アジア・パシフィック原子力医療機器市場規模、株式・動向分析レポート

Market Size in USD Billion

CAGR :

%

USD

4.06 Billion

USD

5.60 Billion

2024

2032

USD

4.06 Billion

USD

5.60 Billion

2024

2032

| 2025 –2032 | |

| USD 4.06 Billion | |

| USD 5.60 Billion | |

| % | |

|

アジア・パシフィック原子力医療機器市場セグメンテーション、製品別(シングル・フォトン・エミッション・コンピューティング・トモグラフィ(SPECT)、ハイブリッド・ペット、平面シンティグラフィー)、アプリケーション(心臓学、腫瘍学、神経学および他の応用)、エンド・ユーザー(病院、イメージングセンター、アカデミック・リサーチセンター、その他エンド・ユーザー)- 業界動向と予測 2032

アジア・パシフィック原子力医療機器市場規模

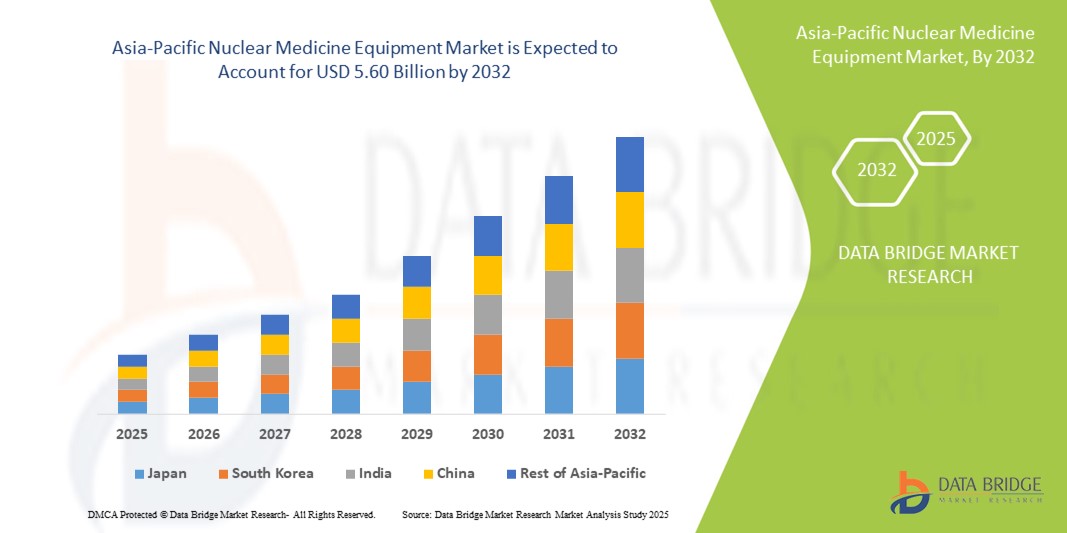

- アジア太平洋原子力医療機器市場規模は、2024年のUSD 4.06億そして到達する予定2032年までのUSD 5.60億, お問い合わせ4.10%のCAGR予報期間中

- 市場成長は、がんおよび心血管疾患の上昇の蔓延によって主に燃料を補給し、地域における新興国における高度な診断イメージング技術の高度化と相まって

- さらに、医療投資の増加、診断インフラの近代化に向けた支援政府の取り組み、正確で非侵襲的なイメージングソリューションの需要の高まりは、核医学装置を選定の重要な診断ツールとして位置付けています。 これらの結合要因は、採用を加速しています, これにより、業界の成長を著しく向上します

アジア・太平洋核医学機器市場分析

- 核医学装置、を含むペット、SPECTおよびガンマのカメラは、高精度、非侵襲的な性質および早期の病気を検出する能力による病院および診断中心の高度の診断イメージ投射および療法のためのますますます重要な用具です

- 核医学機器のエスカレート要求は、がんおよび心血管疾患の上昇前因によって主に燃料を供給され、ヘルスケアインフラ投資を成長させ、技術的に先進的なイメージングソリューションの採用を増加させます

