世界的な眼科疼痛ウイルス治療市場規模、株式および傾向分析レポート

Market Size in USD Billion

CAGR :

%

USD

79.21 Million

USD

146.61 Million

2024

2032

USD

79.21 Million

USD

146.61 Million

2024

2032

| 2025 –2032 | |

| USD 79.21 Million | |

| USD 146.61 Million | |

| % | |

|

医薬品の種類(抗炎症剤、鎮痛剤、抗感染剤、生態学的、および持続解放インプラント)、インディケーション(術後軟骨症、筋肉内炎症、内視鏡炎、腎血管疾患、および神経疾患)、配達ルート(脳内注射、脳内炎症、内視鏡炎、腎血管疾患、血管疾患)、および神経疾患)、配達ルート(脳内視鏡検査、脳内視鏡検査)、および内視鏡検査(脳内視鏡検査)

Ocular の苦痛 Intravitreal の処置の市場のサイズ

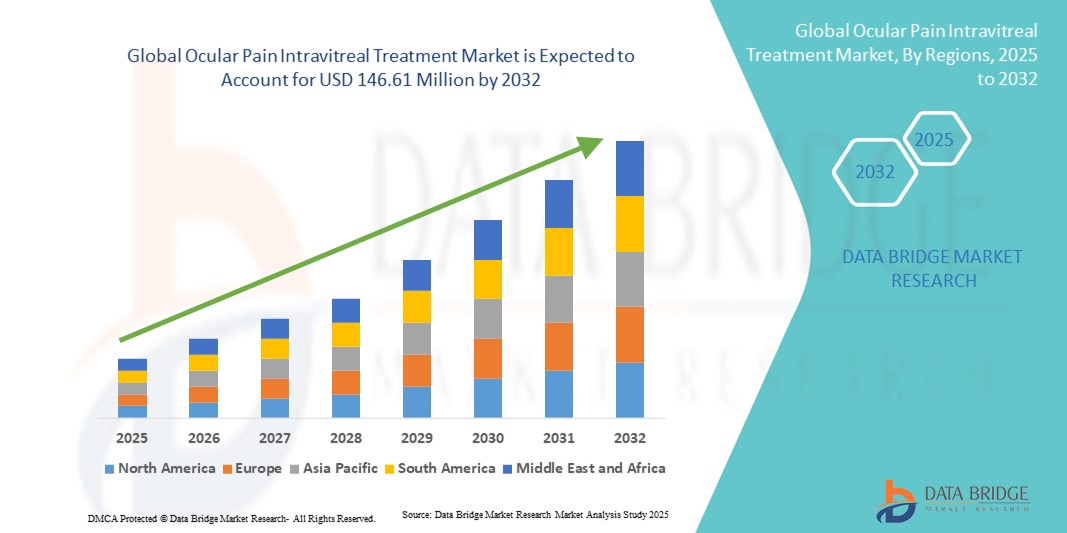

- 世界的な眼科の苦痛のintravitrealの処置の市場のサイズはで評価されました2024年のUSD 79.21百万そして到達する予定ツイート 2032年までの146.61百万, お問い合わせCAGR の 8.00%予報期間中

- 市場成長は、尿道炎、子宮内膜炎、および術後の合併症などの眼科障害の上昇前因によって主に駆動され、多くの場合、子宮内膜介入を必要とする重要な眼科の痛みを引き起こします

- さらに、持続放出インプラントの採用増加、標的抗炎症剤、および革新的な鎮痛剤の採用は、効果的な楕円疼痛管理のための好ましいモダリティとして、intravitreal配信を配置しています。 これらの臨床および技術の進歩は処置のuptakeを加速しま、それによって世界中拡大の燃料を供給します

Ocular の苦痛 Intravitreal の処置の市場分析

- 抗炎症剤、鎮痛剤、抗感染剤、生態学的および持続解放インプラントを含む眼科の痛みのintravitreal処置は、によって引き起こされる痛みを管理するための重要な治療オプションとして現れます尿道炎,子宮内膜炎、網膜血管疾患および術後の合併症は、標的の配信とより長い治療効果による

- これらの治療に対する増加の需要は、主に眼科障害の増加の優先順位、眼科の外科的容積の増加、および繰り返された介入を最小限にし、忍耐強い結果を高める効果的な、長時間作用ソリューションの必要性によって燃料を供給されます

- 北米は、2024年に42.5%の最大の収益分配で、楕円の痛みの侵入治療市場を支配し、先進医療インフラ、眼薬およびインプラントの堅牢なパイプライン、および米国における病院および専門眼科クリニックの横断的治療の高い採用によって支持しました。

