世界の乳製品タンパク質市場の規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

13.18

35.80

2024

2032

13.18

35.80

2024

2032

| 2025 –2032 | |

| USD 13.18 | |

| USD 35.80 | |

| % | |

|

世界の乳製品タンパク質市場:タイプ別(乳タンパク質、ホエイタンパク質、カゼインタンパク質)、含有量別(30%~85%、85%~95%、95%以上)、形態別(乾燥、液体)、用途別(ベーカリー製品、乳製品、スポーツ栄養、菓子、飲料、栄養補助食品、乳児用調合粉乳、栄養バー、朝食用シリアル、ソース、ドレッシング、調味料、RTEミール、肉および鶏肉製品) - 業界動向と2032年までの予測

乳製品タンパク質市場規模

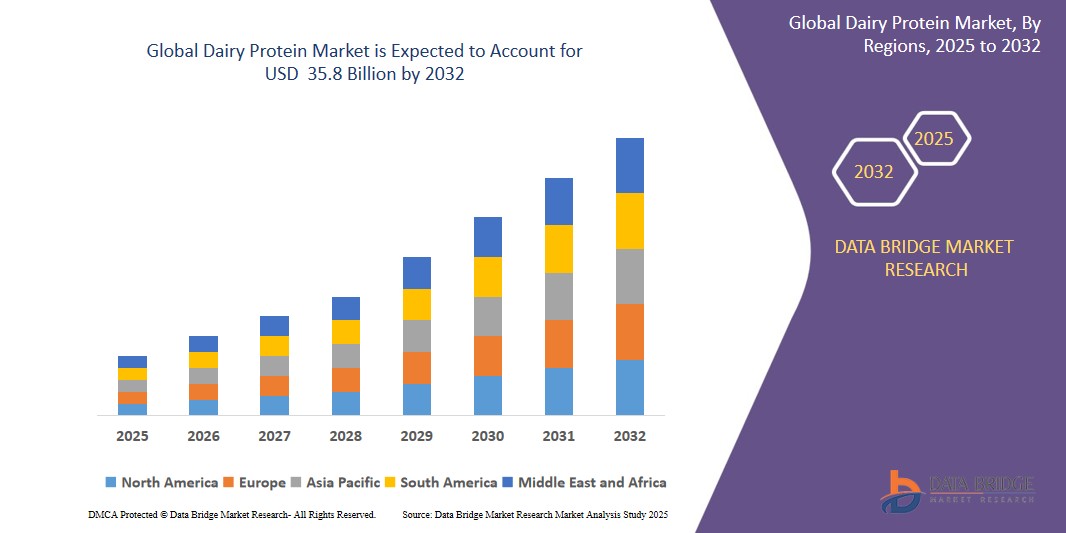

- 世界の乳製品タンパク質市場規模は2024年に131億8000万米ドルと評価され、予測期間中に5.8%のCAGRで成長し、2032年までに358億米ドル に達すると予想されています。

- 市場の成長は、主に健康意識の高まり、高タンパク質食品の需要増加、スポーツ栄養および乳児用調合乳分野の成長、パーソナルケア分野での用途拡大、そして特にアジア太平洋などの新興地域における可処分所得の増加によって推進されています。

- さらに、市場の成長は主に、乳製品加工における技術的進歩、製品用途の拡大、天然成分に対する消費者の嗜好の増加、栄養上の利点に対する意識の高まり、そして乳製品の生産とタンパク質の消費を世界的に促進する政府の支援的な取り組みによって推進されています。

乳製品タンパク質市場分析

- 乳タンパク質市場は、ホエイ、カゼイン、乳タンパク質濃縮物といった種類別に分かれており、栄養価の高さからホエイタンパク質が主流となっています。スポーツ栄養、機能性食品、乳児用調合乳からの需要の高まりが、世界的な市場拡大を牽引しています。

- 加工技術の進歩により、乳タンパク質の純度と機能性が向上し、新たな製品処方が可能になります。加水分解タンパク質やタンパク質ブレンドなどのイノベーションは、消化性と風味を向上させ、食品、飲料、パーソナルケア分野における用途を拡大し、市場全体の成長を促進します。

- 市場は、植物性タンパク質代替品や酪農に関連する環境問題といった課題に直面しています。しかしながら、継続的なイノベーション、製品の多様化、そして主要企業間の戦略的パートナーシップは、競争力を維持し、世界中の消費者の嗜好の変化に適応することに役立っています。

- 北米は世界の乳タンパク質市場を支配しており、市場シェアの約37.4%を占めています。この成長は、確立された乳製品産業、タンパク質強化製品に対する高い消費者需要、高度な加工技術、そして食品・栄養分野におけるイノベーションと製品の多様化に注力する主要市場プレーヤーの強力なプレゼンスによって牽引されています。

- アジア太平洋地域は、健康意識の高まり、可処分所得の増加、急速な都市化、そして高タンパク質食品への需要の高まりを背景に、乳タンパク質市場が最も急速に成長している地域です。インドや中国といった主要国は、乳製品産業の拡大と食生活の変化に支えられ、成長を牽引しています。

- ミルクプロテインセグメントは、その高い栄養価と機能的利点により、乳児用調製粉乳、スポーツ栄養、機能性食品分野での強い需要を反映し、約38.5%の市場シェアで乳製品プロテイン市場を支配すると予想されています。

レポートの範囲と乳タンパク質市場のセグメンテーション

|

属性 |

乳製品タンパク質の主要市場分析 |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

乳製品タンパク質市場の動向

「健康志向の消費者シフト」

- Consumers are increasingly aware of the importance of protein in supporting muscle growth, weight management, and overall wellness, which drives higher demand for dairy protein products as part of a balanced diet.

