervenants, les rapports de marché établis par Data Bridge Market Research comprennent également une analyse approfondie des experts, l'épidémiologie des patients, l'analyse des pipelines, l'analyse des prix et le cadre réglementaire. |

Quelle est la tendance clé du marché de l'assurance maladie au Moyen-Orient et en Afrique

Transformation numérique et intégration de la télésanté

- Une tendance importante et accélérée sur le marché de l'assurance maladie au Moyen-Orient et en Afrique est l'adoption croissante de plateformes numériques ettélésantésolutions permettant aux assurés d'accéder aux services de santé et à la gestion des assurances à distance

- Par exemple, Daman Health, basée aux Émirats arabes unis, intègre les consultations en télémédecine à ses régimes d'assurance, permettant aux membres de recevoir des visites médicales virtuelles et de traiter les demandes par le biais d'une application mobile

- Les plateformes de santé numériques permettent aux assureurs d'analyser les données des patients, d'offrir des programmes de bien-être personnalisés et de rationaliser la gestion des réclamations, en améliorant la commodité et l'engagement des utilisateurs. Par exemple, Discovery Health en Afrique du Sud utilise des outils numériques de santé pour surveiller les maladies chroniques et fournir des renseignements proactifs sur la santé

- L'intégration de la télésanté aux régimes d'assurance facilite la gestion centralisée des services de santé, ce qui permet aux souscripteurs de fixer des rendez-vous, de suivre les demandes et d'accéder aux ressources en soins préventifs par une seule interface

- Cette tendance vers des services d'assurance plus connectés, axés sur la technologie et axés sur le patient modifie les attentes des consommateurs, ce qui incite les assureurs à développer des plates-formes d'applications avec des évaluations de la santé adaptées à l'IA et des options de soins virtuels

- La demande de solutions d'assurance-maladie qui offrent un accès numérique sans faille et l'intégration de la télésanté augmente rapidement dans les secteurs tant individuels que corporatifs, les consommateurs privilégiant de plus en plus la commodité et la gestion globale des soins de santé

- L'expansion du traitement des réclamations en nuage et de la souscription à l'IA permet des approbations plus rapides et une couverture personnalisée, améliorant ainsi l'expérience client globale. Par exemple, AXA Gulf utilise des plates-formes axées sur l'IA pour rationaliser les demandes de remboursement et l'émission de politiques pour ses clients

Dynamique du marché de l'assurance maladie au Moyen-Orient et en Afrique

Chauffeur

Augmentation des coûts des soins de santé et sensibilisation aux prestations d'assurance

- L'augmentation du coût des services de santé au Moyen-Orient et en Afrique, associée à une prise de conscience croissante des prestations d'assurance, est un facteur clé qui alimente l'adoption de produits d'assurance maladie.

- Par exemple, en mars 2025, le Conseil de l ' assurance maladie coopérative de l ' Arabie saoudite a lancé des campagnes de sensibilisation mettant l ' accent sur l ' assurance obligatoire pour les résidents et les expatriés, renforçant ainsi l ' application des politiques.

- Étant donné que les consommateurs cherchent à atténuer les dépenses imprévues et à assurer l'accès à des soins de qualité, les régimes d'assurance-santé offrent une protection financière, des programmes de bien-être et une couverture pour la gestion des maladies chroniques.

- De plus, les règlements et les mesures incitatives du gouvernement favorisant l'inscription à l'assurance encouragent les particuliers et les entreprises à adopter une couverture de santé, en l'intégrant dans les régimes d'avantages sociaux des employés et les régimes de santé familiale.

- La facilité de l'inscription numérique, les options de couverture flexibles et les partenariats avec les hôpitaux et les cliniques sont des facteurs clés de la croissance du marché dans les populations urbaines et rurales

- La demande croissante de la main-d'oeuvre expatriée dans les pays du CCG pousse les assureurs à offrir des plans de santé sur mesure qui répondent à divers besoins des employés. Par exemple, les multinationales des Émirats arabes unis et du Qatar exigent une couverture sanitaire complète pour le personnel étranger.

