欧州注射可能な医薬品配送市場規模、株式および動向分析レポート

Market Size in USD Billion

CAGR :

%

USD

155.98 Billion

USD

368.64 Billion

2024

2032

USD

155.98 Billion

USD

368.64 Billion

2024

2032

| 2025 –2032 | |

| USD 155.98 Billion | |

| USD 368.64 Billion | |

| % | |

|

欧州注射用医薬品デリバリー市場セグメンテーション、種類別(注射用医薬品デリバリー装置および注射用医薬品デリバリー処方)、利用パターン(治療・免疫・その他)、管理モード(皮膚・循環器・筋骨格・臓器・中枢神経系)、用途(自己免疫疾患・ホルモン障害・眼科疾患・腫瘍学・腫瘍学・その他)、エンドユーザー(病院・医療機関)、医薬品・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬学・薬

ヨーロッパの注射可能な薬剤配達市場のサイズ

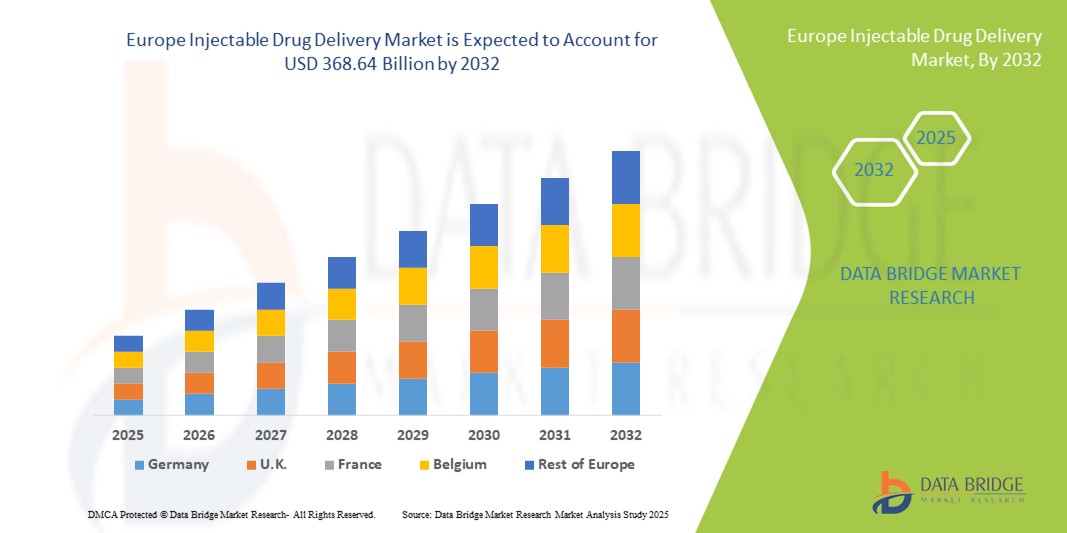

- ヨーロッパの注射可能な薬剤の配達市場のサイズはで評価されましたツイート 155.98 億 に 2024そして到達する予定ツイート 2032年 368.64億, お問い合わせカリフォルニア 11.35%予報期間中

- 市場成長は、慢性疾患の増加の優先順位、自己管理療法の需要の増加、医薬品配信技術の継続的な革新によって主に駆動されます。自動注入器, プレフィルドシリンジとウェアラブルインジェクタ

- さらに、患者中心のヘルスケアソリューションに重点を置き、支持的な規制枠組みとバイオロジカルおよびバイオシミラーの拡大と組み合わせることで、病院とホームケア設定の両方で推奨される選択肢として注射可能な医薬品配送システムを配置しています。 これらの要因は、注射可能な医薬品のデリバリーソリューションの採用を集約して、市場成長を加速する

ヨーロッパの注射可能な薬剤配達市場分析

- デバイスや処方を含む注射可能な医薬品配送システムは、その精度、使いやすさ、および生態学、ワクチン、および病院、診療所、およびホームケア設定に関する高粘度薬との互換性のために、現代の医療にますますます不可欠です

- 注射可能な薬剤の配達のための上昇の要求は主に慢性および孤児の病気の高められた優先順位によって運転され、自己administration療法の採用を高め、安全の、ユーザー フレンドリーおよび統合された配達システムの技術革新を高めます

