アジア太平洋地域の SiC パワー半導体市場、タイプ別 (MOSFET、ハイブリッド モジュール、ショットキー バリア ダイオード (SBDS)、IGBT、バイポーラ接合トランジスタ (BJT)、ピン ダイオード、接合 FET (JFET)、その他)、電圧範囲 (301~900 V、901~1700 V、1701 V 以上)、ウェハー サイズ (6 インチ、4 インチ、2 インチ、6 インチ以上)、ウェハー タイプ (SiC エピタキシャル ウェハー、ブランクSiC ウェハー)、アプリケーション (電気自動車 (EV)、太陽光発電、電源、産業用モーター ドライブ、EV 充電インフラストラクチャ、RF デバイス、その他)、垂直 (自動車、公共事業およびエネルギー、産業、輸送、IT および通信、民生用電子機器、航空宇宙および防衛、商業、その他) の 2030 年までの業界動向と予測。

アジア太平洋地域のSiCパワー半導体市場の分析と規模

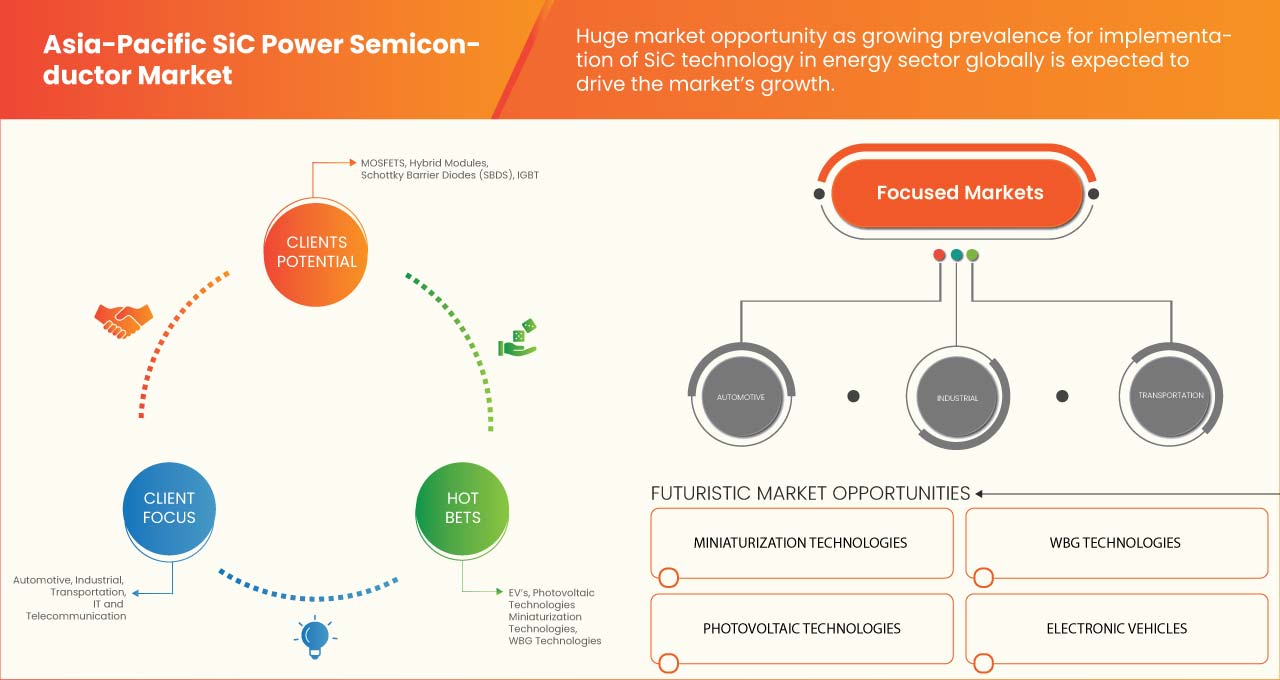

SiCパワー半導体は最も普及している半導体であり、電子機器に最適な選択肢と考えられています。これらのSiCパワー半導体は、家庭、商業、産業部門、およびその他のさまざまな分野に適用されています。SiCパワー半導体には、SiCディスクリートデバイスとSiCベアダイの2種類のデバイスがあります。技術の進歩により、SiCディスクリートデバイスの普及は急速に進んでいます。SiCパワー半導体の重要な特性は、電気を効率的に使用するさまざまな特性とともに、高い熱伝導性です。SiCパワー半導体は、通信、エネルギーと電力、再生可能発電、およびその他のさまざまな場所で使用されています。SiCパワー半導体は、個人の間で普及しつつあるパワーエレクトロニクスで使用されています。アジア太平洋のSiCパワー半導体市場におけるSiCパワー半導体の需要は、より高い割合で増加しています。このため、さまざまな市場プレーヤーが新製品を導入し、アジア太平洋のSiCパワー半導体市場でのビジネスを拡大するためのパートナーシップを形成しています。