- L'incidence croissante de maladies du mode de vie comme le diabète et les troubles cardiovasculaires incite les individus à chercher des solutions d'assurance préventives et complètes. Par exemple, les assureurs d'Afrique du Sud mettent en place des programmes de gestion des maladies chroniques dans leurs plans.

Restriction/Défi

Pénétration de l'assurance limitée et fragmentation réglementaire

- La faible pénétration de l'assurance dans plusieurs pays et la fragmentation des cadres réglementaires posent des défis importants à l'expansion de l'assurance maladie au Moyen-Orient et en Afrique

- Ainsi, dans certaines parties de l ' Afrique subsaharienne, seul un faible pourcentage de la population dispose d ' une assurance maladie officielle, ce qui limite les possibilités de croissance du marché.

- L'incohérence des réglementations entre les pays crée des difficultés de conformité pour les assureurs opérant au niveau régional, qui affectent la normalisation des produits et l'expansion transfrontalière. Par exemple, les assureurs qui entrent au Nigéria sont confrontés à diverses exigences au niveau de l'État qui compliquent les offres de politique uniforme

- L'abordabilité demeure un obstacle, car des primes élevées peuvent dissuader les ménages à faible revenu d'acheter, en particulier dans les pays qui n'ont pas de subventions publiques ou de régimes patronnés par l'employeur.

- Surmonter ces défis grâce à l'harmonisation des réglementations, à des campagnes de sensibilisation ciblées et à la mise au point de produits d'assurance peu coûteux et accessibles sera essentiel pour une croissance soutenue du marché

- La littératie numérique limitée dans les zones rurales et semi-urbaines empêche l'adoption de solutions d'assurance fondées sur l'application et la télésanté. Par exemple, certaines communautés rurales du Kenya luttent pour naviguer dans les processus d'inscription et de réclamation en ligne

- L'instabilité politique et les fluctuations économiques dans certains pays peuvent perturber les opérations d'assurance, réduire la confiance des consommateurs et retarder les plans d'expansion. Par exemple, les assureurs de certaines régions d'Afrique du Nord sont confrontés à des difficultés en période d'incertitude économique.

Portée du marché de l'assurance maladie au Moyen-Orient et en Afrique

Le marché est segmenté en fonction du type, des services, du niveau de couverture, des fournisseurs de services, des régimes d'assurance-maladie, de la démographie, du type de couverture, de l'utilisateur final et du canal de distribution.

- Par type

Sur la base du type, le marché est segmenté en produits et solutions. Le segment des produits a dominé le marché en 2025 en raison de l'adoption généralisée de polices d'assurance-maladie autonomes offrant une couverture financière pour l'hospitalisation, les soins ambulatoires et la gestion des maladies chroniques. Les consommateurs préfèrent les produits pour leur couverture structurée, la transparence des primes et la facilité de compréhension, en particulier dans les pays du CCG qui connaissent bien les prestations d'assurance. Les cadres réglementaires dans des pays comme les Émirats arabes unis et l ' Arabie saoudite ont normalisé ces produits, ce qui les rend largement fiables. Les assureurs regroupent également d'autres services comme les programmes de bien-être, l'accès à la télémédecine et le soutien médical d'urgence, ce qui améliore encore l'appel. Les entreprises et les particuliers comptent de plus en plus sur l'assurance fondée sur les produits pour une couverture prévisible et une gestion budgétaire. Les politiques fondées sur les produits bénéficient également d'une forte reconnaissance du marketing et de la marque, ce qui contribue à la domination du marché.

Le segment des solutions devrait connaître la croissance la plus rapide de 2026 à 2033, en raison de la demande croissante de services intégrés de santé et d'assurance. Ces solutions combinent une couverture d'assurance avec des plateformes de santé numériques, des évaluations de la santé fondées sur l'IA et des programmes de soins préventifs. Les consommateurs et les entreprises recherchent de plus en plus des solutions personnalisées qui traitent à la fois de la protection financière et de la gestion proactive de la santé. Les plateformes app et l'intégration de la télémédecine améliorent la commodité et l'accessibilité, en particulier dans les zones urbaines. Les assureurs-santé innovent avec des solutions qui surveillent la santé des patients, fournissent des rappels pour les examens et offrent un soutien à la gestion des maladies chroniques. L'éducation et la formation numériquessmartphonela pénétration accélère encore l'adoption d'offres d'assurance basées sur des solutions dans la région.

