欧州のGlyoxal市場規模、株式および動向分析レポート

Market Size in USD Billion

CAGR :

%

USD

133.92 Million

USD

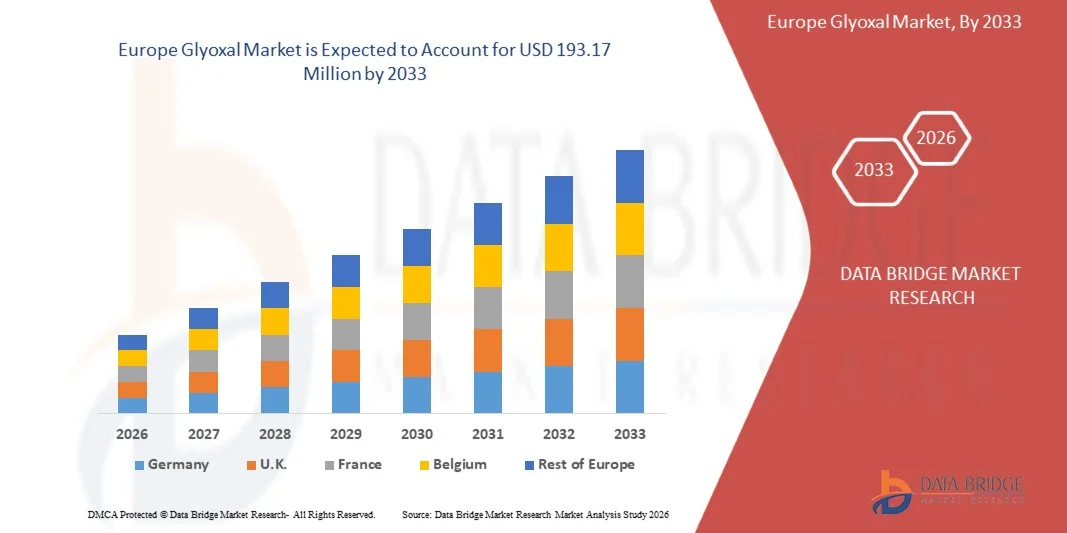

193.17 Million

2025

2033

USD

133.92 Million

USD

193.17 Million

2025

2033

| 2026 –2033 | |

| USD 133.92 Million | |

| USD 193.17 Million | |

| % | |

|

欧州のGlyoxalの市場セグメンテーション、等級(産業等級、薬剤の等級)によって、純度(90%-99%、40%-60%、他)、工程(EthyleneのGlycol、Acetyleneの酸化、他)、包装(びん、ドラム、Jerrycansの合成IBCのバルク)、適用(十字リンク、化学中間物、および他の)、エンド ゼリゾールの化学薬品(アセチルル、エチルル、エチルル、エチルル、エキシル、エチルル、エチルル、エキシル、エチルル、エキシル、エチルル、エキシル、エキシル、エキシル、エチルル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシル、エキシ

ヨーロッパGlyoxal市場規模と概要は何ですか

- データブリッジ市場調査分析では、欧州のグリオキシカル市場が到達する見込み米ドル 193.17 百万 によって 2033からツイート 2025年の133.92百万成長し、4.8%のCAGR2026年から2033年までの予測期間。

- ヨーロッパのGlyoxal市場は織物、ペーパー、革、医薬品、農薬、石油およびガス産業の拡大の使用によって運転される安定した成長を目の当たりにしています。このGlyoxalは、その架橋、結合および仕上げの特性のために評価されます。

市場規模と予測

- ヨーロッパ市場価値 (2025):193.17百万円

- 期待される市場価値 (2033):米ドル 133.92 百万

- 予測CAGR (2026–2033): 4.8%

ヨーロッパのGlyoxal市場分析

- 繊維、紙、樹脂、医薬品、化粧品、水処理などの多岐にわたる業界に渡ります。 要求は専門および性能の化学公式の主中間物として強い架橋の特性そして役割によって運転されます。

- 織物の仕上げ活動を高め、紙包装の消費を増加させ、環境に優しい樹脂の使用は主要な要求の運転者です。 医薬品製造および厳密な排水処理規則の拡大により、世界各地のサステナブルなグリオキシカル消費をサポートしています。

- 市場は、多国籍化学生産者と地域メーカーのミックスを備えています。 競争はプロダクト純度、適用特定の等級、価格設定、供給の信頼性およびキーのエンドユースの企業を渡る環境および安全規則に従うことに基づいています。

- ドイツは欧州のglyoxal市場を支配し、2026年の市場シェアの24.95%を大規模な製造能力、低い生産費および豊富な原料の可用性によって支えられる可能性が高いです。 繊維、樹脂、製紙、皮革の産業からの強い下流の要求は、広範な化学供給の鎖と共に、更にそのリーダーシップを補強します。

- ドイツのグリオキシカル市場は、2026年から2033年までの約5.2%のCAGRで成長し、織物および農薬産業からの需要の増加と産業用途の樹脂およびコーティングの使用の増加によって運転されると予想されます。 地域における産業化と都市化の拡大により、燃料市場の成長が進んでいます。

- 2025年、工業用グレードのセグメントは、樹脂、接着剤、紙処理薬品の広範な使用により、81.89%のシェアでグリオキシカル市場を支配することが期待されます。 セグメントは、大規模な産業用途やバルク生産のための費用対効果の高い需要から恩恵を受けており、他のグレードよりも好ましい選択肢となっています。

レポートスコープと欧州のGlyoxal市場セグメンテーション

|

アトリビュート |

欧州のGlyoxal市場の洞察 |

|

カバーされる区分 |

|

|

カバーされた国 |

ヨーロッパ

|

|

主要市場プレイヤー |

|

|

マーケットチャンス |

|

|

付加価値データインフォセットを追加 |

市場価値、成長率、市場セグメント、地理的カバレッジ、市場プレイヤー、市場シナリオなどの市場洞察に加えて、データブリッジ市場リサーチチームがキュレーションした市場レポートには、詳細なエキスパート分析、インポート/エクスポート分析、価格分析、生産消費分析、および農薬分析が含まれます。 |

ヨーロッパのGlyoxal市場の主な動向は何ですか

「 」スマート製造、倉庫加工、電子商取引包装エコシステムとの統合ツイート

- Glyoxalは、繊維仕上げ、製紙処理、樹脂用途向けのスマート製造環境でますますます活用され、一貫した品質管理、プロセス最適化、および業界 4.0 の取り組みと並ぶデータ主導の生産決定をサポートします。

- 倉庫および処理施設では、材料の安定化、コーティングの性能および湿気の抵抗のglyoxalベースの公式の援助は、処理の効率、貯蔵の耐久性および下流の処理の信頼性を改善します。

- 包装用粘着剤、紙強化剤、表面処理におけるグリオキシアルの増大は、物流ネットワーク全体のパッケージングの整合性、負荷安定性、製品保護を強化することにより、電子商取引の拡大をサポートしています。

インスタンスのため、

- 2025年1月、Glyoxalベースの化学ソリューションは、高度プロセス制御とデジタル監視システムと組み合わせて、産業業務における効率性、一貫性、持続可能性を改善し、次世代製造エコシステムにおけるglyoxalの役割を強調した、自動化された織物および紙加工ラインにますます統合されました。

- 最近の産業開発は、従来のエンドユース部門を超えた拡大の役割を強化し、電子商取引や物流のボリュームとして、glyoxal、高性能包装および産業用途を含む専門アルデヒドベースの化学物質の採用の増加を示しています。

ヨーロッパ・グリオキシカル・マーケット・ダイナミクス

ドライバー

「 」産業近代化および性能主導の化学適用条件の上昇ツイート

- 欧州産業部門は、織物、紙、樹脂、革、特殊化学用途の複雑な性能要件をますますます複雑化し、加速されたグリオキシカルベースのソリューションを採用しています。 メーカーは、製品強度、耐久性、機能性能を向上させるクロスリンク、バインディング、および仕上げ特性のためにglyoxalを優先しています。 産業プロセスは、高い効率と品質の一貫性に進化するにつれて、制御された反応をサポートし、排出を削減し、最終製品の信頼性を向上させる化学製剤の需要が高まっています。

- 産業近代化のイニシアチブ内のglyoxalの拡大の役割は革新する化学生産者のための動的環境を作成しましたり、公式の純度、適用多様性およびプロセス両立性の進歩に導きます。 このデマンド主導シフトに応じて、メーカーは、低ホルムアルデヒドシステム、特殊樹脂、高性能織物処理など、特定のエンドユース要件に適したカスタマイズされたグリオキシカルグレードの開発に投資しています。

- これらの革新はさまざまな処理条件および規制上の制約の下で確実に実行できる適応可能な化学ソリューションを必要とする現代企業の操作上の必要性によって主に運転されます。 業界は、高度な製造と仕上げのワークフローにglyoxalを統合し続けています。この瞬間は、サプライヤー投資戦略に影響を及ぼすだけでなく、産業生産性と材料性能を向上させる上で重要な中間体としてのglyoxalの役割を強化します。

例えば、

- 2023年9月、産業出版物は厳密な環境の承諾の標準に会う間生地の強さおよびしわの抵抗を改善することを目的とした高度の織物の仕上げプロセスのglyoxalの増加された採用を強調しました。

- 2024年2月現在、化学工業のインサイトでは、欧州のメーカーが、持続可能な生産慣行をサポートし、毒性の高まりに対する信頼性を低下させるための、glyoxalベースの樹脂および製紙処理ソリューションの使用を増強したことを示しています。

- 2025年2月、アジア太平洋地域における地域産業の発展は、性能向上と規制のアライメントに焦点を当てたパッケージング、建設、および産業製造分野からの需要増加を満たすために、glyoxalを含む専門的アルデヒド生産における成長投資を強調した。

- 世界的な産業分野横断のglyoxalの採用は、進化する性能、効率および持続可能性の要求と一直線に並ぶ多機能の化学ソリューションとして、その増加の重要性を強調しています。 業界は、高品質の出力とより制御された製造プロセスに進んでいくように、Glyoxalのクロスリンク、結合、および仕上げ能力は、強化された材料の強度、耐久性、および機能的な一貫性の重要な有効化剤として位置します。

- 配合の純度とアプリケーション固有のカスタマイズの革新を経ることで、繊維、紙、樹脂、革、特殊化学物質の関連性を強化します。 投資の増加、規制アライメントの取り組み、および主要地域における産業利用事例の拡大により、glyoxalは、産業の生産性を向上し、より持続可能で高性能な製造慣行への移行をサポートする戦略的に重要な役割を担っています。

拘束/チャレンジ

「化学製造と使用のための調和した欧州規制枠組みの欠如」

- 化学製造、取り扱い、およびエンドユースのアプリケーションを支配する調和の取れた欧州規制の欠如は、規制要件が国や地域で著しく異なるため、欧州のGlyoxal市場にとって注目すべき課題を提示します。