- ドイツは、2024年に37.2%の最大の収益分配で欧州注射可能な医薬品配達市場を支配しました。先進医療インフラ、バイオロジカルの高い採用、強力な規制枠組み、および主要な市場プレーヤーの重要な存在によって支持され、注射可能な医薬品配送装置と病院および家庭医療における処方の増大率が増加しました。

- イタリアは、ヘルスケア支出の増加、免疫プログラムの普及啓発、および治療および専門的療法の需要の増加による予測期間中、欧州の注射可能な医薬品配信市場で最速成長国であることが期待されます

- 注射可能な薬剤の配達装置の区分は便利、安全および忍耐強い承諾を高める自動注入器、プレフィルドのスポイト、および身につけられる注入器の革新によって運転される2024年に42.8%の市場占有と市場を支配しました

レポートの規模およびヨーロッパの注射可能な薬剤配達市場区分

| アトリビュート | ヨーロッパの注射可能な薬剤配達主市場の洞察 |

| カバーされる区分 |

|

| カバーされた国 | ヨーロッパ

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

ヨーロッパの注射可能な薬剤配達市場の傾向

コネクテッドおよび患者中心デバイスにおける高度化

- 欧州の注射可能な薬剤の配達市場の重要な、加速傾向は自動注入器および身につけられる注入器のような接続された、スマートな配達装置の開発です、実時間監視および高められた忍耐強い付着力を可能にします

- 例えば、接続された自動注入器はヘルスケア プロバイダーに注入データを送信できます、治療の付着力および適量の正確さの遠隔追跡を可能にし、忍耐強い結果を改善します

- デジタルヘルスプラットフォームとの統合により、インジェクションリマインダー、線量ロギング、アラートなどの機能が欠落した線量を可能にします。 たとえば、スマートプレフィルドシリンジは、スマートフォンアプリを介して患者や介護者に通知し、慢性疾患管理の遵守を改善することができます

- このような相互接続配送システムは、患者治療の集中管理を容易にし、グルコースメーターや血圧モニターなどの広範な健康モニタリングツールで注射を統合

- インテリジェントで、患者中心的な、そしてデジタルに接続された注射可能な装置へのこの傾向は治療管理のためのユーザーの期待を変形させます。 その結果、Ypsomedなどの企業は、リアルタイム監視、アプリ接続、および患者様の利便性向上のための線量追跡でスマートインジェクタを開発しています。

- 患者およびヘルスケア提供者が薬物管理の利便性、正確さおよび付着性をます優先するので、接続された、データ処理可能な装置のための要求は病院およびホームケアの設定を渡って急速に成長しています

ヨーロッパの注射可能な薬剤配達市場の動的

ドライバー

慢性疾患および自己適応性環境の普及

- 慢性および自己管理された療法のための忍耐強い好みと結合される自己管理された病気の上昇の優先順位は注射可能な薬剤の伝達システムのための増加の要求のための重要な運転者です

- たとえば、糖尿病やリウマチの患者は、家庭用のオートインジェクターとプレフィルド注射器を採用し、病院の訪問の依存性を減らし、利便性を向上させる

- 注入可能な装置は高められた安全、精密投薬および使用の容易さを提供しま、有効な療法の付着を支え、管理の間違いを減らす。 例えば、線量の記憶のスマートなペンは患者が薬物使用法を正確に追跡することを可能にします

- さらに、患者中心のヘルスケアソリューションとパーソナライズされた治療計画に対する成長の焦点は、家庭で使いやすい注射可能な医薬品配送システムを採用しています。

- 利便性、正確さ、病院の依存性を減らし、患者のエンパワーメントは、病院とホームケアの両方の採用を促進する重要な要因です。 デジタルヘルスインテグレーションとテレメディシンへのトレンドは、市場成長を加速します

拘束/チャレンジ

高デバイスコストと規制コンプライアンス要件

- 高度な注射可能なデバイスと厳格な規制要件の比較的高いコストは、ヨーロッパにおける市場浸透の拡大に大きな課題を提起します。 高度の自動注入器および身につけられる注入器は頻繁に採用を、特に価格に敏感な区分で限ることができる優れた価格設定と来ます