- Par services

Sur la base des services, le marché est segmenté en soins hospitaliers, soins ambulatoires, assistance médicale, etc. En 2025, le secteur des soins aux malades hospitalisés a dominé le secteur en raison des coûts élevés associés à l'hospitalisation, aux chirurgies et aux soins d'urgence. Les consommateurs des Émirats arabes unis, de l'Arabie saoudite et de l'Afrique du Sud préfèrent des plans couvrant les séjours à l'hôpital et les soins critiques, minimisant ainsi les paiements à l'extérieur. Les règlements d'assurance obligatoires pour les expatriés et les employés dans les pays du CCG conduisent à l'adoption à grande échelle. Les assureurs comprennent souvent des services à valeur ajoutée comme l'accès au réseau hospitalier, la modernisation des salles et l'aide à la préautorisation pour accroître l'attrait. La couverture des malades hospitalisés demeure essentielle pour la protection financière contre les événements sanitaires graves. Ce segment contribue considérablement aux recettes globales en raison de primes plus élevées et d'une utilisation plus large.

Le segment des traitements ambulatoires devrait connaître la croissance la plus rapide au cours de la période de prévision, en raison de la demande croissante de consultations, de diagnostics et de procédures mineures. L'adoption de la télémédecine et les programmes de soins préventifs stimulent la croissance, en particulier dans les zones urbaines. La couverture ambulatoire s'adresse aux assurés qui recherchent des soins de santé quotidiens abordables et pratiques. Les assureurs comprennent de plus en plus de programmes de bien-être, de couverture vaccinale et de contrôles de routine pour attirer les clients. Les plateformes numériques qui fournissent des consultations à distance et des abonnements électroniques améliorent l'adoption du segment. Les entreprises offrant des prestations ambulatoires aux employés appuient également une croissance rapide dans ce segment.

- Par niveau de couverture

Sur la base du niveau de couverture, le marché est segmenté enbronze,argent, or et platine. Le segment de l'or a dominé en 2025 en raison de son coût abordable équilibré et des avantages globaux, y compris l'hospitalisation, les soins ambulatoires et les programmes de bien-être. Les entreprises adoptent souvent des régimes à taux d'or pour les employés, tandis que les personnes à revenu élevé les préfèrent pour la couverture familiale. Les plans d'or comprennent également la télémédecine et les avantages de la gestion des maladies chroniques, ce qui les rend attrayants pour tous les groupes démographiques. Les assureurs promeuvent activement les plans d'or numériquement et par le biais de liens d'entreprise. Les options de couverture internationale dans les plans d'or renforcent encore l'adoption dans les pays du CCG. La combinaison de l'abordabilité et des avantages globaux assure la domination de ce segment.

Le segment du platine devrait connaître la croissance la plus rapide de 2026 à 2033, en raison de la demande de primes et d'assurances tout compris chez les personnes à forte valeur nette et les expatriés. Les plans Platinum offrent une couverture mondiale, des services de conciergerie et des options de télésanté avancées. L'augmentation de l'abondance et du tourisme médical dans les pays du CCG augmente l'adoption. Les politiques de Platinum font appel aux personnes qui recherchent une protection maximale avec des dépenses minimes. Les assureurs marketing ces plans avec des avantages de bien-être et de prévention supplémentaires pour attirer des clients premium. La croissance est également alimentée par les entreprises offrant des plans d'élite pour les cadres supérieurs et le personnel international.