- 規制当局は、化学物質の分類、許容暴露制限、環境の遵守、ラベル付け、輸送、排水排出に関するさまざまな基準を適用します。 この規制のフラグメンテーションは、各市場のための処方、文書、安全プロトコル、およびコンプライアンス戦略を変更し、運用の複雑さ、コンプライアンスコスト、および市場投入までの時間を増やすために、glyoxalメーカーとダウンストリームユーザーを構成します。

- その結果、企業は、特にクロスボーダー取引と繊維、紙、樹脂、および特殊化学アプリケーションを提供する多国籍サプライチェーンのために、スケーリングglyoxal生産と流通ヨーロッパで制約に直面しています。

例えば、

- 2025年、アジアおよびヨーロッパ地域の環境当局は、グリオクサルを含むアルデヒドベースの化学物質のコンプライアンス要件が異なることを発表しました。エミッションのしきい値と報告義務のバリエーション、標準化された生産と輸出戦略を複雑化する規制の矛盾を強調しています。

- 2025年5月、新興市場での国内および地方の規制機関は、既存の中央ガイドラインを超えて厳しい化学的取り扱いと輸送制限を実施し、実施期間中に追加の承認と物流ワークフローの修正が必要だったグルクタールメーカーやディストリビューターの一時的な運用中断を作成します。

- 結論として、調和のとれたグローバル規制枠組みの欠如は、標準化された生産、流通、クロスボーダー取引の容易さを制限し、グローバルグリオクサル市場の構造的課題を提起し続けています。 化学物質の分類、環境の遵守、取り扱い、輸送に関する多様な地域要件は、運用の複雑性を高め、メーカーおよび下流ユーザーに対するコンプライアンスコストを向上します。

- これらの規制当局は、市場参入とスケーラビリティを遅くするだけでなく、地域全体の処方、文書、物流戦略への頻繁な調整が必要であるだけでなく、矛盾しています。 その結果、規制の断片化は、グローバル市場拡大の重要な制約を維持し、より効率的な国際サプライチェーンと持続可能な市場成長を支えるために、化学ガバナンスにおけるより大きなアライメントと透明性の必要性を強調しています。

ヨーロッパグリオキシカル市場スコープ

ヨーロッパのGlyoxalの市場は等級、純度、工程、包装の適用、エンド ユースの化学薬品およびエンド ユースの企業に基づいている7つの注目すべき区分に分類されます。

グレード別

等級に基づいて、ヨーロッパのGlyoxalの市場は産業等級および薬剤の等級に主に分けられます。

2026年までに、インダストリアルグレードのセグメントは、合計シェアの81.81%を占める市場を支配する予定です。 繊維、製紙加工、樹脂、革加工、水処理など、さまざまな業界に及ぶ幅広い用途に強みがあります。 産業用グレードのグリオキシカルの大量消費量は、大規模運用におけるコスト効率と効率性によりさらにサポートされます。 また、欧州地域における産業・製造業の急速な拡大は、強固で持続的な需要を担っています。 その結果、産業グレードのグリオキシカルは、地域市場における主要な成長ドライバーを維持することが期待されます。

欧州のGlyoxal市場における医薬品グレードのセグメントは、2026年から2033年にかけて急速に成長する見込みで、医薬品合成、高純度薬品の厳しい規制要件、および高度な医薬品製造および専門用途の拡大によって推進されています。 これらの要因は、APIおよび革新的な医薬品製剤における高品質のグリオキシカルの採用を促進します。

純度によって

純度に基づいて、欧州のグリオキシカル市場は90%〜99%、40%〜60%、その他に分けられます。

2026年までに、40%〜60%の純度セグメントが市場を支配し、合計シェアの72.86%を占めることが期待されます。 このセグメントの優位性は、その優れた性能、より高い反応、および高度なアプリケーションに対する適合性に起因しています。医薬品、専門の樹脂、織物および化粧品。 一貫した品質は、厳しい業界標準に準拠し、強固で持続的な要求をさらに促進します。 また、効果とコスト効率の両立により、この純度範囲はメーカーに優先されます。 その結果、40%〜60%の純度セグメントは、欧州のGlyoxal市場で成長する主要な貢献者を維持するために計画されています。

ヨーロッパGlyoxal市場における90%-99%純度セグメントは、2026年から2033年までの最も速い成長を目撃する見込みで、高純度のグリオキシカルを必要とする医薬品および専門化学アプリケーションで広く使用されているため、高度な医薬品処方と規制に準拠した生産プロセスの需要の増加に伴い、成長を期待しています。

生産プロセスによって

生産プロセスに基づいて、欧州のGlyoxal市場はEthylene Glycol、アセチレンの酸化、および他の触媒作用の酸化に分けられます。

2026年までに、エチレングリコールセグメントの触媒酸化は、合計シェアの89.89%を占める市場を支配することが期待されます。 このセグメントの優位性は、アセチレンベースのプロセスと比較して、より高い生産効率、より良い収穫制御、および低不純物レベルによって駆動されます。 また、より環境に配慮し、大規模製造に適しています。 この方法の費用効果が大きいおよびスケーラビリティは更に製造業者間の好みを補強します。 その結果、触媒酸化経路は、欧州のGlyoxal市場における成長の第一次ドライバーを維持するために供給されます。

ヨーロッパGlyoxal市場における「アセチレンの酸化」の生産プロセスセグメントは、2026年から2033年までの最速成長を目撃し、医薬品および専門化学用途に適した高純度のグリオキシカルを生産する能力によって駆動され、高度な医薬品処方の需要の増加と厳格な品質と規制基準の遵守を伴います。

包装によって

包装に基づいて、ヨーロッパグリオキシカル市場はドラム、コンポジットIBC、バルク、ジェリーカン、およびボトルに分割されます。

2026年、ドラムセグメントは市場を支配し、合計シェアの39.96%を占めることが期待されます。 この優位性は、その汎用性、取り扱いのしやすさ、および安全なストレージ、特に小型のアプリケーションに起因します。 びんは薬剤のために特に適しています、化粧品、および精密および安全が重要である専門化学使用。 さらに、幅広い可用性と費用対効果の高い生産により、業界全体の強力な採用を促進します。 びんの包装の便利そして信頼性は製造業者およびエンド ユーザーのためのそれの好まれた選択を同様にします。

ヨーロッパGlyoxal Marketの「Composite IBC」パッケージング部門は、2026年から2033年までの最も速い成長を目撃し、バルク化学物質の保存と輸送の効率性、安全性と耐薬品性の強化、医薬品、専門化学、および信頼性の高い大容量パッケージソリューションを必要とする産業ユーザーからの需要の増加によって主導されると予想されます。

用途別

包装に基づいて、欧州のGlyoxal市場は、アプリケーションクロスリンク、化学中間体、その他に区分されます。

2026年、クロスリンクセグメントは、市場を支配し、合計シェアの65.28%を占めることが期待されます。 この優位性は、その汎用性、取り扱いのしやすさ、および安全なストレージ、特に小型のアプリケーションに起因します。 ボトルは、医薬品、化粧品、特殊化学用途に特に適しており、精度と安全性が重要である。 さらに、幅広い可用性と費用対効果の高い生産により、業界全体の強力な採用を促進します。 びんの包装の便利そして信頼性は製造業者およびエンド ユーザーのためのそれの好まれた選択を同様にします。

欧州のGlyoxal市場における化学中間体アプリケーションセグメントは、2026年から2033年までの最も急速に成長するセグメントであり、樹脂、ポリマー、および専門薬品の需要増加、化学工業産業の拡大、および産業および専門用途における多岐にわたる架橋および反応中間体としてglyoxalの使用によって促進される。

エンドユース薬品による

エンド ユースの化学薬品に基づいて、ヨーロッパのGlyoxalの市場はDihydroxyethylene Urea (DHEU)、2-Imidazolidinone、Glyoxalated Polyacrylamide (GPAM)、Glyoxylicの酸、Glyoxalated Starch、Glyoxal Phenolの樹脂、EthyleneのグリコールのDiformate、Urea-GlyoxaloxateのConcentoxate、Quadlyoxalate、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyazole、Glyoxalate、G

2026年までに、ディヒドロキシエチレン尿素(DHEU)セグメントは、合計シェアの20.03パーセントを占める市場を支配することが期待されます。 繊維仕上げ、製紙加工、樹脂加工など、幅広い用途にお応えします。 セグメントは、さまざまな産業プロセスと高い反応、一貫性のある性能、互換性から恩恵を受けます。 また、欧州地域における高品質の繊維や特殊化学品の需要が高まっています。 DHEUの費用対効果および効率は製造業者およびエンド ユーザー間の好みを更に補強します。

欧州のGlyoxal市場における2イミダソリジノンのエンドユース化学物質セグメントは、2026年から2033年まで急速に成長し、医薬品、農薬、および特殊化学用途での使用が増えることが期待されています。 その成長は高度の公式のための合成の2-Imidazolidinoneの主中間物として高純度のglyoxalのための上昇の要求によって燃料を供給され、調整可能な化学生産。

エンドユーザーによる

エンドユーザーに基づいて、欧州のグリオキシカル市場は織物、パルプおよびペーパー、革、ペンキおよびコーティング、水処理、薬剤、世帯プロダクト、化粧品およびパーソナル ケア、包装、電気および電子工学、オイルおよびガスおよび他のに分けられます。

2026年、繊維セグメントは市場を支配し、合計シェアの35.36%を占めることが期待されます。 この成長は生地の仕上げ、しわの抵抗およびしわ防止処置の広範な使用によって運転されます。 耐久性と高品質の織物の需要の増加、アパレルおよび家庭用家具業界の急速な拡大と相まって、市場成長をサポートします。 さらに、プレミアムと長持ちする生地の消費者の好みが高まり、グリオキシカルベースのソリューションの採用が高まります。 その結果、テキスタイルセグメントは、欧州のGlyoxal市場への主要な貢献を維持するために表彰されます。

ヨーロッパグリオキシカル市場におけるパルプおよび紙エンドユーザーセグメントは、2026年から2033年にかけて急速に成長する見込みで、耐湿性樹脂の需要増加と紙の耐久性と品質を向上させる化学添加物の需要増加によって駆動されます。 紙や包装産業の拡大と、高性能で持続可能な紙製品へのシフトによる成長をサポートします。

ヨーロッパのGlyoxal市場地域分析

- ドイツは、強力な規制枠組み、高度な化学製造能力、および十分に確立された産業基盤によって支えられた2026年にヨーロッパのGlyoxal市場会計シェアで支配している国です。

- 繊維、製紙加工、建材薬品、樹脂、特殊薬品の活用を促進し、持続可能で高純度な化学生産への投資を継続し、国における長期市場拡大を推進

フランス Glyoxal マーケット インサイト

紙加工、織物仕上げ、医薬品、特殊化学用途の需要が高まっています。 政府は、持続可能な化学使用量に焦点を当て、低排出処方の採用の増加は、産業分野における市場開発をサポートしています。

