グローバル包装樹脂市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

329.53 Billion

USD

557.78 Billion

2024

2032

USD

329.53 Billion

USD

557.78 Billion

2024

2032

| 2025 –2032 | |

| USD 329.53 Billion | |

| USD 557.78 Billion | |

| % | |

|

グローバル包装樹脂市場セグメンテーション、タイプ(低密度ポリエチレン(LDPE)、ポリプロピレン(PP)、高密度ポリエチレン(HDPE)、ポリスチレン(PS)、ポリスチレン(EPS)、ポリエチレンテレフタレート(PET)、ポリビニル塩化(PVC)))、アプリケーション(食品および飲料、消費財、ヘルスケア、産業およびその他) - 業界動向と2032への予測

包装の樹脂の市場のサイズ

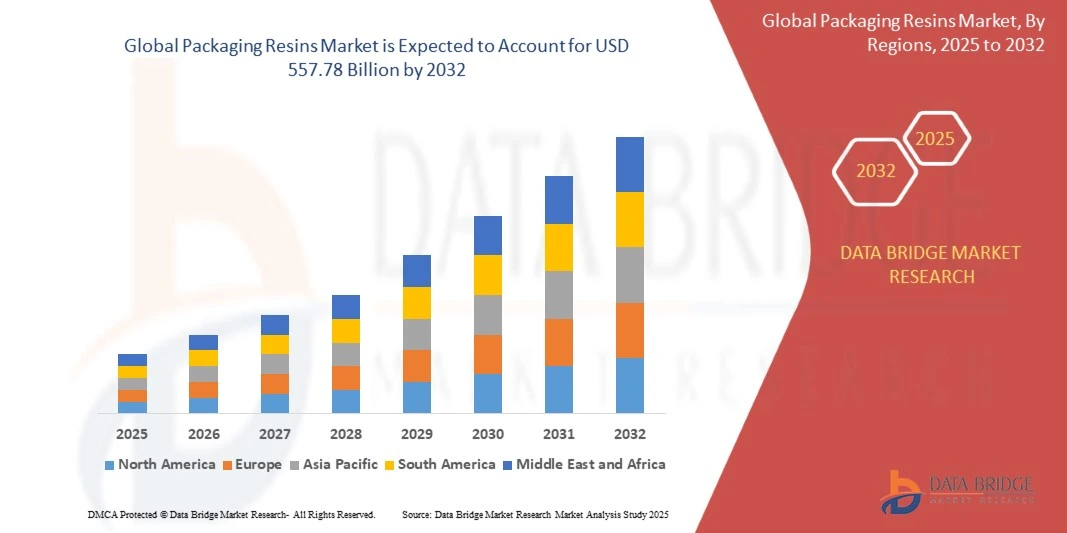

- グローバル包装樹脂市場規模が評価されました2024年のUSD 329.53億そして到達する予定米ドル 557.78 億 によって 2032, お問い合わせ6.8%のCAGR予報期間中

- 市場成長は、食品や飲料、ヘルスケア、消費財業界における軽量、耐久性、費用対効果の高いパッケージングソリューションの需要が高まっています。 パッケージ製品、急速な都市化、および電子商取引の拡大の上昇の消費は世界的な樹脂ベースの包装材料のより大きい信頼性を運転しています

- さらに、持続可能でリサイクル可能なパッケージングソリューションへの成長したシフトは、先進的な樹脂製剤を革新するためにメーカーをプッシュしています。 これらの収束因子は、パッケージング樹脂の採用を加速し、市場の成長を著しく向上しています

包装樹脂市場分析

- 包装の樹脂は適用範囲が広いフィルム、堅い容器、びんおよび産業包装の適用の作成で使用される多目的ポリマー材料です。 耐久性、耐薬品性、軽量性能など、商品の保護、棚寿命の延伸、安全輸送の確保に不可欠です。

- 包装樹脂の需要は、主に包装食品産業の成長によって燃料を供給され、ヘルスケア包装ニーズを高め、電子商取引の出荷を拡大しています。 また、再生可能で環境に優しい材料を促進する持続可能性への取り組みや規制は、パッケージング分野における樹脂イノベーションの未来を形作ります。

