欧州農作物保護製品市場規模、株式および動向分析レポート

Market Size in USD Billion

CAGR :

%

USD

21.68 Billion

USD

30.86 Billion

2024

2032

USD

21.68 Billion

USD

30.86 Billion

2024

2032

| 2025 –2032 | |

| USD 21.68 Billion | |

| USD 30.86 Billion | |

| % | |

|

欧州農作物保護製品市場セグメンテーション、活性成分(Bacillus Thuringiensis(BT)、Azoxystrobin、Bifenthrin、Fludioxonil、Acephate、Boscalid、Bendiocarb、1-Methylcyclopropene、Calcium Chloride、Daminozide、Benzyl Adenine、および他)、製品タイプ(Herbicides、殺虫剤、殺菌剤、植物、増殖剤、殺虫剤、その他)、草剤、その他

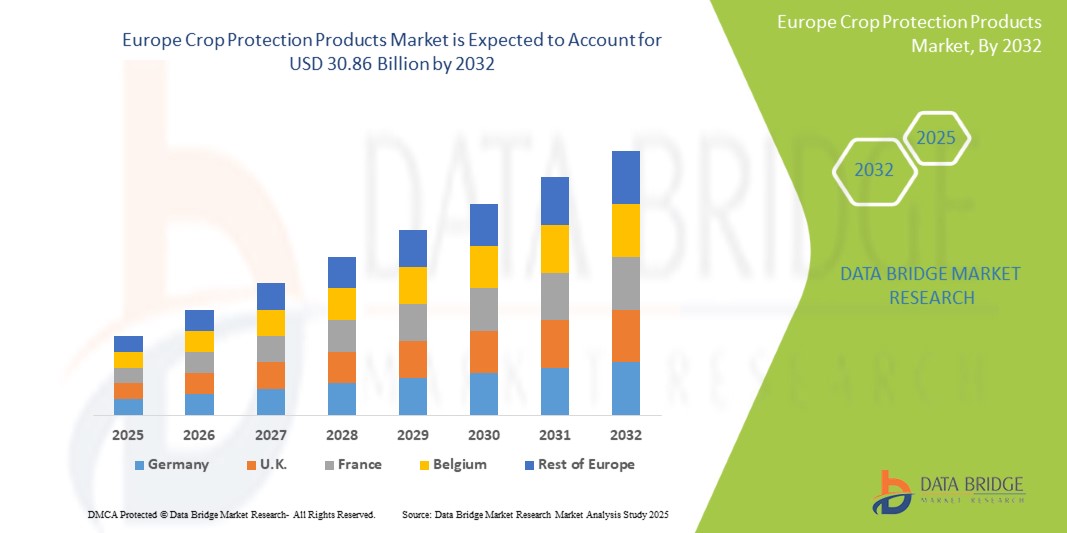

ヨーロッパの穀物の保護プロダクト市場のサイズ

- ヨーロッパの穀物の保護プロダクト市場のサイズはで評価されました2024年のUSD 21.68億そして到達する予定2032年までに30.86億米ドル, お問い合わせCAGRの4.51%予報期間中

- 市場成長は、農業の生産性を高め、食品のセキュリティに対する需要の高まり、高度の農業の実践の採用によって大きく燃料を供給しています

- 害虫、雑草および病気による作物の損失を減らすための成長した圧力は、商業農業の拡大とともに、市場の拡大を支えます

ヨーロッパの穀物の保護プロダクト市場分析

- 作物の保護プロダクト市場は収穫を保護し、質を改善する有効な解決をますます優先順位付けし、農業従事者として安定した成長を経験しています

- 持続可能なバイオベースの作物保護代替のライジングの採用は、競争力のある風景を再構築し、厳しい規制基準と安全な農業産物のための消費者需要と一致しています

- ドイツ農作物は、2024年の最大の収益分配で、欧州農作物保護製品市場を支配し、持続可能な農業と農作物の収穫最適化に重点を置いています。 ファーマーは厳密なEUの規則に従う革新的な化学および生物作物の保護解決を採用します

- U.K.は、最も高い化合物の年間成長率(CAGR)を目撃する見込みヨーロッパの穀物の保護プロダクト革新的な作物保護技術の採用、持続可能な害虫や病気管理の実践に対する需要の増加、環境に責任ある農業を支える政府の取り組みによる市場。 近代化農業技術や精密農業へのシフトは、さらなる市場成長を促進しています。

- Bacillus Thuringiensis (BT) セグメントは、2024 年に最大の市場収益シェアを保有し、持続可能な農業慣行と幅広いスペクトルの害虫駆除特性と互換性を主導しました。 BT ベースのソリューションは、さまざまな作物の効率性、低環境影響、および適合性のために広く好まれています