U.K. Glyoxalマーケットインサイト

U.K. Glyoxal Marketは、紙加工、織物仕上げ、医薬品、特殊化学物質の使用量を増やすことで、安定した成長を目撃しています。 厳しい環境規制は、持続可能な製造と低排出処方に重点を置き、主要な産業用途における採用を推進しています。

ヨーロッパのGlyoxal市場シェア

Glyoxal は、主に、以下のような広範な企業によって導かれています。

- Amzole India Pvt. Ltd (インド)

- Asis Scientific Pty Ltd(オーストラリア)

- Atamanの化学薬品(インド)

- BASF SE(ドイツ)

- Bidvestの化学薬品(南アフリカ)

- Bisley Asia (M) Sdn Bhd (マレーシア)

- イーストマン化学株式会社(米国)

- Fluorochem Limited(イギリス)

- 富士フイルム和光純薬株式会社(日本)

- グレンタムライフサイエンスリミテッド(イギリス)

- GetChem Co.、株式会社(中国)

- ハンナインスツルメンツ株式会社(米国)

- ヒメディア研究所(インド)

- 関東科学(日本)

- Kemira Oyj (フィンランド)

- メルク・カーガ(ドイツ)

- Meru Chem Pvt. Ltd (インド)

- Mubyの化学薬品(インド)

- マルチケム専門プライベートリミテッド(インド)

- オークウッド製品株式会社(米国)

- Otto Chemie Pvt. Ltd (インド)

- Oxford LabファインケムLLP(インド)

- サンタクルスバイオテクノロジー株式会社(米国)

- サゾル(南アフリカ)

- シルバーフェーンケミカル株式会社(米国)

- サーモフィッシャーサイエンス株式会社(米国)

- Univar Solutions LLC(米国)

- Weylchem International GmbH(ドイツ)

- Zhishangの化学薬品(中国)

欧州のGlyoxal市場の最新動向

- 2025年10月、Multichemの専門性は企業Outlookの雑誌によってトップ10の専門化学ディストリビューター2025の間で、専門の化学薬品のセクターの質、革新および信頼できるサービスに強調表示されました。 2025年7月には、ブリーチ・キャンデー・病院信託と共同で成功した献血ドライブを組織し、従業員やコミュニティのメンバーが医療ニーズに対応できるようにしています。

- 2024年2月、マルチケム・スペシャリティーズ・プライベート・リミテッドは、インドのヴィタフーズ・インディアに参画し、お客様やパートナーが拡大する化学的ポートフォリオを提示し、栄養補助食品および専門成分の分野での存在を強化しました。

- Otto Chemie Pvt. Ltd.は、医薬品、研究開発、産業分野におけるプレゼンスを強化し、高純度ラボ薬品および試薬のポートフォリオを拡大しました。 同社は、インドと国際市場を横断して成長する需要を満たすために、流通ネットワークとサプライチェーン機能を強化しました。

- 2024年7月、オット・チェミー・ピボット・リミテッドは、地域病院と共同で献血と健康意識を促進し、地域社会の福祉と従業員の社会的責任への取り組みへのコミットメントを反映しています。

- 2025年3月、オックスフォード・ラボファイン・ケムLLPは、環境にやさしい包装ソリューションと、生産および流通プロセスにおける廃棄物管理の最適化を実施し、持続可能で責任ある化学製造へのコミットメントを強化しています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

目次

1 導入事例

1.1 スタディの目的

1.2 マーケットデファインション

1.3 ヨーロッパ・グリオカル・マーケットの概観

1.4 制限事項

1.5 市場開拓

2 市場調査

2.1 市場開拓

2.2 ジオグラフィックスコープ

2.3 年はスタディのために考慮

2.4 カルレンシー&ピッキング

2.5 DBMR 駆動型データ検証モデル

2.6 究極のモデルリング

2.7 製品の種類 ライフライン カーブ

2.8 主要オピニオンリーダーによるプライマリインタビュー

2.9 DBMRの市場POSITIONの格子

2.1 市場エンド ユーザー カバー グリッド

2.11 二次会

2.12 アセンブリ

3 エグゼクティブ ミーティング

4 プレミアムINSIGHTS

4.1 EUROPE GLYOXALの市場: バリューチェーン分析

4.1.1 RAW素材とフェードストックサプライ(5%〜10%のバリューシェア)

4.1.2 製造・加工(15%~25% バリューシェア)

4.1.3 流通・物流(30%~40% バリューシェア)

4.1.4 エンドユースインダストリーズ&セールスチャネル(10%〜20%のバリューシェア)

4.2 サプライチェーン分析

4.2.1 RAW素材の調達と処理

4.2.2 生産及びプロダクト製造(生産)

4.2.3 サプライチェーン・物流(輸送)

4.2.4 小売および商業バイヤーのチャネル(運転及び販売)

4.3 PORTER'S FIVE FORCESアナリシス

4.3.1 バイヤー/コンシューマーのキャリアを高める – High

4.3.2 新入店の座席 - 低い順

4.3.3 SUBSTITUTE製品のTHREAT – 高度に供給

4.3.4 スプライマーの警備員 - 近代

4.3.5 包括的なRIVALRYの強度 – 高

5 マーケット・オーバービュー

5.1 ドライバー

5.1.1 十字架としてGLYOXALのRISING UTILIZATION EXTILE FINISHING.

5.1.2 ペーパー及びWET-STRENGTHおよび表面処理の適用のための包装のローディングの高度。

5.1.3 医薬品および薬学におけるインターメディア化学的開発の展開。

5.1.4 リジンおよび粘着システムにおける低周波の高度のための補強。

5.2 削除

5.2.1 高度の実効性および安定性の感受性に必要性を収容する

5.2.2 応用規格の安定性の可否。

5.3 機会

5.3.1 FEEDSTOCK PRICINGの容量 コストの計算

5.3.2 強固な環境およびOCCUPATIONALの安全性。

5.3.3 価格競争力のある市場における限られた製品の違い

5.4 チャレンジ

5.4.1 修飾および適用指定の亜鉛めっきの開発。

5.4.2 消費者の消費から出発する

6 EUROPEのGLYOXALの市場、GRADEによる

6.1 概要

6.2 産業等級

6.3 医薬品グレード

6.4 EUROPEのGLYOXALの市場、GRADEによって、2018-2033 (THOUSAND TONS)

6.4.1 産業等級

6.4.2 薬剤の等級

6.5 EUROPE の GLYOXAL の市場、地域によって、2018-2033 (USD の THOUSANDAND)

6.5.1 アジアパシフィック

6.5.2 ノースアメリカ

6.5.3 ヨーロッパ

6.5.4 中東&アフリカ

6.5.5 南アフリカ

6.6 EUROPE PHARMACEUTICALGRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSANDAND), ポルトガル

6.6.1 アジアパシフィック

6.6.2 ノースアメリカ

6.6.3 ヨーロッパ

6.6.4 中東・アフリカ

6.6.5 南アフリカ

7 EUROPE GLYOXALの市場、PURITYによる

7.1 概要

7.1.1 40%-60%

7.1.2 90%-99%

7.1.3 その他

7.2 EUROPE 40%-60% GLYOXAL 市場, REGION, 2018-2033 (USD THOUSAND)

7.2.1 アジアパシフィック

7.2.2 ノースアメリカ

7.2.3 ヨーロッパ

7.2.4 中東・アフリカ

7.2.5 南アフリカ

7.3 EUROPE 90%-99% GLYOXAL MARKET、REGION、2018-2033(USD THOUSAND)で

7.3.1 アジアパシフィック

7.3.2 北アメリカ

7.3.3 ヨーロッパ

7.3.4 中東&アフリカ

7.3.5 南アフリカ

7.4 GLYOXAL 市場におけるヨーロッパ, 地域別, 2018-2033 (USD THOUSAND)

7.4.1 アジアパシフィック

7.4.2 北アメリカ

7.4.3 ヨーロッパ

7.4.4 中東・アフリカ

7.4.5 南アフリカ

8 EUROPEのGLYOXALの市場、生産のプロセスによる

8.1 閲覧

8.1.1 エチルネグリカラーの触媒酸化

8.1.2 アセティルネの酸化

8.1.3 その他

8.2 EUROPE ETHYLENE GLYOXAL MARKET, REGION, 2018-2033 (USD THOUSAND)の触媒酸化

8.2.1 アジアパシフィック

8.2.2 ノースアメリカ

8.2.3 ヨーロッパ

8.2.4 中東・アフリカ

8.2.5 南アフリカ

8.3 グリオクサルの市場におけるACETYLENEのEUROPEの酸化, REGIONによって, 2018-2033 (USD THOUSAND)

8.3.1 アジアパシフィック

8.3.2 北アメリカ

8.3.3 ヨーロッパ

8.3.4 中東&アフリカ

8.3.5 南アフリカ

8.4 GLYOXAL MARKETで他のヨーロッパ, REGIONによって, 2018-2033 (USD THOUSAND)

8.4.1 アジアパシフィック

8.4.2 北アメリカ

8.4.3 ヨーロッパ

8.4.4 中東とアフリカ

8.4.5 南アフリカ

9 EUROPEの包装によるGLYOXALの市場、

9.1 レビュー

9.2 ドラム

9.3 コンポジットIBC

9.4 バルク

9.5 ケルリカン

9.6 ボトル

9.7 ヨーロッパ グルーム に 銀河市場, によって タイプ, 2018-2033 (USD THOUSAND)

9.7.1 プラスチック ドラム(HDPE)

9.7.2 TIGHT-HEADドラム

9.7.3 LINERSインサイドドラム

9.7.4 化学的適合性コーティングによる破棄

9.7.5 営業トップ ドラム

9.8 EUROPE DRUMS で 銀河市場, によって REGION, 2018-2033 (USD THOUSAND)

9.8.1 アジアパシフィック

9.8.2 北アメリカ

9.8.3 ヨーロッパ

9.8.4 中東・アフリカ

9.8.5 南アフリカ

9.9 ユーロスコープコンポジットIBC in グリオクサル マーケット, タイプ別, 2018-2033 (USD THOUSAND)

9.9.1 作曲 IBCS

9.9.2 ライギド IBCS

9.9.3 INSULATIONのIBCS

9.9.4 その他

9.1 EUROPEコンポジットIBC in GLYOXAL MARKET, REGION, 2018-2033 (USD THOUSAND)

9.10.1 アジアパシフィック

9.10.2 ノースアメリカ

9.10.3 ヨーロッパ

9.10.4 中東&アフリカ

9.10.5南アフリカ

2018-2033年(USD THOUSAND)、GLYOXAL MARKETで9.11 EUROPE BULK

9.11.1 アジアパシフィック

9.11.2 ノースアメリカ

9.11.3 ヨーロッパ

9.11.4 中東&アフリカ

9.11.5 南アメリカ

2018-2033のタイプによってGLYOXALの市場、の9.12 EUROPEのJERRYCANS、2018-2033 (USD THOUSAND)