- アジア・パシフィックが包装樹脂市場を廃止 シェアで食品や飲料の消費の急激な成長、電子商取引パッケージの拡大、大規模なプラスチック樹脂製造ハブの存在による2024年に50%以上

- 北米は、パッケージ食品の消費の増加、ヘルスケアパッケージングの需要の増加、およびオンライン小売出荷における成長により、予測期間中に包装樹脂市場で最速成長地域であることが期待されます

- ポリプロピレン(PP)の区分は適用範囲が広い包装、堅い容器および分類の適用の広範な使用による2024年の31.9%の市場占有と市場を、分けました。 PPは優秀な明快さ、高い化学抵抗および軽量の特性を提供し、それに複数のエンドユースの企業を渡る好まれた材料を作ります。 その費用効果が大きいおよび再生利用できままた持続可能な包装の解決の採用を高めます。 食品、飲料、消費財のパッケージングの需要が高まっています。PPは、開発および新興市場で重要な材料を残しています。

レポートの規模および包装の樹脂の市場区分

| アトリビュート | 包装の樹脂の主市場の洞察 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

ヨーロッパ

アジアパシフィック

中東・アフリカ

南米

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、データブリッジ市場調査によってキュレーションされた市場レポートには、インポートエクスポート分析、生産能力概要、生産消費分析、価格推移分析、気候変動シナリオ、サプライチェーン分析、バリューチェーン分析、バリューチェーン分析、原材料/消耗品概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークなどがあります。 |

包装樹脂市場動向

サステナビリティへの貢献

- 包装樹脂市場は、消費者や規制当局が環境負荷の低減で材料を求めるため、持続可能な包装ソリューションの需要が高まっています。 再生可能、生分解性、およびバイオベースの樹脂へのシフトは、製品開発を再構築し、食品や飲料、医薬品、消費財などの業界の循環経済原則と材料効率を強調しています。

- たとえば、ExxonMobil ChemicalとSABICは、認定再生可能なポリプロピレンと化学的にリサイクルされたポリエチレン樹脂のラインを備えた主要な革新で、ブランドが妥協することなく持続可能性の約束を満たすことを可能にします。 グリーンドットバイオプラスチックは、既存の包装プロセスと互換性のある堆肥樹脂グレードを導入し、柔軟で硬質なパッケージングにおける生分解性代替品の増大促進を図っています。

- リサイクルおよびバイオベースの樹脂の障壁の特性、明快さおよび強さを高める技術進歩はプロダクト保存および棚の生命延長が重要である敏感な食品包装の適用で拡大された使用を可能にします。 IoTセンサーやQRコードなどのスマートパッケージの統合も組み込まれており、透明性と消費者のエンゲージメントを向上させます。

- 樹脂メーカー、コンバーター、ブランド所有者、リサイクル業者を含む業界全体のコラボレーションは、持続可能な樹脂製品およびサプライチェーンの透明性の採用を加速しています。 樹脂対レジンリサイクル、堆積システム、再生品コンテンツ認定への取り組みが主流となり、継続的な市場転換を推進

- ライジング電子商取引の成長は、耐久性、軽量、保護包装材料、高性能、持続可能な樹脂のさらなる燃料供給需要を必要とします。 消費者の利便性と安全性を優先し、プラスチック廃棄物削減に関する規制の義務と相まって、持続可能な樹脂の採用の長期的重要性を強調

- 持続可能なパッケージングの焦点は、継続的なイノベーション、拡張アプリケーション、および規制の勢いを促進し、指数関数的な成長と広範囲にわたる受諾で包装樹脂市場をシェイピングする決定的な傾向であることが示されています

包装樹脂市場ダイナミクス

ドライバー

消費者の利便性向上

- 便利で使いやすい、そしてオンザ・ゴーの包装のフォーマットのための消費者好みを育てることは包装の樹脂の市場を促進する重要な運転者です。 樹脂は、柔軟な包装、再封容器、および拡張棚寿命と使いやすさをサポートする軽量フィルムの生産を可能にします