レポートスコープとヨーロッパクロップ保護製品市場セグメンテーション

| アトリビュート | ヨーロッパの穀物の保護プロダクト主市場の洞察 |

| カバーされる区分 |

|

| カバーされた国 | ヨーロッパ

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

ヨーロッパ作物の保護プロダクト市場の傾向

高度な作物保護ソリューションの活用

- 高度な作物保護ソリューションに対する成長したシフトは、農薬の収量を高め、害虫、雑草、病気による損失を減らすことによって、農業の風景を変革しています。 これらのソリューションは、適時かつ正確なアプリケーションを可能にし、農家の全体的な生産性と収益性を改善します。 農作物の健康と近代的な処方の長期的利点についての意識の増加は、多様な農業システム全体での採用を加速する

- 持続可能なおよびバイオベースの農薬および除草剤に対する需要の増加は、環境に優しい製剤の採用を加速しています。 これらの製品は、土壌の健康を維持し、作物の保護を確保しながら、環境への影響を減らすのに役立ちます。 ファーマーや農業事業は、これらのソリューションを長期にわたる作物管理戦略に統合し、より安全な生産のための規制圧力と消費者の好みに対応

- 現代の作物保護製品の手頃な価格と使いやすさの向上は、小株主や商業農家の間でより広い採用を奨励しています。 頻繁な使用はよりよく作物の監視を支え、大規模な損失の危険を減らす。 事前に測定された処方やスマートアプリケーション機器などの技術的進歩は、機械化農場の少ない場合でも、効率的な作物保護が可能となります。

- たとえば、近年では、統合型害虫管理キットと精密除草剤アプリケーションツールを使用して農家は、より高い作物品質と削減された化学的廃棄物を報告しています。 これらのツールは、ターゲティングされたアクションを可能にし、生産コストを削減し、長期的な土壌の持続可能性を高めます。 これらのイノベーションの採用は、知識の共有と環境安全基準の遵守を促進しています

- 高度な作物保護製品は、収量と効率性を向上させながら、その成功は、継続的なイノベーション、農家の教育、および費用対効果に依存します。 メーカーは、スケーラブル、安全、および環境的に責任あるソリューションに焦点を当て、市場需要を完全に増大する必要があります。 農業の延長サービスとトレーニングプログラムとのコラボレーションは、その有効性と長期的な市場浸透を最大化するための鍵です

ヨーロッパ農作物保護製品市場ダイナミクス

ドライバー

害虫、雑草、植物病の増大

- 植物病とともに害虫および雑草の徴候を、上昇することは有効な穀物の保護プロダクトのための要求を運転しています。 ファーマーや農業事業は、歩留まりの損失を最小限にし、作物の品質を維持するソリューションを優先しています。 世界的な食糧需要を成長させ、一貫したサプライチェーンの必要性は保護対策の採用をさらに高めます

- 生産性と収益損失の減少を含む、未処理の作物の脅威の財政影響の意識は、農薬、除草剤、殺菌剤の定期的な使用を動機づけています。 適切な作物の保護は農場の収益性および長期運用の持続可能性を直接支えます。 農業従事者と農家とのコラボレーションを強化し、製品の選定とタイミングを最大限に高めます。

- 安全かつ効果的な作物保護の実践を促進する政府のガイドラインと農業団体は、さらに市場成長をサポートしています。 規制枠組みは、害虫の管理と環境に配慮した処方の統合を促します。 高度プロダクトを採用するための集中力および補助物質はまた異なった農場のサイズ間の使用法を拡大する重要な役割を担います

- たとえば、最近の農業プログラムは、統合作物保護ソリューションの使用を奨励し、従来製品とバイオ製品の両方の採用を奨励しています。 トレーニングのイニシアチブと認知キャンペーンは、これらのプログラムを補完し、適切なアプリケーションを確保し、誤用を削減します。 結果は、クロップ健康を改善し、化学残渣を削減し、持続可能性メトリックを強化します。

- 害虫駆除と規制対応は市場を駆動する一方で、広範な採用は、適切なトレーニング、技術統合、およびすべてのタイプの農家のための手頃な価格のソリューションを必要とします。 デジタル農業ツールおよび精密農業機器への継続的な投資により、作物の保護戦略の有効性がさらに向上します。 ディストリビューターや協同組合とのパートナーシップは、小規模農家のギャップを埋めるのに役立ちます

拘束/チャレンジ

高度な作物保護製品とアクセス制限のコストが高い

- 高度な作物保護化学物質、処方、および精密アプリケーションツールの価格は、小規模な農家にとってはアクセスできません。 プレミアム製品は、多くの場合、市販の操作に限定され、広範な使用を制限します。 コストバリアは、農場の所得や断片分布ネットワークの低い地域で特に有意である