- アジア・パシフィックは、予報期間中の眼科疼痛治療市場で最も急速に成長する地域であることが期待され、眼科疾患の増加、高度眼科ケアへのアクセス拡大、眼科に焦点を当てた研究とインフラへの投資の増加

- 抗炎症薬のセグメントは、2024年に43%のシェアを持つ楕円の痛みのintravitreal治療市場を支配し、コルチコステロイドおよびステロイドインプラントの広範な使用に起因し、眼球炎症および関連する痛みを軽減するための金規格として

レポートの規模およびOcularの痛みのintravitrealの処置の市場区分

| アトリビュート | Ocular の苦痛 Intravitreal の処置のキー マーケットの洞察 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

ヨーロッパ

アジアパシフィック

中東・アフリカ

南米

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

Ocular の苦痛 Intravitreal の処置の市場の傾向

Sustained-Release Implantsの進歩およびターゲットを絞られた療法

- 世界的な眼科の痛みのintravitreal治療市場での有意で加速傾向は、炎症や痛みから長期にわたる救済を提供するように設計された持続放出インプラントと生物学的の急速な採用であり、反復的な注射の負担を軽減

- たとえば、Ozurdex(デキサメタゾンイントラビエントリアルインプラント)は、尿道および黄道浮腫に関連する眼科の痛みを管理するための強力な臨床受諾を得ており、拡張解放技術が治療プロトコルを再構築する方法を実証しています。

- 新しい研究パイプラインは、治療精度を高め、楕円組織の浸透を改善し、全身の副作用を最小限に抑える標的薬配信システムに焦点を当てています。

- たとえば、調査生態学およびデポベースの鎮痛製剤は、慢性眼瞼の痛みや再発炎症条件を持つ患者のためのより効果的で持続的な救済を提供するために開発されています

- 高度なポリマー技術とナノキャリアシステムの統合は、非公式療法に制御された薬物放出を容易にし、より予測可能な治療結果とより少ない介入訪問を提供

- より長時間作用、精密ターゲティング、および患者に優しい非公式治療に対するこの傾向は、眼科の痛み管理を再定義し、有効性と利便性のための新しいベンチマークを作成します

Ocular の苦痛 Intravitreal の処置の市場 動的

ドライバー

眼科障害および外科的介入の有利な負担

- 尿道炎、子宮内膜炎、および網膜血管疾患などの眼科疾患の増大可能性は、白内障および消化管外科の上昇率と組み合わせ、眼科の痛みに対する非公式治療の需要を大幅に促進しています

- 例えば、2024年、アメリカ眼科アカデミーは、手術後の眼科炎症症例の手術を強調し、イントラウイルス性コルチコステロイドとインプラントの効果的な疼痛管理の役割を果たした。

- 高度の眼球療法の忍耐強い意識が育つにつれて、非現実的な治療は、長期にわたる眼球炎症の制御のための重要なツールとして認識され、持続的な救済と視力的な結果を維持する

- さらに、先進市場における医療インフラの拡充と再投資支援の拡充は、病院や専門眼クリニックにおけるイントラウイルス性疼痛管理ソリューションの採用を推進しています。

- ターゲットを絞った、ローカライズされた薬物濃度を届けるイントラヴィレアル療法の実証済みの能力は、それらが全身の薬よりも優先的に選択され、眼科の痛みの治療戦略における優位性を強化します。

- パーソナライズされた医療と眼科パイプラインにおける継続的な革新へのシフトは、さらに、世界的なイントラウイルス性疼痛管理ソリューションの成長軌跡を強化します

拘束/チャレンジ

侵襲的配送方法と規制遵守ハルール

- 感染のリスク、網膜の剥離、および患者の不快感を含む、イントラウイルス注射の侵襲的な性質を取り巻く懸念は、眼科の痛みの侵入治療の広範な受け入れへの大きな課題をポーズします

- たとえば、intravitrealの手順に関連付けられている内視鏡炎の複数のレポートは、患者とプロバイダーの両方の注意を高まらせ、特定の地域での摂取量を制限しました

- 最小侵襲的配送システムにおけるイノベーションを通じたこれらの安全上の懸念に対処する、インジェクションデバイスの改善、および患者の信頼を高めるための強化された医師のトレーニングが不可欠です。

- さらに、複雑な治療のための厳格な規制経路、広範な臨床試験と安全評価を必要とする、新しい痛み管理薬やインプラント製品の承認や市場参入を遅らせることができます

- 伝統的なトピックやシステム的な痛みの治療と比較して、高度なインプラントやバイオロジックの比較的高いコストは、特にコスト感度の高い医療市場で採用する障壁を作成します