- たとえば、シングルサーブスナック包装および準備された食事市場における急速な成長は、DowやLyondellBasellなどのメーカーが、柔軟で多層パッケージングソリューションの樹脂を仕立てています。 電子商取引のサージはより安全なプロダクト配達を保障するために耐久および保護樹脂に基づく包装のための要求を高めました

- 消費者は、製品の完全性を損なうことなく、利便性を提供し、マイクロバブル、リサイクル可能、および剥離可能なパッケージングなどのイノベーションの需要を押し出す包装フォーマットをますます。 これらは、ユーザーエクスペリエンスを向上させ、忙しいライフスタイルに合わせて整列し、さらに樹脂用途を拡大します。

- 包装樹脂は、製品の鮮度を維持し、汚染を防止し、食品廃棄物の最小化に不可欠であり、利便性重視の市場の重要性を再構築します。 機能性包装ソリューションは、食品、飲料、パーソナルケア業界における樹脂消費量の上昇を支援します。

- コンビニエンスパッケージの消費者主導の需要は、包装樹脂市場でのコア成長エンジンを形成し、樹脂生産者やコンバーターを奨励し、急速に革新し、進化する消費者行動を満たすために製品を拡大する

拘束/チャレンジ

原料価格の変動

- 原材料価格のボラティリティは、パッケージング樹脂市場にとって重要な拘束力を持ち、サプライチェーン全体で生産コストと収益性に影響を与えます。 エチレン、プロピレン、ベンゼンなどの主要な石油化学原料の価格の変化は、樹脂メーカーの予測不可能なコスト構造につながる

- たとえば、グローバル供給の混乱と地政的緊張は、定期的に樹脂価格の急激な変動を引き起こし、BASF、Dow、SABICなどの主要なプレーヤーの調達と価格設定戦略を組み合わせています。 原料の価格の変動はまたブランドの所有者およびコンバーターのための契約交渉そして余白に影響を与えます

- 原料価格の不安定性は包装の樹脂の企業内の長期投資の計画そして革新の努力を妨げます。 持続可能性とパフォーマンスの属性に競争するために努力する小規模なメーカーやスタートアップにとって、不確実性とリスクが増加します。

- 化石由来の飼料製品に対する市場の依存性は、原油価格の分散性に曝露しますが、バイオベースの樹脂生産は、いくつかの緩和の可能性を提供しています。 しかし、バイオベースの代替品のスケールは、資本の集中力を維持し、農業商品価格のスイングの対象となります

- 結論として、包装樹脂の需要は強く、原料価格のボラティリティは、安定した市場成長にチャレンジします。 戦略的な調達、多様化するフィードストック開発、およびコスト最適化は、市場のレジリエンスと継続的な革新のために不可欠です

包装の樹脂の市場規模

市場はタイプおよび適用に基づいて区分されます。

• タイプによって

タイプに基づいて、包装樹脂市場は低密度ポリエチレン(LDPE)、ポリプロピレン(PP)、高密度ポリエチレン(HDPE)、ポリスチレン(PS)および拡大されたポリスチレン(EPS)、ポリエチレンテレフタレート(PET)、ポリ塩化ビニル(PVC)に区分されます。 Polypropylene (PP) の区分は 2024 年に 31.9% の最大の市場収益のシェアを、適用範囲が広い包装、堅い容器および分類の適用の広範な使用に起因しました。 PPは優秀な明快さ、高い化学抵抗および軽量の特性を提供し、それに複数のエンドユースの企業を渡る好まれた材料を作ります。 その費用効果が大きいおよび再生利用できままた持続可能な包装の解決の採用を高めます。 食品、飲料、消費財のパッケージングの需要が高まっています。PPは、開発および新興市場で重要な材料を残しています。

ポリエチレンテレフタレート(PET)セグメントは、2025年から2032年までの最も速い成長率を目撃し、飲料およびヘルスケア産業におけるペットボトルや容器の需要が高まっています。 ペットの強度、透明性、およびガスに対するバリア特性は、炭酸飲料、ボトル入り水、医薬品包装に最適です。 軽量、リサイクル可能、環境に優しい材料の消費者の好みを増加させ、持続可能なパッケージングへの取り組みにおけるペットの採用をさらに加速します。 政府やブランドから円の経済慣行への押しは、予測期間にわたってペット需要を強化することが期待されています。