- 技術的な知識の欠如と効果的な適用方法の訓練は、特に小規模な農家の間で、農作物保護製品の効率性を低下させます。 誤った使用法は作物の損傷、化学抵抗、または環境の危険をもたらすことができます。 投与量、タイミング、および安全プロトコルの農家を教育することは、生産性と安全性の両方を最大限に活用することが重要である

- 専門的な処方と機器のサプライチェーン制約により、さらなる可用性が制限され、従来の方法の潜在的使用や信頼性が向上します。 配達および矛盾したプロダクト質で遅れは悪質に作物の周期に影響を与えることができます。 物流を強化し、倉庫化し、ローカル製造能力は、これらの課題を克服するために不可欠です

- たとえば、調査では、農家の有意な部分が、適切なガイダンスの費用や欠如による農薬の遅延や減少を遅らせることを示しています。 このようなギャップは、手頃な価格、使いやすい、そして広くアクセス可能な作物保護ソリューションの必要性を強調しています。 市場利害関係者は、製品革新と実用的な展開モデルを組み合わせた戦略を開発する必要があります

- 作物保護の革新が続いていますが、手頃な価格、アクセシビリティ、および訓練に取り組むことは重要なままです。 市場プレーヤーは、費用対効果の高いソリューション、分散型流通、および教育プログラムに焦点を合わせ、長期的な市場の潜在的なロックを解除する必要があります。 政府機関、NGO、協力機関と連携することで、採用を加速し、農業全体の生産性を向上させることができます。

ヨーロッパの穀物の保護プロダクト市場規模

市場は、有効成分、製品の種類、起源、フォーム、アプリケーション、クロップタイプに基づいてセグメント化されます。

•活動的な原料によって

有効成分に基づいて、ヨーロッパ作物保護製品市場は、Bacillus Thuringiensis(BT)、Azoxystrobin、Bifenthrin、Fludioxonil、Acephate、Boscalid、Bendiocarb、1-Methylcyclopropene、Calcium Chloride、Daminozide、Benzyl Adenineおよび他に分けられます。 Bacillus Thuringiensis (BT) セグメントは、2024 年に最大の市場収益シェアを保有し、持続可能な農業慣行と幅広いスペクトルの害虫駆除特性と互換性を主導しました。 BT ベースのソリューションは、さまざまな作物に対する効率性、環境負荷の低い、および適合性のために広く好まれています。

アゾキシストロビンセグメントは、真菌疾患に対する高い有効性によって駆動され、果物、野菜、シリアル全体の採用を成長させる2025から2032までの最速の成長率を目撃する予定です。 アゾキシストロビン製剤は、その信頼性、長期残留活動、および統合された害虫管理プログラムとの互換性のためにますます優先されます。

• プロダクト タイプによって

製品の種類に基づいて、欧州の作物保護製品市場は、除草剤、殺虫剤、殺菌剤、植物成長レギュレータ、農薬、燻蒸剤、ネマリスト、拡散接着剤、その他に分けられます。 Herbicidesのセグメントは、効果的な雑草管理と高い作物の収量の増加の必要性によって駆動される2024年に最大の市場収益シェアを開催しました。 除草剤は精密な適用を提供し、作物の損傷を最小にし、大規模なシリアルおよび穀物の生産システムを渡る広く採用されます。

殺虫剤のセグメントは、2025年から2032年までの最も速い成長率を目撃し、害虫の侵入を増加させ、作物の損失防止の重要性が高まっています。 高度の殺虫剤の公式はターゲットを絞られた行為、減らされた化学使用および高められた穀物の保護効率を提供しま、商業および小さいホールダーの農家間の採用を高めます。

・起源によって

起源に基づいて、ヨーロッパの作物の保護プロダクト市場は総合的なおよび生物農薬に分けられます。 合成部門は、2024年に世界最大の市場収益シェアを保有し、その広範な有効性、コスト効率性、および作物タイプの広範な可用性を主導しました。 合成製剤は、大規模な商業農業に広く採用されています。

バイオ農薬セグメントは、環境にやさしい、持続可能な作物保護ソリューションの需要の増加によって駆動され、2025年から2032年までの最速成長率を目撃する見込みです。 生体農薬は、低環境負荷、規制順守、有機農業慣行の適合性により人気が高まっています。

・フォーム

形態に基づいて、ヨーロッパ作物の保護プロダクト市場は液体および乾燥したに分けられます。 液体セグメントは、アプリケーションの使いやすさ、より迅速な吸収、自動スプレーシステムとの互換性により、2024年に最大の市場収益シェアを保持しました。 液体はfoliarのスプレーおよびポスト ハーヴェストの処置のために広く利用されています。