- 例えば、デジタル監視機能を備えたスマートコネクティッドインジェクターは、従来のプレフィルドシリンジよりも高価であり、一部のヘルスケアプロバイダーや患者にとって有益性を懸念しています。

- 安全、有効性、およびデバイス承認プロセスに関する規制ハードルは、市場や開発コストを増加させます。 例えば、EUにおけるMDR(医療機器規制)の遵守には、広範な臨床評価と文書が必要です。

- 患者の安全、デバイスの信頼性、規制遵守を徹底し、コストを管理することは、市場受入に不可欠です。

- 費用対効果の高いデバイス設計、合理化された承認経路、および高度の注射可能なシステムの利点の忍耐強い教育を通してこれらの課題を克服することは、持続的な成長のために不可欠です

ヨーロッパの注射可能な薬剤配達市場規模

市場は、タイプ、使用パターン、管理モード、アプリケーション、エンドユーザー、および配布チャネルに基づいてセグメント化されます。

- タイプ別

タイプに基づいて、ヨーロッパの注射可能な薬剤の配達市場は注射可能な薬剤の配達装置および注射可能な薬剤の配達公式に分けられます。 注射可能な医薬品デリバリーデバイスセグメントは、2024年に42.8%の最大の収益シェアで市場を支配し、自動注入器、プレフィルド注射器、および患者の利便性と接着性を向上させるウェアラブルインジェクタの革新によって駆動しました。 病院や家庭のヘルスケアプロバイダは、精密な投薬を可能にし、誤りを最小限に抑え、自己管理をサポートし、特に慢性および自己免疫疾患の治療のために、デバイスをますますます好む。 デバイスの採用は、監視、リマインダー、および付着力の追跡を提供するデジタルヘルスプラットフォームとの統合によって更に燃料を供給されます。 高粘度バイオロジカルとワクチンに対応した機器の可用性は、従来の処方よりも好みを高めます。 デバイス人間工学、安全性、コネクティビティの大手選手による強力な研究開発投資も市場優位性をサポートします。 大手企業は、リアルタイムのフィードバックと治療監視を可能にし、患者のエンゲージメントを高めるコネクテッドデバイスに焦点を当てています。

注射可能な薬剤の配達公式の区分は、生態学、ワクチンおよび専門薬剤の採用の増加による2025年から2032年までの最も速い成長を目撃すると期待されます。 高濃度の生態学のような安定した、正確および有効な配達を、要求する公式は高度の注射可能な公式のための要求を運転しています。 製薬会社は、ドージング頻度を削減し、患者のコンプライアンスを改善し、家庭管理を可能にする新しい処方に投資しています。 また、Orphan薬および標的療法に対する増加焦点は、特殊な注射可能な処方の必要性を高める。 欧州における新規医薬品やバイオシミラーの規制当局の承認をライジングし、このセグメントの成長をサポートします。 複雑なバイオロジックの拡大パイプラインは、革新的な処方の需要をさらに加速します。

- 使用法パターンによって

使用パターンに基づいて、市場は治療、免疫などの分野に分けられます。 治療分野は、慢性疾患、自己免疫障害、腫瘍学療法のための注射治療の需要が高いため2024年に支配しました。 病院や診療所は、注射可能な治療に依存し、正確で効果的な治療を提供し、自己管理のための患者の好みは、このセグメントを強化します。 ヘルスケアプロバイダーは、管理された投与量を配信し、入院時間を短縮し、治療の遵守を向上させる能力のための注射可能なソリューションを評価します。 セグメントはまた、デバイス人間工学と安全機能の継続的な革新から恩恵を受けています。 治療用アプリケーションは、多くの場合、デジタル監視ツールを活用して、治療成果を最適化し、このセグメントの魅力をさらに高めます。 治療追跡と患者管理を組み合わせた統合医療プラットフォームは、セグメントの成長をサポートします。