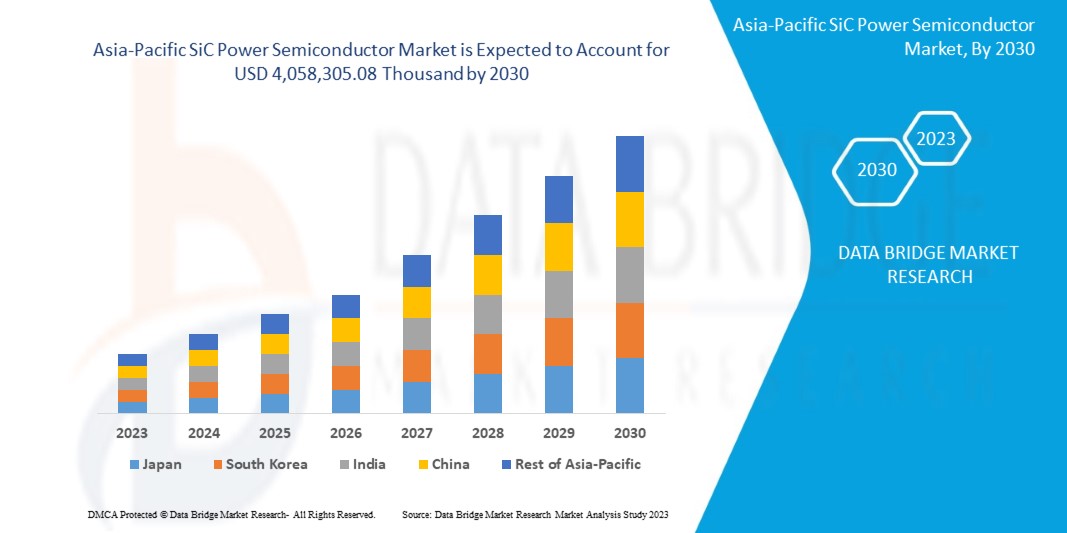

データブリッジマーケットリサーチは、アジア太平洋地域のSiCパワー半導体市場は、予測期間中に25.9%のCAGRで成長し、2030年までに4,058,305.08米ドルに達すると予測しています。アジア太平洋地域のSiCパワー半導体市場レポートでは、価格分析、特許分析、技術進歩についても包括的に取り上げています。

|

レポートメトリック |

詳細 |

|

予測期間 |

2023年から2030年 |

|

基準年 |

2022 |

|

歴史的な年 |

2021 (2020~2016年にカスタマイズ可能) |

|

定量単位 |

売上高は千米ドル、販売数量は個数、価格は米ドル |

|

対象セグメント |

タイプ別 (MOSFET、ハイブリッド モジュール、ショットキー バリア ダイオード (SBDS)、IGBT、バイポーラ接合トランジスタ (BJT)、ピン ダイオード、接合 FET (JFET)、その他)、電圧範囲別 (301 ~ 900 V、901 ~ 1700 V、1701 V 以上)、ウェハー サイズ別 (6 インチ、4 インチ、2 インチ、6 インチ以上)、ウェハー タイプ別 (SiC エピタキシャル ウェハー、ブランク SiC ウェハー)、アプリケーション別 (電気自動車 (EV)、太陽光発電、電源、産業用モーター ドライブ、EV 充電インフラストラクチャ、RF デバイス、その他)、垂直分野別 (自動車、公共事業およびエネルギー、産業、輸送、IT および通信、民生用電子機器、航空宇宙および防衛、商業、その他)。 |

|

対象国 |

日本、中国、韓国、インド、オーストラリア、ニュージーランド、香港、台湾、シンガポール、タイ、インドネシア、マレーシア、フィリピン、ベトナム、その他のアジア太平洋地域。 |

