アジア・パシフィック・ポリイミド映画市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

1.69 Billion

USD

3.16 Billion

2024

2032

USD

1.69 Billion

USD

3.16 Billion

2024

2032

| 2025 –2032 | |

| USD 1.69 Billion | |

| USD 3.16 Billion | |

| % | |

|

アジアパシフィックポリイミドフィルム市場セグメンテーション、原材料(Pyromellitic Dianhydride(PMDA)、4,4'-Oxydianiline(ODA)、Biphenyl-Tetracarboxylic酸Dianhydride(BPDA)、Phenylenediamine(PDA))、フィルム厚さ(0.5ミル、1ミル、2ミル、3ミル、5ミル、その他)、カラー(Amber、ホワイトケーブル、その他)、特殊鋼材、特殊鋼材、特殊鋼材、特殊鋼材、特殊鋼材、その他

アジアパシフィックポリイミドフィルム市場規模

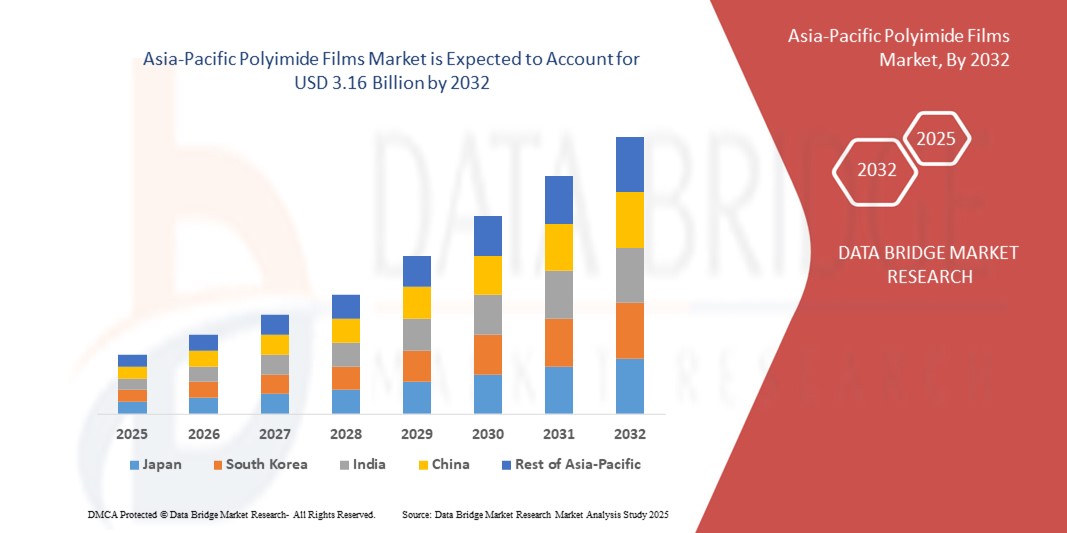

- アジアパシフィックポリイミドフィルム市場規模が評価されました2024年のUSD 1.69億そして到達する予定2032年までのUSD 3.16億, お問い合わせ8.10%のCAGR予報期間中

- 市場成長は、電子機器、自動車、航空宇宙、フレキシブルディスプレイなどの主要業界を横断し、軽量、耐久性、高性能材料の需要が高まっています。

- フレキシブルプリント基板、断熱材、ウェアラブルエレクトロニクスのポリイミドフィルムの採用拡大が更に市場拡大に貢献

アジアパシフィックポリイミドフィルム市場分析

- アジア・パシフィック・ポリイミド・フィルム・マーケットは、エレクトロニクス製造ハブの普及に伴い、特に中国、日本、韓国、台湾などの国々で、半導体やコンシューマー・エレクトロニクスのグローバルリーダーとして活躍しています。

- 電気自動車や再生可能エネルギープロジェクトに対する成長したシフトは、次世代技術の重要な要素として、耐熱性と信頼性の高い断熱材の必要性を強化し、ポリイミドフィルムを位置づける

- 中国は、2024年に46.23%の世界最大の収益シェアを持つアジア太平洋ポリイミドフィルム市場を支配し、強力な電子機器製造エコシステム、電気自動車の急速な採用、および高度な断熱材の需要の増加

- 日本は、最も高い化合物の年間成長率(CAGR)を目撃する見込みアジアパシフィックポリイミドフィルム高性能材料の継続的な革新、航空宇宙および自動車分野からの需要の増加、およびエネルギー効率性技術の焦点の増加による市場

- PMDA セグメントは、2024 年に最大の市場収益シェアを保有し、高性能ポリイミドフィルムを優れた熱・機械的特性で生産しています。 電子および自動車適用を渡るその広範な採用は優位の市場の位置を補強します

