世界の毛細管血液採取・サンプリング装置市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

2.77 Billion

USD

3.96 Billion

2024

2032

USD

2.77 Billion

USD

3.96 Billion

2024

2032

| 2025 –2032 | |

| USD 2.77 Billion | |

| USD 3.96 Billion | |

| % | |

|

世界の毛細管血液採取およびサンプリング装置市場のセグメンテーション:製品別(血液採取装置、毛細管血液採取装置、迅速検査カセット、遠隔毛細管血液採取装置、ウェアラブル毛細管血液採取装置)、モダリティ別(手動採取、自動/自動注入採取)、投与方法別(穿刺および切開)、用途別(心血管疾患、感染症および呼吸器疾患、癌、関節リウマチ、その他)、プラットフォーム別(酵素免疫測定プラットフォーム(ELISAプラットフォーム)、PCRプラットフォーム、ラテラルフロー免疫測定プラットフォーム、ELTABAプラットフォーム、その他)、手順別(従来型検査およびポイントオブケア検査)、年齢層別(高齢者、乳児、小児、成人)、検査タイプ別(全血検査、乾燥血液スポット検査、血漿/血清タンパク質検査、肝パネル/肝プロファイル/肝機能)検査、包括的代謝パネル(CMP)検査、その他)、技術(容積測定吸収マイクロサンプリング、キャピラリー電気泳動ベースの化学分析、その他)、材質(プラスチック、ガラス、ステンレス鋼、セラミック)、エンドユーザー(研究室および在宅ケア環境)、流通チャネル(直接入札、小売販売、その他) - 2032年までの業界動向と予測

毛細管血液採取・サンプリング装置市場規模

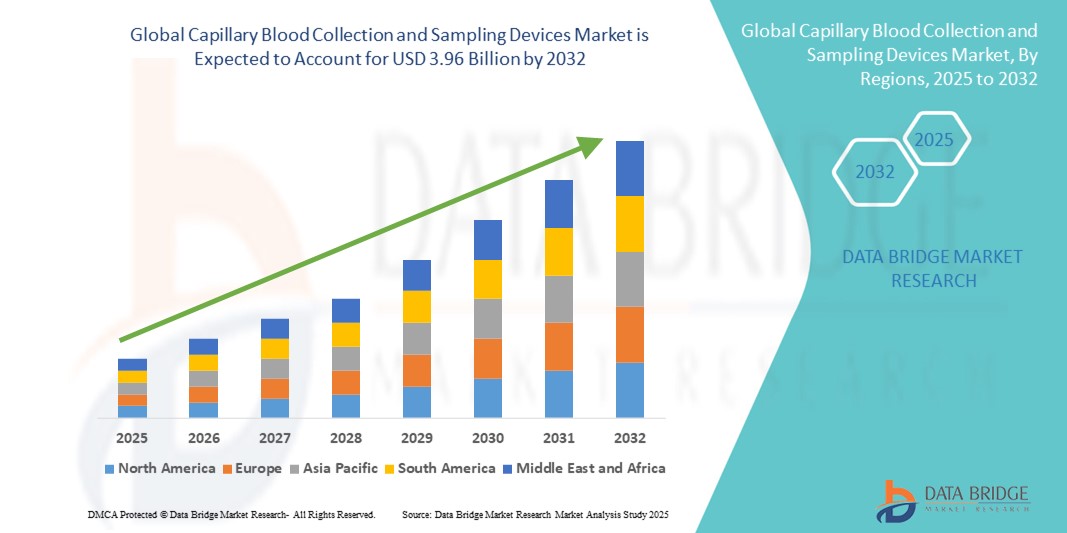

- 世界の毛細管血液採取およびサンプリング装置市場規模は2024年に27億7000万米ドルと評価され、予測期間中に4.55%のCAGRで成長し、2032年には39億6000万米ドル に達すると予想されています 。

- 市場の成長は、慢性疾患の罹患率の増加、ポイントオブケア検査の需要の増加、臨床および家庭環境でより迅速かつ正確な血液サンプルを可能にする低侵襲診断技術の進歩によって主に推進されています。