9.12.1プラスチックジャーリン

9.12.2 スタッカブル・ジェリカンス

9.12.3 メタル・ジェリカンス

9.12.4 その他のジェリカン

Region、2018-2033(USD THOUSAND)により、GLYOXAL MARKETで9.13 EUROPE JERRYCANS

9.13.1アジアパシフィック

9.13.2 ノースアメリカ

9.13.3 ヨーロッパ

9.13.4 中東&アフリカ

9.13.5 南アメリカ

9.14 グリオクサルの市場、タイプによって、2018-2033 (USD THOUSAND)

9.14.1 スモール・ラボリー・ボトル

9.14.2 化粧品/パーソナルケアの使用容器

9.14.3 特別な特徴の容器

9.14.4 その他のボトル

2018-2033(USD THOUSAND)で、GLYOXAL MARKETで9.15 EUROPE BOTTLES、

9.15.1 アジアパシフィック

9.15.2 ノースアメリカ

9.15.3 ヨーロッパ

9.15.4 中東&アフリカ

9.15.5 南アフリカ

10 EUROPEのGLYOXALの市場、適用による

10.1 概要

10.2 クロスリンク

10.3 ケミカル・インターメディア

10.4 その他

10.5 EUROPE CROSS-LINKING IN GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

10.5.1 GLYOXALATED ポリアクリルアミド (GPAM)

10.5.2 GLYOXALATEDスタート

2018-2033(USD THOUSANDAND)のRegion、GLYOXAL MARKETで10.6 EUROPE クロスリンク

10.6.1 アジアパシフィック

10.6.2 ノースアメリカ

10.6.3 ヨーロッパ

10.6.4 中東・アフリカ

10.6.5 南アフリカ

10.7 EUROPEケミカル、GLYOXAL MARKET、タイプ別、2018-2033(USD THOUSAND)

10.7.1 バルク化学品製造

10.7.2 ポリマー加工

10.8 ヨーロッパ バルク ケムマニュファクチャリング に 銀河 市場, タイプ, 2018-2033 (USD THOUSAND)

10.8.1 2枚入

10.8.2 ETHYLENE グリコール DIFORMATE

10.8.3 QUINOXALINE 開発

10.9 グリオクサル マーケットでのプロセッシング, タイプ別, 2018-2033 (USD THOUSAND)

10.9.1 GLYOXAL 尿素

10.9.2 GLYOXALの容器の樹脂

10.9.3 GLYOXAL-BIS(2-ヒドロキシアンイル)

2018-2033(USD THOUSANDAND)、GLYOXAL MARKETの10.1 EUROPEケミカルインターネット

10.10.1 アジアパシフィック

10.10.2 ノースアメリカ

10.10.3 ヨーロッパ

10.10.4 中東・アフリカ

10.10.5 南アフリカ

10.11 グルクタールの市場におけるヨーロッパ, タイプ別, 2018-2033 (USD THOUSAND)

10.11.1 ジヒドロキシルヌ尿素尿素(DHEU)

10.11.2 メチル グリオカル

2018-2033(USD THOUSAND)、GLYOXAL MARKETの10.12 EUROPE OTHERS

10.12.1 アジアパシフィック

10.12.2 ノースアメリカ

10.12.3 ヨーロッパ

10.12.4 中東・アフリカ

10.12.5 南アフリカ

11 EUROPEのGLYOXALの市場、エンド ユースの化学薬品による

11.1 概要

11.2 ディヒドロキシルヌ尿素尿素(DHEU)

11.3 2-イミダゾーリドン

11.4 GLYOXALATED ポリアクリルアミド (GPAM)

11.5 グリオキシル酸

11.6 GLYOXALATEDスタート

11.7 GLYOXALの容器の樹脂

11.8 GLYOXAL 尿素

11.9 ETHYLENE グリコール DIFORMATE

11.1 尿 - 亜鉛めっき

11.11 QUINOXALINE 開発

11.12 メチル グリオカル

11.13 GLYOXAL-BIS(2-ヒドロキシアンイル)

11.14 GLYOXAL SODIUM ビスフルト

11.15 キノクライン

11.16 2-メタリミダゾール

11.17 イミダゾール

11.18 グリコール

11.19 アラントイン

11.2 テトラメチル ACETYLENEDIUREA

2018-2033(USD THOUSAND)、GLYOXAL MARKETで11.21 EUROPEディヒドロキシエシレン尿素尿素(DHEU)

11.21.1 アジアパシフィック

11.21.2 ノースアメリカ

11.21.3 ヨーロッパ

11.21.4 中東・アフリカ

11.21.5 南アメリカ

2018-2033(USD THOUSANDAND)、11.22 EUROPE 2-IMIDAZOLIDINONE、GLYOXAL MARKET, BY REGION, 2018-2033(USD THOUSAND)で

11.22.1 アジアパシフィック

11.22.2 ノースアメリカ

11.22.3 ヨーロッパ

11.22.4 中東・アフリカ

11.22.5 南アフリカ

11.23 EUROPE GLYOXALATED POLYACRYLAMIDE (GPAM) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) (USD THOUSAND) (USD THOUSAND)) のユーロスコープのGLYOXALATED POLYACRYLAMIDE (GPAM)

11.23.1 アジアパシフィック

11.23.2 ノースアメリカ

11.23.3 ヨーロッパ

11.23.4 中東・アフリカ

11.23.5 南アフリカ

Region、2018-2033(USD THOUSAND)によるGLYOXAL MARKETの11.24 EUROPE GLYOXYLIC ACID

11.24.1 アジアパシフィック

11.24.2 ノースアメリカ

11.24.3 ヨーロッパ

11.24.4 中東・アフリカ

11.24.5 南アフリカ

11.25 EUROPE GLYOXALATEDがGLYOXAL MARKETで始まります, REGIONによって, 2018-2033 (USD THOUSAND)

11.25.1 アジアパシフィック

11.25.2 ノースアメリカ

11.25.3 ヨーロッパ

11.25.4 中東・アフリカ

11.25.5 南アフリカ

2018-2033(USD THOUSAND) - 11.26 EUROPE GLYOXAL PHENOL RESIN in GLYOXAL MARKET - ポルトガル

11.26.1 アジアパシフィック

11.26.2 ノースアメリカ

11.26.3 ヨーロッパ

11.26.4 中東・アフリカ

11.26.5 南アフリカ

2018-2033 (USD THOUSAND) - 11.27 EUROPE GLYOXAL 尿素は、GLYOXAL MARKET、REGION、による

11.27.1 アジアパシフィック

11.27.2 ノースアメリカ

11.27.3 ヨーロッパ

11.27.4 中東・アフリカ

11.27.5 南アフリカ

2018-2033 (USD THOUSAND) - 11.28 EUROPE ETHYLENE GLYCOL DIFORMATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - ポルトガル

11.28.1 アジアパシフィック

11.28.2 ノースアメリカ

11.28.3 ヨーロッパ

11.28.4 中東とアフリカ

11.28.5 南アフリカ

2018-2033 (USD THOUSAND) - 11.29 EUROPE UREA-GLYOXAL の公式アカウント

11.29.1 アジアパシフィック

11.29.2 ノースアメリカ

11.29.3 ヨーロッパ

11.29.4 中東とアフリカ

11.29.5 南アフリカ

11.3 EUROPE QUINOXALINEは、GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) で運営しています。

11.30.1 アジアパシフィック

11.30.2 ノースアメリカ

11.30.3 ヨーロッパ

11.30.4 中東・アフリカ

11.30.5 南アフリカ

2018-2033 (USD THOUSANDAND) - 11.31 EUROPE METHYLOL GLYOXAL(グリクサル) - ポルトガル

11.31.1 アジアパシフィック

11.31.2 ノースアメリカ

11.31.3 ヨーロッパ

11.31.4 中東・アフリカ

11.31.5 南アメリカ

2018-2033(USD THOUSAND)で11.32 EUROPE GLYOXAL-BIS(2-HYDROXYANIL)

11.32.1 アジアパシフィック

11.32.2 ノースアメリカ

11.32.3 ヨーロッパ

11.32.4 中東・アフリカ

11.32.5 南アフリカ

2018-2033(USD THOUSAND)、GLYOXAL MARKETで11.33 EUROPE GLYOXAL SODIUM BISULFITE

11.33.1 アジアパシフィック

11.33.2 北アメリカ

11.33.3 ヨーロッパ

11.33.4 中東&アフリカ

11.33.5 南アメリカ

Region、2018-2033(USD THOUSAND)によるGLYOXAL MARKETの11.34 EUROPE QUINOXALINE

11.34.1 アジアパシフィック

11.34.2 ノースアメリカ

11.34.3 ヨーロッパ

11.34.4 中東とアフリカ

11.34.5 南アフリカ

11.35 EUROPE 2-METHYLIMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSANDAND), ポルトガル

11.35.1 アジアパシフィック

11.35.2 ノースアメリカ

11.35.3 ヨーロッパ

11.35.4 中東とアフリカ

11.35.5 南アフリカ

2018-2033 (USD THOUSAND) - 11.36 EUROPE IMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - ポルトガル

11.36.1 アジアパシフィック

11.36.2 ノースアメリカ

11.36.3 ヨーロッパ

11.36.4 中東・アフリカ

11.36.5 南アフリカ

Region、2018-2033(USD THOUSAND)によるGLYOXAL MARKETの11.37 EUROPE GLYCOLURIL

11.37.1 アジアパシフィック

11.37.2 ノースアメリカ

11.37.3 ヨーロッパ

11.37.4 中東・アフリカ

11.37.5 南アフリカ

2018-2033(USD THOUSAND)で、GLYOXAL MARKETで11.38 EUROPEアラントニン、

11.38.1 アジアパシフィック

11.38.2 ノースアメリカ

11.38.3 ヨーロッパ

11.38.4 中東とアフリカ

11.38.5 南アフリカ

2018-2033 (USD THOUSAND) - 11.39 EUROPE TETRAMETHYLOL ACETYLENEDIUREA(グリクサル)

11.39.1 アジアパシフィック

11.39.2 ノースアメリカ

11.39.3 ヨーロッパ

11.39.4 中東とアフリカ

11.39.5 南アフリカ

12 EUROPE GLYOXAL MARKET、エンドユーザーによる

12.1 概要

12.2 テキスタイル

12.3 PULPおよびペーパー

12.4 レザー

12.5 パインとコーティング

12.6 水処理

12.7 医薬品

12.8 ハウスホールド製品

12.9 化粧品とパーソナルケア

12.1 包装

12.11 電気および電子工学

12.12 オイルおよびガス

12.13 その他

2018-2033年(USD THOUSAND)、GLYOXAL MARKETの12.14 EUROPE TEXTILE

12.14.1 アジアパシフィック

12.14.2 北アメリカ

12.14.3 ヨーロッパ

12.14.4 中東とアフリカ

12.14.5 南アフリカ

12.15 EUROPE PULP and PAPER IN GLYOXAL MARKET, REGION, 2018-2033 (米ドル)

12.15.1 アジアパシフィック

12.15.2 ノースアメリカ

12.15.3 ヨーロッパ

12.15.4 中東・アフリカ

12.15.5 南アフリカ

2018-2033年(USD THOUSAND)、GLYOXAL MARKETの12.16 EUROPE LEATHER

12.16.1 アジアパシフィック

12.16.2 ノースアメリカ

12.16.3 ヨーロッパ

12.16.4 中東・アフリカ

12.16.5 南アフリカ

2018-2033(USD THOUSANDAND)で、GLYOXAL MARKETで12.17 EUROPE PAINTSとCOATINGS

12.17.1 アジアパシフィック

12.17.2 ノースアメリカ

12.17.3 ヨーロッパ

12.17.4 中東・アフリカ

12.17.5 南アフリカ

12.18 グリオクサルの市場におけるヨーロッパの水処理, REGION, 2018-2033 (USD THOUSAND)