|

対象となる市場プレーヤー |

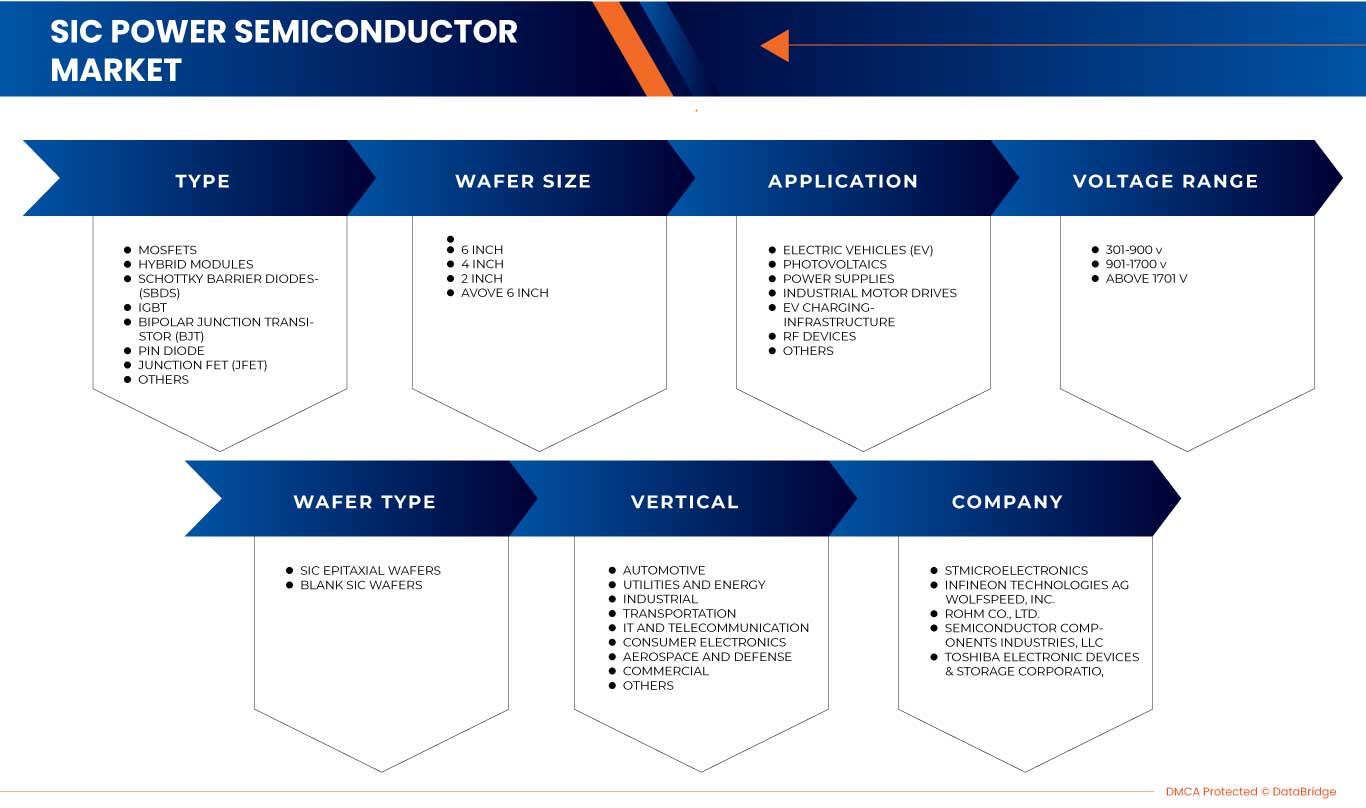

WOLFSPEED, INC.、STMicroelectronics、ローム株式会社、富士電機株式会社、三菱電機株式会社、Texas Instruments Incorporated、Infineon Technologies AG、Semikron Danfoss、厦門電力威先進材料有限公司、ルネサス エレクトロニクス株式会社、東芝デバイス&ストレージ株式会社、Microchip Technology Inc.、Semiconductor Components Industries, LLC、NXP Semiconductors、UnitedSiC、SemiQ Inc.、Littlefuse, Inc.、Allegro MicroSystems, Inc.、日立パワーデバイス株式会社(日立グループ子会社)、GeneSiC Semiconductor Inc. 他 |

市場の定義

SiC パワー半導体とは、炭素とシリコンを含み、非常に高い電圧と温度で動作する半導体の一種です。SiC パワー半導体は、強度と硬度に優れた材料の製造に使用できます。SiC パワー半導体は、通信、エネルギーと電力、自動車、再生可能発電など、さまざまな分野で実装できます。基本的に、最大熱伝導率が高く、応用範囲が広がるためと考えられています。SiC パワー半導体は、主に無線通信に適用できる高周波パワーデバイスと見なされるデバイスです。SiC 半導体は、シリコン半導体に比べて、絶縁破壊電界強度が 10 倍、熱伝導率が 3 倍、バンドギャップが 3 倍です。SiC 半導体は、その高性能と効率性から市場を席巻しています。SiC パワー半導体は、高電圧と高電流で動作し、高温でも効率的であるだけでなく、オン抵抗も低くなっています。したがって、シリコンカーバイドとの組み合わせは、半導体のより優れた最適な選択肢であることが証明されています。

アジア太平洋地域のSiCパワー半導体市場の動向

このセクションでは、市場の推進要因、利点、機会、制約、課題について理解します。これらについては、以下で詳しく説明します。

ドライバー

- SiCパワー半導体の登場

There are very useful properties of SiC as a semiconductor material. In applications such as inverters, motor drives, and battery chargers, silicon carbide (SiC) devices offer many advantages, such as improved power density, reduced cooling requirements, and reduced overall system cost. These advantages are enough to make SiC power semiconductors at the high efficient stage.

The energy lost by SiC during the reverse recovery phase is only 1% of the energy lost by silicon which creates a huge difference in the efficiency of the material. The virtual absence of a tail current allows a faster turn‑off, and it makes lower losses. Since there is less energy to dissipate, a SiC device able to switch at higher frequencies and improve efficiency. The more efficient, small size, and lower weight of SiC as compared to other materials can create a higher-rated solution or a smaller design with reduced cooling requirements. Thus, the advent of SiC power semiconductors is a major factor expected to drive the growth of the Asia-Pacific SiC power semiconductor market.

- Rising Penetration of Electronic Vehicles

The world is changing so fast, and it is turning towards renewable energy. All sectors, market players, and government institutes are making more focus to build electric vehicle infrastructure and generate more demand for electric vehicles.

As per the information from International Energy Agency (IEA), 16.5 million electric cars were on the road in 2021, a tripling in just three years, and this is a big number as compared to 2020. Electric car sales increased and doubled in China, continued to increase in Europe, and picked up in the U.S. in 2021. This data shows that there is a tremendous increase in the penetration of EVs in the market, which may positively affect the environment as well as the Asia-Pacific SiC power semiconductor market. SiC is highly efficient at high voltages, enabling fast battery charging times that are comparable to filling the tank of conventional vehicles. Silicon carbide power electronics are enabling a surge in 800-volt drive systems, paving the way for lighter EVs with greater range.

Opportunity

- Strategic Partnership and Acquisition by SiC Manufacturers

There are various organizations and market players which are creating strategic partnerships and acquisitions. This partnership creates a huge positive impact on the growth of the Asia-Pacific SiC power semiconductor market. This collaboration results in cooperation, becoming a low-cost route for new competitors to gain technology and market access.

A joint venture involves two or more businesses pooling their resources and expertise to achieve a particular goal. There are many organizations that collaborate with each other's and create a positive impact on the growth of the Asia-Pacific SiC power semiconductor market.

Restraint/Challenge

- Issues Related With SiC Wafer Manufacturing

A SiC wafer is a semiconductor material that has excellent electrical and thermal properties. It is a high-performance semiconductor that is ideal for a wide variety of applications. In addition to its high thermal resistance, it also features a very high level of hardness. There is a lot of fabrication challenge faced by SiC wafer manufacturers. The main defects that can occur during the manufacturing of SiC substrates are crystalline stacking faults, micro pipes, pits, scratches, stains, and surface particles. These factors are adversely affecting the performance of SiC devices which have been detected more frequently on 150-mm wafers than on 100-mm wafers. This is because SiC is the third-hardest composite material in the world and is also very fragile, and its production poses complex challenges related to cycle time, cost, and dicing performance. It is effective to predict that even switching to 200-mm wafers will entail significant issues. In fact, it will be necessary to guarantee the same quality of the substrate, facing an inevitably higher density of defects.