• 適用によって

用途に応じて、包装樹脂市場は食品・飲料、消費者商品、ヘルスケア、産業、その他に分けられます。 フード&ビバレッジのセグメントは、2024年に最大の市場収益シェアを占め、パッケージ食品、ボトル入り飲料、およびすぐに食べられる食事の大量消費によってサポートされています。 都市化を促進し、中級の人口を増加させ、食生活パターンを変えていくことで、耐久性、安全、軽量なパッケージングソリューションが求められます。 長期貯蔵寿命の必要性および汚染に対する保護は食糧および飲料の包装の樹脂のさらなる運転された信頼性を備えています。

ヘルスケアセグメントは、2025年から2032年までの最速成長率を目撃し、安全性、滅菌、医薬品、医療機器、診断製品に対するタンパー明白なパッケージングの需要が高まっています。 医療用医薬品の普及、医薬品製造の進展、およびパーソナライズされた医薬品の成長傾向は、高性能樹脂の採用を加速する重要な要因です。 また、製品の整合性や患者の安全確保をグローバルに重視し、樹脂ベースのヘルスケアパッケージングソリューションのイノベーションを推進し、堅牢な未来の拡大に向けたこのセグメントを位置づけています。

包装樹脂市場地域分析

- アジア・パシフィックは、食品・飲料消費の急激な成長、電子商取引パッケージの拡大、大型プラスチック樹脂製造ハブの存在を牽引し、2024年に最大50%以上の収益シェアを誇る包装樹脂市場を廃止しました。

- 地方の費用対効果の高い生産エコシステム、パッケージングイノベーションへの投資を増加させ、樹脂ベースのパッケージング材料の輸出を成長させ、市場拡大を加速

- 新興国における熟練した労働、支援政府のイニシアチブ、高速化した工業化の可用性は、複数のエンドユース業界における包装樹脂の需要増加に貢献しています。

中国包装樹脂市場洞察

中国は、プラスチック樹脂の生産および処理能力の優位性によって支持され、2024年にアジア太平洋包装樹脂市場で最大のシェアを開催しました。 国の強力なコンシューマーベース、パッケージ食品や飲料業界を成長させ、電子商取引パッケージングのリーダーシップは重要な樹脂消費を促進します。 政府は、リサイクルインフラと持続可能なパッケージングの推進に重点を置き、長期的な成長見通しを高めます。

インド包装樹脂市場インサイト

インドは、アジア・パシフィック地域において最も急速に成長し、食品や飲料包装、FMCGの急速な拡大、ヘルスケアパッケージニーズの高まりから需要を増大させています。 国内樹脂生産を推進し、中級の消費量を増加させ、小売・電子商取引活動の推進に取り組みます。 持続可能な包装ソリューションへの政府の推進とリサイクルインフラへの投資の増加により、市場勢いをさらに強化。

ヨーロッパ包装樹脂市場インサイト

欧州包装樹脂市場は、厳しい環境規制、リサイクル可能な包装材の需要が高い順調に拡大し、循環型経済への取り組みに重点を置きます。 地域の成熟した食品および製薬業界は、高品質の、豊富なパッケージングソリューションの一貫した需要を促進します。 R&D投資をバイオ分解性およびバイオベースの樹脂代替品に取り込むことは、市場ダイナミクスをさらに形成しています。

ドイツ包装樹脂市場インサイト

ドイツのパッケージング樹脂市場は、先進的な製造拠点、持続可能なパッケージングイノベーションのリーダーシップ、および国の食品およびヘルスケア業界からの強い需要によって駆動されます。 重要な化学および包装会社の存在は、十分に確立されたリサイクルのインフラと結合しましたり、長期市場成長を支えます。 工業・消費者向けパッケージングにおける高性能樹脂の需要も、欧州の主要役割にも貢献しています。