- さらに、医療従事者と患者の間で、痛みの軽減、使いやすさ、利便性といった毛細管採血の利点に対する認識が高まっており、これらのデバイスは日常的な血液検査における好ましい方法として定着しつつあります。これらの要因が重なり、毛細管採血およびサンプリングソリューションの導入が加速し、業界の成長を大きく促進しています。

毛細管血液採取・サンプリング装置市場分析

- 毛細血管からの血液の最小侵襲採取用に設計された毛細血管採血およびサンプリング装置は、その使いやすさ、痛みの軽減、迅速なサンプル処理能力により、現代の診断、ポイントオブケア、在宅検査のアプリケーションにおいてますます重要になっています。

- これらの機器の採用増加の主な要因は、慢性疾患の罹患率の上昇、ポイントオブケア診断の需要増加、臨床および在宅医療の現場における便利で患者に優しいサンプリング方法の必要性である。

- 北米は、高度な医療インフラ、高い医療費、主要な市場プレーヤーの存在に牽引され、2024年には毛細血管採血およびサンプリング装置市場で39%という最大の収益シェアを獲得して市場を席巻しました。米国では、マイクロ採血装置と自動サンプリングシステムの革新に支えられ、病院、診断ラボ、在宅健康モニタリングプログラムで大幅な導入が見込まれています。

- アジア太平洋地域は、医療意識の高まり、慢性疾患や感染症の蔓延、都市部や準都市部における診断施設へのアクセス拡大により、予測期間中に毛細血管採血およびサンプリング装置市場で最も急速に成長する地域になると予想されています。

- 毛細管血液採取装置セグメントは、その利便性、ポイントオブケアおよびラボテストとの互換性、従来の血液採取方法に比べて侵襲性が最小限であることから、2024年には毛細管血液採取およびサンプリング装置市場を42.5%のシェアで支配しました。

レポートの範囲と毛細管血液採取およびサンプリングデバイス市場のセグメンテーション

|

属性 |

毛細管血液採取およびサンプリング装置に関する主要な市場洞察 |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

毛細管血液採取・サンプリング装置市場動向

ポイントオブケアおよびリモートサンプリングソリューションの採用増加

- 世界の毛細管血液採取およびサンプリング装置市場における主要なトレンドは、ポイントオブケア(POC)検査と遠隔血液サンプリング技術の採用の増加であり、従来の研究室環境外でのより迅速な診断と患者のモニタリングを可能にしています。

- 例えば、遠隔毛細管採血装置により、患者は自宅で少量の血液サンプルを採取し、検査のために検査室に送ることができるため、頻繁な通院の必要性が軽減されます。同様に、糖尿病や心血管疾患などの慢性疾患のバイオマーカーを継続的にモニタリングするためのウェアラブル毛細管採血装置の開発も進められています。

- 技術の進歩により、デバイスの精度、使いやすさ、そしてデジタルヘルスプラットフォームとの統合性が向上しています。マイクロコレクションキットや自動サンプリングユニットなどのデバイスは、リアルタイムのサンプル検証機能を提供し、モバイルアプリケーションを通じて患者データを追跡できるようになりました。

- 毛細管サンプリング装置を遠隔医療およびモバイル診断プラットフォームと統合することで、集中的な患者モニタリングが容易になり、医療提供者は検査結果、傾向、異常を遠隔で追跡できるようになります。

- Companies such as Tasso, Inc. and Seventh Sense Biosystems are focusing on developing smart, user-friendly blood collection devices with features such as minimal invasiveness, automated sampling, and secure data transmission

- This trend towards more convenient, connected, and patient-centric blood collection solutions is reshaping diagnostic practices, driving adoption across hospitals, laboratories, and home healthcare sectors

Capillary Blood Collection and Sampling Devices Market Dynamics

Driver

Increasing Demand Due to Chronic Disease Prevalence and Home-Based Diagnostics

- The rising prevalence of chronic diseases, coupled with the growing emphasis on home-based and minimally invasive diagnostics, is a key driver for the market

- For instance, in March 2024, Seventh Sense Biosystems expanded its remote blood collection offerings for chronic disease monitoring, highlighting the convenience and accuracy of their micro-sampling technology

- Patients and healthcare providers are increasingly favoring capillary blood sampling due to its reduced pain, smaller sample volume requirements, and suitability for frequent monitoring of conditions such as diabetes, cardiovascular disease, and infectious diseases