- Par les fournisseurs de services

Sur la base des prestataires de services, le marché est segmenté en prestataires publics d'assurance maladie et en prestataires privés d'assurance maladie. Le segment des fournisseurs privés a dominé en 2025 avec une part de marché de 46,8 % en raison d'un large éventail d'options de régime, d'un traitement plus rapide des demandes et de services à valeur ajoutée comme les programmes de télémédecine et de bien-être. Les assureurs privés s'adressent à la fois aux entreprises et aux particuliers, offrant une couverture souple dans plusieurs établissements de soins de santé. Des pays comme les Émirats arabes unis et l'Afrique du Sud ont une forte présence d'assureurs privés, ce qui augmente la part de marché. Les assureurs privés sont plus agiles dans l'innovation des produits et l'adoption numérique, améliorant la satisfaction des clients. Leurs partenariats avec les hôpitaux et les cliniques assurent une meilleure accessibilité des services et soutiennent la domination. Le marketing et la visibilité de la marque contribuent également à une large adoption.

Le segment des fournisseurs publics devrait connaître la croissance la plus rapide de 2026 à 2033, en raison des initiatives gouvernementales qui étendent la couverture d'assurance aux populations mal desservies. Les programmes en Arabie saoudite, au Kenya et dans d'autres pays visent à accroître l'inscription par des politiques et des subventions obligatoires. Les régimes d'assurances publiques mettent l'accent sur l'abordabilité, l'accessibilité et l'inclusion, en aidant les populations rurales et à faible revenu. Les plateformes numériques d'inscription et les services mobiles favorisent l'adoption. Les partenariats avec des assureurs privés pour la prestation de services en réseau se multiplient également. L'augmentation des dépenses publiques consacrées aux campagnes de sensibilisation à la santé et aux assurances est à l'origine de la croissance rapide de ce segment.

- Par les régimes d'assurance-maladie

Sur la base de plans, le marché est segmenté en POS, EPOS, Indemnity, HSA, QSEHRA, PPO, HMO, etc. Le segment des OHM a dominé en 2025 en raison de son réseau structuré de fournisseurs, de l'efficience et de la couverture des soins préventifs. Les entreprises des Emirats arabes unis et des pays du CCG adoptent souvent des régimes d'assurance-chômage pour les avantages sociaux des employés. Les soins coordonnés, le traitement centralisé des demandes et l'inclusion de la télémédecine renforcent son appel. Les OSM offrent également des programmes de gestion des maladies chroniques et de mieux-être, ce qui accroît leur attractivité. De vastes réseaux hospitaliers et cliniques renforcent l'adoption. Les souscripteurs apprécient la prévisibilité des coûts et des services, ce qui renforce la domination.

Le segment des PPO devrait connaître la croissance la plus rapide entre 2026 et 2033, en raison de la souplesse dans le choix des fournisseurs et des établissements de soins. Les expatriés et les personnes à revenu élevé préfèrent les PPO pour la liberté de choix du fournisseur. Les assureurs améliorent les offres de PPO avec la télémédecine, le bien-être et la couverture internationale. Une sensibilisation accrue aux soins de santé personnalisés favorise l'adoption. Les plans de PPO attirent également les clients de l'entreprise à la recherche de la satisfaction et de la mobilité des employés. Les plateformes numériques facilitent les revendications et l'accès au réseau, accélérant la croissance.

- Données démographiques

Sur la base de la démographie, le marché est segmenté en adultes, mineurs et personnes âgées. Le segment des adultes a dominé en 2025 en raison d'une plus grande sensibilisation aux risques pour la santé, au revenu disponible et à la responsabilité de la couverture familiale. Les adultes, en particulier les professionnels, sont les principaux acheteurs de politiques. Les plans d'entreprise contribuent à la domination. Les assurances pour adultes comprennent souvent des services ambulatoires, hospitaliers et préventifs. Le segment bénéficie d'une couverture individuelle et familiale. Les campagnes de sensibilisation et les exigences réglementaires favorisent une adoption généralisée.