12.18.1 アジアパシフィック

12.18.2 ノースアメリカ

12.18.3 ヨーロッパ

12.18.4 中東・アフリカ

12.18.5 南アフリカ

2018-2033(USD THOUSANDAND)のRegion、GLYOXAL MARKETの12.19 EUROPEの医薬品

12.19.1 アジアパシフィック

12.19.2 ノースアメリカ

12.19.3 ヨーロッパ

12.19.4 中東とアフリカ

12.19.5 南アフリカ

2018-2033年(USD THOUSAND)で12.2 EUROPE HOUSEHOLD製品

12.20.1 アジアパシフィック

12.20.2 ノースアメリカ

12.20.3 ヨーロッパ

12.20.4 中東・アフリカ

12.20.5 南アフリカ

12.21 ヨーロッパ化粧品および地方の市場、タイプによって、2018-2033 (米ドル)

12.21.1 ローションとクリーム

12.21.2 利用目的と保証

12.21.3 その他

12.22 ヨーロッパ化粧品と地域別市場における個人ケア, 2018-2033 (USD THOUSAND)

12.22.1 アジアパシフィック

12.22.2 ノースアメリカ

12.22.3 ヨーロッパ

12.22.4 中東・アフリカ

12.22.5 南アメリカ

2018-2033年(USD THOUSAND)で12.23 EUROPE PACKAGING IN GLYOXAL MARKET, BY REGION, 2018-2033

12.23.1 アジアパシフィック

12.23.2 ノースアメリカ

12.23.3 ヨーロッパ

12.23.4 中東・アフリカ

12.23.5 南アメリカ

12.24 EUROPE GLYOXAL MARKET、REGION、2018-2033(USD THOUSANDAND)の電動および電気電子機器

12.24.1 アジアパシフィック

12.24.2 ノースアメリカ

12.24.3 ヨーロッパ

12.24.4 中東・アフリカ

12.24.5 南アフリカ

12.25 EUROPE 油とガス に 銀河 市場, REGION, 2018-2033 (USD THOUSAND)

12.25.1 アジアパシフィック

12.25.2 ノースアメリカ

12.25.3 ヨーロッパ

12.25.4 中東・アフリカ

12.25.5 南アフリカ

12.26 グルクタール市場におけるヨーロッパ, 地域別, 2018-2033 (USD THOUSAND)

12.26.1 アジアパシフィック

12.26.2 ノースアメリカ

12.26.3 ヨーロッパ

12.26.4 中東・アフリカ

12.26.5 南アフリカ

13 EUROPE GLYOXALの市場、REGIONによる

13.1 ヨーロッパ

13.1.1 ドイツ

13.1.2 アメリカ

13.1.3 イタリア

13.1.4 フランス

13.1.5 ロシア

13.1.6 スペイン

13.1.7 スイス

13.1.8 オランダ

13.1.9 ターキー

13.1.10 ベルギー

13.1.11 デンマーク

13.1.12 スウェーデン

13.1.13 ノーウェイ

EUROPEの13.1.14のREST

14 EUROPE GLYOXALの市場、会社LANDSCAPE

14.1 会社案内:グローバル

15 SWOT分析

16 会社案内

16.1 BASFの

16.1.1 会社案内 SNAPSHOT

16.1.2 到着分析

16.1.3 製品ポートフォリオ

16.1.4 最近の開発

16.2 マーク KGAA

16.2.1 会社案内 SNAPSHOT

16.2.2 再燃分析

16.2.3 製品ポートフォリオ

16.2.4 最近の開発

16.3 サーモフィッシャー科学株式会社

16.3.1 会社案内 SNAPSHOT

16.3.2 到着分析

16.3.3 製品ポートフォリオ

16.3.4 最近の開発

16.4 WEYLCHEMインターナショナル合同会社

16.4.1 会社案内

16.4.2 製品ポートフォリオ

16.4.3 最近の開発

16.5 アルファ ケミカ。

16.5.1 会社案内 SNAPSHOT

16.5.2 製品ポートフォリオ

16.5.3 最近の開発

16.6 AMZOLEインドPVT。株式会社

16.6.1 会社案内 SNAPSHOT

16.6.2 製品ポートフォリオ

16.6.3 最近の開発

16.7 EMCOの染料TUFF

16.7.1 会社案内 SNAPSHOT

16.7.2 製品ポートフォリオ

16.7.3 最近の開発

16.8 限られるFLUOROCHEM

16.8.1 カンパニースナプショット

16.8.2 製品ポートフォリオ

16.8.3 最近の開発

16.9 富士フイルム和光純正株式会社

16.9.1 会社案内 SNAPSHOT

16.9.2 製品ポートフォリオ

16.9.3 最近の開発

16.1 GETCHEM株式会社

16.10.1 会社名 SNAPSHOT

16.10.2 製品ポートフォリオ

16.10.3 最近の開発

16.11 グローバルライフサイエンスリミテッド

16.11.1 会社案内 SNAPSHOT

16.11.2 製品ポートフォリオ

16.11.3 最近の開発

16.12 HANNA EQUIPMENTS(インド)PVT。 お問い合わせ

16.12.1 会社案内 SNAPSHOT

16.12.2 製品ポートフォリオ

16.12.3 最近の開発

16.13 HEZE RUNQUANケミカル株式会社

16.13.1 会社名 SNAPSHOT

16.13.2 製品ポートフォリオ

16.13.3 最近の開発

16.14 ヒメディア研究所

16.14.1 会社名 SNAPSHOT

16.14.2 製品ポートフォリオ

16.14.3 最近の開発

16.15 HUBEI SHUNHUI バイオテクノロジー株式会社

16.15.1 会社案内 SNAPSHOT

16.15.2製品ポートフォリオ

16.15.3 最近の開発

16.16 KANTO KAGAKU(カガク)

16.16.11 会社名 SNAPSHOT

16.16.2 製品ポートフォリオ

16.16.3 最近の開発

16.17 ケミラ

16.17.1 会社の SNAPSHOT

16.17.2 到着分析

16.17.3 製品ポートフォリオ

16.17.4 最近の開発

16.18 LOBACHEMIE PVT(ロバッチェミー)

16.18.1 会社の SNAPSHOT

16.18.2 製品ポートフォリオ

16.18.3 最近の開発

16.19 MERU CHEM PVT.LTD.(株)ムルケム

16.19.1 会社案内 SNAPSHOT

16.19.2 製品ポートフォリオ

16.19.3 最近の開発

16.2 マルティッチ・スペシャリスト リミテッド

16.20.1 会社名 SNAPSHOT

16.20.2製品ポートフォリオ

16.20.3 最近の開発

16.21 OTTOケミカルPVT

16.21.1 会社案内 SNAPSHOT

16.21.2 製品ポートフォリオ

16.21.3 最近の開発

16.22 OXFORD LABファインケミカルLP

16.22.1 会社名 SNAPSHOT

16.22.2 製品ポートフォリオ

16.22.3 最近の開発

16.23 三田カルツバイオテクノロジー株式会社

16.23.1 会社名 SNAPSHOT

16.23.2製品ポートフォリオ

16.23.3 最近の開発

16.24 SHANDONG ZHISHANG の化学工業 CO.LTD、

16.24.1 会社名 SNAPSHOT

16.24.2 製品ポートフォリオ

16.24.3 最近の開発

16.25 SIHAULIケミカルズ PRIVATE LIMITED

16.25.1 会社名 SNAPSHOT

16.25.25.2製品ポートフォリオ

16.25.3 最近の開発

16.26 シルバーフェンケミカル合同会社

16.26.1 会社案内 SNAPSHOT

16.26.26.2 製品のポートフォリオ

16.26.3 最近の開発

16.27 シムソンファーマリミテッド

16.27.1 会社の SNAPSHOT

16.27.2製品ポートフォリオ

16.27.3 最近の開発

16.28 東京ケミカル工業株式会社

16.28.1 会社のSNAPSHOT

16.28.2 製品ポートフォリオ

16.28.3 最近の開発

16.29 ユニバーソリューションズ合同会社

16.29.1 会社案内

16.29.2 製品ポートフォリオ

16.29.3 最近の開発

16.3 ウシランセンケミカル株式会社

16.30.1 会社の SNAPSHOT

16.30.2 製品ポートフォリオ

16.30.3 最近の開発

17 質問会議

18 関連するレポート

表のリスト

表1 MAJOR ENDはGLYOXALのためのプロダクトを使用します

TABLE 2 EUROPEのGLYOXALの市場、GRADEによって、2018-2033 (USD THOUSAND)

TABLE 3 EUROPEのGLYOXALの市場、GRADEによって、2018-2033 (THOUSAND TONS)

TABLE 4 EUROPE INDUSTRIAL GRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - ポルトガル

TABLE 5 EUROPE PHARMACEUTICAL GRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - ポルトガル

TABLE 6 EUROPE GLYOXAL の市場、PURITY によって、 2018-2033 (USD THOUSAND)

TABLE 7 EUROPE 40%-60% GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) で購入

TABLE 8 EUROPE 90%-99%のGLYOXALの市場、REGIONによって、2018-2033 (USD THOUSAND)

2018-2033(USD THOUSAND)で、GLYOXAL MARKETのTABLE 9 EUROPE OTHERS、

TABLE 10 EUROPE GLYOXALの市場、生産の工程によって、2018-2033 (USD THOUSAND)

TABLE 11 ヨーロッパ タリスティック グリクサル マルケットのエチル グリコールのオキシドレーション, REGION, 2018-2033 (USD THOUSAND)

2018-2033(USD THOUSAND)、GLYOXAL MARKETでACETYLENEのケーブル12ユーロオクシエーション

TABLE 13 グリオクサル マーケットのヨーロッパ, REGION, 2018-2033 (USD THOUSAND)

TABLE 14 EUROPE GLYOXALの市場、包装によって、 2018-2033 (USD THOUSAND)

TABLE 15 EUROPE DRUMS IN GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 16 EUROPE DRUMS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 17 EUROPEコンポジットIBC、タイプ別、2018-2033(USD THOUSAND)