- The convenience of home collection, rapid sample processing, and compatibility with point-of-care and laboratory testing workflows further propels adoption across both clinical and home healthcare environments

- Growing prevalence of chronic diseases and the need for minimally invasive, home-based diagnostics is driving the market

- Capillary blood sampling offers reduced pain, smaller sample volume requirements, and suitability for frequent monitoring, making it attractive for both patients and healthcare providers

Restraint/Challenge

Sample Accuracy, Standardization, and Regulatory Compliance

- Concerns regarding sample accuracy, proper collection techniques, and regulatory compliance pose significant challenges to broader market adoption. Improper capillary blood collection can lead to hemolysis, contamination, or insufficient sample volume, affecting test reliability

- For instance, high variability in results from at-home blood collection kits has raised questions about standardization and quality assurance, prompting regulatory authorities to set stricter guidelines for device approval

- Addressing these challenges requires improved device design, clear user instructions, and integration with automated or volumetric sampling technologies to reduce human error. Companies such as Becton Dickinson and Sarstedt emphasize quality control, user training, and adherence to regulatory standards to ensure reliable testing outcomes

- In addition, the relatively higher cost of advanced automated or wearable sampling devices compared to traditional finger-prick kits can limit adoption in price-sensitive regions

- Variability in sample quality and collection technique can affect test reliability, raising concerns among users and healthcare professionals

- 規制遵守と、高度な自動化デバイスやウェアラブルデバイスの比較的高いコストにより、価格に敏感な地域での導入が制限される可能性がある。

- デバイスの精度向上、規制遵守、ユーザー教育を通じてこれらの障壁を克服することは、世界の毛細管血液採取およびサンプリングデバイス市場の持続的な成長にとって極めて重要です。

毛細管血液採取およびサンプリング装置市場の範囲

市場は、製品、モダリティ、投与方法、アプリケーション、プラットフォーム、手順、年齢層、テストの種類、テクノロジー、材料、エンドユーザー、流通チャネルに基づいてセグメント化されています。

- 製品別

製品別に見ると、毛細管採血・サンプリング装置市場は、採血装置、毛細管採血装置、迅速検査カセット、遠隔毛細管採血装置、ウェアラブル毛細管採血装置に分類されます。毛細管採血装置セグメントは、病院、診断ラボ、ポイントオブケア検査などで広く使用されていることから、2024年には42.5%のシェアで市場を席巻しました。これらの装置は、低侵襲性のサンプル採取を可能にし、患者の不快感を軽減し、正確な少量採血を保証します。全血、血漿、乾燥血液スポット検査など、複数の検査タイプに対応しており、臨床用途に最適です。慢性疾患の増加と定期的なモニタリングの必要性も、このセグメントの優位性をさらに支えています。

遠隔毛細管採血装置セグメントは、在宅診断および遠隔医療ソリューションの普及拡大に牽引され、2025年から2032年にかけて最も高い成長が見込まれています。遠隔デバイスにより、患者は自宅で検体を採取し、検査機関に送付できるため、通院回数が減り、患者のコンプライアンスが向上します。自動追跡、ユーザーフレンドリーなインターフェース、遠隔医療プラットフォームとの互換性といった技術の進歩も、この分野の普及を促進しています。患者中心のケアモデルへの意識の高まりと在宅検査の利便性が、この成長を加速させています。

- モダリティ別

毛細管採血・サンプリング装置市場は、モダリティに基づいて、手動サンプリングと自動/自動注入サンプリングに分類されます。手動サンプリングセグメントは、シンプルさ、低コスト、そして家庭や臨床現場での広範な使用により、2024年には60.7%のシェアを占め、市場を席巻しました。手動デバイスを使用することで、医療従事者はサンプル採取を制御でき、日常検査における正確性と信頼性を確保できます。特に、自動化システムが実現できないリソースの限られた環境では、手動サンプリングが好まれます。手動サンプリングは、複数の年齢層や検査タイプに対応しているため、実用性が向上しています。このセグメントは、従来の採取装置の大規模な設置基盤の恩恵を受けています。日常的なモニタリングのために、研究室、診療所、在宅ケア環境で広く使用されています。