Post-COVID-19 Impact on Asia-Pacific SiC Power Semiconductor Market

The SiC power semiconductor industry noted a gradual decrease in demand due to the lockdown and COVID-19 governmental laws, as manufacturing facilities and services were closed. Even private and public development was called off. Moreover, the industry was also affected by the halt of the supply chain, especially of raw materials used in the manufacturing process of SiC power semiconductors. Stringent government regulations for different industries and restrictions on trade & transportation were some of the top factors that caused a dent in the growth of the market for SiC power semiconductors around the world in 2020 and in the first two quarters of 2021. As the SiC power semiconductor production slowed down owing to the restrictions by governments across the globe, the production was not meeting the demand in the first three quarters of 2020. Moreover, high demand/requirement for SiC power semiconductor products in the automotive and defense industry, in the medical sector, and in hydraulics applications has been witnessed. The resumption of production of the oil and gas industry and automotive; further fuelled the rising demand for SiC power semiconductors across the globe. Thus, this not only led to a hike in demand but also increased the cost of the product.

Recent Developments

- In December 2022, STMicroelectronics and Soitec (Euronext Paris), in designing and manufacturing innovative semiconductor materials, announced the next stage of their cooperation on Silicon Carbide (SiC) substrates, with the qualification of Soitec's SiC substrate technology by ST planned over the next 18 months. The goal of this cooperation is the adoption by ST of Soitec's SmartSiC technology for its future 200mm substrate manufacturing, feeding its devices and modules manufacturing business, with volume production expected in the midterm. This collaboration will help the company to boost its financials as well as the growth of the Asia-Pacific SiC power semiconductor market.

- In July 2022, Semikron Danfoss and the Kyoto-based company ROHM Semiconductor have been collaborating for more than ten years with regard to the implementation of silicon carbide (SiC) inside power modules. Recently, ROHM's latest 4th generation of SiC MOSFETs has been fully qualified in SEMIKRON's eMPack modules for automotive use. Hence, both companies serve worldwide customers' needs. This collaboration enhanced the company's financials and made a positive impact on the growth of the Asia-Pacific SiC power semiconductor market.

Asia-Pacific SiC Power Semiconductor Market Scope

The Asia-Pacific SiC power semiconductor market is segmented on the basis of type, voltage range, wafer size, wafer type, application, and vertical. The growth amongst these segments will help you analyze meager growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

By Type

- MOSFETS

- Hybrid Modules

- Schottky Barrier Diodes (SBDS)

- IGBT

- Bipolar Junction Transistor (BJT)

- Pin Diode

- Junction FET (JFET)

- Others

On the basis of type, the Asia-Pacific SiC power semiconductor market is segmented into MOSFETS, Hybrid Modules, Schottky Barrier Diodes (SBDS), IGBT, Bipolar Junction Transistor (BJT), Pin Diode, Junction FET (JFET) and others.

By Voltage Range

- 301-900 V

- 901-1700 V

- Above 1701 V

On the basis of voltage range, the Asia-Pacific SiC power semiconductor market is segmented into 301-900 V, 901-1700 V, and above 1701 V.

By Wafer Size

- 6 Inch

- 4 Inch

- 2 Inch

- Above 6 Inch

On the basis of wafer size, the Asia-Pacific SiC power semiconductor market is segmented into 6 Inch, 4 Inch, 2 Inch, and above 6 Inch.

By Wafer Type

- SiC epitaxial wafers

- Blank SiC wafers

On the basis of the wafer type, the Asia-Pacific SiC power semiconductor market is segmented into SiC epitaxial wafers and blank SiC wafers.

By Application

- Electric Vehicles (EV)

- Photovoltaics

- Power supplies

- Industrial motor drives

- EV charging infrastructure

- RF Devices

- Others

On the basis of the application, the Asia-Pacific sic power semiconductor market is segmented into electric vehicles (EV), photovoltaics, power supplies, industrial motor drives, EV charging infrastructure, RF devices, and others.

By Vertical

- Automotive

- Utilities and energy

- Industrial

- Transportation

- IT and telecommunication

- Consumer electronics

- Aerospace and defense

- Commercial

- Others

On the basis of the vertical, the Asia-Pacific SiC power semiconductor market is segmented into automotive, utilities and energy, industrial, transportation, IT and telecommunication, consumer electronics, aerospace and defense, commercial, and others.

Asia-Pacific SiC Power Semiconductor Market Regional Analysis/Insights

The Asia-Pacific SiC power semiconductor market is analyzed, and market size insights and trends are provided by region, type, voltage range, wafer size, wafer type, application, and vertical as referenced above.

The countries covered in the Asia-Pacific SiC power semiconductor market report are Japan, China, South Korea, India, Australia and New Zealand, Hong Kong, Taiwan, Singapore, Thailand, Indonesia, Malaysia, Philippines, Vietnam, and Rest of Asia-Pacific.

In 2023, China is expected to dominate the Asia-Pacific SiC power semiconductor market due to the size of its domestic electronics market and its status as a production base for entire industries is expected to act as a driving factor for the growth of the market.

The region section of the report also provides individual market-impacting factors and changes in market regulation that impact the current and future trends of the market. Data points like downstream and upstream value chain analysis, technical trends, and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of Asia-Pacific brands and their challenges faced due to large or scarce competition from local and domestic brands, the impact of domestic tariffs, and trade routes are considered while providing forecast analysis of the region data.

Competitive Landscape and Asia-Pacific SiC power semiconductor Market Share Analysis

Asia-Pacific SiC power semiconductor Market competitive landscape provides details by the competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, Asia-Pacific presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, and application dominance. The above data points provided are only related to the companies' focus related to the Asia-Pacific SiC power semiconductor Market.