Le segment des personnes âgées devrait connaître la croissance la plus rapide de 2026 à 2033, en raison du vieillissement de la population, de l'augmentation de la prévalence des maladies chroniques et de l'augmentation des dépenses de santé. Les plans spécialisés pour les aînés couvrent les conditions liées à l'âge, les soins à domicile et les soins préventifs. Les assureurs des EAU et de l'Afrique du Sud ciblent les personnes âgées avec des produits sur mesure. Les plateformes numériques et les services de conciergerie améliorent l'accessibilité. L'augmentation de l'espérance de vie entraîne une demande d'assurance à long terme. Les programmes gouvernementaux et privés se concentrent de plus en plus sur la couverture des personnes âgées, ce qui accélère l ' adoption.

- Par type de couverture

En fonction du type de couverture, le marché est segmenté en couverture à vie et en couverture à terme. En 2025, le segment de la couverture à terme a dominé en raison de l'abordabilité, des durées flexibles et de l'aptitude des entreprises et des particuliers. Les politiques à terme s'adressent aux jeunes adultes qui cherchent une couverture pour des périodes ou des projets précis. Les plans à court terme et les plans renouvelables permettent une gestion facile des primes. Les souscripteurs bénéficient de coûts prévisibles et de réclamations simples. La couverture à terme est populaire dans les régimes obligatoires d'assurance des entreprises. La familiarité du marché et la facilité d'achat renforcent la domination.

Le segment de la couverture à vie devrait connaître la croissance la plus rapide de 2026 à 2033, en raison des besoins de protection financière à long terme et de la sécurité des soins de santé après la retraite. Les assureurs offrent des politiques à vie avec des avantages de bien-être et de gestion des maladies chroniques. Les personnes à haute valeur nette préfèrent une couverture à vie pour une sécurité complète. Le vieillissement des populations du CCG et de l'Afrique du Sud est à l'origine de la demande. Les assureurs améliorent les outils numériques pour la gestion des réclamations et des politiques. La croissance est également alimentée par une sensibilisation accrue aux risques à long terme pour la santé.

- Par Utilisateur final

Sur la base de l'utilisateur final, le marché est segmenté en entreprises, particuliers et autres. Le segment des entreprises a dominé en 2025 en raison de l'assurance mandatée par l'employeur, de l'augmentation des besoins en matière de santé de la main-d'oeuvre et de l'inclusion des prestations dans les régimes de rémunération. Les grandes organisations négocient des politiques de groupe, ce qui entraîne des revenus élevés du marché. Les entreprises bénéficient également de la prévisibilité des coûts et de la rationalisation des réclamations. Les programmes de bien-être des employés appuient davantage l'adoption. Les assureurs ciblent activement les entreprises clientes par le biais de ventes numériques et directes. Les mandats réglementaires des pays du CCG renforcent l'adoption des entreprises.

Le segment des personnes devrait connaître la croissance la plus rapide de 2026 à 2033, en raison de la sensibilisation accrue à la santé, des plateformes d'assurance numériques et de l'accroissement de la population de la classe moyenne. Les particuliers préfèrent les régimes personnels offrant une souplesse et des avantages sur mesure. Les applications Smartphone et les portails en ligne rendent les processus d'achat et de réclamation pratiques. Les consommateurs soucieux de la santé recherchent une couverture de soins préventifs. Le marketing numérique et l'intégration de la télémédecine favorisent une adoption rapide. Les politiques pour les pigistes et les propriétaires de petites entreprises favorisent également la croissance.

- Par canal de distribution

Sur la base du canal de distribution, le marché est segmenté en ventes directes, institutions financières, commerce électronique, hôpitaux, cliniques, etc. Le segment des ventes directes a dominé en 2025 en raison de solides relations entre les assureurs et les clients, de services consultatifs personnalisés et d'offres d'entreprise personnalisées. Les assureurs s'engagent activement auprès des clients individuels et des entreprises, ce qui améliore la pénétration. Les équipes de vente directe expliquent les termes complexes de la politique et les avantages de la couverture, renforçant la confiance. Les clients de grande valeur préfèrent souvent les interactions en personne. Les campagnes de marketing renforcent la visibilité de la marque. L'accessibilité des agents et des courtiers contribue à la domination du segment.