自動/自動注入サンプリング分野は、ハイスループット、高精度、かつエラーの少ないサンプル採取に対する需要の高まりを背景に、最も急速な成長が見込まれています。病院や診断ラボは、効率性とワークフローの統合性を向上させるために自動化を導入しています。自動化システムは、人的ミスを削減し、サンプル量を標準化し、再現性を向上させます。デジタルヘルスプラットフォームや検査情報システムとの統合も、自動化の導入をさらに後押しします。品質管理と標準化の要件に対する意識の高まりも、この成長を加速させています。

- 投与方法別

投与方法に基づいて、毛細血管採血およびサンプリングデバイス市場は、穿刺と切開に分類されます。穿刺セグメントは、低侵襲性で不快感が少なく、成人、小児、高齢者の患者に適しているため、2024年には68.4%のシェアを占めました。指先穿刺やかかと穿刺システムなどの穿刺ベースのデバイスは、日常診断やポイントオブケアアプリケーションで広く使用されています。そのシンプルさと合併症のリスクの低さから、病院と在宅ケアの両方で非常に好まれています。穿刺法は、ELISAやPCRなど、複数の検査タイプとプラットフォームと互換性があります。迅速な採取と即時分析をサポートし、患者のコンプライアンスを向上させます。慢性疾患モニタリングのための低侵襲ソリューションの需要の高まりも、この優位性を強化しています。

切開セグメントは、より大量の血液を必要とする特殊な診断への応用により、予測期間中に最も高い成長が見込まれています。安全性と効率性におけるイノベーションにより、病院や研究室での導入が拡大しています。切開デバイスは、分子分析や高感度検査のための正確なサンプル採取を可能にします。この成長は、希少疾患の罹患率の上昇と研究主導のサンプル採取ニーズに支えられています。さらに、検査室の自動化と標準化された手順の導入が成長をさらに加速させます。

- アプリケーション別

毛細管採血・サンプリング装置市場は、用途別に、心血管疾患、感染症、呼吸器疾患、がん、関節リウマチ、その他に分類されます。心血管疾患分野は、疾患の有病率の高さとバイオマーカーの頻繁なモニタリング要件により、2024年には29.6%のシェアを占め、市場を牽引しました。毛細管採血装置は、コレステロール、グルコース、心筋酵素の低侵襲検査を可能にします。病院や在宅ケアの現場での日常的なモニタリングが、この分野の普及を促進しています。患者は、簡便性、利便性、そして不快感の軽減という理由から、毛細管採血を好みます。また、この分野は慢性疾患管理プログラムとの統合による恩恵も受けています。心血管疾患の健康と早期診断への意識の高まりも、成長に貢献しています。

感染症・感染症分野は、アウトブレイクの発生、迅速診断の需要増加、そしてポイントオブケア検査に牽引され、予測期間中に最も高い成長が見込まれています。自宅や診療所で感染症検査のための迅速かつ確実な検体採取を可能にする機器の普及が進んでいます。特に、検査インフラが限られている新興国では需要が高まっています。この成長は、遠隔医療の取り組み、疫学研究、そして政府のスクリーニングプログラムの拡大によって支えられています。遠隔検体採取の利便性は、患者のコンプライアンス向上につながります。

- プラットフォーム別

プラットフォームに基づいて、毛細血管採血・サンプリング装置市場は、ELISA、PCR、ラテラルフロー免疫測定法、ELTABA、その他に分類されます。ELISAプラットフォームは、高い精度、再現性、そして毛細血管採血からのバイオマーカー検出における幅広い適用性により、2024年には33.2%のシェアを占め、市場を席巻しました。病院、検査室、研究施設において、日常検査やハイスループット検査に使用されています。複数の採取装置や検査タイプとの互換性により、幅広い導入が期待されています。ELISAプラットフォームは、慢性疾患モニタリング、感染症検査、臨床研究をサポートしています。トレーニングと標準化により、世界中の検査室で好まれるプラットフォームとなっています。VAMS(多項目血球系免疫測定法)やDBS(多項目血球系免疫測定法)との技術統合により、その地位はさらに強化されています。