アジア太平洋地域の SiC パワー半導体市場で活動している主要企業としては、WOLFSPEED、STMicroelectronics、ローム株式会社、富士電機株式会社、三菱電機株式会社、Texas Instruments Incorporated、インフィニオン テクノロジーズ AG、セミクロン ダンフォス、厦門電力威先進材料有限公司、ルネサス エレクトロニクス株式会社、東芝デバイス&ストレージ株式会社、Microchip Technology Inc.、Semiconductor Components Industries, LLC、NXP Semiconductors、UnitedSiC、SemiQ Inc.、Littlefuse, Inc.、Allegro MicroSystems, Inc.、日立パワーデバイス株式会社(日立グループの子会社)、GeneSiC Semiconductor Inc. などがあります。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

目次

1 はじめに

1.1 研究の目的

1.2 市場の定義

1.3 アジア太平洋地域のSICパワー半導体市場の概要

1.4 通貨と価格

1.5 制限

1.6 対象市場

2 市場セグメンテーション

2.1 対象市場

2.2 研究期間の考慮

2.3 地理的範囲

2.4 DBMR TRIPODデータ検証モデル

2.5 主要なオピニオンリーダーとの一次インタビュー

2.6 DBMR市場ポジショングリッド

2.7 ベンダーシェア分析

2.8 多変量モデリング

2.9 タイプカーブ

2.1 市場アプリケーションカバレッジグリッド

2.11 二次資料

2.12 仮定

3 概要

4つのプレミアムインサイト

5 市場概要

5.1 ドライバー

5.1.1 SiCパワー半導体の登場

5.1.2 電気自動車の普及率の上昇

5.1.3 太陽光発電技術の利用増加

5.1.4 半導体産業の成長

5.1.5 データセンターにおけるWBGパワー半導体の導入増加

5.2 拘束

5.2.1 SiC基板に関連する高コスト

5.3 機会

5.3.1 SICメーカーによる戦略的提携と買収

5.3.2 北米と欧州におけるサプライチェーンの能力の拡大

5.3.3 エネルギー分野におけるSIC技術の導入

5.3.4 半導体市場を活性化するための政府/企業による強力な取り組みと投資。

5.4 課題

5.4.1 SiCウェーハ製造に関する問題

5.4.2 サプライチェーンの混乱によるシリコンカーバイド半導体の不足

6 アジア太平洋地域のSICパワー半導体市場(タイプ別)

6.1 概要

6.2 MOSFET

6.3 ハイブリッドモジュール

6.4 ショットキーバリアダイオード(SBDS)

6.5 IGBT

6.6 バイポーラ接合トランジスタ(BJT)

6.7 ピンダイオード

6.8 接合型FET(JFET)

6.9 その他

7 アジア太平洋地域のSICパワー半導体市場(電圧範囲別)

7.1 概要

7.2 301-900V

7.3 901-1700V

7.4 1701 V 以上

8 アジア太平洋地域のSICパワー半導体市場(ウェハサイズ別)

8.1 概要

8.2 6インチ

8.3 4インチ

8.4 2インチ

8.5 6インチ以上

9 アジア太平洋地域のSICパワー半導体市場(ウェーハタイプ別)

9.1 概要

9.2 SiCエピタキシャルウェーハ

9.3 ブランクSICウェーハ

10 アジア太平洋地域のSICパワー半導体市場(用途別)

10.1 概要

10.2 電気自動車

10.3 太陽光発電

10.4 電源

10.5 産業用モータードライブ

10.6 EV充電インフラ

10.7 RFデバイス

10.8 その他

11 アジア太平洋地域のSICパワー半導体市場(業種別)

11.1 概要

11.2 自動車

11.3 ユーティリティとエネルギー

11.4 工業

11.5 輸送

11.6 ITと通信

11.7 民生用電子機器

11.8 航空宇宙および防衛

11.9 商業

11.1 その他

12 アジア太平洋地域のSICパワー半導体市場(地域別)