Le segment du commerce électronique devrait connaître la croissance la plus rapide entre 2026 et 2033, en raison de l'adoption numérique croissante, des achats fondés sur la politique de téléphonie mobile et de la gestion des réclamations en ligne. Les assureurs investissent dans des plateformes numériques faciles à utiliser qui fournissent des devis instantanés, une comparaison des politiques et le traitement des demandes. Les populations urbaines préfèrent de plus en plus les canaux en ligne. App-based inscription simplifie l'accès à la couverture pour les consommateurs de technologie. L'intégration de la télémédecine aux plateformes de commerce électronique accroît la valeur. Les tendances de l'adoption numérique en Afrique du Sud et du CCG accélèrent la croissance du segment.

Moyen-Orient et Afrique Analyse régionale du marché de l'assurance maladie

- Les Emirats arabes unis ont dominé le marché de l'assurance maladie au Moyen-Orient et en Afrique avec la plus grande part des revenus de 38,5 % en 2025, caractérisée par des dépenses élevées en soins de santé, des règlements d'assurance obligatoires et une forte présence d'assureurs de premier plan, avec une forte croissance de l'adoption de politiques en raison de la couverture médicale obligatoire pour les résidents et les employés des entreprises

- Les consommateurs des EAU apprécient de plus en plus la couverture complète, l'accès aux réseaux de soins de santé privés et les programmes intégrés de bien-être offerts par les fournisseurs d'assurance-maladie. Les politiques parrainées par l'entreprise et la couverture prescrite par l'employeur améliorent encore l'adoption

- Cette adoption généralisée est soutenue par de solides initiatives gouvernementales, l'augmentation des coûts des soins de santé et la demande croissante de solutions d'assurance numérique, la mise en place d'une assurance maladie comme outil essentiel de planification financière et de soins de santé pour les particuliers et les entreprises des Émirats arabes unis

Aperçu du marché de l'assurance maladie des EAU

Le marché de l'assurance maladie des Émirats arabes unis a enregistré la plus grande part des revenus de 38,5 % en 2025 dans la région du Moyen-Orient et de l'Afrique, alimentée par la réglementation obligatoire de l'assurance maladie pour les résidents et les expatriés, l'augmentation des coûts des soins de santé et la sensibilisation aux prestations d'assurance. Les consommateurs privilégient de plus en plus la couverture complète, l'accès aux réseaux de soins de santé privés et les programmes intégrés de bien-être. La tendance croissante de l'assurance parrainée par les entreprises et de la gestion des politiques numériques propulse le marché. De plus, les initiatives du gouvernement des Émirats arabes unis visant à élargir l'accès aux soins de santé et à promouvoir l'adoption d'une assurance contribuent grandement à la croissance du marché.

Sur le marché de l'assurance maladie en Arabie saoudite

Le marché saoudien de l'assurance maladie devrait s'étendre à un TCAC important tout au long de la période de prévision, principalement grâce à l'assurance maladie coopérative obligatoire pour les employés et les résidents, à l'urbanisation croissante et à l'augmentation des infrastructures de soins de santé privées. Les consommateurs sont attirés par des plans complets couvrant l'hospitalisation, les soins ambulatoires et la gestion des maladies chroniques. Les plateformes numériques pour le traitement des demandes et la gestion des politiques favorisent l'adoption. La demande augmente également dans les secteurs des entreprises, des particuliers et des expatriés. De plus, les réformes en cours en matière de soins de santé et les investissements dans les établissements médicaux stimulent l'expansion du marché.

Aperçu du marché de l'assurance maladie en Égypte

Le marché égyptien de l'assurance maladie devrait croître à un TCAC remarquable au cours de la période de prévision, en raison d'une sensibilisation accrue aux soins de santé, d'initiatives d'assurance menées par le gouvernement et d'une participation accrue du secteur privé. Les préoccupations concernant les frais médicaux élevés hors de la poche encouragent les particuliers et les familles à adopter une assurance maladie. La mise en place de programmes d'assurance maladie sociale et de partenariats avec des assureurs privés améliore l'accessibilité. Les populations urbaines accordent une plus grande préférence aux inscriptions numériques et aux installations de réclamation sans espèces. La croissance de la couverture d'assurance des sociétés et des régimes de santé volontaires contribue également au développement du marché.