- 手頃な価格の価格のモデル、合理化された規制戦略、および治療上の利点の高められた忍耐強い教育を通してこれらの課題を克服することは、非公式の痛みの治療市場で持続的な成長のために不可欠です

Ocular の苦痛 Intravitreal の処置の市場規模

市場は薬剤のタイプ、徴候、配達ルートおよびエンド ユーザーに基づいて区分されます。

- 医薬品の種類別

薬の種類に基づいて、眼科の痛みのintravitreal治療市場は、抗炎症剤、鎮痛剤、抗感染剤、生物学的製剤、および持続放出インプラントに分けられます。 抗炎症剤は、2024年に最大の収益分配で市場を支配し、43%を占めています。 そのようなコルチコステロイドsデキサメタゾンそしてtriamcinoloneはuveitisおよびポスト外科合併症のような条件にリンクされる炎症および楕円の苦痛を管理するために広く利用されています。 彼らの実証済みの有効性、よく確立された臨床ガイドライン、およびintravitreal注射とインプラントフォームの両方の可用性は、それらに優先される第一線治療を行います。 病院および眼科医はまた急速な軽減、再発率を削減し、長期治療の結果を維持する能力のために抗炎症薬を支持します。 さらに, 持続解放ステロイドインプラントの増加の可用性は、さらに、このセグメントの優位性を高めます.

バイオロジカルセグメントは、2025年から2032年までの最速成長率を目撃し、モノクローナル抗体および遺伝子治療ベースのアプローチの拡大パイプラインによって燃料供給され、根本的な炎症経路を標的としています。 バイオロジックは、従来のコルチコステロイドが効果が少なく、副作用に関連した慢性眼科の痛み症例に対処する可能性があります。 また、臨床試験の増大数、規制当局の承認、眼科生物製剤の増大投資の増加が採用を強化しています。 ターゲットを絞った療法の意識を高め、パーソナライズされた薬へのプッシュと相まって、バイオロジックを最速で展開するカテゴリにします。

- インディケーション

徴候に基づいて、市場は術後眼の苦痛、筋肉内炎症、網膜管の病気、網膜の痛みおよび神経痛に分けられます。 術後眼の痛みは2024年に市場を支配し、白内障および消化器外科の上昇の全体的な容積によって支えられました。 これらの手順は頻繁に炎症と痛みにつながる, 実質のコルチコステロイドと効果的な回復のために重要な鎮痛. 病院と血管外科センターは、合併症を最小限に抑え、回復期間を短縮し、患者の快適性を向上させるために、非公式療法に大きく依存しています。 セグメントの成長は、先進市場における有利な償還方針によっても支持され、複数のポスト外科的介入の必要性を削減するサステナブルリリースインプラントの採用が増加しました。

神経病眼疾患の認知度を高め、慢性眼科疼痛管理における未測定ニーズを増加させることで、予測期間中に最も急速に成長するセグメントであることが期待されます。 従来の治療は、神経関連の痛みを適切に対処し、新しい鎮痛剤、生態学、および高度な配信システムのための機会を作成します。 イオンチャネルモジュレータや神経保護生物学などの標的経路の研究は急速に拡大しています。 眼科医と患者の間で意識が成長するにつれて、診断機能の進歩と相まって、神経病性眼科の痛みの治療は、需要の急激な上昇を経験するために計画されています。

- 配送経路から探す

配達ルートに基づいて、市場はintravitrealの注入、periocular、intracameralおよびsubretinalに分けられます。 Intravitreal注射は、2024年に最大のシェアで市場を支配し、高い薬物濃度を直接目のポスターセグメントに提供する金基準を維持しています。 コルチコステロイド、抗生物質、および生態学のための病院および専門医のどちらの病院そして専門医でその広範な使用は楕円の苦痛管理の中心ロールをアンダースコアします。 物理学者は、その精度、迅速な行動のオンセット、およびシステム露出を迂回する能力のためにこのルートを好む、それによって副作用を最小限に抑えます。 臨床データおよび数十年の経験によって支えられる十分に確立された安全プロフィールは、更に一流の位置を保護します。

サブレシナルルートは、遺伝子治療や再生医療などの高度療法で増加するアプリケーションによって駆動され、予測期間にわたって最速成長配信モードになることを期待しています。 採用の初期段階ではまだ、副産物配達は、痛みに関連した網膜障害に対する高度に標的された治療を可能にします。 R&D、治験活動、およびマイクロ外科技術の技術革新におけるライジング投資は、このセグメントの成長を加速しています。 より多くの療法が規制当局の承認を得るにつれて、今後数年間で強力な成長軌道を追い出すために副産物配達が期待されます。

