世界のカテーテル検査サービス市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

52.20 Billion

USD

82.51 Billion

2024

2032

USD

52.20 Billion

USD

82.51 Billion

2024

2032

| 2025 –2032 | |

| USD 52.20 Billion | |

| USD 82.51 Billion | |

| % | |

|

世界のカテーテル検査サービス市場セグメンテーション、タイプ別(心臓カテーテル検査、血管造影、血管形成術およびステント留置、頸動脈ステント留置)、サービスタイプ別(治療用カテーテル検査サービスおよび診断用カテーテル検査サービス)、アプリケーション別(病院、クリニック、その他) - 業界動向と2032年までの予測

カテーテル検査サービス市場規模

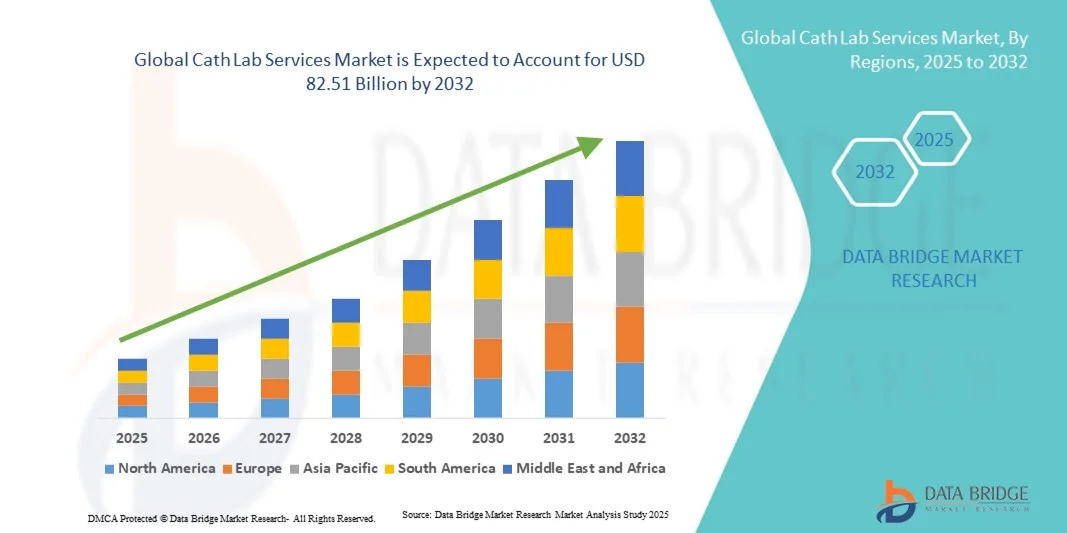

- 世界のカテーテル検査室サービス市場規模は2024年に522億米ドルと評価され、予測期間中に5.89%のCAGRで成長し、2032年までに825億1000万米ドル に達すると予想されています 。

- 市場の成長は、主に心血管疾患の罹患率の増加、高齢者人口の増加、先進国と新興国の両方における低侵襲心臓手術の需要の増加によって推進されています。

- さらに、画像技術の進歩、専門サービスプロバイダーとの病院の戦略的な提携、モバイルカテーテル検査室の拡大により、アクセス性と効率性が向上し、カテーテル検査室サービスの導入が世界中で大幅に加速しています。

カテーテル検査サービス市場分析

- 血管造影や血管形成術などの診断および介入心臓処置を提供するカテーテル検査室サービスは、早期疾患検出、低侵襲治療オプション、病院および外来での患者転帰の改善における役割により、現代の心血管ケアにおいてますます重要になっています。

- 心血管疾患の世界的な負担の増大、高齢化の進行、そしてインターベンション心臓学の継続的な進歩は、世界中でカテーテル検査室サービスの需要を刺激する主な要因です。

- 北米は、確立された医療インフラ、冠動脈疾患の高い罹患率、専門の心臓センターやサービスプロバイダーの強力な存在に支えられ、2024年にはカテーテル検査サービス市場で39.1%という最大の収益シェアを獲得して優位に立った。

- アジア太平洋地域は、中国やインドなどの国における急速な医療インフラの発展、医療費の増加、高度な心臓治療へのアクセスの拡大により、予測期間中に最も急速に成長する地域になると予測されています。