PCRプラットフォームセグメントは、分子診断と感染症検出の需要増加により、予測期間中に最も高い成長が見込まれています。毛細管血は少量のサンプルで済むため、PCRに適しています。在宅、ポイントオブケア、そして遠隔医療ソリューションは、PCRの普及を促進しています。ウイルス感染の早期診断への意識の高まりも成長を後押ししています。PCRは高い感度と特異性を備えており、研究所や研究機関にとって好ましいプラットフォームとなっています。分子診断への政府および民間からの資金提供の増加も成長を加速させています。

- 手順別

手順に基づいて、毛細血管採血・サンプリング装置市場は、従来型検査とポイントオブケア検査に分類されます。ポイントオブケア検査(POCT)セグメントは、迅速診断、在宅検査、患者近傍検査ソリューションの導入増加により、2024年には57.1%のシェアを占め、市場を席巻しました。POCTは、より迅速な結果取得を可能にし、中央検査室への依存度を低減し、患者管理を改善します。このセグメントは、慢性疾患のモニタリングや感染症の検出にますます利用されています。毛細血管採血装置との互換性により、使いやすさと患者のコンプライアンスが向上します。デジタルヘルスプラットフォームとの統合により、モニタリングとレポート機能が強化されます。利便性、精度、スピードから、POCTは医療現場で広く採用されています。

The Conventional Testing segment is expected to witness the fastest growth during forecast period, particularly in emerging markets where centralized laboratory infrastructure is expanding. Conventional testing requires standardized workflows, and capillary blood collection devices support sample integrity for these analyses. Adoption is driven by expanding hospital and laboratory networks. Conventional testing continues to dominate routine diagnostics in several regions. Growth is also supported by increasing demand for chronic disease and cardiovascular testing. Integration with laboratory automation further boosts adoption.

- By Age Group

On the basis of age group, the capillary blood collection and sampling devices market is segmented into geriatrics, infant, pediatric, and adult. The Adult segment dominated with a 46.8% share in 2024, driven by high prevalence of chronic diseases, routine monitoring, and frequent diagnostic testing. Adults require blood sampling for cardiovascular, metabolic, and infectious disease management. Hospitals, labs, and home care settings widely adopt devices designed for adults. Minimally invasive, accurate, and easy-to-use devices enhance compliance. Integration with telehealth and remote monitoring platforms further supports adoption. Growing chronic disease prevalence globally reinforces the segment’s dominance.

The Infant segment is expected to witness the fastest growth, fueled by neonatal screening programs and rising awareness for early detection of metabolic and genetic disorders. Heel-prick and finger-prick devices are minimally invasive and safe for newborns. Adoption is supported by hospitals and pediatric clinics for routine infant testing. Remote and home-based collection kits improve compliance and accessibility. Technological innovations make devices easier for caregivers to use. Government initiatives in infant screening further drive growth.

- By Test Type

On the basis of test type, the capillary blood collection and sampling devices market is segmented into Whole Blood Test, Dried Blood Spot Tests, Plasma/Serum Protein Tests, Liver Panel, CMP Tests, and Others. The Whole Blood Test segment dominated with a 38.5% share in 2024, due to its widespread use in routine diagnostics and clinical applications. Whole blood collection allows testing for multiple analytes, including glucose, cholesterol, and infectious disease markers. Hospitals, labs, and home care services prefer whole blood tests for their reliability and accuracy. Capillary blood collection devices are compatible with whole blood analysis, supporting rapid results. Patients benefit from reduced sample volume requirements and minimal discomfort. Rising prevalence of chronic and infectious diseases further strengthens adoption.

The Dried Blood Spot (DBS) Tests segment is expected to witness the fastest growth during forecast period, driven by suitability for remote collection, storage stability, and telehealth-based diagnostics. DBS allows home collection, minimizes handling errors, and supports infectious disease monitoring. Technological improvements in DBS sample analysis enhance accuracy and reproducibility. Adoption is increasing in population studies, epidemiology, and chronic disease management. Patients prefer DBS for convenience and reduced invasiveness. Growth is supported by increasing availability of DBS collection kits through online and retail channels.