TABLE 18 EUROPEコンポジットIBC in GLYOXAL MARKET, REGION, 2018-2033 (USD THOUSANDAND) により

TABLE 19 EUROPE BULK IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 20 EUROPE JERRYCANS IN GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 21 EUROPE JERRYCANS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - ポルトガル

TABLE 22 グリオクサルの市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 23 EUROPEのバスケット、REGION、2018-2033 (USD THOUSAND)

TABLE 24 EUROPE GLYOXALの市場、適用によって、2018-2033 (USD THOUSAND)

TABLE 25 EUROPE CROSS-LINKING IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 26 EUROPE CROSS-LINKING IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSANDAND), ポルトガル

TABLE 27 EUROPEケミカル、GLYOXAL MARKET、TYPE、2018-2033(USD THOUSAND)で

TABLE 28 EUROPE BULK CHEMICALSがGLYOXAL MARKETで開催されます。

TABLE29 EUROPEポリマーは、タイプによって、GLYOXALの市場、2018-2033 (USD THOUSAND)で処理します

TABLE 30 EUROPE GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - ポルトガル

TABLE 31 グリオクサル マーケットのヨーロッパ, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 32 EUROPE 地域別市場, 2018-2033 (USD THOUSAND)

TABLE 33 EUROPE GLYOXAL MARKET, エンドユースケミカルズによって, 2018-2033 (USD THOUSAND)

TABLE 34 EUROPE DIHYDROXYETHYLENE UREA (DHEU) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) (USD THAND)

TABLE 35 EUROPE 2-IMIDAZOLIDINONE、GLYOXAL MARKET、REGION、2018-2033(USD THOUSAND)で

TABLE 36 EUROPE GLYOXALATED POLYACRYLAMIDE (GPAM) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) (USD THOUSAND) (USD THOUSAND)) (USD THAND)) (USD THAND)) (USD THAND)) (USD THAND) (USD THAND)) (USD THAND)) (USD THAND) (USD THAND)) (USD))))

TABLE 37 EUROPE GLYOXYLICは、地域別、2018-2033(USD THOUSAND)で取引

TABLE 38 EUROPE GLYOXALATEDは、GLYOXAL MARKETで始まります, REGIONによって, 2018-2033 (USD THOUSAND)

TABLE 39 EUROPE GLYOXAL PHENOL GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - ポルトガル

TABLE 40 EUROPE GLYOXAL UREAは、GLYOXAL MARKET、REGION、2018-2033(USD THOUSAND)の4つです。

TABLE 41 EUROPE ETHYLENE GLYCOL DIFORMATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - ポルトガル

TABLE 42 EUROPE UREA-GLYOXAL BERTATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) により

TABLE 43 EUROPE QUINOXALINEは、GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) で開発されました。

TABLE 44 EUROPE METHYLOL GLYOXAL IN GLYOXAL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) (USD THOUSAND) (USD THOUSAND)) - 現金でのお支払い方法

TABLE 45 EUROPE GLYOXAL-BIS(2-HYDROXYANIL)、REGION、2018-2033(USD THOUSAND)で

TABLE 46 EUROPE GLYOXAL SODIUM BISULFITE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) (USD THOUSAND) (USD THOUSAND)) - ベストプライス ▷ FC-Moto

TABLE 47 EUROPE QUINOXALINE in GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSANDAND), ポルトガル

TABLE 48 EUROPE 2-METHYLIMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 49 EUROPE IMIDAZOLE IN GLYOXAL MARKET, REGION, 2018-2033 (USD THOUSAND) - ポルトガル

TABLE 50 EUROPE GLYCOLURIL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - ポルトガル

TABLE 51 EUROPE アリオシン に グリオクサル マーケット, によって REGION, 2018-2033 (USD THOUSAND)

TABLE 52 EUROPE TETRAMETHYLOL ACETYLENEDIUREA IN GLYOXAL MARKET, BY REGION, 2018-2033 (米ドル THOUSAND)

TABLE 53 EUROPE GLYOXAL MARKET、エンドユーザーによる、2018-2033(USD THOUSAND)

TABLE 54 EUROPE TEXTILE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - ベストプライス ▷ FC-Moto

TABLE 55 EUROPE PULP and PAPER IN GLYOXAL MARKET, REGION, 2018-2033 (USD THOUSANDAND) により

TABLE 56 グリオクショナル・マーケットのヨーロッパ, REGION, 2018-2033 (USD THOUSAND)

TABLE 57 EUROPE PAINTSとCOATINGS IN GLYOXAL MARKET, REGION, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 58 グリオクサル マーケットでのヨーロッパ水処理, 地域別, 2018-2033 (USD THOUSAND)

TABLE 59 EUROPE PHARMACEUTICALS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSANDAND) - ポルトガル

TABLE 60 EUROPE HOUSEHOLDは、GLYOXAL MARKET、REGION、2018-2033(USD THOUSAND)で製品を製造しています。

TABLE 61 ヨーロッパ化粧品および地方の市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 62 ヨーロッパ化粧品と地域別市場における個人ケア, 2018-2033 (USD THOUSAND)

調整可能な63のヨーロッパのパッケージ、地域別、2018-2033(USD THOUSAND)

TABLE 64 EUROPE GLYOXAL MARKET, REGION, 2018-2033 (USD THOUSAND)の電動および電子機器

TABLE 65 EUROPE OIL と ガス に GLYOXAL MARKET, REGION, 2018-2033 (USD THOUSAND)

TABLE 66 EUROPE OTHERS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 67 EUROPE GLYOXAL MARKET, カントリー, 2018-2033 (USD THOUSAND)

TABLE 68 EUROPE GLYOXAL MARKET, BY COUNTRY, 2018-2033 (THOUSAND TONS) - 現金自動預け払い機

テーブル 69 ヨーロッパ

TABLE 70 EUROPEのGLYOXALの市場、GRADEによって、2018-2033 (USD THOUSAND)

TABLE 71 EUROPEのGLYOXALの市場、GRADEによって、2018-2033 (THOUSAND TONS)

TABLE 72 EUROPE GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND), キプロス

TABLE 73 EUROPEのGLYOXALの市場、生産のプロセスによって、2018-2033 (USD THOUSAND)

TABLE 74 EUROPEのGLYOXALの市場、包装によって、2018-2033 (USD THOUSAND)

TABLE 75 EUROPE DRUMS IN GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 76 EUROPEコンポジットIBC in GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 77 EUROPE JERRYCANS IN GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 78 EUROPEのバスケット、タイプによって、2018-2033 (USD THOUSAND)

TABLE 79 EUROPE GLYOXALの市場、適用によって、2018-2033 (USD THOUSAND)

TABLE 80 EUROPE CROSS-LINKING IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 81 EUROPEケミカル、GLYOXAL MARKET、TYPE、2018-2033(USD THOUSAND)

TABLE 82 EUROPE BULK CHEMICALSは、タイプによって、GLYOXALの市場、2018-2033(USD THOUSAND)で測定します

TABLE 83 EUROPE ポリ塩化物、タイプによって、2018-2033 (USD THOUSAND)

TABLE 84 グリオクサル マーケットのヨーロッパ, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 85 EUROPE GLYOXAL MARKET, エンドユースケミカルズによって, 2018-2033 (USD THOUSAND)

TABLE 86 EUROPE GLYOXAL MARKET, エンドユーザーによる, 2018-2033 (USD THOUSAND)

TABLE 87 EUROPEの化粧品および個人はタイプによって、2018-2033 (USD THOUSAND)グリコール マーケット、

TABLE 88 GERMANY GLYOXAL MARKET, グレード, 2018-2033 (USD THOUSAND)

TABLE 89 GERMANY GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS) - ポルトガル

TABLE 90 GERMANY GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND), ドイツ

TABLE 91 GERMANY GLYOXAL MARKET, by PRODUCTION PROCESS, 2018-2033 (USD THOUSAND), ポルトガル

TABLE 92 GERMANY GLYOXAL の市場、包装によって、 2018-2033 (USD THOUSAND)

TABLE 93 ゲルマニー ドレス に 銀河 市場, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 94 GERMANYコンポジットIBC in GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 95 ゲルマニ・ジェリカンス・イン・グリオカル・マーケット, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 96 グリオクサル マーケットのドイツびん、タイプによって、2018-2033 (USD THOUSAND)

TABLE 97 GERMANY GLYOXAL の市場、適用によって、 2018-2033 (USD THOUSAND)

TABLE 98 GERMANY CROSS-LINKING IN GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 99 GERMANY CHEMICAL INTERMEDIATES, IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 100 GERMANY BULK CHEMICALS グルクサル マーケット、タイプによって、2018-2033 (USD THOUSAND)

TABLE 101 GERMANY POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSANDAND) - ポルトガル

TABLE 102 GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) のドイツ その他

TABLE 103 GERMANY GLYOXAL MARKET, エンドユースケミカルズ, 2018-2033 (USD THOUSAND)

TABLE 104 GERMANY GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND), ドイツ

TABLE 105 ゲルマニー化粧品と腹部の市場におけるパーソナルケア, タイプ, 2018-2033 (USD THOUSAND)

TABLE 106 U.K. GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND), ポルトガル

TABLE 107 U.K. GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS), ポルトガル

TABLE 108 U.K. GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 109 U.K. GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 110 U.K. GLYOXAL の市場、包装によって、 2018-2033 (USD THOUSAND)

TABLE 111 U.K. グリオクサルの市場、タイプによって、 2018-2033 (USD THOUSAND)

TABLE 112 U.K. グリオクサルの市場におけるコンポジットIBC, 種類別, 2018-2033 (USD THOUSAND)

TABLE 113 U.K. GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)のJERRYCANS

TABLE 114 U.K. BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 115 U.K. GLYOXAL の市場、適用によって、2018-2033 (USD THOUSAND)

TABLE 116 U.K. クロスリンク による 銀河市場, タイプ, 2018-2033 (USD THOUSAND)

TABLE 117 U.K. ケミカル・インターメディア、GLYOXAL MARKET、TYPE、2018-2033(USD THOUSAND)

TABLE 118 U.K. BULK CHEMICALS グルクサール マーケット, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 119 U.K. オリンピック マーケットでのポリマー処理, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 120 U.K. OTHERS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金の支払い

TABLE 121 U.K. GLYOXAL MARKET, BY END-USE CHEMICALS, 2018-2033 (USD THOUSAND) - 公式ウェブサイト

TABLE 122 U.K. GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND) - 公式ウェブサイト

TABLE 123 U.K.の化粧品および個人はタイプによって、2018-2033 (USD THOUSAND)グリコール マーケット、

TABLE 124 イタリア オリンピック マーケット、GRADE、2018-2033 (USD THOUSAND)

TABLE 125イタリア オリンピック マーケット、GRADE、2018-2033(Thousand TONS)

TABLE 126 イタリア オリンピック マーケット、PURITY、2018-2033 (USD THOUSAND)

TABLE 127 イタリア オリンピック マーケット、生産プロセスによる 2018-2033 (USD THOUSAND)