- 病院セグメントは、熟練した心臓専門医、包括的な緊急サポート、病院施設内に統合された高度な画像診断および介入機器の利用可能性により、2024年に55.9%の市場シェアで市場を支配しました。

レポートの範囲とカテーテル検査サービス市場のセグメンテーション

|

属性 |

カテーテル検査サービスの主な市場分析 |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、患者の疫学、パイプライン分析、価格分析、規制の枠組みも含まれています。 |

カテーテル検査サービス市場動向

モバイルおよびハイブリッドカテーテル検査室の拡張によるアクセシビリティの向上

- 世界のカテーテル・ラボ・サービス市場における主要かつ加速的なトレンドの一つは、モバイル型およびハイブリッド型のカテーテル・ラボの急速な拡大です。これらは、医療サービスが行き届いていない遠隔地において、高度な心臓診断とインターベンションケアを提供することを目的として設計されています。このアプローチにより、アクセス性が向上し、重要な心臓手術における患者の移動時間が短縮されます。

- 例えば、アライアンス・ヘルスケア・サービスとトライデントケアは、高度な画像システムを備えたモバイルカテーテル検査ユニットを導入し、病院や診断センターが大規模なインフラ投資をすることなくサービス範囲を拡大できるようにしています。

- モバイル型およびハイブリッド型のカテーテルラボの導入により、医療提供者はより多くの患者数に対応し、特に常設のカテーテルラボ設備が不足している地域において、緊急の心臓疾患症例に迅速に対応することが可能になります。これらの設備は、病院の改修時や需要が集中する時期においても柔軟な展開を可能にします。

- この傾向は、病院ネットワーク、診断チェーン、民間サービスプロバイダー間の協力が増加し、介入心臓病サービスへの地域的なアクセスが拡大していることからも加速している。

- Mobile and hybrid labs are being integrated with real-time telemedicine capabilities, allowing remote monitoring, virtual specialist consultations, and faster decision-making, which further enhances operational efficiency and patient care outcomes

- This growing trend towards portable, accessible, and technologically advanced cath lab setups is transforming the service delivery landscape and enabling equitable access to life-saving cardiac care worldwide

- Advancements in AI-powered imaging and cloud-based data storage are improving diagnostic precision and allowing secure sharing of angiographic data between institutions, strengthening collaborative treatment models

Cath Lab Services Market Dynamics

Driver

Rising Cardiovascular Disease Burden and Demand for Minimally Invasive Procedures

- The increasing global prevalence of cardiovascular diseases (CVDs) and the rising aging population are major drivers fueling demand for cath lab services across hospitals and diagnostic centers

- For instance, in March 2024, Philips Healthcare expanded its interventional cardiology solutions with next-generation imaging systems designed to support precise and minimally invasive cardiac procedures, reinforcing market growth potential

- As more patients and clinicians prefer minimally invasive interventions due to shorter recovery times and reduced complication risks, cath labs have become central to modern cardiac care delivery models

- Furthermore, the growing number of public–private partnerships and healthcare modernization programs in emerging economies is driving investments in advanced cath lab facilities

- The ability to provide accurate, real-time cardiac imaging, quick intervention turnaround, and high diagnostic accuracy makes cath labs indispensable in both emergency and planned cardiac treatments

- The increasing integration of AI-based analytics and robotic-assisted catheterization systems is further enhancing procedural efficiency, safety, and outcomes—contributing significantly to market expansion

- Governments and health organizations are increasingly funding cardiac awareness and screening programs, which in turn increase the demand for diagnostic cath lab procedures

- The rise of multi-specialty hospitals integrating dedicated cardiac wings is expanding the global capacity for interventional cardiology services, boosting overall market growth

Restraint/Challenge

High Operational Costs and Shortage of Skilled Cardiologists

- The significant capital and operational expenses associated with establishing and maintaining cath lab facilities pose a major challenge for smaller hospitals and healthcare providers, especially in developing regions

- For instance, cath lab setup costs involving imaging systems, radiation shielding, and maintenance can exceed USD 2–3 million per unit, which restricts market penetration in cost-sensitive markets

- Moreover, the shortage of skilled interventional cardiologists and trained technicians limits the ability of many healthcare centers to operate cath labs efficiently, leading to underutilization of existing infrastructure

- The requirement for strict compliance with radiation safety and healthcare regulations adds further complexity, increasing administrative and training costs for operators. While telecardiology and remote-assisted interventions are emerging solutions, adoption remains limited due to connectivity and technology integration challenges in rural and low-resource settings

- Overcoming these barriers through cost-efficient mobile lab models, workforce training programs, and government-funded cardiac care initiatives will be crucial for sustainable market growth

- In addition, limited reimbursement frameworks for interventional cardiac procedures in certain regions hinder hospitals’ ability to recover operational expenses, restricting service expansion

- The growing equipment maintenance and upgrade costs associated with rapid technological advancements also pressure smaller healthcare institutions to delay modernization, impacting service quality

Cath Lab Services Market Scope

The market is segmented on the basis of type, service type, and application.