免疫組織は、インフルエンザ、COVID-19ブースター、およびその他の予防免疫を含むヨーロッパ各地の予防プログラムを増加させ、予測期間中に最速の成長を目撃する予定です。 充填された注射器および自動注入器は、使用の容易さ、汚染のリスクの低減、および大量免疫キャンペーンの迅速な管理のために好まれています。 予防医療、政府の取り組み、公衆衛生支出の増大の意識を増大させ、このセグメントの拡大を支援します。 企業は、効率的な免疫化要求を満たすために、組み合わせワクチンと革新的な配信フォーマットに投資しています。

- 管理モードによる

管理モードに基づいて、市場は皮膚、循環/筋骨格、臓器、中枢神経系(CNS)に分けられます。 関節炎、心血管の状態および他の全身障害のための注射可能な療法の高い優先性による2024年に分けられた循環/musculoskeletalの区分。 病院およびホームケアの患者は急速な薬物の吸収、精密な投薬および長期作用の公式のための注入をますますますますます好みます。 このセグメントは、自動インジェクターと患者のコンプライアンスを強化し、管理の痛みを最小限に抑えるウェアラブルインジェクターの革新から恩恵を受けます。 デジタルプラットフォームとの統合により、治療従順を追跡し、セグメントを強化します。 慢性筋骨格および心血管の状態の増加の優先順位は長期要求を運転します。 企業は、人間工学に基づいた設計機器を開発し、患者の快適性と使いやすさを改善しています。

CNSセグメントは、神経疾患の早期増加による予測期間における最速成長を目撃し、複数の脊柱症やパーキンソン病などのCNS条件を標的とした注射療法の採用を高めることが期待されます。 針のない注入器およびスマートな注入システムを含む薬剤の配達装置の技術的な進歩はより安全で、より便利なCNS療法の管理を促進しています。 患者の意識とホームケアオプションを成長させ、セグメントの拡大に貢献します。 CNS ターゲット バイオ ロジックの R&D を増加させるも、特殊な注射剤の需要を高める.

- 用途別

適用に基づいて、市場は自己免疫疾患、ホルモン障害、孤児病、腫瘍学、その他に分けられます。 自己免疫疾患のセグメントは、リウマチの関節炎、乾癬、およびクローン病などの条件の上昇の蔓延によって駆動され、2024年に支配される。 満たされた注射器および自動注入器は自己管理のために、忍耐強い承諾を改善し、病院の訪問を減らすために好まれます。 病院およびホームケアの提供者は正確な投薬および最低の注入の不快感を可能にする装置を評価します。 自己免疫障害のバイオロジックを標的とする製薬研究開発の取り組みは、市場成長を促進します。 デジタル密着ツールとの統合により、患者様のエンゲージメントを高めます。 慢性疾患管理のための支援政府政策もセグメントの採用を促進します。

腫瘍学セグメントは、モノクローナル抗体および標的生物学を含む注射可能ながん療法に対する需要の増加による2025年から2032年までの最速成長を目撃することが期待されます。 がんの発生率を高め、家庭の投与療法に対する患者の嗜好と組み合わせることで、燃料化の採用です。 安全を改善し、正確さを投薬し、付着力を高める革新的な製剤および接続された配達装置はこの区分の急速な拡張を支えます。 病院や専門がんクリニックは、これらの高度なソリューションを採用しています。 パーソナライズされた腫瘍学療法への投資もセグメントの成長に貢献します。

- エンドユーザーによる

エンドユーザーに基づいて、市場は病院やクリニック、ホームヘルスケア、研究機関、医薬品、バイオテクノロジー企業、その他に分けられます。 病院および医院は高度の忍耐強い容積、高度のヘルスケアの下部組織による最大の収益の共有と2024年に市場を支配し、急性および慢性条件のための注射可能な療法の信頼性を認めます。 これらの設定は、正確な投薬、管理エラーを最小限に抑え、統合された患者ケアをサポートするデバイスと処方を好む。 製薬会社との強力なパートナーシップにより、高度な注射可能なソリューションへのアクセスも容易になります。 病院は、治療管理のためのデジタル統合からも恩恵を受けています。 政府の医療政策と償還支援は、病院の採用を強化します。

在宅医療分野は、自己管理療法の優先度を高め、老化人口、慢性疾患の有病率を増加させることにより、予測期間中に最速の成長を目撃することが期待されます。 デジタル監視と共に接続し、ユーザー フレンドリー装置は、忍耐強い付着力および便利を高め、成長を運転します。 また、ホームケアサービスおよびリモート患者管理ソリューションの拡張もセグメントをサポートしています。 患者のエンパワーメントとヘルスケアデリバリーのコストダウンに関する意識を高めることで、セグメントのメリットが高まります。