TABLE 128イタリア・GLYOXALの市場、包装によって、2018-2033 (USD THOUSAND)

TABLE 129 LYOXAL の市場、タイプによって、 2018-2033 (米ドル THOUSAND)

TABLE 130イタリアコンポジットIBC in GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 131 イタリアのジェリカン に 銀河市場, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 132 イタリア 車両 に 銀河 市場, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 133イタリア オリンピック マーケット、適用によって、2018-2033 (USD THOUSAND)

TABLE 134 イタリア 十字リンク によって 銀河 市場, タイプ, 2018-2033 (USD THOUSAND)

TABLE 135 イタリア ケミカル インターメディア、GLYOXAL マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 136 イタリアのバルクケミカルは、型によって、GLYOXAL の市場、2018-2033 (USD THOUSAND)

TABLE 137 イタリア ポリエステル 輸送 に 銀河 市場, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 138 LYOXAL の市場、タイプによって、 2018-2033 (USD THOUSAND)

TABLE 139 イタリア オリンピック マーケット、エンドユース ケミカルズ、2018-2033 (USD THOUSAND)

TABLE 140イタリア・グリオカル・チケット, エンド・ユーザーによる, 2018-2033 (USD THOUSAND)

TABLE 141イタリア化粧品および地方の市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 142 フランチェスコの市場, によって グレード, 2018-2033 (USD THOUSAND)

TABLE 143 FRANCE GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS) 中古建機の通販専門店

TABLE 144 フランス オリンピック マーケット、PURITY, 2018-2033 (USD THOUSAND)

TABLE 145 FRANCE GLYOXAL MARKET(生産プロセスによる)、2018-2033(USD THOUSAND)

TABLE 146 FRANCE GLYOXAL MARKET, パックイング, 2018-2033 (USD THOUSAND)

TABLE 147 FRANCE DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金でのお支払い

TABLE 148 FRANCEコンポジットIBC in GLYOXAL MARKET, 種類別, 2018-2033 (USD THOUSAND)

TABLE 149 FRANCE JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 150 FRANCE BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金でのお支払い

TABLE 151 FRANCE GLYOXAL MARKET, による 応用, 2018-2033 (USD THOUSAND)

TABLE 152 FRANCE CROSS-LINKING IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 153 フランス ケミカル インターメディア、GLYOXAL マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 154 FRANCE BULK CHEMICALSは、GLYOXAL MARKET、TYPE、2018-2033(USD THOUSAND)で製造されています。

TABLE 155 FRANCE ポリマーは、GLYOXAL の市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 156 グリオクサル マーケットの他の部分, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 157 FRANCE GLYOXAL MARKET, エンドユースケミカルズ, 2018-2033 (USD THOUSAND)

TABLE 158 FRANCE GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 159 FRANCE 化粧品と地上階の商業施設, 種類別, 2018-2033 (USD THOUSAND)

TABLE 160 RUSSIA GLYOXAL MARKET, グレード, 2018-2033 (USD THOUSAND)

TABLE 161 RUSSIA GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS), オーストラリア

TABLE 162 RUSSIA GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND), オーストラリア

TABLE 163 RUSSIA GLYOXAL MARKET, by PRODUCTION PROCESS, 2018-2033 (USD THOUSAND), ポルトガル

TABLE 164 RUSSIA GLYOXAL の市場、包装によって、2018-2033 (USD THOUSAND)

TABLE 165 RUSSIA DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 166 RUSSIAコンポジットIBC in GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 167 RUSSIA JERRYCANS IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 168 RUSSIA BOTTLES IN GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 169 RUSSIA GLYOXAL の市場、適用によって、2018-2033 (USD THOUSAND)

TABLE 170 RUSSIA CROSS-LINKING IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 171 RUSSIA ケミカル インターメディア、GLYOXAL マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 172 RUSSIA BULK CHEMICALS MANUFACTURING IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 173 RUSSIA 正規販売店、タイプ別、2018-2033(USD THOUSAND)

TABLE 174 RUSSIA OTHERS IN GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 175 RUSSIA GLYOXAL MARKET, エンドユースケミカルズ, 2018-2033 (USD THOUSAND)

TABLE 176 RUSSIA GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND), オーストラリア

TABLE 177 RUSSIAの化粧品および個人はタイプによって、2018-2033 (USD THOUSAND)グリコール マーケット、

TABLE 178 スパンコール マーケット、GRADEによる 2018-2033 (USD THOUSAND)

TABLE 179 スパンコール マーケット、GRADEによる 2018-2033 (Thousand TONS)

TABLE 180 SPAIN GLYOXAL MARKET, by PURITY, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 181 Spain GLYOXAL MARKET, by PRODUCTION PROCESS, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 182 スパンコールの市場, による PACKAGING, 2018-2033 (USD THOUSAND)

TABLE 183 グリオクサルの市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 184 グリオクサール マーケットのスペインのコンポジット IBC, タイプ, 2018-2033 (USD THOUSAND).

TABLE 185 グリオクサルの市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 186 グリオクサールのバスケット、タイプによって、2018-2033 (USD THOUSAND)

TABLE 187 スパンコールの市場, 応用によって, 2018-2033 (USD THOUSAND)

TABLE 188 グリオカル マーケットでのスパンリンク, タイプによって, 2018-2033 (USD THOUSAND).

TABLE 189 スパンケミカル インターメディア、GLYOXAL マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 190 スパン バルクケミカル グルクタール マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 191 グリクサル マーケットでのスパイン ポリマー処理, 種類別, 2018-2033 (USD THOUSAND)

TABLE 192 グリオキシカル マーケットの他、タイプによって、2018-2033 (USD THOUSAND)

TABLE 193 スパンコール市場, エンドユースケミカルズによる, 2018-2033 (USD THOUSAND)

TABLE 194 スパンコール マーケット、エンドユーザーによる 2018-2033 (USD THOUSAND)

テーブル 195 スパン 化粧品および個人はタイプによって、2018-2033 (米ドルのthousand)グリコール マーケット、

TABLE 196 スイス オリンピック マーケット、2018-2033(USD THOUSAND)

TABLE 197 SWITZERLAND GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS) 株式会社ドリックス

TABLE 198スイス・グリオカル・マーケット、2018-2033(USD THOUSAND)

TABLE 199スイス オリンピック マーケット、生産プロセスによる 2018-2033 (USD THOUSAND)

TABLE 200スイス グリオキシカル マーケット, パックイング, 2018-2033 (USD THOUSAND)

TABLE 201 SWITZERLAND DRUMS IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 202スイスコンポジットIBC in GLYOXAL MARKET, BY TYPE, 2018-2033(USD THOUSANDAND) により

TABLE 203 グリクサル マーケットでスイスのジェリカン, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 204 グリオカル マーケットのスイスのブーツ, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 205スイス オリンピック マーケット、適用によって、 2018-2033 (米ドル THOUSAND)

TABLE 206 スイス クロスリンク に 銀河市場, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 207 スイスの中国、GLYOXAL の市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 208スイスバルクケミカルズがグリオクサルのマーケットでマニュファクター、タイプ別、2018-2033(USD THOUSAND)

TABLE 209 スイス ポリ塩化物、タイプによって、2018-2033 (USD THOUSAND)

TABLE 210 グリクサル マーケットのスイス その他, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 211スイス・グリオクショナル・マーケット、2018-2033(USD THOUSANDAND)

TABLE 212スイス・グリオクサール・マルケット、2018-2033(USD THOUSAND)

TABLE 213スイスの化粧品および地方の市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 214 NETHERLANDS GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND), オーストラリア

TABLE 215 NETHERLANDS GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS) ミネソタ日米協会

TABLE 216 NETHERLANDS GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND), オーストラリア

TABLE 217 NETHERLANDS GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND), ポルトガル

TABLE 218 NETHERLANDS GLYOXAL MARKET, バイ PACKAGING, 2018-2033 (USD THOUSAND), ポルトガル

TABLE 219 NETHERLANDS DRUMS IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 220 NETHERLANDS COMPOSITE IBC in GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSANDAND)

TABLE 221 NETHERLANDS JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 222 NETHERLANDS BOTTLES IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 223 オランダ政府の市場、適用によって、2018-2033 (米ドルのThousAND)

TABLE 224 NETHERLANDS CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 225 NETHERLANDS CHEMICAL INTERMEDIATES, IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) ミネソタ日米協会

TABLE 226 NETHERLANDS BULK CHEMICALS グルクサール マーケット、タイプ別、2018-2033(USD THOUSAND)

TABLE 227 NETHERLANDS POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 228 NETHERLANDS を GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 229 NETHERLANDS GLYOXAL MARKET, BY END-USE CHEMICALS, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 230 NETHERLANDS GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 231 オランダの化粧品と地域別商業施設 2018-2033(米ドル)

TABLE 232 TURKEY GLYOXAL の市場、GRADEによって、2018-2033 (USD THOUSAND)

TABLE 233 TURKEY GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS) 株式会社ドリックス

TABLE 234 TURKEY GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 235 TURKEY GLYOXAL の市場、生産のプロセスによって、 2018-2033 (米ドル THOUSAND)

TABLE 236 TURKEY GLYOXAL の市場、包装によって、2018-2033 (USD THOUSAND)

TABLE 237 の TURKEY はタイプによって、 2018-2033 (USD の THOUSAND) GLYOXAL の市場、

TABLE 238 の TURKEY のコンポジット IBC の GLYOXAL の市場、タイプによって、 2018-2033 (米ドル THOUSAND)

TABLE 239 の TURKEY の GLYOXAL の市場、タイプによって、 2018-2033 (米ドル THOUSAND)

TABLE 240 グリオクサルの市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 241 TURKEY GLYOXAL の市場、適用によって、2018-2033 (USD THOUSAND)

TABLE 242 TURKEY CROSS-LINKING IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 243 のトルコの解釈、GLYOXAL の市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 244 TURKEY BULK CHEMICALSは、GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 245 TURKEY ポリカーは、GLYOXAL のマーケット、タイプによって、2018-2033 (USD THOUSAND)

TABLE 246 グリオカル マーケットのターキー マザーズ、タイプによって、2018-2033 (USD THOUSAND)

TABLE 247 TURKEY GLYOXAL MARKET, エンドユースケミカルズ, 2018-2033 (USD THOUSAND)

TABLE 248 TURKEY GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND) - 公式ウェブサイト

TABLE 249のトルコの化粧品および個人はタイプによって、2018-2033 (USD THOUSAND)グリコール マーケット、

TABLE 250のベルギーのGLYOXALの市場、GRADEによって、2018-2033 (USD THOUSAND)

TABLE 251のベルギーのGLYOXALの市場、GRADEによって、2018-2033 (THOUSAND TONS)

TABLE 252のベルギーのGLYOXALの市場、PURITYによって、2018-2033 (USD THOUSAND)

TABLE 253 ベルギー オリンピック マーケット、生産プロセスによる 2018-2033 (USD THOUSAND)