- By Type

On the basis of type, the cath lab services market is segmented into cardiac catheterization, vascular angiogram, vascular angioplasty and stenting, and carotid artery stenting. The Cardiac Catheterization segment dominated the market with the largest revenue share of 35.4% in 2024, driven by its essential role in diagnosing coronary artery diseases, evaluating heart function, and detecting blockages. Hospitals and specialized cardiac centers widely adopt cardiac catheterization due to its minimally invasive nature and ability to guide treatment planning effectively. The increasing prevalence of cardiovascular diseases and early screening initiatives further reinforce the demand for cardiac catheterization procedures. Technological advancements such as 3D imaging, AI-assisted diagnostics, and robotic catheter navigation enhance procedural accuracy and safety, increasing adoption in developed and emerging markets.

The Vascular Angioplasty and Stenting segment is expected to witness the fastest CAGR of 7.8% from 2025 to 2032, fueled by the rising preference for minimally invasive interventions to restore blood flow in patients with coronary and peripheral artery diseases. The procedure’s effectiveness in reducing recovery times and hospital stays makes it highly attractive for patients and healthcare providers. Moreover, innovations in drug-eluting stents, bioresorbable scaffolds, and robotic-assisted deployment are driving increased adoption. The segment is witnessing growing demand in Asia-Pacific and Latin America due to expanding healthcare infrastructure and rising awareness about interventional cardiology.

- By Service Type

On the basis of service type, the market is segmented into therapeutic cath lab services and diagnostic cath lab services. The Diagnostic Cath Lab Services segment dominated the market with a revenue share of 54.1% in 2024, as these services are essential for identifying cardiovascular abnormalities, evaluating disease severity, and guiding treatment planning. Hospitals and outpatient centers prioritize diagnostic cath lab procedures to ensure timely and accurate interventions. The rise of preventive healthcare programs, cardiovascular screening initiatives, and early detection strategies is contributing significantly to segment growth. Integration of AI-powered imaging and advanced hemodynamic monitoring enhances diagnostic precision, attracting more healthcare providers to adopt these services.

The Therapeutic Cath Lab Services segment is expected to witness the fastest growth rate of 8.2% from 2025 to 2032, driven by the increasing adoption of minimally invasive procedures such as angioplasty, stenting, and percutaneous valve interventions. These services reduce patient hospitalization time and offer better post-procedure outcomes compared to traditional surgical methods. Innovations in robotic-assisted interventions, real-time imaging, and hybrid procedure approaches are further boosting adoption across developed and emerging regions. Rising demand for elective and emergency therapeutic procedures also contributes to rapid market growth.

- By Application

On the basis of application, the market is segmented into hospitals, clinics, and others. The Hospitals segment dominated the market with a revenue share of 55.9% in 2024, attributed to the availability of advanced imaging systems, skilled interventional cardiologists, and emergency support for high-risk patients. Hospitals provide comprehensive cardiac care, including diagnostic and therapeutic procedures, making them the preferred choice for cath lab services. The growing trend of multi-specialty hospitals integrating dedicated cardiac wings and adopting cutting-edge technologies further strengthens this segment. For instance, large hospitals increasingly deploy hybrid cath labs to perform complex interventions efficiently while maintaining high patient throughput.

The Clinics segment is expected to witness the fastest growth rate of 9.1% from 2025 to 2032, fueled by the expansion of outpatient cardiology centers and ambulatory surgical units that provide cost-effective and accessible cath lab services. Clinics are increasingly equipped with advanced imaging and interventional tools, allowing for quick diagnosis and minor procedures. The rising prevalence of outpatient procedures, patient preference for shorter hospital visits, and expanding healthcare access in emerging regions are key factors driving segment growth. Clinics also benefit from partnerships with mobile cath lab providers to enhance service coverage.