レポートスコープとアジア太平洋ポリイミドフィルム市場セグメンテーション

| アトリビュート | アジア・パシフィック・ポリイミド・フィルム・キー・マーケット・インサイト |

| カバーされる区分 |

|

| カバーされた国 | アジアパシフィック

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、データブリッジ市場調査によってキュレーションされた市場レポートには、インポートエクスポート分析、生産能力概要、生産消費分析、価格推移分析、気候変動シナリオ、サプライチェーン分析、バリューチェーン分析、バリューチェーン分析、原材料/消耗品概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークなどがあります。 |

アジアパシフィックポリイミドフィルム市場動向

フレキシブルエレクトロニクスとウェアラブルデバイスの開発

- フレキシブルエレクトロニクスの需要増加は、優れた熱安定性、機械的強度、誘電特性を提供するため、アジア太平洋のポリイミドフィルム市場を再構築しています。 ディスプレイ、折りたたみ式デバイス、ウェアラブルでの使用は、小型化と軽量の製品開発をサポートしています。 これにより、設計の柔軟性を高め、消費者の電子機器間でイノベーションを加速

- 中国、韓国、日本などの市場でウェアラブルデバイスや折り畳み式スマートフォンの普及が高まっています。 製造業者は従来のガラスを取り替える透明で、無色のポリイミドのフィルムを採用し、耐久性および高い光学明快さを保障します。 次世代デバイス製造において特に重要である

- ポリイミドのフィルムの費用効果が大きい、拡張性および信頼性は適用範囲が広い回路およびマイクロエレクトロニクスの大規模な生産のためにそれらに魅力的にします。 高周波信号伝送とコンパクトな回路基板の適合性により、電子機器や半導体産業の需要が高まります。

- たとえば、2023年に、中国の大手スマートフォンブランドは、透明なポリイミドフィルムを組み込み、スクリーンの耐久性と柔軟性を高めました。 次世代コンシューマーエレクトロニクスの選定に重点を置いた材料の役割を強化

- フレキシブルな電子機器は主要なドライバーですが、トレンドの成功は、フィルム加工、ローカライズされたサプライチェーン機能、そして地域における新興経済の高騰に対応するコスト最適化の継続的な進歩に依存しています。

アジア・パシフィック・ポリイミド・フィルム・マーケット・ダイナミクス

ドライバー

電気自動車や航空宇宙用途での需要拡大

- アジア・パシフィックの電気自動車(EV)の生産におけるサージは、ポリイミドフィルムなどの高性能絶縁材料の必要性を大幅に促進しています。 電池の絶縁材、モーター巻上げおよび適用範囲が広いプリント回路の彼らの適用はEVsの安全、信頼性および改善されたエネルギー効率を保障します。 EVの採用が中国、日本、韓国を横断するにつれて、耐久性および軽量材料の需要は上昇し続けます

- 航空宇宙メーカーは、極端な条件に対する優れた耐性のために、配線断熱、軽量部品、および熱管理システムのポリイミドフィルムを採用しています。 これらの特性は、より安全で燃費効率の高い航空機の設計を可能にし、商業および防衛航空の成長した投資と一直線に合わせます。 航空宇宙の信頼性における材料の実績は、グローバルサプライチェーンにおける採用を強化しています。

- EV導入と航空成長を支える政府政策が、需要基盤を強化する。 補助金、規制基準、排出削減目標などのインセンティブは、メーカーが先進材料を採用することを奨励します。 これらの企業のポリイミドのフィルムの統合は証明された耐久性、高温抵抗および国際的な安全基準に従うことによって支えられます

- たとえば、2022年に、日本のEV部門は、蓄電池モジュールの断熱材のポリイミドフィルムの採用増加を報告し、高容量リチウムイオン電池の安全性と拡張性能の両方を確保しました。 この傾向は、次世代モビリティの安全と効率の要件を満たすポリイミドの役割で成長する信頼を反映しています。 地域産業が先進的な断熱ソリューションの初期採用者になる方法の例

- EVと航空宇宙の需要が強く増加する一方で、一貫したイノベーション、生産のスケーラビリティ、およびコストの削減は、多様なアプリケーション間でこれらの機会を十分に活用するために不可欠です。 メーカーは、費用対効果の高い処理方法を開発し、生産能力を拡大し、ローカライズされた材料の可用性を保証します。 戦略的パートナーシップは、これらの課題に対処する上で重要な役割を果たし、持続的な成長を支援します

拘束/チャレンジ

原材料の高生産コストとサプライチェーンの依存性

- 複雑な処理方法および高度装置の条件によって運転される製造のpolyimideのフィルムの高い費用は、小さく、中型の製造業者のための障壁をおおいます。 これは、価格に敏感なアプリケーションで低コストの代替品に対して材料より少ない競争をします。 その結果、パッケージングや消費者向け商品など、より幅広い業界における市場採用が制限されています