- By Technology

On the basis of technology, the capillary blood collection and sampling devices market is segmented into Volumetric Absorptive Microsampling (VAMS), Capillary Electrophoresis-Based Chemical Analysis, and Others. The VAMS segment dominated with a 31.4% share in 2024, due to precision in small-volume blood collection, compatibility with multiple platforms, and minimal handling errors. It is widely used in hospitals, labs, and research facilities. VAMS supports both point-of-care and home-based diagnostics. Accuracy, reproducibility, and ease of use drive adoption. Integration with telehealth and remote monitoring enhances its utility. R&D investment in VAMS further strengthens its position.

The Capillary Electrophoresis-Based Chemical Analysis segment is expected to witness the fastest growth during forecast period, driven by adoption in laboratories and research facilities for detailed molecular and biochemical analysis. Small-volume capillary samples allow high-precision testing. This technology is used in drug development, biomarker research, and specialized diagnostics. Automation integration reduces human errors and increases efficiency. Rising adoption of personalized medicine and advanced diagnostics supports growth. Funding in advanced research accelerates market expansion.

- By Material

On the basis of material, the capillary blood collection and sampling devices market is segmented into Plastic, Glass, Stainless Steel, and Ceramic. The Plastic segment dominated with a 52.6% share in 2024, due to cost-effectiveness, disposability, lightweight design, and safety. Plastic devices reduce contamination risk and are widely adopted for home and clinical use. Compatibility with multiple test types, including whole blood and DBS, supports adoption. Plastic devices are easier to transport and store. They are ideal for single-use, point-of-care applications. Growing demand for affordable devices globally strengthens this segment.

The Stainless Steel segment is expected to witness the fastest growth during forecast period, driven by durability, precision, and suitability for high-throughput labs and automated sampling systems. Stainless steel supports repeated use in professional settings. It integrates with autoinjection and automated systems for accuracy. Hospitals and research labs prefer stainless steel for its reliability and long-term use. Increasing investments in advanced laboratory infrastructure enhance adoption. Rising awareness of quality and safety standards supports growth.

- By End User

On the basis of end user, the capillary blood collection and sampling devices market is segmented into Laboratories and Home Care Settings. The Laboratories segment dominated with a 61.2% share in 2024, as most capillary blood samples are processed in hospitals, diagnostic, and research labs. Laboratories demand high-accuracy, standardized devices compatible with automation and high-throughput workflows. Integration with analytical platforms such as ELISA, PCR, and VAMS ensures efficiency. Institutional procurement contracts and direct tenders further reinforce dominance. Capillary devices are essential for chronic disease, infectious disease, and research testing. Laboratories prefer reliable, reproducible, and compliant solutions.

The Home Care Setting segment is expected to witness the fastest growth during forecast period, due to rising telemedicine adoption, chronic disease self-monitoring, and patient-centric care. Home devices allow convenient and minimally invasive blood collection. Patients and caregivers prefer easy-to-use, reliable devices for remote sample collection. Growth is supported by wearable and remote collection technologies. Increasing awareness of home diagnostics and online kit availability fuels adoption. Chronic disease prevalence and government initiatives further accelerate growth.

- By Distribution Channel

On the basis of distribution channel, the capillary blood collection and sampling devices market is segmented into Direct Tender, Retail Sales, and Others. The Direct Tender segment dominated with a 49.8% share in 2024, due to large-scale procurement by hospitals, laboratories, and clinics. Institutional tenders ensure quality, compliance, and favorable bulk pricing. Hospitals prefer this channel for consistent supply and secure sourcing. Direct tender contracts support integration with automated systems and high-throughput workflows. Long-term agreements with suppliers reinforce dominance. Developed regions with established healthcare infrastructure drive market strength.

The Retail Sales segment is expected to witness the fastest growth during forecast period, fueled by online availability, growing consumer awareness, and demand for home-based diagnostic kits. Retail channels allow patients to access devices directly for self-collection, supporting telehealth and home diagnostics. E-commerce expansion and smartphone-based health platforms enhance adoption. Home-based testing kits, wearables, and remote devices benefit from retail distribution. Patient preference for convenience, minimal invasiveness, and fast results accelerates growth. Rising adoption in emerging markets further supports retail sales expansion.