Cath Lab Services Market Regional Analysis

- 北米は、確立された医療インフラ、冠動脈疾患の高い罹患率、専門の心臓センターやサービスプロバイダーの強力な存在に支えられ、2024年にはカテーテル検査サービス市場で39.1%という最大の収益シェアを獲得して優位に立った。

- この地域の医療提供者は早期診断と低侵襲治療に重点を置いており、病院や専門心臓センター全体で診断と治療の両方のカテーテル検査室サービスの需要が高まっています。

- この強力な市場プレゼンスは、多額の医療費、熟練した介入心臓専門医の存在、最先端の画像技術とロボット支援システムの統合によってさらに支えられており、北米は高品質の心臓ケアの重要な拠点としての地位を確立しています。

米国カテーテル検査サービス市場インサイト

米国のカテーテル検査サービス市場は、心血管疾患の有病率の高さと高度な医療インフラの整備を背景に、2024年には北米で最大の収益シェアとなる42%を獲得しました。病院や専門心臓センターでは、血管造影、血管形成術、ステント留置術といった低侵襲診断・介入治療の導入が進んでいます。心臓疾患の早期発見への需要の高まりに加え、AI支援画像診断やロボットカテーテルシステムといった技術の進歩も、市場の成長を牽引しています。さらに、堅調な医療費支出、熟練した介入心臓専門医、そして心血管ケアを支援する政府の取り組みも、市場の成長に大きく貢献しています。

欧州カテーテル検査サービス市場インサイト

欧州のカテーテル・ラボ・サービス市場は、主に心血管疾患の発症率の上昇と低侵襲手術への需要増加を背景に、予測期間を通じて大幅なCAGRで拡大すると予測されています。病院インフラの強化と高度な画像技術の進歩により、住宅型および商業型の医療施設におけるカテーテル・ラボ・サービスの導入が促進されています。欧州の医療提供者は予防ケアと早期診断を重視しており、診断カテーテル・ラボ・サービスの利用が増加しています。この地域では、有利な償還政策と政府の医療政策に支えられ、病院、外来診療所、専門心臓センターにおいて著しい成長が見込まれています。

英国カテーテル検査サービス市場インサイト

英国のカテーテル・ラボ・サービス市場は、冠動脈疾患の有病率上昇とインターベンショナル・カーディオロジー(心臓血管インターベンション)の導入拡大を背景に、予測期間中に注目すべきCAGRで成長すると予想されています。さらに、医療提供者が低侵襲手術と患者の回復期間の短縮に注力していることも、高度なカテーテル・ラボ・サービスの利用を促進しています。英国では、質の高い医療インフラの整備、熟練したインターベンショナル・カーディオロジー専門医の育成、そして病院の改修への投資増加が、市場の成長を引き続き刺激すると予想されます。

ドイツカテーテル検査サービス市場洞察

ドイツのカテーテル・ラボ・サービス市場は、心血管疾患への意識の高まりと、高度な技術を用いた介入に対する需要の高まりを背景に、予測期間中に大幅なCAGRで拡大すると予想されています。ドイツは、確立された医療インフラ、医療イノベーションへの注力、そして患者の高い期待感から、診断および治療におけるカテーテル・ラボ・サービスの導入が進んでいます。病院や専門心臓センターでは、高度な画像診断システムとロボット支援介入技術を導入し、効率性と患者アウトカムの向上に努めています。規制当局による支援と保険償還制度も、同国における市場導入をさらに後押ししています。

アジア太平洋地域のカテーテル検査サービス市場インサイト

アジア太平洋地域のカテーテル・ラボ・サービス市場は、2025年から2032年にかけて、心血管疾患の有病率の上昇、都市化の進展、そして中国、インド、日本などの国々における医療インフラの拡大を背景に、9.5%という最も高い年平均成長率(CAGR)で成長すると見込まれています。この地域では、早期診断、予防医療、低侵襲手術への関心が高まっており、カテーテル・ラボ・サービスの導入が進んでいます。さらに、医療の近代化を促進する政府の取り組みや、費用対効果の高い介入ソリューションの利用可能性の向上により、高度な心臓ケアへのアクセスが拡大しています。アジア太平洋地域では、病院とモバイル・カテーテル・ラボ・プロバイダーとの連携が拡大しており、地域の医療サービス提供範囲が拡大しています。