- 芳香族ジアンヒドおよびジアミンを含む専門にされた原料の依存は、アジア太平洋のサプライチェーンの危険を作成します。 特定の国における価格のボラティリティと限られた国内生産能力は、調達課題に加え、長期的なコスト安定性に影響を及ぼします。 輸入に関するこの信頼性は、グローバル取引の変動と規制の障壁に対する脆弱性も増加します

- 市場成長は生産のスケーラビリティの問題によってさらに妨げられ、大量の一貫性のある品質を実現するためには、高度な技術と専門知識が必要です。 すべての地域の選手は、生産ボトルネックにつながる製品性能の均一性を達成するために技術的なノウハウを持っています。 これらの課題は、確立されたグローバルサプライヤーと効果的に競合する中小企業を防ぐ

- 例えば、2023年、東南アジアのいくつかの電子機器メーカーは、ポリイミドフィルム製造に必要な原材料の不足による遅延やコストの増加を報告し、サプライチェーンレジリエンスの脆弱性を強調した。 このような混乱は、配送のタイムラインに影響を与え、コストリーなインポートに対する依存性を高め、イノベーションサイクルを妨げます。 これらの要因は、成長需要のペースを維持するために、地域の企業の能力を制限します

- ポリイミドフィルムは、プロセス革新、ローカライズされた材料調達、技術投資を通じて、膨大なコストと供給の課題を克服する可能性を秘めていますが、アジア太平洋地域におけるより広い採用を解除することが不可欠です。 リサイクルソリューションを開発し、代替原料源もリスクを減らすことができます。 政府と民間部門のコラボレーションは、これらのハードルに効果的に取り組む上で不可欠です

アジアパシフィックポリイミドフィルム市場スコープ

市場は原料、フィルムの厚さ、色、配分チャネル、適用およびエンド ユーザーの基礎で分けられます。

- 原料から探す

原材料をベースに、アジア・パシフィック・ポリイミド・フィルム市場は、ピロムリスティック・ディアンヒド(PMDA)、4,4’-オキシディアニリン(ODA)、バイフェニル・テトラカルボキシル酸ジアンヒド(BPDA)、フェニレンジアミン(PDA)に分けられます。 PMDA セグメントは、2024 年に最大の市場収益シェアを保有し、高性能ポリイミドフィルムを優れた熱・機械的特性で生産しています。 電子機器や自動車用途の幅広い採用により、優位性のある市場位置が向上します。

BPDAの区分は高められた次元安定性、化学抵抗およびより低い湿気の吸収とフィルムを渡す機能によって運転される2025から2032までの最も速い成長率を目撃するために期待されます。 これらの特性は、長期的な信頼性と耐久性が重要である航空宇宙、太陽光、およびフレキシブルプリント回路などの要求用途で、BPDAベースのポリイミドフィルムをますますます人気を上げます。

- フィルムの厚さによって

フィルムの厚さに基づいて、市場は0.5ミル、1ミル、2ミル、3ミル、5ミル、その他に分けられます。 2024年に最大の収益シェアを占める1つのミルセグメントは、柔軟性、断熱性、耐久性の最適なバランスを提供し、電子機器、フレキシブルプリント回路、およびワイヤ絶縁で広く使用されている。 汎用性の高い特性は、消費者用電子機器および産業用アプリケーションにおける優位性をサポートします。

超薄型・小型化機器の適合性により、2025~2032年最速成長率を目撃する0.5ミルセグメントが期待されています。 コンパクトな電子機器や軽量自動車用部品に対する需要が高まっています。先進的な回路基板、センサー、電池部品に薄膜を採用し、地域を横断して高い取組を加速しています。

- 色によって

色に基づいて、市場はアンバー、白、透明、その他に分けられます。 アンバーセグメントは、電子機器、航空宇宙、および高温への耐久性と耐性が重要である自動車用途の広範な使用により、2024年に最大の市場収益シェアを保持しました。 複数の業界に実績のある性能で、市場需要が高まります。

透明セグメントは、2025年から2032年までの最速成長率を目撃する見込みで、回路やコンポーネントの検査や監視が容易になります。 このプロパティは、フレキシブルディスプレイ、光電子デバイス、およびソーラーアプリケーションでますます価値が高まっています。高度な製造業界を横断して採用しています。