ドライセグメントは、種子処理、土壌処理、および精密農業用途の採用によって駆動され、2025から2032までの最速の成長率を目撃する予定です。 乾式処方は、機械化機器の安定性、長い棚寿命、および適合性に優先されます。

• 適用によって

応用に基づいて、欧州の作物の保護プロダクト市場はFoliarのスプレー、種の処置、土の処置、ポスト ハーヴェスト、chemigationおよび他に分けられます。 フォリアスプレーセグメントは、急速なターゲットの害虫や病気制御を提供する能力によって駆動され、2024年に最大の市場収益シェアを開催しました。 Foliarのスプレーは効率および便利による価値の高い穀物のために広く採用されます。

種子処理セグメントは、初期段階の作物保護ニーズによって駆動され、果物、野菜、シリアルの採用の増加によって、2025から2032までの最速の成長率を目撃する予定です。 種子処理は、害虫の攻撃を減らし、発芽を改善し、全体的な作物のパフォーマンスを向上させるのに役立ちます。

• 作物のタイプによって

作物のタイプに基づいて、ヨーロッパの作物の保護プロダクト市場は穀物および穀物、フルーツおよび野菜、油をさされるおよび脈拍、泥炭およびOrnamentalsおよび他の作物に分けられます。 CerealsとGrainsのセグメントは、大規模な栽培と世界的なステープル作物の需要によって駆動され、2024年に最大の市場収益シェアを開催しました。 これらの作物は、歩留まりを維持するために広範な雑草および害虫の管理を必要とします。

果物と野菜のセグメントは、2025年から2032年までの最も速い成長率を目撃し、消費量の増加、より高い値、品質と安全な生産のための要求によって駆動されます。 精密作物の保護の解決および生物ベースのプロダクトは食糧安全および収穫の最適化を保障するためにこれらの高値作物でますます採用されます。

ヨーロッパ農作物保護製品市場地域分析

- ドイツ農作物は、2024年の最大の収益分配で、欧州農作物保護製品市場を支配し、持続可能な農業と農作物の収穫最適化に重点を置いています。 ファーマーは厳密なEUの規則に従う革新的な化学および生物作物の保護解決を採用します

- ドイツのよく発達した農業インフラと相まって、環境にやさしい、高性能な製品に対する要求は、広範な採用を推進しています

U.K.クロッププロテクション製品市場インサイト

U.K. 作物保護製品市場は、2025年から2032年までの最速成長率を目撃し、持続可能で効率的な害虫、雑草、および病気の制御ソリューションの採用によって推進されています。 農家は、高度な除草剤、殺菌剤、殺虫剤を活用して、生産性を維持し、食品安全基準を満たしています。 環境に責任ある作物保護の実践を促進する政府プログラムは、長期的な成長をサポートすることが期待されます。

ヨーロッパ農作物保護製品市場シェア

ヨーロッパの穀物の保護プロダクト企業は主に下記のものを含んでいる十分に確立された会社によって、導きます:

- バイエルAG(ドイツ)

- Syngenta AG(スイス)

- BASF SE(ドイツ)

- ベルキム作物保護(ベルギー)

- Koppert 生物システム(オランダ)

- Sipcam オクソン (イタリア)

- Agriphar(ベルギー)

- セラティス・ヨーロッパ(オランダ)

- Nufarm Europe GmbH(オーストリア)

- Andermatt Biocontrol(スイス)

欧州農作物保護製品市場の最新動向

- 2024年6月、シンジェンタとInstaDeepは、AIの大規模ランゲージモデルを活用した作物の種特性調査を加速するために提携しました。 このパートナーシップは、スピード、精度、および特性開発の加速における効率性を高めることで、Syngenta SeedsのR&D機能を強化します。 大規模なランゲージモデル(LLM)は、研究サイクルを短縮し、意思決定プロセスを強化し、農家に貴重なソリューションを提供するように設計されています。 組み合わせた専門知識は、コラボレーションと最先端技術によるトウモロコシと大豆の作物のための変革的な製品革新を実行します

- 2023年8月、植物および種子の健康のための生物学的ソリューションのポートフォリオを高めるために、当社は実質的な投資を行いました。 2020年のヴァラグロの買収に伴い、同社は一貫して研究開発に投資し、一連の商業パートナーシップや研究コラボレーションを通じて高度な生物学的ソリューションの範囲を拡大しています。 このパートナーシップは、より多くのグローバルプレゼンスを高めるのに役立ちます

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。