12.1 アジア太平洋

12.1.1 中国

12.1.2 日本

12.1.3 韓国

12.1.4 インド

12.1.5 台湾

12.1.6 オーストラリアとニュージーランド

12.1.7 シンガポール

12.1.8 タイ

12.1.9 インドネシア

12.1.10 マレーシア

12.1.11 フィリピン

12.1.12 ベトナム

12.1.13 その他のアジア太平洋地域

13 アジア太平洋地域のSICパワー半導体市場、企業概要

13.1 企業シェア分析: アジア太平洋

14 SWOT分析

15 企業プロフィール

15.1 STマイクロエレクトロニクス

15.1.1 会社概要

15.1.2 収益分析

15.1.3 企業株式分析

15.1.4 製品ポートフォリオ

15.1.5 最近の動向

15.2 インフィニオンテクノロジーズAG

15.2.1 会社概要

15.2.2 収益分析

15.2.3 企業株式分析

15.2.4 製品ポートフォリオ

15.2.5 最近の動向

15.3 ウルフスピード株式会社

15.3.1 会社のスナップショット

15.3.2 収益分析

15.3.3 企業株式分析

15.3.4 製品ポートフォリオ

15.3.5 最近の動向

15.4 ローム株式会社

15.4.1 会社のスナップショット

15.4.2 収益分析

15.4.3 企業株式分析

15.4.4 製品ポートフォリオ

15.4.5 最近の動向

15.5 セミコンダクターコンポーネントインダストリーズLLC

15.5.1 会社のスナップショット

15.5.2 収益分析

15.5.3 企業株式分析

15.5.4 製品ポートフォリオ

15.5.5 最近の動向

15.6 アレグロマイクロシステムズ株式会社

15.6.1 会社のスナップショット

15.6.2 収益分析

15.6.3 企業株式分析

15.6.4 製品ポートフォリオ

15.6.5 最近の動向

15.7 富士電機株式会社

15.7.1 会社のスナップショット

15.7.2 収益分析

15.7.3 製品ポートフォリオ

15.7.4 最近の動向

15.8 ジェネシックセミコンダクター株式会社

15.8.1 会社のスナップショット

15.8.2 製品ポートフォリオ

15.8.3 最近の動向

15.9 日立パワーデバイス株式会社

15.9.1 会社のスナップショット

15.9.2 製品ポートフォリオ

15.9.3 最近の動向

15.1 リトルヒューズ株式会社

15.10.1 会社のスナップショット

15.10.2 収益分析

15.10.3 製品ポートフォリオ

15.10.4 最近の動向

15.11 マイクロチップテクノロジー株式会社

15.11.1 会社のスナップショット

15.11.2 収益分析

15.11.3 製品ポートフォリオ

15.11.4 最近の動向

15.12 三菱電機株式会社

15.12.1 会社のスナップショット

15.12.2 収益分析

15.12.3 製品ポートフォリオ

15.12.4 最近の動向

15.13 NXPセミコンダクター

15.13.1 会社概要

15.13.2 収益分析

15.13.3 デザインポートフォリオ

15.13.4 最近の動向

15.14 ルネサスエレクトロニクス株式会社

15.14.1 会社概要

15.14.2 収益分析

15.14.3 製品ポートフォリオ

15.14.4 最近の動向

15.15 セミクロンダンフォス

15.15.1 会社概要

15.15.2 製品ポートフォリオ

15.15.3 最近の動向

15.16 セミック株式会社

15.16.1 会社概要

15.16.2 製品ポートフォリオ

15.16.3 最近の動向

15.17 テキサスインスツルメンツ株式会社

15.17.1 会社概要

15.17.2 収益分析

15.17.3 製品ポートフォリオ

15.17.4 最近の動向

15.18 東芝デバイス&ストレージ株式会社

15.18.1 会社概要

15.18.2 製品ポートフォリオ

15.18.3 最近の動向

15.19 ユナイテッドシック

15.19.1 会社概要

15.19.2 製品ポートフォリオ

15.19.3 最近の動向

15.2 厦門パワーウェイ先端材料株式会社

15.20.1 会社概要

15.20.2 製品ポートフォリオ

15.20.3 最近の動向

16 アンケート

17 関連レポート

表のリスト

表1 アジア太平洋地域のSICパワー半導体市場、タイプ別、2021年~2030年(千米ドル)

表2 アジア太平洋地域のSiCパワー半導体市場におけるMOSFET、地域別、2021年~2030年(千米ドル)

表3 アジア太平洋地域のSICパワー半導体市場におけるハイブリッドモジュール、地域別、2021年~2030年(千米ドル)

表4 アジア太平洋地域のショットキーバリアダイオード(SBDS)のSICパワー半導体市場、地域別、2021年~2030年(千米ドル)

表5 アジア太平洋地域のIGBT in SICパワー半導体市場、地域別、2021-2030年(千米ドル)

表6 アジア太平洋地域のSICパワー半導体市場におけるバイポーラ接合トランジスタ(BJT)、地域別、2021年~2030年(千米ドル)

表7 アジア太平洋地域のSICパワー半導体市場におけるPINダイオード、地域別、2021年~2030年(千米ドル)

表8 アジア太平洋地域のSICパワー半導体市場における接合FET(JFET)、地域別、2021年~2030年(千米ドル)

表9 アジア太平洋地域のSICパワー半導体市場におけるその他企業、地域別、2021年~2030年(千米ドル)

表10 アジア太平洋地域のSICパワー半導体市場、電圧範囲別、2021年~2030年(千米ドル)

表11 アジア太平洋地域の301-900V SICパワー半導体市場、地域別、2021-2030年(千米ドル)

表12 アジア太平洋地域の901-1700VのSICパワー半導体市場、地域別、2021-2030年(千米ドル)

表13 アジア太平洋地域の1701V以上のSiCパワー半導体市場、地域別、2021年~2030年(千米ドル)

表14 アジア太平洋地域のSICパワー半導体市場、ウェーハサイズ別、2021年~2030年(千米ドル)

表15 アジア太平洋地域の6インチSiCパワー半導体市場、地域別、2021年~2030年(千米ドル)

表16 アジア太平洋地域4インチSiCパワー半導体市場、地域別、2021年~2030年(千米ドル)

表17 アジア太平洋地域2インチSiCパワー半導体市場、地域別、2021年~2030年(千米ドル)

表18 アジア太平洋地域の6インチ以上のSiCパワー半導体市場、地域別、2021年~2030年(千米ドル)

表19 アジア太平洋地域のSICパワー半導体市場、ウェーハタイプ別、2021年~2030年(千米ドル)

表20 アジア太平洋地域のSICパワー半導体市場におけるSICエピタキシャルウェーハ、地域別、2021年~2030年(千米ドル)

表21 アジア太平洋地域のSICパワー半導体市場におけるブランクSICウェーハ、地域別、2021年~2030年(千米ドル)

表22 アジア太平洋地域のSICパワー半導体市場、用途別、2021年~2030年(千米ドル)

表23 アジア太平洋地域の電気自動車(EV)向けSICパワー半導体市場、地域別、2021年~2030年(千米ドル)

表24 アジア太平洋地域の太陽光発電用SiCパワー半導体市場、地域別、2021年~2030年(千米ドル)

表25 アジア太平洋地域のSICパワー半導体市場における電源、地域別、2021年~2030年(千米ドル)

表26 アジア太平洋地域の産業用モータードライブのSICパワー半導体市場、地域別、2021年~2030年(千米ドル)

表27 アジア太平洋地域のEV充電インフラ向けSICパワー半導体市場、地域別、2021年~2030年(千米ドル)

表28 アジア太平洋地域のRFデバイスSICパワー半導体市場、地域別、2021-2030年(千米ドル)

表29 アジア太平洋地域のSICパワー半導体市場におけるその他企業、地域別、2021年~2030年(千米ドル)

表30 アジア太平洋地域のSICパワー半導体市場、業界別、2021年~2030年(千米ドル)

表31 アジア太平洋地域の自動車用SiCパワー半導体市場、地域別、2021年~2030年(千米ドル)

表32 アジア太平洋地域の公益事業およびエネルギー向けSICパワー半導体市場、地域別、2021年~2030年(千米ドル)

表33 アジア太平洋地域の産業用SiCパワー半導体市場、地域別、2021年~2030年(千米ドル)

表34 アジア太平洋地域の輸送用SiCパワー半導体市場、地域別、2021年~2030年(千米ドル)