- 流通チャネル

流通チャネルに基づき、市場は電子商取引、専門店、その他に分けられます。 専門店は顧客が品質保証、カスタマイズされた解決およびテクニカル サポートのための公認のディストリビューターからの直接購入を好むので2024年に市場を支配します。 産業用バイヤーとの強い関係は、このチャネルのリーダーシップを強化します。

eコマースセグメントは、2025年から2032年までの最速成長率を目撃する見込みで、調達プロセスの高度化とオンライン購入の利便性によって燃料を供給しました。 特殊なB2Bプラットフォームでポリイミドフィルムの可用性を高めることで、小型・中規模の企業を横断してこのチャネルの迅速な採用を支援しています。

- 用途別

適用に基づいて、市場は適用範囲が広いプリント回路、専門によって製造されるプロダクト、圧力敏感なテープ、ワイヤーおよびケーブル、モーター/発電機、絶縁材の毛布、管の絶縁材、管の絶縁材、エッチング、リチウム イオン電池の細胞/pouchの覆い、陶磁器の板取り替え、熱的に伝導性の屈曲回路、光沢および他のに分けられます。 フレキシブルなプリント回路は、フレキシブル、耐久性、耐熱性の電子機器製造における多層フィルムの広範な採用によって駆動され、2024年に最大の収益分配のために考慮しました。

リチウムイオン電池セル/ポーチラップセグメントは、2025年から2032年までの最速成長率を目撃する見込みで、電気自動車や再生可能エネルギー貯蔵システムの急速な拡大によって燃料を供給しました。 Polyimideのフィルムは高められた性能、安全および延長ライフサイクルを保障します電池の優秀な絶縁材そして熱安定性を提供します。

- エンドユーザーによる

エンド ユーザーに基づいて、市場は電子工学、自動車、大気および宇宙空間、太陽、医学、採鉱および訓練、建物および構造、分類し、化学処理、プラスチックおよび包装、産業、エネルギーおよび他のに分けられます。 電子セグメントは、スマートフォン、タブレット、半導体、およびフレキシブルディスプレイでポリイミドフィルムが広く使用されているため、2024年に市場を支配しました。

自動車分野は、2025年から2032年にかけて最も速い成長率を目撃する見込みで、アジア太平洋地域における電気自動車生産のサージによって支えられています。 EV電池、モーター絶縁材および適用範囲が広い回路の適用は地域ポリイミドのフィルムの市場のための主要な成長の運転者として自動車セクターを確立する重要な採用を運転しています。

アジア・パシフィック・ポリイミド・フィルム市場地域分析

- 中国は、2024年に46.23%の世界最大の収益シェアを持つアジア太平洋ポリイミドフィルム市場を支配し、強力な電子機器製造エコシステム、電気自動車の急速な採用、および高度な断熱材の需要の増加

- 半導体、電池、および適用範囲が広い電子工学の国の大規模な生産は優秀な熱安定性および信頼性のために評価されるpolyimideのフィルムのための一貫した要求を作成します、

- この優位性は、再生可能エネルギー、自動車技術の進歩、航空宇宙における継続的な投資を促進するために重要な政府の取り組みによってさらに支持され、中国の地域の市場における継続的なリーダーシップを確保

日本ポリイミドフィルム市場動向

日本ポリイミドフィルム市場は、2025年から2032年までのアジア太平洋で最速の成長を目撃する見込みで、電気自動車技術の進歩と高性能電子機器の国の強い存在によって燃料を供給しました。 ポリイミドフィルムをリチウムイオン電池絶縁、軽量航空宇宙部品、次世代回路用途に統合しています。 市場は、日本のイノベーション、厳格な品質基準、持続可能な技術の採用に重点を置いています。 また、防衛、再生可能エネルギー、および消費者向け電子機器の製造における継続的な投資は、日本を地域で最速成長市場として位置付け、ポリイミドフィルムの需要を加速しています。

アジア太平洋ポリイミドフィルム市場シェア

アジア・パシフィック・ポリイミド・フィルム業界は、主に、以下の分野を含む、老舗企業によって導かれています。

- 株式会社カネカ(日本)

- 株式会社宇部工業(日本)

- SKCコロンPI(韓国)

- デュポン帝人映画(中国)

- 住友化学(日本)

- 株式会社タイミドテック(台湾)

- ユンダ電子材料有限公司(中国)

- Loparex(中国)

- Jingyiのフィルム材料Co.、株式会社(中国)

- Shengyuanグループ(中国)

- 日東デンコ(中国)有限公司(中国)

- フォルモサプラスチックス株式会社(台湾)

- サビック(サウジアラビア)

- 昭和電工株式会社(日本)

アジア太平洋ポリイミドフィルム市場の最新動向

- 2020年11月には、超耐熱ポリイミドフィルム「Pixeo IB」を高速・高周波数5G向けに開発しました。 2021年10月にサンプルを発売し、本格的なロールアウトを予定。 「Pixeo IB」は、高周波数の誘電損失を0.0025に低減し、ポリイミドフィルムのグローバル最高レベル

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。