Capillary Blood Collection and Sampling Devices Market Regional Analysis

- North America dominated the capillary blood collection and sampling devices market with the largest revenue share of 39% in 2024, driven by advanced healthcare infrastructure, high healthcare expenditure, and the presence of key market players

- Consumers and healthcare providers in the region increasingly prefer minimally invasive, reliable, and rapid blood collection solutions for hospitals, laboratories, and home care settings. High awareness of telemedicine and point-of-care testing further supports market adoption

- The dominance is reinforced by strong government initiatives promoting early disease detection, routine health monitoring, and remote patient management programs. In addition, increasing investments by key players in R&D and innovation for advanced collection devices contribute to the market’s growth in North America

U.S. Capillary Blood Collection and Sampling Devices Market Insight

The U.S. capillary blood collection and sampling devices market captured the largest revenue share of 42% in 2024, driven by advanced healthcare infrastructure, widespread adoption of telemedicine, and high awareness of minimally invasive diagnostic solutions. Hospitals, laboratories, and home care providers are increasingly prioritizing patient-friendly collection devices for routine monitoring of chronic and infectious diseases. The growing demand for point-of-care testing, coupled with integration of remote sampling technologies, further propels market growth. Moreover, strong government initiatives for early disease detection and preventive healthcare programs contribute significantly to the expansion of the market. Increasing availability of automated and wearable devices enhances convenience and adoption among patients and healthcare providers.

Europe Capillary Blood Collection and Sampling Devices Market Insight

The Europe capillary blood collection and sampling devices market is projected to expand at a significant CAGR during the forecast period, primarily driven by increasing adoption of advanced diagnostic tools and stringent healthcare regulations. Rising awareness regarding chronic disease monitoring and minimally invasive sampling methods is fostering market growth. European healthcare providers and laboratories increasingly prefer capillary blood collection devices for reliability, accuracy, and patient comfort. The market benefits from established distribution networks, government-backed screening programs, and reimbursement policies supporting routine diagnostics. Countries such as Germany, the U.K., and France are witnessing rising adoption across both hospital and home care settings. Continuous technological innovation, including automated and remote collection devices, is further fueling market expansion.

U.K. Capillary Blood Collection and Sampling Devices Market Insight

The U.K. capillary blood collection and sampling devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing prevalence of chronic and infectious diseases, coupled with rising awareness of home-based diagnostics. Healthcare providers and patients are showing a growing preference for minimally invasive, reliable, and easy-to-use capillary blood collection devices. The strong e-commerce and retail infrastructure in the country facilitates widespread availability of home-use kits. Government health initiatives promoting early disease detection and preventive care further stimulate adoption. Integration with telehealth platforms and point-of-care testing technologies is accelerating market growth. The focus on convenience, patient comfort, and timely diagnostics underpins continued demand in both residential and clinical segments.

Germany Capillary Blood Collection and Sampling Devices Market Insight

The Germany capillary blood collection and sampling devices market is expected to expand at a considerable CAGR, fueled by rising awareness of preventive healthcare, early diagnostics, and advanced laboratory infrastructure. Capillary blood collection devices are increasingly preferred for routine monitoring of cardiovascular, metabolic, and infectious diseases. Germany’s emphasis on innovation, quality standards, and sustainability encourages adoption of high-precision and reusable devices. Hospitals, diagnostic centers, and research laboratories are implementing these devices to enhance workflow efficiency and reduce patient discomfort. Increasing integration with automated and digital platforms for sample collection and reporting is supporting market growth. Consumer demand for safe, reliable, and eco-conscious devices further strengthens adoption.

Asia-Pacific Capillary Blood Collection and Sampling Devices Market Insight

The Asia-Pacific capillary blood collection and sampling devices market is poised to grow at the fastest CAGR of 25% from 2025 to 2032, driven by rapid urbanization, rising disposable incomes, and increasing healthcare accessibility in countries such as China, Japan, and India. The adoption of telemedicine and home-based diagnostics is rising, encouraging the use of capillary blood collection devices. Government initiatives supporting maternal and infant health, infectious disease monitoring, and chronic disease management are accelerating demand. Technological advancements in remote and wearable devices improve convenience and accuracy. APAC is also emerging as a manufacturing hub for these devices, making them more affordable and accessible to a broader population. Growing awareness of patient-centric care and preventive healthcare is a key driver for the region.