- The rise in lifestyle-related health issues like obesity and diabetes encourages consumers to seek nutrient-dense, high-protein foods, positioning dairy proteins as preferred options for maintaining metabolic health and controlling hunger.

- People are particularly focused on clean-label, natural ingredients, leading to increased consumption of minimally processed dairy proteins free from artificial additives and preservatives.

- Fitness enthusiasts and athletes boost the market by prioritizing protein intake for muscle repair and recovery, often choosing dairy proteins for their high bioavailability and essential amino acid profiles.

- Growing trends in personalized nutrition and wellness diets promote tailored protein consumption, with dairy proteins favored for their versatility, ease of incorporation in various food and beverage products, and proven health benefits.

Dairy Protein Market Dynamics

Driver

“Rising health awareness boosts demand for dairy proteins”

- Increasing consumer focus on balanced nutrition encourages incorporation of dairy proteins, recognized for their complete amino acid profile and benefits in muscle maintenance, weight management, and overall health support.

- Awareness of chronic diseases and lifestyle-related health issues motivates people to choose high-quality protein sources like dairy proteins to improve metabolism, boost immunity, and support cardiovascular health.

- Growing interest in fitness and active lifestyles drives demand for dairy proteins as effective supplements for muscle recovery, energy replenishment, and enhanced physical performance among athletes and health-conscious consumers.

- Educational campaigns and social media influence promote understanding of protein’s role in wellness, highlighting dairy proteins as natural, nutrient-rich options compared to synthetic or plant-based alternatives.

For Instance,

- In 2024, rising consumer demand for protein-rich diets drove growth in the dairy industry. High-protein products gained popularity, with companies innovating to meet health-focused preferences, blending traditional dairy and plant-based proteins to expand the market and satisfy diverse needs.

- Consumers increasingly seek functional foods fortified with dairy proteins, leveraging their benefits beyond basic nutrition to include gut health, bone strength, and anti-inflammatory properties, aligning with holistic health goals.

Restraint/Challenge

“High production costs limit expansion in dairy protein”

- The complex extraction and processing methods for dairy proteins require significant investment in advanced equipment and skilled labor, increasing overall production costs and limiting affordability for smaller manufacturers and new entrants

- Fluctuations in raw milk prices and supply disruptions contribute to inconsistent production expenses, making it challenging for companies to maintain stable pricing and profitability in the dairy protein market

- Energy-intensive processes and strict quality control standards add to operational costs, which can deter investment in expanding production capacities, especially in regions with high energy prices and limited infrastructure.

- Regulatory compliance related to food safety, labeling, and environmental sustainability demands additional expenditure, increasing barriers for companies looking to scale operations or enter new markets.

- High costs are often transferred to consumers through premium pricing, limiting mass-market penetration and making dairy protein products less accessible in price-sensitive developing economies.

Dairy Protein Market Scope

The market is segmented on the basis of functional type, content, form and application.

- By Type

The Milk Protein segment dominates with an estimated 36% revenue share in 2025, driven by its superior nutritional quality, high digestibility, widespread use in infant formulas, sports nutrition products, and growing consumer preference for natural, complete protein sources in functional foods.

The Milk Protein segment is anticipated to witness the fastest growth rate of around 6.3% due to increasing demand for affordable, high-quality protein sources in emerging economies, driven by rising health awareness, urbanization, and growing consumption of infant and sports nutrition products.

- By Content

The 30%-85% segment held the largest market revenue share in 2025, driven by its versatility, optimal protein concentration for nutritional supplements, and wide usage in sports nutrition, infant formula, and functional foods catering to health-conscious and performance-focused consumers.

The 30%-85% segment is expected to witness the fastest CAGR from 2025 to 2032, driven by rising demand for balanced-protein formulations in nutrition products.

- By Form

The dry segment held the largest market revenue share in 2025, driven by its extended shelf life, ease of storage and transportation, and cost-effectiveness in bulk handling. Its widespread use in infant formula, protein powders, and processed foods further contributed to its dominance in the dairy protein market.

The dry segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing demand for convenient, shelf-stable protein products, cost-effective logistics, and rising applications in sports nutrition, functional foods, and dietary supplements across both developed and emerging markets.