日本カテーテル検査サービス市場インサイト

日本のカテーテル検査サービス市場は、高齢化、心血管疾患の有病率の高さ、そして予防的心臓ケアへの注力により、成長を加速させています。病院や外来心臓センターでは、患者の転帰改善を目指し、診断および介入処置の導入が進んでいます。AIベースの画像診断、遠隔心臓病学、ロボット支援介入の統合が成長を牽引する一方、早期診断と高度な心臓ケアを支援する政府のヘルスケアイニシアチブも市場拡大を後押ししています。

インドのカテーテル検査サービス市場に関する洞察

インドのカテーテル・ラボ・サービス市場は、急速な都市化、心血管疾患の負担増加、そして医療費の増加を背景に、2024年にはアジア太平洋地域最大の市場収益シェアを占めると予測されています。インドでは、病院と外来診療所の両方で、診断および介入カテーテル・ラボの導入が急速に進んでいます。民間心臓ケアネットワークの拡大、政府の保健政策、そして費用対効果の高いソリューションの提供が、市場の成長を牽引する重要な要因となっています。さらに、低侵襲処置と予防医療への意識の高まりも、全国でカテーテル・ラボ・サービスの需要をさらに加速させています。

カテーテル検査サービス市場シェア

カテーテル ラボ サービス業界は、主に、次のような定評のある企業によって牽引されています。

- メドトロニック(アイルランド)

- ボストン・サイエンティフィック・コーポレーション(米国)

- アボット(米国)

- ジョンソン・エンド・ジョンソン・サービス社(米国)

- シーメンス・ヘルシニアーズAG(ドイツ)

- GEヘルスケア(米国)

- Koninklijke Philips NV (オランダ)

- キヤノンメディカルシステムズ株式会社(日本)

- 富士フイルムホールディングス株式会社(日本)

- 島津製作所(日本)

- 日立製作所(日本)

- ストライカー(米国)

- Ziehm Imaging GmbH(ドイツ)

- アグファ・ゲバルトグループ(ベルギー)

- B.ブラウンSE(ドイツ)

- テルモ株式会社(日本)

- カーディナル・ヘルス社(米国)

世界のカテーテル検査室サービス市場における最近の動向は何ですか?

- アイオワ州のアレン病院は、2025年9月に3棟目の心臓カテーテル検査室の建設を開始しました。この拡張は、今後5年以内に年間3,800人以上のカテーテル検査患者が利用することが見込まれる、診断および治療に対する需要の増加に対応することを目的としています。新検査室は年末までに稼働開始予定で、シーダーバレー地域に包括的な心臓ケアを提供するという病院のコミットメントをさらに強化します。

- 2024年10月、バプテスト・ヘルスはフロリダ州ボイントンビーチのベセスダ・イースト病院に最先端の心臓カテーテル検査室を開設しました。この施設により、血管造影やステント留置術などの高度な心臓手術を実施できる病院の能力が向上し、地域住民にとって重要な心臓ケアサービスへのアクセスが向上します。

- 2024年9月、マンガロールのウェンロック地区病院は初のカテーテル検査室を開設し、血管形成術と血管造影検査を初めて実施しました。マニパル高等教育アカデミーの支援を受けたこの取り組みは、貧困ライン以下(BPL)のカード保有者を対象に、アユシュマン・バーラト制度に基づく無料の心臓治療を提供することを目的としています。

- 2024年4月、アーンドラ・プラデーシュ州のY・サティア・クマール・ヤダフ保健大臣は、州内の公立総合病院(GGH)の診断施設を強化する提案を承認しました。この計画には、6台の新しいCTスキャン装置と3台のカテーテル検査装置が設置され、総投資額は約5億ルピーに上ります。これらの施設は、アーンドラ・プラデーシュ州の経済的に恵まれない患者の医療アクセスと診断能力の向上を目指しています。

- 2024年3月、カルナータカ州のチャマラジャナガル医科大学(CIMS)は、イェダプラにある同大学の集中治療棟にカテーテル検査室を設置することを提案しました。この施設は完成間近です。この施設には1億ルピーの投資が必要で、血管造影や血管形成術といった高度な低侵襲心臓手術を提供することを目指しています。この取り組みは、この地域における心臓救急医療の充実と死亡率の低減を目指しています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。