表35 アジア太平洋地域のITおよび通信向けSICパワー半導体市場、地域別、2021年~2030年(千米ドル)

表36 アジア太平洋地域の民生用電子機器向けSICパワー半導体市場、地域別、2021年~2030年(千米ドル)

表37 アジア太平洋地域の航空宇宙および防衛向けSICパワー半導体市場、地域別、2021年~2030年(千米ドル)

表38 アジア太平洋地域の商業用SICパワー半導体市場、地域別、2021年~2030年(千米ドル)

表 39 アジア太平洋地域の SiC パワー半導体市場におけるその他企業、地域別、2021-2030 年 (千米ドル)

表40 アジア太平洋地域のSICパワー半導体市場、国別、2021年~2030年(千米ドル)

表41 アジア太平洋地域のSICパワー半導体市場、タイプ別、2021年~2030年(千米ドル)

表42 アジア太平洋地域のSICパワー半導体市場、電圧範囲別、2021年~2030年(千米ドル)

表43 アジア太平洋地域のSICパワー半導体市場、ウェーハサイズ別、2021年~2030年(千米ドル)

表44 アジア太平洋地域のSICパワー半導体市場、ウェーハタイプ別、2021年~2030年(千米ドル)

表45 アジア太平洋地域のSICパワー半導体市場、アプリケーション別、2021年~2030年(千米ドル)

表46 アジア太平洋地域のSICパワー半導体市場、業界別、2021年~2030年(千米ドル)

表47 中国SICパワー半導体市場、タイプ別、2021-2030年(千米ドル)

表48 中国SICパワー半導体市場、電圧範囲別、2021-2030年(千米ドル)

表49 中国のSICパワー半導体市場、ウェーハサイズ別、2021年~2030年(千米ドル)

表50 中国SICパワー半導体市場、ウェーハタイプ別、2021-2030年(千米ドル)

表51 中国SICパワー半導体市場、用途別、2021-2030年(千米ドル)

表52 中国SICパワー半導体市場、業種別、2021年~2030年(千米ドル)

表53 日本SICパワー半導体市場、タイプ別、2021-2030年(千米ドル)

表54 日本SICパワー半導体市場、電圧範囲別、2021-2030年(千米ドル)

表55 日本SICパワー半導体市場、ウェーハサイズ別、2021年~2030年(千米ドル)

表56 日本SICパワー半導体市場、ウェーハタイプ別、2021年~2030年(千米ドル)

表57 日本SICパワー半導体市場、用途別、2021年~2030年(千米ドル)

表58 日本SICパワー半導体市場、産業別、2021年~2030年(千米ドル)

表59 韓国のSICパワー半導体市場、タイプ別、2021-2030年(千米ドル)

表60 韓国のSICパワー半導体市場、電圧範囲別、2021-2030年(千米ドル)

表61 韓国のSICパワー半導体市場、ウェーハサイズ別、2021年~2030年(千米ドル)

表62 韓国のSICパワー半導体市場、ウェーハタイプ別、2021年~2030年(千米ドル)

表63 韓国のSICパワー半導体市場、用途別、2021年~2030年(千米ドル)

表64 韓国のSICパワー半導体市場、業種別、2021年~2030年(千米ドル)

表65 インドのSICパワー半導体市場、タイプ別、2021-2030年(千米ドル)

表66 インドのSICパワー半導体市場、電圧範囲別、2021-2030年(千米ドル)

表67 インドSICパワー半導体市場、ウェーハサイズ別、2021-2030年(千米ドル)

表68 インドSICパワー半導体市場、ウェーハタイプ別、2021-2030年(千米ドル)

表 69 インド SiC パワー半導体市場、アプリケーション別、2021-2030 年 (千米ドル)

表 70 インドの SIC パワー半導体市場、業種別、2021-2030 年 (千米ドル)

表71 台湾のSICパワー半導体市場、タイプ別、2021年~2030年(千米ドル)

表72 台湾のSICパワー半導体市場、電圧範囲別、2021年~2030年(千米ドル)

表73 台湾のSICパワー半導体市場、ウェーハサイズ別、2021年~2030年(千米ドル)

表74 台湾のSICパワー半導体市場、ウェーハタイプ別、2021年~2030年(千米ドル)

表 75 台湾の SIC パワー半導体市場、アプリケーション別、2021-2030 年 (千米ドル)

表 76 台湾の SIC パワー半導体市場、業種別、2021-2030 年 (千米ドル)

表 77 オーストラリアとニュージーランドの SIC パワー半導体市場、タイプ別、2021-2030 年 (千米ドル)

表 78 オーストラリアとニュージーランドの SIC パワー半導体市場、電圧範囲別、2021-2030 年 (千米ドル)

表 79 オーストラリアとニュージーランドの SIC パワー半導体市場、ウェーハサイズ別、2021-2030 年 (千米ドル)

表80 オーストラリアとニュージーランドのSICパワー半導体市場、ウェーハタイプ別、2021年~2030年(千米ドル)

表81 オーストラリアとニュージーランドのSICパワー半導体市場、用途別、2021年~2030年(千米ドル)

表82 オーストラリアとニュージーランドのSICパワー半導体市場、業種別、2021年~2030年(千米ドル)

表83 シンガポールのSICパワー半導体市場、タイプ別、2021-2030年(千米ドル)

表84 シンガポールのSICパワー半導体市場、電圧範囲別、2021-2030年(千米ドル)

表85 シンガポールのSICパワー半導体市場、ウェーハサイズ別、2021年~2030年(千米ドル)

表86 シンガポールのSICパワー半導体市場、ウェーハタイプ別、2021年~2030年(千米ドル)

表 87 シンガポールの SIC パワー半導体市場、アプリケーション別、2021-2030 年 (千米ドル)

表88 シンガポールのSICパワー半導体市場、業界別、2021年~2030年(千米ドル)