- 日本は、2024年に39%の世界最大の収益シェアを持つアジア太平洋原子力医療機器市場を支配しました。先進医療インフラ、革新的なイメージングモダリティの高い採用、そして大手機器メーカーの存在感、ペットの大きな成長とAI支援診断およびハイブリッドイメージングシステムとの統合によるSPECTインストールが大幅に向上しました。

- 中国は、原子力医療施設の拡大、ヘルスケア支出の上昇、早期疾患診断の普及による予測期間中、アジア・パシフィック原子力医療機器市場で最も急速に成長している国であることが期待されています

- ハイブリッドPETセグメントは、2024年の45.8%の市場シェアで原子力医療機器市場を支配し、優れたイメージング分解能、腫瘍学的用途の精度、および多品種イメージング技術との統合を強化

報告書 スコープ・アジア・太平洋 核医学機器市場セグメント

| アトリビュート | アジア・太平洋核医学機器 主要市場動向 |

| カバーされる区分 |

|

| カバーされた国 | アジアパシフィック

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

アジア・太平洋核医学機器市場動向

ハイブリッドPETとSPECTイメージング技術の高度化

- アジア・パシフィック原子力医療機器市場における重要な加速傾向は、PET/CTやSPECT/CTなどのハイブリッドイメージングシステムの統合で、腫瘍学、心臓学、神経学アプリケーションにおける診断精度と臨床的意思決定を強化しています。

- 例えば、シーメンスバイオグラフmCTはPETとCTイメージングを組み合わせ、臨床医が1つのスキャンで解剖構造に沿って代謝活動を視覚化し、早期疾患の検出と治療モニタリングを改善します。

- ハイブリッドイメージング技術により、スキャン時間の削減、放射線線量の低減、高分解能画像の低減、正確な診断と患者固有の治療計画の促進が可能になります。 たとえば、GEヘルスケアのディスカバリーNM/CT 670システムは、 SPECT と CT を統合し、病変のローカリゼーションと定量を改善します。

- 成長する採用ツイート- 核医学機器における画像再構築と定量分析により、これらのシステムの臨床的有用性が向上し、より速く、より正確なスキャンの解釈を可能にします。 人工知能のアルゴリズムを通して、病院はより微妙な異常を検出し、病気の進行を追跡できます

- この傾向は、より正確で効率的かつ統合されたイメージングシステムへの根本的に診断の期待を再構築し、キヤノンメディカルシステムズなどの自動車メーカーは、AIベースの画像最適化と線量削減技術でハイブリッド核医学機器を開発する

- 高度のイメージングおよびAIの統合の雑種ペットおよびSPECTシステムのための要求は臨床医が精密、効率および広範囲の診断機能を優先するので、病院およびイメージング センターを渡る急速に成長しています

アジア・太平洋核医学機器市場ダイナミクス

ドライバー

がんおよび心血管疾患の増大

- アジア太平洋諸国におけるがん、心血管障害、神経疾患の高まりは、病院や診断センターにおける核医学機器の普及のための主要なドライバーです。

- 例えば、2024年、国立がんセンター・ジャパンは、初期がんを検知するPET/CTスキャン利用を大幅に増加させ、先進的な核撮像モーダリティに対する臨床需要の上昇を強調した。

- 早期疾患の検出と正確な診断に関する臨床医と患者の意識の拡大は、高解像SPECTおよびハイブリッドPETシステムへの投資を加速し、信頼性と非侵襲的なイメージングソリューションを提供します

- さらに、政府の医療への取り組みや診断インフラの資金調達の増加は、機器のアップグレードや最新の核医学技術を採用し、先進的なイメージングサービスへのアクセスを強化する病院を奨励しています。

- 精密医薬品や標的療法の焦点が高まり、治療計画やモニタリングに欠かせない核薬装置をつくり、正確なイメージングにより、最適な患者固有のケアを実現

拘束/チャレンジ

高い機器コストと規制コンプライアンスハルール

- ハイブリッドペットおよびSPECTシステムを含む原子力医療機器に必要な高い初期投資は、特に開発途上国における小規模な病院や診断センターの採用のための重要な課題です

- たとえば、完全に統合されたPET / CTスキャナーのコストは、臨床上の優位性にもかかわらず、予算に配慮した医療プロバイダのアクセシビリティを制限し、数百万米ドルを超えることができます。