TABLE 254のベルギーのGLYOXALの市場、包装によって、2018-2033 (USD THOUSAND)

TABLE 255のグリオクサルの市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 256 の GLYOXAL の市場、タイプによって、2018-2033 (米ドルの THOUSAND)のベルギーのコンポジット IBC

TABLE 257 の GLYOXAL の市場、タイプによって、2018-2033 (米ドルの THOUSAND) のベルギーのジェリカン

TABLE 258 グリオクサルの市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 259 ベルギーの GLYOXAL の市場、適用によって、 2018-2033 (USD THOUSAND)

TABLE 260の塩化ビウムの十字リンク タイプによって、2018-2033 (USD THOUSAND)

TABLE 261 ベルギー ケミカル インターメディア、GLYOXAL マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 262 ベルギー バルクケミカル グルクタール マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 263 塩化ビウムのポリエステルはタイプによって、2018-2033 (USD THOUSANDAND) GLYOXAL の市場、作ります

TABLE 264 塩化ビウムの他はタイプによって、2018-2033 (USD THOUSAND)

TABLE 265 BELGIUM GLYOXAL MARKET, エンドユースケミカルズ, 2018-2033 (USD THOUSAND)

TABLE 266のベルギーのGLYOXALの市場、エンド ユーザーによる、2018-2033 (USD THOUSAND)

TABLE 267 ベルギーの化粧品および個人はタイプによって、2018-2033 (USD THOUSAND)グリコール マーケット、

TABLE 268 DENMARK GLYOXALの市場、GRADEによって、2018-2033 (USD THOUSAND)

TABLE 269 DENMARK GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS) 中古建機・中古建機の買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取・買取

TABLE 270 DENMARK GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 271 DENMARK GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 272 DENMARK GLYOXAL MARKET, バイ PACKAGING, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 273 グリオクサルの市場、タイプによって、 2018-2033 (USD THOUSAND)

TABLE 274 DENMARKコンポジットIBC in GLYOXAL MARKET、タイプ別、2018-2033(USD THOUSAND)

TABLE 275 DENMARK JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 276 グリオクサルの市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 277 DENMARK GLYOXAL の市場、適用によって、2018-2033 (USD THOUSAND)

TABLE 278 DENMARK CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSANDAND) のリンク

TABLE 279 デンマーク ケミカル インターメディア、GLYOXAL マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 280 デンマーク・バルク・ケミカルズ・マニュファクチュアリング・イン・グリオカル・マーケット、2018-2033(USD THOUSAND)

TABLE 281 銀河市場、TYPE、2018-2033(USD THOUSANDAND)で処理するデンマークポリマー

TABLE 282 グリオクサール マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 283 デンマーク・グリオクショナル・マーケット、2018-2033(USD THOUSAND)

TABLE 284 DENMARK GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND) - 公式ウェブサイト

TABLE 285 DENMARK の化粧品および個人はタイプによって、2018-2033 (USD THOUSAND) GLYOXAL の市場、

TABLE 286 SWEDENのGLYOXALの市場、GRADEによって、2018-2033 (USD THOUSAND)

TABLE 287 SWEDEN GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS), ブル・ギャルド・マーケット, ブル・ギャルド, 2018-2033

TABLE 288 SWEDEN GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 289 SWEDEN GLYOXAL MARKET, by PRODUCTION PROCESS, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 290 SWEDEN GLYOXAL の市場、包装によって、2018-2033 (USD THOUSAND)

TABLE 291 SWEDEN DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 292 SWEDENコンポジットIBC in GLYOXAL MARKET、タイプ別、2018-2033(USD THOUSAND)

TABLE 293 グリオカル マーケットのスウェーデンのジェリカン, タイプによって, 2018-2033 (USD THOUSAND)

TABLE 294 SWEDEN BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 295 SWEDEN GLYOXALの市場、適用によって、2018-2033 (USD THOUSAND)

TABLE 296 SWEDEN CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 297 SWEDEN CHEMICAL INTERMEDIATES, IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 298 SWEDEN BULK CHEMICALSは、GLYOXAL MARKET、TYPE、2018-2033(USD THOUSAND)で製造されています。

TABLE 299 グリオキシカル マーケット、TYPE、2018-2033 (USD THOUSAND) のポリエステル処理

TABLE 300 グリオクサール マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 301 SWEDEN GLYOXAL MARKET, エンドユースケミカルズ, 2018-2033 (USD THOUSAND)

TABLE 302 SWEDEN GLYOXAL MARKET、エンドユーザーによる、2018-2033(USD THOUSAND)

TABLE 303スウェーデンの化粧品および地方の市場、タイプによって、2018-2033 (USD THOUSAND)

TABLE 304 NORWAY GLYOXAL MARKET, グレード, 2018-2033 (USD THOUSAND)

TABLE 305 NORWAY GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS), ブル 305 ノーウェイ オリンピック マーケット, グレード, 2018-2033 (THOUSAND TONS)

TABLE 306 NORWAY GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND), キプロス

TABLE 307 NORWAY GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND), ポルトガル

TABLE 308 NORWAY GLYOXAL の市場、包装によって、2018-2033 (USD THOUSAND)

TABLE 309 NORWAY DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 310 ノーウェイコンポジット IBC in グリクサル マーケット, タイプ, 2018-2033 (USD THOUSAND)

TABLE 311 ノーウェイ グリクサル マーケット、タイプ別、2018-2033 (USD THOUSAND)

TABLE 312 NORWAY BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 313 NORWAY GLYOXAL MARKET、適用によって、2018-2033 (USD THOUSAND)

TABLE 314 NORWAY CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSANDAND) の口コミを投稿します。

TABLE 315 NORWAY CHEMICAL INTERMEDIATES, IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 316 NORWAY BULK CHEMICALSは、GLYOXAL MARKET、TYPE、2018-2033(USD THOUSAND)で製造されています。

TABLE 317 ノーウェイ オリンピック マーケットでのポリマー処理, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 318 NORWAY OTHERS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND) - 現金自動預け払い機

TABLE 319 NORWAY GLYOXAL MARKET, BY エンドユースケミカルズ, 2018-2033 (USD THOUSAND)

TABLE 320 NORWAY GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND) - 公式ウェブサイト

TABLE 321 ノーウェイ 化粧品および個人ケア によって 銀河市場, タイプ, 2018-2033 (USD THOUSAND)

2018-2033(USD THOUSAND)のGRADE、EUROPE GLYOXAL MARKETのTABLE 322 REST

2018-2033年(Thousand TONS)のGRADE、EUROPE GLYOXAL MARKETのTABLE 323のREST、

2018-2033(USD THOUSAND)のPURITY、EUROPE GLYOXAL MARKETのTABLE 324 REST

2018-2033(USD THOUSANDAND) 生産プロセスによるEUROPE GLYOXAL MARKETのTABLE 325 REST、

2018-2033 (USD THOUSAND) で、EUROPE GLYOXAL MARKET の TABLE 326 REST、

TABLE 327 REST OF EUROPE DRUMS IN GLYOXAL MARKET, タイプ別, 2018-2033 (USD THOUSAND)

TABLE 328 REST OF EUROPEコンポジットIBC in GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

TABLE 329 REST OF EUROPE JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSANDAND) - ベストプライス ▷ FC-Moto

TABLE 330 欧州のバスケットの残りの部分, タイプによって, 2018-2033 (USD THOUSAND)

2018-2033 (USD THOUSAND) の適用によって、EUROPE GLYOXALの市場、の331 REST。

2018-2033(USD THOUSANDAND)タイプにより、GLYOXAL MARKETでEUROPE CROSS-LINKINGの332 RESTをテーブル

TABLE 333 ユーロ通信の残りの部分, によって 銀河市場, タイプ, 2018-2033 (USD THOUSAND)

TABLE 334 欧州バルクケミカルズの残りの部分は、タイプによって、 2018-2033 (USD THOUSAND)

TABLE 335 欧州連合会の残りの部分は、タイプによって、2018-2033 (USD THOUSAND)

TABLE 336 REST OF EUROPE OTHERS IN GLYOXAL MARKET, によって タイプ, 2018-2033 (USD THOUSAND)

エンドユースケミカルズ、2018-2033(USD THOUSAND)によるEUROPE GLYOXAL MARKETのTABLE 3373 REST

エンドユーザーによるEUROPE GLYOXAL MARKETのTABLE 338 REST, 2018-2033 (USD THOUSAND)

2018-2033(USD THOUSANDAND)タイプで、ヨーロッパ化粧品およびパーソナルケアのテーブル339 REST

図表一覧

フィギュア 1 ヨーロッパ オリンピック マーケット: セッション

フィギュア2 EUROPE GLYOXAL MARKET:データ連携

フィギュア 3 ヨーロッパ オリンピック マーケット: DROC ANALYSIS

フィギュア 4 ヨーロッパ オリンピック マーケット: フィリピン VS 地域分析

フィギュア5のヨーロッパのGLYOXALの市場:会社の調査の分析

フィギュア6 EUROPE GLYOXAL マーケット:インタビュー

フィギュア7 EUROPE GLYOXAL マーケット:DBMR マーケット ポジション グリッド

フィギュア8のDBMRのベンダー シャルア分析

フィギュア 9 ヨーロッパ オリンピック マーケット: セッション

フィギュア 10 の執行のまとめ

フィギュア11ストラテジックディシジョン

フィギュア 12 の SIX の沈殿物は EUROPE の GLYOXAL の市場、プロダクトによって(2025) 来ます

2026年から2033年までの2026年から2033年までのヨーロッパ政府の市場を運転することに期待されるクロスリンクとしてGLYOXALの重要な13のRISING UTILIZATION

フィギュア 14 インダストリアル・グレード・セグメントは、2026 & 2033年のヨーロッパ・グリオクサル・マーケットの最大のシェアのために計算されます

フィギュア 15 バルブチェーン分析

フィギュア 16 サプライチェーン分析

フィギュア17 PORTER’S FIVE FORCES ANALYSIS

フィギュア 18 ドライバー, RESTRAINTS, オペラ座とEUROPE GLYOXAL MARKETのチャレンジ

フィギュア19 GLYOXAL MARKET:GRADE, 2025

フィギュア20 GLYOXAL マーケット:2025

フィギュア21 GLYOXAL MARKET: 製作工程で、2025年

フィギュア 22 ヨーロッパ GLYOXAL の市場: 包装によって、2025

フィギュア 23 ヨーロッパ GLYOXAL の市場: 応用によって、2025

フィギュア 24 ユーロ GLYOXAL 市場: エンド ユース ケミカルズ、2025

フィギュア25ユーロ圏市場:エンドユーザーによる、2025

フィギュア 26 ヨーロッパ GLYOXAL 市場: ジオグラフィック分析

フィギュア27のヨーロッパのGLYOXALの市場:会社のシャープ2025の(%)

フィギュア28 EUROPE GLYOXALの市場、SNAPSHOT (2025)

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。