表89 タイのSICパワー半導体市場、タイプ別、2021年~2030年(千米ドル)

表90 タイのSICパワー半導体市場、電圧範囲別、2021-2030年(千米ドル)

表91 タイのSICパワー半導体市場、ウェーハサイズ別、2021年~2030年(千米ドル)

表92 タイのSICパワー半導体市場、ウェーハタイプ別、2021年~2030年(千米ドル)

表93 タイのSICパワー半導体市場、用途別、2021年~2030年(千米ドル)

表94 タイのSICパワー半導体市場、業界別、2021年~2030年(千米ドル)

表95 インドネシアのSICパワー半導体市場、タイプ別、2021-2030年(千米ドル)

表96 インドネシアのSICパワー半導体市場、電圧範囲別、2021-2030年(千米ドル)

表97 インドネシアのSICパワー半導体市場、ウェーハサイズ別、2021年~2030年(千米ドル)

表98 インドネシアのSICパワー半導体市場、ウェーハタイプ別、2021年~2030年(千米ドル)

表99 インドネシアのSICパワー半導体市場、用途別、2021年~2030年(千米ドル)

表 100 インドネシアの SIC パワー半導体市場、業種別、2021-2030 年 (千米ドル)

表 101 マレーシアの SIC パワー半導体市場、タイプ別、2021-2030 年 (千米ドル)

表 102 マレーシアの SIC パワー半導体市場、電圧範囲別、2021-2030 年 (千米ドル)

表 103 マレーシアの SIC パワー半導体市場、ウェーハサイズ別、2021-2030 年 (千米ドル)

表 104 マレーシアの SIC パワー半導体市場、ウェーハタイプ別、2021-2030 年 (千米ドル)

表 105 マレーシアの SIC パワー半導体市場、アプリケーション別、2021-2030 年 (千米ドル)

表 106 マレーシアの SIC パワー半導体市場、業種別、2021-2030 年 (千米ドル)

表 107 フィリピンの SIC パワー半導体市場、タイプ別、2021-2030 年 (千米ドル)

表 108 フィリピンの SIC パワー半導体市場、電圧範囲別、2021-2030 年 (千米ドル)

表 109 フィリピンの SIC パワー半導体市場、ウェーハサイズ別、2021-2030 年 (千米ドル)

表 110 フィリピンの SIC パワー半導体市場、ウェーハタイプ別、2021-2030 年 (千米ドル)

表 111 フィリピンの SIC パワー半導体市場、アプリケーション別、2021-2030 年 (千米ドル)

表 112 フィリピンの SIC パワー半導体市場、業種別、2021-2030 年 (千米ドル)

表113 ベトナムのSICパワー半導体市場、タイプ別、2021-2030年(千米ドル)

表114 ベトナムのSICパワー半導体市場、電圧範囲別、2021-2030年(千米ドル)

表115 ベトナムのSICパワー半導体市場、ウェーハサイズ別、2021年~2030年(千米ドル)

表116 ベトナムのSICパワー半導体市場、ウェーハタイプ別、2021年~2030年(千米ドル)

表 117 ベトナム SIC パワー半導体市場、アプリケーション別、2021-2030 年 (千米ドル)

表 118 ベトナムの SIC パワー半導体市場、業種別、2021-2030 年 (千米ドル)

表 119 その他のアジア太平洋地域の SIC パワー半導体市場、タイプ別、2021-2030 年 (千米ドル)

図表一覧

図1 アジア太平洋地域のSICパワー半導体市場:セグメンテーション

図2 アジア太平洋地域のSICパワー半導体市場:データ三角測量

図3 アジア太平洋地域のSICパワー半導体市場:DROC分析

図4 アジア太平洋地域のSICパワー半導体市場:地域市場分析

図5 アジア太平洋地域のSICパワー半導体市場:企業調査分析

図6 アジア太平洋地域のSICパワー半導体市場:インタビュー人口統計

図7 アジア太平洋SICパワー半導体市場:DBMR市場ポジショングリッド

図8 アジア太平洋地域のSICパワー半導体市場:ベンダーシェア分析

図9 アジア太平洋地域のSICパワー半導体市場:多変量モデリング

図10 アジア太平洋地域のSICパワー半導体市場:タイプ曲線

図11 アジア太平洋地域のSICパワー半導体市場:市場アプリケーション範囲グリッド

図12 アジア太平洋地域のSICパワー半導体市場:セグメンテーション

図13 市場における電気自動車の普及率の上昇が、2023年から2030年の予測期間におけるアジア太平洋地域のSICパワー半導体市場の成長を牽引すると予想される

図14 MOSFETセグメントは、2023年と2030年にアジア太平洋地域のSICパワー半導体市場で最大のシェアを占めると予想されています。

図15 アジア太平洋地域のSICパワー半導体市場の推進要因、制約要因、機会、課題

図16 アジア太平洋地域のSICパワー半導体市場:タイプ別、2022年

図17 アジア太平洋地域のSICパワー半導体市場:電圧範囲、2022年

図18 アジア太平洋地域のSICパワー半導体市場:ウェーハサイズ別、2022年

図19 アジア太平洋地域のSICパワー半導体市場:ウェーハタイプ別、2022年

図20 アジア太平洋地域のSICパワー半導体市場:アプリケーション別、2022年

図21 アジア太平洋地域のSICパワー半導体市場:業種別、2022年

図22 アジア太平洋地域のSICパワー半導体市場:スナップショット(2022年)

図23 アジア太平洋地域のSICパワー半導体市場:国別(2022年)

図24 アジア太平洋地域のSICパワー半導体市場:国別(2023年および2030年)

図25 アジア太平洋地域のSICパワー半導体市場:国別(2022年および2030年)

図26 アジア太平洋地域のSICパワー半導体市場:タイプ別(2023-2030年)

図27 アジア太平洋地域のSICパワー半導体市場:企業シェア2022(%)

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。