- 機器の安全性、放射線順守、および輸入承認のための厳格な規制要件は、追加のハードルをポーズし、インストールを遅延させ、メーカーやエンドユーザーのための運用の複雑性を高めます

- また、先進的な訓練を受けた人員が、原子力医療システムを運用・維持し、運用コストをさらに向上し、特に新興国では迅速な導入を制限する必要性が高まっています。

- 金融ソリューション、政府補助金、医療スタッフのトレーニングプログラムを通じて、これらの課題に取り組むことは、持続可能な市場成長とアジア太平洋地域における原子力医療機器の普及に不可欠です。

アジア・太平洋核医学機器市場規模

市場は製品、アプリケーション、エンドユーザーに基づいてセグメント化されます。

- 製品情報

製品をベースに、アジア・パシフィックの核医学機器市場は、シングルフォトン・エミッション・コンピューティング・トモグラフィー(SPECT)、ハイブリッド・ペット、平面シンティグラフィに分けられます。 ハイブリッドPETセグメントは、2024年に最大45.8%の収益シェアで市場を支配し、優れたイメージング分解能、腫瘍学的および心臓学的アプリケーションの高感度、単一のスキャンで分析的および機能的なイメージングを提供する能力を発揮しました。 病院やイメージングセンターは、早期疾患の検出と治療監視の精度でハイブリッドPETシステムをますますます好ましく、臨床的意思決定を強化します。 また、AIによる画像再構築や、他の画像モダリティとの統合により、先端医療施設の採用を強化しました。 ハイブリッドPETシステムは、独自の治療計画と治療評価を可能にします。 セグメントの優位性は、継続的な技術の進歩と精密医療に注力することで強化されます。

SPECT セグメントは、2025 から 2032 までの 22.1% の最速成長率を目撃し、心臓学および神経学の適用の増加による燃料供給を期待しています。 SPECTシステムは、中国やインドなどの新興市場での費用対効果の高い信頼性の高い診断を提供する、心臓と脳の機能イメージングに広く使用されています。 SPECTディテクタ技術、画像の解像度、CTスキャナとの統合の改善は、病院やイメージングセンターでの臨床ユーティリティと採用を強化しています。 ハイブリッドPETシステムと比較して、比較的低コストで、中層医療従事者向けにSPECTの魅力を発揮します。 さらに、SPECTの幅広い範囲との互換性ラジオ医薬品多様な診断アプリケーションをサポートし、市場成長を促進します。

- 用途別

適用に基づいて、市場は心臓学、腫瘍学、神経学および他の適用に分けられます。 腫瘍学のセグメントは、2024年に41.6%の収益シェアで市場を支配し、がんの上昇の蔓延と早期診断と治療計画の高まりの重要性を主導しました。 核医学装置、特にハイブリッドPETおよびSPECTは、腫瘍の検出、ステージング、および治療上の応答を監視するためにますます使用されています。 病院および専門がんセンターの腫瘍学部門は、パーソナライズされた治療アプローチをサポートする精度と能力のために、これらのシステムを急速に採用しています。 放射線薬学およびAIベースの画像解析の進歩により、腫瘍学診断の精度と速度を向上させることができます。 患者と臨床医の間で早期のがん検出の意識が高まり、この応用分野の優位性を補強しています。

心臓学分野は、2025年から2032年まで最速のCAGRを目撃し、アジア太平洋諸国における心血管疾患の普及と核心臓学イメージングの採用を加速させることで期待されています。 心機能および虚血症の評価でSPECTおよびペットの助けを使用してmyocardialの注入のイメージ投射のような技術は、時機を得た介入を促進します。 心臓のケアインフラを改善し、診断センターでの投資を増加させるための政府の取り組みは、心臓学における核医学機器の使用を加速しています。 セグメントは、ハイブリッドイメージングシステムやAI支援量定量分析などの技術の進歩から恩恵を受けており、診断精度と患者の成果を改善します。