Aperçu du marché de l'assurance maladie en Afrique du Sud

Le marché sud-africain de l'assurance maladie devrait se développer à un TCAC considérable au cours de la période de prévision, alimenté par l'augmentation de la demande de soins de santé privés, l'augmentation de la prévalence des maladies chroniques et la sensibilisation aux prestations d'assurance. Les consommateurs sud-africains apprécient les plans offrant de vastes réseaux hospitaliers, des soins préventifs et des programmes de bien-être. Les programmes de groupes parrainés par les entreprises sont largement adoptés dans toutes les industries. La gestion des politiques numériques et mobiles est de plus en plus courante, ce qui permet d'accélérer l'inscription et le traitement des demandes. L'intégration de l'assurance-maladie aux programmes de télémédecine et de gestion des soins chroniques favorise l'adoption. Les initiatives de viabilité et d'abordabilité des assureurs attirent une clientèle plus large.

Quelles sont les entreprises les plus importantes au Moyen-Orient et en Afrique

L'industrie de l'assurance maladie au Moyen-Orient et en Afrique est principalement dirigée par des entreprises bien établies, notamment :

- Allemagne(Arabie saoudite)

- La Compagnie nationale d'assurance (EAU)

- Abu Dhabi National Insurance Company (EAU)

- Groupe d ' assurance du Qatar (Qatar)

- Sanlam Limited(Afrique du Sud)

- Groupe Allianz (Allemagne)

- Iran Insurance Company (Iran)

- Assurance Orient PJSC (EAU)

- AXA (France)

- Cigna Santé Moyen-Orient (EAU)

- Aetna Inc.(États-Unis)

- Maintenant Health International (Hong Kong)

- Société Centene (États-Unis)

- Anthem Insurance Companies, Inc. (États-Unis)

- Broadstone Corporate Benefits Limited (Royaume-Uni)

- Vitalité (Royaume-Uni)

- International Medical Group, Inc. (États-Unis)

- Groupe Vhi (Irlande)

- Société d'assurance coopérative (Arabie saoudite)

Quelles sont les évolutions récentes au Moyen-Orient et en Afrique

- En octobre 2025, Vitals et MSH MENA ont signé un protocole d'entente (PE) à Dubaï pour collaborer à des solutions de santé administratives intégrées qui améliorent les services transfrontaliers d'assurance maladie pour les expatriés, les multinationales et les citoyens du monde entier

- En mai 2025, la Fondation OMS a signé son premier partenariat dans la région du CCG avec Tawuniya, le plus grand assureur d'Arabie saoudite, pour faire progresser l'innovation en matière de santé et la prestation de soins de santé numériques dans toute la Méditerranée orientale. L'entente vise à tirer parti de l'IA, des plateformes numériques et des stratégies fondées sur des données probantes pour améliorer la prestation des soins et les résultats en matière de santé

- En novembre 2023, Cigna Healthcare a annoncé un partenariat stratégique avec AAR Insurance Kenya pour fournir des services d'assurance maladie élargis et innovants en Afrique de l'Est, combinant l'expertise mondiale en assurance et les connaissances du marché local pour améliorer l'accès aux soins

- En juillet 2023, le gouvernement égyptien a mis en lumière la première phase de son système global d'assurance maladie, avec un investissement de 1,09 milliard de dollars US dans l'infrastructure sanitaire qui comprendra des centaines d'établissements et élargira les services assurés aux niveaux primaire, secondaire et tertiaire.

- En juin 2023, Esaal (plate-forme de santé et de bien-être en ligne) et Allianz Insurance Egypt ont lancé un partenariat exclusif pour intégrer les consultations en santé mentale et en nutrition dans les offres d'assurance maladie élargissant les services de soins holistiques offerts aux assurés en Égypte et dans toute la région MENA

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.