- 流通チャネル

流通チャネルに基づいて、市場は病院の薬局、薬局店、直接入札、オンライン薬局に分けられます。 病院薬局は、入院患者および外来治療のための注射可能な治療への直接アクセスのために2024年に支配された分配および適切な処理を保障します。 病院は信頼できる製造者からの調達装置そして公式を好み、質および規制の承諾を維持します。 病院の在庫およびデジタル監視システムとの統合はまたこの区分の優位性を支えます。 病院の薬剤師はまたバルク調達および供給のチェーン効率を促進します。 医薬品メーカーとの関連性を更に強化し、市場位置を強化

オンライン薬局のセグメントは、電子薬局の採用、利便性、およびホームデリバリー注射療法の需要増加による予測期間中の最速の成長を目撃する予定です。 デジタルプラットフォームは、特に慢性疾患管理と予防ケアのために、デバイスと処方の両方に簡単にアクセスできます。このチャネルの急速な拡大をサポートします。 オンライン薬局は、サービス提供を強化するために、遠隔医療とデジタル相談を活用しています。 オンライン購入でインターネットの普及と消費者の快適性を高め、さらに成長を加速します。

ヨーロッパの注射可能な医薬品配達市場地域分析

- ドイツは、2024年に37.2%の最大の収益分配で欧州注射可能な医薬品配達市場を支配しました。先進医療インフラ、バイオロジカルの高い採用、強力な規制枠組み、および主要な市場プレーヤーの重要な存在によって支持され、注射可能な医薬品配送装置と病院および家庭医療における処方の増大率が増加しました。

- ヘルスケアプロバイダーや各国の患者は、精密な投薬、自己管理の容易さ、およびデジタル監視プラットフォームとの統合により、治療の遵守を強化するデバイスと処方をますますますますますます重要

- この広範囲にわたる採用は、実質的な研究開発投資、堅牢な医薬品およびバイオテクノロジー産業の存在によってさらに支持され、患者中心的なケアの意識を高め、注射可能な医薬品の配送システムを確立し、病院と家庭のヘルスケア設定の両方で好まれる選択肢として確立します

ドイツ 注射薬 デリバリー マーケット インサイト

ドイツは、2024年に37.2%の最大の収益分配で欧州注射薬のデリバリー市場を支配しました。先進医療インフラ、生態学の高い採用、革新的な医薬品デリバリー機器や処方の強力な規制サポートによって駆動しました。 病院およびホームケアの提供者はますます精密な投薬、減らされた管理の間違いおよび改善された忍耐強い承諾のための自動注入器、満たされたスポイトおよび身につけられる装置を好みます。 デジタルヘルスプラットフォームとのインテグレーションにより、治療監視、リマインダー、および付着力の追跡を可能にし、さらなる採用を強化します。 ドイツは、イノベーション、患者中心のケア、持続可能な医療ソリューションに焦点を合わせ、病院とホームケアの双方のアプリケーションを横断する普及促進を推進しています。 医薬品やバイオテクノロジーの大手プレイヤーは、接続された医薬品のデリバリー技術に投資し、デバイスの安全と利便性を高めています。 堅牢なR&D、規制対応、高い患者意識の組み合わせにより、ドイツは欧州の優位性のある市場として確立します。

U.K. 注射用医薬品デリバリーマーケットインサイト

U.K.注射可能な医薬品配送市場は、予測期間中に注目すべきCAGRで成長することを期待しています。, 自己管理療法およびホームケア注射ソリューションの需要の増加によって駆動. 自己免疫障害やホルモン不均衡などの慢性疾患の蔓延を増加させ、プレフィルド注射器や自動注射器を採用する患者を奨励します。 U.K.の強力な医療インフラは、デジタルヘルスの採用を増加させ、市場の成長を刺激し続けることが期待されています。 患者やプロバイダーも、安全、ユーザーフレンドリー、コネクテッドデリバリーシステムを優先して、遵守と治療の監視を強化しています。