- エンドユーザーによる

エンドユーザーに基づいて、市場は病院、イメージングセンター、学術および研究センター、およびその他のエンドユーザーに分かれています。 病院のセグメントは、2024年に52.4%の最大の収益シェアで市場を支配し、設備の整った放射線学部門、高患者量、先進的な核医学システムへの投資の増加の存在によって駆動しました。 病院は正確な診断、処置の監視および研究の目的のためにハイブリッド ペットおよびSPECT装置を好みます。 AIベースのワークフローソリューション、PACS、病院情報システムとの統合により、運用効率が向上します。 加えて、病院はしばしば訓練された核医学の専門家の専任チームを持ち、これらのハイエンドイメージングシステムを最大限に活用できるようにします。 先進の核医学機器の病院の需要は、アジア・太平洋諸国における政府の医療イニシアティブや民間部門の投資によっても支持されています。

イメージングセンターのセグメントは、2025年から2032年までの最速成長を目撃する見込みで、スタンドアロンの診断センターが増え、専用のイメージングサービスの患者様の好みが高まります。 イメージングセンターは、コスト効率の高いSPECTシステムとハイブリッドイメージング技術を採用し、より短い待ち時間で正確で非侵襲的な診断を提供します。 機器メーカーが提供する柔軟な資金調達モデルやリースオプションも、新興市場でのイメージングセンターの拡大を支援しています。 早期診断の意識を成長させ、技術の進歩と相まって、過渡的な設定で核医学機器の需要を主導しています。 イメージングセンターは、患者の利便性と高スループット診断に重点を置き、市場成長を加速しています。

アジア・太平洋核医学機器市場地域分析

- 日本は、2024年に39%の世界最大の収益シェアを持つアジア太平洋原子力医療機器市場を支配しました。先進医療インフラ、革新的なイメージングモダリティの高い採用、そして大手機器メーカーの存在感、ペットの大きな成長とAI支援診断およびハイブリッドイメージングシステムとの統合によるSPECTインストールが大幅に向上しました。

- 日本における病院やイメージングセンターは、腫瘍学、心臓学、神経学の用途にハイブリッドPETおよびSPECTシステムを利用し、早期疾患の検出と治療監視における高い診断精度と効率性を高めています。

- この広範囲にわたる採用は、強力な政府の医療イニシアティブ、原子力医療専門家の熟練した労働力、および主要な機器メーカーの存在によってさらに支持され、病院および国を渡る専門的イメージングセンターの好まれる診断ツールとして原子力システムを確立します

日本核医療機器市場動向

日本原子力医療機器市場は、高度医療インフラ、ハイブリッドペットやSPECTシステムの普及、早期疾病検知に重点を置いた、2024年に最大39%の収益シェアを誇るアジア太平洋地域を占めています。 病院およびイメージングセンターは、腫瘍学、心臓学および神経学の適用の精密な診断を優先順位付けし、AI-assistedイメージングを活用して、精度とワークフローの効率性を向上させます。 高度の診断設備を支える政府のイニシアチブおよび一流の装置の製造業者の存在は市場優位性を高めます。 また、日本の高齢化の人口と、住宅医療と専門センターを横断する先進の核医療機器の精密医療ドライブの需要に重点を置いています。

中国核医学機器市場洞察

中国原子力医療機器市場は、予測期間中、アジア太平洋地域で急速に成長し、急激な医療インフラの拡大、がんおよび心血管疾患の増大、ハイブリッドペットおよびSPECTイメージングシステムの導入の増加が期待されています。 病院およびイメージングセンターは、早期疾患の検出と精密治療計画のための近代的な診断技術に投資しています。 ヘルスケアのモダナイゼーション、AI-assisted Imagingの統合およびローカル製造能力を促進する政府の取り組みは市場成長を加速しています。 手頃な価格の核医学機器の可用性を拡大し、臨床医や患者の間で認知度が高まっています。都市と半都市の領域を横断して採用を促進しています。

インド 核医学機器市場 洞察

インドの核医学装置市場は、病院を拡大し、診断センターの数を増加させ、癌および心疾患の蔓延を高めることによって運転される強い成長を目撃しています。 早期病態検知・治療計画にハイブリッドPETやSPECTシステムを採用。 スマートな病院およびヘルスケアのインフラの近代化サポート市場の成長を促進する政府の取り組み。 費用対効果の高い機器の可用性と、都市および階層2都市におけるヘルスケアプロバイダーのさらなる燃料導入に対する意識の増加。 また、公立病院と私立病院の腫瘍学および心臓学部門の需要の増加は、市場拡大を強化します。