Japan Capillary Blood Collection and Sampling Devices Market Insight

The Japan capillary blood collection and sampling devices market is gaining momentum due to the country’s high-tech healthcare infrastructure, aging population, and emphasis on convenience and patient safety. Adoption is driven by the increasing number of smart hospitals, connected clinics, and home-based diagnostic solutions. Capillary blood collection devices integrated with automated and wearable technologies are widely used for chronic disease monitoring and infectious disease testing. Government programs promoting preventive healthcare, along with a strong focus on research and development, further support market growth. The elderly population benefits from minimally invasive and easy-to-use devices. Rising awareness of telehealth solutions is also enhancing adoption in both residential and clinical sectors.

India Capillary Blood Collection and Sampling Devices Market Insight

The India capillary blood collection and sampling devices market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, expanding middle-class population, and rising awareness of telemedicine and home-based testing solutions. Capillary blood collection devices are increasingly used in hospitals, diagnostic labs, and home care settings for routine monitoring of chronic diseases and infectious conditions. Government initiatives supporting smart healthcare and digital health programs boost market adoption. Affordable device options and strong domestic manufacturing capabilities further drive growth. Increasing demand in residential, commercial, and remote care applications contributes to rapid expansion. Telehealth integration and point-of-care testing solutions are enhancing convenience and accessibility for Indian consumers.

Capillary Blood Collection and Sampling Devices Market Share

The Capillary Blood Collection and Sampling Devices industry is primarily led by well-established companies, including:

- BD (U.S.)

- Tasso, Inc. (U.S.)

- YourBio Health, Inc. (U.S.)

- Neoteryx LLC (U.S.)

- Greiner Bio-One International GmbH(オーストリア)

- オーウェン・マムフォード・リミテッド(英国)

- VMG(デンマーク)

- HemaXis(スイス)

- ドローブリッジ・ヘルス社(米国)

- サーモフィッシャーサイエンティフィック社(米国)

- SARSTEDT AG & Co. KG (ドイツ)

- MEDIpoint International, Inc.(米国)

- キャピラリーテクノロジーズインディアリミテッド(シンガポール)

- ラジオメーターメディカルApS(デンマーク)

- バイオ・ラッド・ラボラトリーズ社(米国)

- ケント・サイエンティフィック・コーポレーション(米国)

世界の毛細管血液採取およびサンプリング装置市場における最近の動向は何ですか?

- 2025年3月、BDは、同社の新型指先採血装置が、特定の検体において従来の静脈採血と同等の検査精度を示したと発表しました。この装置は、より低侵襲で簡便な代替手段を提供することで、患者が診断検査を受けやすくし、複数回の針刺しの必要性を減らすことを目指しています。

- 2025年2月、患者中心の臨床グレードの血液採取ソリューションを提供するリーディングプロバイダーであるTasso, Inc.は、乾燥血液スポット(DBS)サンプル採取のための次世代技術の発売を発表しました。この革新的な採取システムは、Tassoの新しいTile-T20乾燥全血カートリッジとTasso Miniデバイスを組み合わせ、臨床試験やスポーツアンチ・ドーピング検査のためのDBSサンプルを正確かつ簡便に採取することを可能にします。

- 2023年12月、ベクトン・ディッキンソン(BD)は、BD MiniDraw毛細血管採血システムがFDA 510(k)承認を取得したと発表しました。このデバイスにより、医療従事者は患者の指を使って検査室品質の血液サンプルを採取することができ、従来の静脈採血法よりも侵襲性の低い代替手段となります。このシステムは、薬局を含む様々な環境での採血へのアクセス拡大を目指しています。

- 2023年10月、YourBio Healthは、同社のTAP Micro Select採血デバイスがCEマーキング認証を取得し、規制当局の承認範囲を拡大したと発表しました。このデバイスは、遠隔で実質的に痛みのない毛細血管採血を可能にし、Myriad GeneticsのSneakPeek Testsなどのアプリケーションをサポートします。この承認により、欧州でのより広範な使用が可能になり、非侵襲的検査へのアクセスが向上します。

- 2024年9月、Tasso社は、同社のTasso+デバイスがFDA 510(k)クラスII医療機器承認を取得したと発表しました。この使い捨ての患者中心の採血製品は、従来の採血方法に代わる低侵襲的な方法を提供することを目的として設計されており、様々な医療現場で血液検査へのアクセスを容易にします。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。