- By Application

The bakery product segment held the largest market revenue share in 2025, driven by its widespread consumer demand, versatility of dairy proteins in enhancing texture and shelf life, and the growing trend of high-protein, functional baked goods in daily diets.

ベーカリー製品セグメントは、高タンパク質スナックに対する消費者の嗜好の高まり、機能性食品の需要の増加、栄養価と保存安定性の向上のために乳タンパク質を取り入れた革新的な製品開発により、2025年から2032年にかけて最も速いCAGRを達成すると予想されています。

乳製品タンパク質市場の地域分析

- 北米は世界の乳タンパク質市場をリードしており、市場全体の約37.4%を占めています。このリーダーシップは、高タンパク質食品・飲料に対する消費者の強い需要、確立された乳製品産業、そして機能性食品やスポーツ栄養製品の普及によって支えられています。

- この優位性は、成熟した乳製品業界、タンパク質を豊富に含む食事に対する消費者の高い需要、スポーツ栄養、機能性食品、健康志向の食品および飲料のイノベーションにおける乳製品タンパク質の広範な使用によって推進されています。

- 大手企業は、変化する消費者の嗜好に応えるためにクリーンラベルの高タンパク製品の開発に注力しており、一方で堅牢な流通ネットワークが小売、フィットネス、ヘルスケアの各分野にわたる広範な入手可能性をサポートし、地域の成長をさらに促進しています。

北米乳製品タンパク質市場の洞察

北米の乳製品タンパク質市場は、高タンパク質および機能性食品に対する消費者の需要の増加、確立された乳製品インフラ、スポーツ栄養トレンドの高まり、乳製品タンパク質摂取に関連する健康上の利点に対する意識の高まりにより、37.4%という最大の収益シェアを獲得しました。

欧州乳製品タンパク質市場の洞察

欧州の乳タンパク質市場は、主に健康意識の高まり、タンパク質強化機能性食品の需要増加、高齢化人口の増加、持続可能でクリーンラベルの乳タンパク質製品への重点化により、予測期間を通じて大幅なCAGRで拡大すると予想されています。

アジア太平洋地域の乳製品タンパク質市場に関する洞察

アジア太平洋地域の乳製品タンパク質市場は、可処分所得の増加、健康意識の高まり、急速な都市化、中流階級人口の拡大、タンパク質を豊富に含む食事や革新的な乳製品ベースの栄養製品に対する需要の増加により、予測期間中に注目すべきCAGRで成長すると予想されています。

乳製品タンパク質市場シェア

乳製品タンパク質業界は、主に、次のような定評のある企業によって牽引されています。

- アーラフーズ (デンマーク)

- フォンテラ協同組合グループ(ニュージーランド)

- ネスレSA (スイス)

- ダノンSA(フランス)

- Glanbia plc (アイルランド)

- ラクタリスグループ(フランス)

- Saputo Inc.(カナダ)

- ヒルマーチーズカンパニー(米国)

- アグロプール協同組合(カナダ)

- ミルクスペシャリティーズグローバル(米国)

- マレー・ゴールバーン協同組合(オーストラリア)

- イングレディオン社 (米国)

- ロイヤル・フリースランド・カンピナNV(オランダ)

- カーベリーグループ(アイルランド)

- Volac International Ltd.(英国)

世界の乳タンパク質市場の最新動向

- 2025年5月、ダノンのオイコスブランドは、オゼンピックやウィーゴビーなどのGLP-1阻害薬の服用者をターゲットとした新しいプロテインシェイクを発売しました。これらの食欲抑制薬の登場により、高タンパクで適量を摂取できる食品の需要が高まっています。このシェイクには5グラムの食物繊維が含まれており、米国の主要小売店で販売されています。

- 2024年10月、イスラエルの企業DairyXは、牛を使わずに、伸びが良くクリーミーなチーズに不可欠なカゼインタンパク質を生産できる酵母株を開発しました。この革新は、植物由来チーズの食感の問題を解決し、環境への影響を軽減します。規制当局の承認は2027年までに得られる見込みです。

- 2025年2月、世界有数の乳製品協同組合であるArla Foodsは、収益が2023年の137億ユーロから2024年には138億ユーロへとわずかに増加すると報告しました。同社は、乳製品価格の上昇と消費者の購買力の安定により、2025年にはさらなる収益増加を予測しています。

- 2025年4月、黄色いエンドウ豆から作られるピーミルクは、牛乳に代わる持続可能で栄養価の高い代替品として注目を集めています。1カップあたり7.5グラムのタンパク質を含み、牛乳に比べて水の使用量が大幅に少なく、温室効果ガスの排出量も少ないという利点があります。しかしながら、消費者の受け入れには依然として課題が残っています。

- 2025年3月、Lactalis UK & Irelandは、リンダール初のプロテインチーズ&ミルク飲料を発売しました。カッテージチーズ、ゴーダスライス、ギリシャチーズ、クワルクなど、高タンパク・低脂肪の製品を取り揃えています。これらの製品は、体重管理や筋肉の回復のためのタンパク質を求める健康志向の消費者のニーズに応えています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。