- エンドユーザーによる

エンドユーザーに基づいて、市場は病院、断熱外科センター(ASC)、専門眼科クリニック、薬局に分けられます。 病院は2024年に市場を支配し、55%の収益シェアを占め、先進的なインフラでサポートし、複雑な外科的介入を処理する能力、および最新の非公式療法へのアクセスを認めた。 病院はまた、直感的な痛みの軽減を必要とする術後および急性の条件のためのより高い忍耐強い負荷を管理し、それらを楕円の痛みの治療のための第一次設定にします。 熟練した眼科医の存在は、先進国の償還フレームワークと相まって、このセグメントのリーダーシップを強化します。

Ambulatory 外科センター(ASC)は、2025年から2032年までの最速成長を目撃する見込みで、費用対効果の高い外来眼法へのグローバルなシフトによって推進されています。 ASCは、病院と比較して、より迅速なターンアラウンド、治療コストの削減、および患者の利便性を提供します。 小児外の設定で白内障および網膜手術の需要が高まっています。また、先進的な非公式薬送達能力を持つASCを装備し、迅速な採用を促進しています。 この傾向は、特に北米とアジア太平洋で顕著で、医療システムが効率性と患者中心のケアに焦点を当てています。

Ocular の苦痛 Intravitreal の処置の市場地域の分析

- 北米は、2024年に42.5%の最大の収益分配で、楕円の痛みの侵入治療市場を支配し、先進医療インフラ、眼薬およびインプラントの堅牢なパイプライン、および米国における病院および専門眼科クリニックの横断的治療の高い採用によって支持しました。

- 領域内の患者やプロバイダは、視力的な結果を維持しながら、楕円の痛みを軽減するintravitreal注射、インプラントおよび生物学的製剤の有効性を非常に評価します

- この広範囲にわたる採用は、有利な償還方針、堅牢な臨床研究基盤、および主要な製薬およびバイオテクノロジー企業の存在によって積極的に新しい眼科療法を開発することによって支持されます

U.S. Ocular の痛みの Intravitreal の処置の市場洞察

米国の楕円形の痛みのウイルス治療市場は、北米で2024年の最大の収益シェアをキャプチャし、網膜疾患、グルコマ、手術後の合併症の高前因によって燃料を供給しました。 患者は、効果的な痛みの軽減とより良い視覚的結果のために、より積極的に治療を優先しています。 大手製薬会社の強力な存在は、バイオロジスティックスとサステンドリリースインプラントの急速な採用と組み合わせ、市場成長を促進します。 また、サステナブル・リリース・デポスなど、先進的なデリバリー・システムを幅広く活用し、市場拡大に貢献しています。

ヨーロッパ Ocular の苦痛 Intravitreal の処置の市場洞察

ヨーロッパの楕円の痛みのintravitreal治療市場は、主に白内障および網膜条件のための外科的介入の増加によって運転される、予測期間全体で実質的なCAGRで拡大するように計画されています。 眼球炎症および内視鏡炎の増大負荷は、非ウイルス注射の採用を促進しています。 欧州のヘルスケア プロバイダーは、革新的なバイオ ロジックおよび抗炎症薬に耐久性のある救済を提供するように描画されます。 地域は、病院、専門眼科クリニック、および血管外科センターを横断して強い採用を経験しています。

U.K. Ocularの痛みのintravitrealの処置の市場洞察

U.K. 眼科の痛みのintravitreal治療市場は、予測期間中に注目すべきCAGRで成長することを期待しています, 筋肉内炎症の発生率を高め、高度な眼科ケアの患者意識を高めました. また、術後の眼瞼の痛みや視力の保存に対する懸念は、非vitrealの生態学と鎮痛療法を採用する患者やプロバイダを奨励しています。 全国の堅牢な医療インフラは、高い臨床試験活動と相まって、市場成長を加速し続けることが期待されています。

ドイツ Ocular の苦痛 Intravitreal の処置の市場洞察

予測期間中、ドイツ眼科の痛みの無軌道治療市場は、生態学の需要を増加させ、眼科の痛みを効果的に管理するために持続放出インプラントを燃やすことが期待されます。 ドイツは先進医療インフラを整備し、新たな治療法の統合を臨床実践に支援するイノベーションに重点を置いています。 公的および私的ヘルスケア設定の強力な採用とともに、主要な学術研究機関の存在は、長期にわたる痛み管理に適した非公式ソリューションの使用を促進しています。