オーストラリア 核医学機器市場 洞察

オーストラリアの核医学装置市場は高度のヘルスケアのインフラ、雑種のペットおよびSPECTシステムの高い採用による安定した成長を経験し、腫瘍学および心臓学の診断に焦点を合わせます。 病院やイメージングセンターでは、早期疾患の検出と精密治療を強調しています。 政府の資金調達、民間医療投資、AI支援画像技術の統合は、採用を推進しています。 最先端の診断サービスのための国の強い医学の観光セクターそして要求は市場拡大を支えます。 ハイブリッドイメージングのメリットや、病院の能力を高めることで、安定した市場成長に貢献します。

アジア・太平洋核医学機器市場シェア

アジア・パシフィックの核医療機器業界は、主に、以下を含む老舗の企業によって導かれています。

- GEヘルスケア(英国)

- Siemens Healthineers AG(ドイツ)

- Koninklijke Philips N.V. (オランダ)

- キャノンメディカルシステムズ株式会社(日本)

- カリウムファーマ(フランス)

- Telix Pharmaceuticals(オーストラリア)

- 中国イソトープ&放射線株式会社(中国)

- ノルディオン株式会社(カナダ)

- NTP.(南アフリカ)

- ジュビラント・ラジオファーマ(インド)

- AdvanCell(オーストラリア)

- シンセンMindrayの生物医学の電子工学Co.、株式会社(中国)

- 原子力エネルギー研究所(台湾)

- 江蘇Huayiの技術Co.、株式会社(中国)

- 浙江Jiutaiの新しい薬剤Co.、株式会社(中国)

- シクロファーマ研究所(フランス)

- 株式会社メディソ(ハンガリー)

- Neusoftの医療機器Co.、株式会社(中国)

アジア・パシフィック原子力医療機器市場における最近の発展とは?

- 2025年8月、エスコライフサイエンスグループは、第6回マレーシア核医学年次会議(MNMAC 2025)に参加しました。 核医学における安全・コンプライアンス・技術革新を強調し、制御環境の先進的なシステムを導入。 Escoの関与は、マレーシアでの核医学の成長と発展を支援するというコミットメントを強調しています

- 2025年6月、AIIMS Raipurは、先進の核医学インフラを確立するために、ハティスガーの唯一の政府病院になりました。 PSMA、DOTA、FAPI、Exendin PETなどの次世代ペット用ラジオトレーサの製造を可能にし、自動ラジオシンセサイザーとガリウムジェネレータを設置しました。 この開発は、診断精度を高め、パーソナライズされた治療戦略をサポートし、外部サプライヤーの信頼性を低下させ、治療の意思決定を迅速化し、患者のスループットを増加させます。

- 国際原子エネルギー機関(IAEA)は、2025年6月、アジア・太平洋地域における先進国を支援し、核医学や放射線療法サービスへのアクセスを拡大する戦略的資金文書を開発する初のワークショップを開催しました。 この取り組みは、核医学技術を統合する総合がんケアプログラムの確立を促進し、地域におけるがんの増大の負担を解決することを目指しています。

- 住友商事は、2025年4月、日本とアジア諸国の融合型医療用同位体を配布する新技術との戦略的パートナーシップを締結しました。 このコラボレーションは、医療用同位体のための安定したサプライチェーンを確立し、原子力医療診断と治療に欠かせない放射線薬学の可用性を高めることを目指しています。 パートナーシップは、事業ポートフォリオ全体を網羅する初の総合コラボレーションです。

- 2025年2月、WORK Medical Technology Group Ltd.は、上海Chartwell Medical Device Co., Ltd.と2025年2月に戦略的パートナーシップを締結しました。 本アライアンスは、核医学・イメージング・リハビリテーション技術の高度化に注力しています。 共同投資、先進技術の共同開発、国際市場への進出、核医学機器のアクセシビリティと品質の向上を目指した協業

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。