フランスの注射可能な薬剤配達市場洞察

フランスの注射可能な医薬品のデリバリー市場は、生態学、ワクチン、自己管理療法に対する需要の増加によって、着実に成長するように計画されています。 フランスの医療提供者および患者は治療の承諾、安全および便利を改善するために満たされた注射器および自動注入器を採用します。 強固な規制対応、高度の病院のインフラ、および慢性疾患管理のさらなるボルスター市場成長に関する忍耐強い意識の増加。 治療監視アプリなどのデジタルヘルスソリューションの統合により、病院とホームケアの双方の採用を強化します。

イタリア 注射薬 デリバリー マーケット インサイト

イタリアの注射可能な医薬品配達市場は、増加する医療費増殖、慢性疾患の蔓延、および自己投与療法の患者の嗜好を高めることにより、予測期間の間に最速の成長を目撃することが期待されます。 病院およびホームケアの提供者はますます高度の自動注入器を採用し、付着力を改善し、病院の依存性を減らすために満たされたスポイトは採用します。 免疫・慢性疾患管理を推進する政府の取り組みも市場拡大をサポートします。 デジタルヘルス監視プラットフォームの採用により、患者のエンゲージメントと治療精度が向上します。

ヨーロッパの注射可能な薬剤配達市場シェア

ヨーロッパの注射可能な薬剤の配達企業は主に下記のものを含んでいる井戸確立された会社によって、導きます:

- 株式会社テルモ(日本)

- AbbVie Inc.(米国)

- メルク&株式会社(米国)

- SCHOTTファーマAG&Co. KGaA(ドイツ)

- Gerresheimer AG(ドイツ)

- インジェクションを有効にする(米国)

- メディンセルS.A.(フランス)

- バイオジェン株式会社(米国)

- ノボノルディスク A/S(デンマーク)

- サンオフィ(フランス)

- バイエルAG(ドイツ)

- Novartis AG(スイス)

- F.ホフマン・ラ・ロチェ株式会社(スイス)

- GSK plc(イギリス)

- ジョンソン&ジョンソンサービス株式会社(米国)

- Pfizer Inc.(米国)

- エリ・リリー・アンド・カンパニー(米国)

- アストラゼネカ(イギリス)

- Boehringer Ingelheim International GmbH (ドイツ)

ヨーロッパ注射薬配達市場における最近の発展は何ですか?

- 2025年7月、テルモ株式会社(本社:東京都港区、代表取締役社長:樋口 宏)は、欧州におけるイムシズ・イントラダマル・インジェクション・システムの商用発売を発表しました。 この装置は、子宮内経路を介してワクチンやその他の承認された薬を届けるために設計されており、注射量を減らし、患者様の快適性を向上させるなどの利点を提供します。 欧州市場での医薬品のデリバリー技術を発展させるための進展

- 2025年3月、インジェクションを有効にすると、EU医療機器規則に基づくCEマークの承認が認められていると発表しました。 このウェアラブルドラッグデリバリープラットフォームは、家庭でのバイオロジックの自己管理を可能にすることで、患者の快適性とコンプライアンスを強化するように設計されています

- 2024年7月、Sanofiは、ドイツ・フランクフルトの長期インシュリン生産施設をアップグレードするために、最大USD 1.78億ドルの投資を検討しています。 ドイツの医薬品製造拠点としてドイツの魅力を反映し、特にEli LillyやDaiichi Sankyoなどの企業からの最近の投資を軽視

- 2024年5月、EisaiとBiogenは、アルツハイマーの薬物であるLeqembiの皮下注射バージョンの米国FDAへの転用申請を開始しました。 新たな処方は、現在承認された静脈内形態と比較して、より便利な投与スケジュールを提供することを目指しています。これは、隔週の注入を必要とする。 承認された場合、注射可能なバージョンは、患者の遵守を著しく高め、市場アクセスを拡大できます

- 2023年11月、エリ・リリーは、ドイツ初の製造施設を建設し、アルゼイのハイテク工場で2,70億米ドルを投資する計画を発表しました。 糖尿病や肥満の治療の需要が高まっている、注射用製品やデバイスの生産を強化し、同社のMounjaroおよびZepbound薬を含む

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。