Asia-Pacific Ocular Pain Intravitreal 治療市場 洞察

アジア・パシフィックの眼科疼痛治療市場は、2025年から2032年の予測期間で23%の最も速いCAGRで成長し、外科的容積の増加、老化の人口、および糖尿病性網膜症および網膜血管疾患の上昇の発生率によって運転されます。 政府主導の医療モダナイゼーションで支えられた先進的なバイオロジカルと革新的なデリバリールートの領域の普及が急速に加速しています。 さらに、APACは、眼科薬の治験および製造拠点として出現すると同時に、より広い患者基盤への実用性およびアクセシビリティが拡大しています。

日本眼科疼痛ウイルス治療市場インサイト

先進医療システム、高齢化人口増加、網膜および炎症性眼疾患の負担が高まっています。 日本市場は、持続可能な放出インプラントの採用を推進し、革新的なバイオロジカルと医薬品由来のシステムに重点を置いています。 糖尿病性眼疾患管理を含む広範囲の眼科ケアプロトコルでウイルス治療の統合は、成長を燃料化しています。 また、日本の技術の進歩と患者様が最小限の侵襲的治療に対する要求が、さらなる導入の加速が期待されます。

インド Ocular 痛み Intravitreal 治療市場 洞察

2024年にアジア・パシフィックで最大の市場収益シェアを占めるインドの眼科疼痛intravitreal治療市場は、術後疼痛、感染症、糖尿病性網膜症関連の合併症の国の高前因に起因しています。 インドは、眼科手術の最大の市場の一つとして位置付けられ、内臓療法は、病院や専門クリニックでますます普及しています。 強固な国内医薬品製造と共に、眼科インフラの拡充と費用対効果の高いイントラウイルス注射の可用性への押しは、インドの市場を推進する重要な要因です。

Ocular の苦痛 Intravitreal の処置の市場シェア

Ocular の苦痛 Intravitreal の処置の企業は主に下記のものを含む十分に確立された会社によって、導きます:

- AbbVie Inc.(米国)

- Genentech, Inc.(米国)

- Regeneron Pharmaceuticals Inc.(米国)

- Novartis AG(スイス)

- Alimera Sciences(米国)

- Bausch + Lomb(アメリカ)

- サンテン製薬株式会社(日本)

- アイポイント製薬株式会社(米国)

- Clearside Biomedical. (米国)

- アルコン株式会社(スイス)

- Apellis Pharmaceuticals, Inc.(米国)

- Opthea Limited(オーストラリア)

- アステラス製薬株式会社(米国)

- Oxurion NV (ベルギー)

- Ocular Therapeutix, Inc.(米国)

- カラ医薬品株式会社(米国)

- バイエルAG(ドイツ)

- SIFI S.p.A.(イタリア)

- Dompé(イタリア)

グローバル眼科疼痛ウイルス治療市場における最近の発展は何ですか?

- 2025年7月、前方位相2a試験結果 PER-001、新低速リリースイントラウイルス注入標的内分受容体が公開されました。 インプラントは、視力、網膜症、およびグルコマおよび糖尿病性網膜症患者における構造的パラメータの改善を実証し、進行性眼疾患に関連する痛みや虚血症に対処する可能性を強調しました

- 2025年4月、ANI Pharmaceuticalsは、FDAの承認がILUVIEN®のラベルを拡大し、ポスターセグメントの慢性非感染性尿道炎を含むことを発表しました。 ラベルの延長は、眼科の痛み管理におけるインプラントの臨床ユーティリティを強化し、痛みを伴う炎症性眼疾患に苦しむ患者のための耐久性のある無軌道オプションで医師に提供します

- 2025年3月、米国FDAはフラクシノロンのアセトニドのintravitrealのインプラントILUVIEN®を承認し、眼(NIU-PS)のポスターセグメントに影響を与える慢性の非感染性尿道の治療のために、糖尿病性浮腫を超えて治療範囲を拡大しました。 この承認は、炎症性関節痛および関連する合併症のための効果的な長期ソリューションとして、イントラウイルスインプラントの成長認識を下見します

- 2025年2月、GenentechのSusvimo®は、糖尿病性浮腫(DME)の治療のためにranibizumabの継続的な配信プラットフォームとして米国FDAの承認を受けました。 この承認は、標準的な注射よりも少数の非公式治療薬を患者に提供し、痛みの負担を軽減し、長期の網膜疾患管理の遵守を改善します

- 2024年10月、Okyoファーマは、ニューロパシー性角膜痛(NCP)用に設計された新治療法「OK-101」の第2相臨床試験で第一次患者を服用しました。 限られた処置の選択の慢性の眼科の痛みの状態として、このマイルストーンの試験は、持続的な角膜の痛みを和らげる非全身の解決を開発するための重要なステップを表します

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。