U.K. 包装樹脂市場インサイト

米国の市場は、パッケージされた商品、持続可能なパッケージングを推進する政府の政策、および再生可能な樹脂の採用に対する強い消費者需要の恩恵を受けています。 シングルユースプラスチックを削減する取り組みは、高性能およびバイオベースの樹脂代替品の機会を創出しています。 ダイナミックな小売部門の存在、電子商取引の普及、そしてローカライズされた生産への成長の焦点は市場需要を強化します。

北米包装樹脂市場インサイト

北米は、2025年から2032年にかけて最も速いCAGRで成長し、パッケージ食品の消費量の増加、ヘルスケアパッケージングの需要の増加、およびオンライン小売出荷における成長によって推進されています。 先進的なパッケージング技術の急速な採用と相まって、持続可能でリサイクル可能な樹脂に重点を置き、地域拡大を推進しています。 さらなる市場採用を加速する支援規制と業界コラボレーション。

米国包装樹脂市場インサイト

米国は、2024年に北米市場で最大のシェアを獲得し、広範なパッケージ食品業界、ヘルスケアパッケージングのリーダーシップ、樹脂メーカーの強い存在によって支持されています。 国の堅牢なR&Dエコシステム、持続可能なパッケージングソリューションへの投資、およびeコマース部門の拡大は、主要な成長ドライバーです。 リサイクルおよび環境に優しい包装に重点を置いた規制が増加し、さらに、米国の優位性を地域に強化します。

包装樹脂市場シェア

包装の樹脂の企業は主にを含むよく確立された会社によって、導きます:

- 中国石油・化学株式会社(中国)

- エクソンモビル株式会社(米国)

- Lyondellbasell Industries Holdings B.V (オランダ)

- サビック(サウジアラビア)

- 石油中国株式会社(中国)

- ボレアリスAG(オーストリア)

- Braskem(ブラジル)

- ドー(米国)

- デュポン(アメリカ)

- Indorama Ventures Public Company Limited(タイ)

- MGケミカル(カナダ)

- アーケマ(フランス)

- BASF SE(ドイツ)

- BOROUGE(UAE)

- DAK Americas(アメリカ)

- ファーイースタンニューセンチュリー株式会社(台湾)

- INEOS(アメリカ)

- サンフェムグループ(中国)

- レジアンスインダストリーズ株式会社(インド)

包装樹脂市場の最新動向

- ドウは、2024年6月、ドイツのポリオレフィン系フィルムメーカーであるRKWグループと共同で、レボロップリサイクルプラスチック樹脂の2つの新グレードの樹脂を発売しました。 これらのグレードの1つには、100パーセントのポストコンシューマーリサイクル(PCR)プラスチックが含まれているため、持続可能なパッケージングソリューションの大きな進歩が見られます。 この開発は、高品質のリサイクル樹脂の可用性を拡大することにより、ラウンドエコノミーにおけるドーのリーダーシップを強化することが期待されます。 非食品接触包装での使用のために承認されることにより、イニシアチブはバージンプラスチックの信頼性を低下させ、また環境に優しい包装材料のための成長した企業そして規制要求を支えます

- 2022年8月、BASFは、日本塗料メーカーである日本塗料と提携し、乾燥混合乳製品向けの環境に優しい産業包装ソリューションを導入しました。 包装は従来の非再生可能な障壁を取り替える水ベースのアクリルの分散であるBASFのJoncrylの高性能の障壁(HPB)を利用します。 このコラボレーションは、リサイクル性でパフォーマンスをバランスよくする持続可能なパッケージングへの市場シフトを反映しています。 ソリューションは、樹脂の生産者が、産業分野におけるグリーンパッケージの代替品の上昇環境規制と消費者の需要を満たすために革新しているかを強調しています

- 2020年10月には、LyondellとSasolは、Sasolの低密度のポリエチレンプラント、エタンクラッカー、および関連インフラの半分を占めるLouisiana統合PolyEthylene JV LLCを形成する2億米ドルの合意に署名しました。 これにより、Lyondellの樹脂生産能力が大幅に拡大し、北米でのサプライチェーンの統合を強化しました。 取引は、グローバルパッケージ樹脂市場でのより強い競争相手として合弁を置き、スケール、より広い製品の可用性、およびポリエチレンベースのパッケージングソリューションの急成長要求に対応する能力の向上を実現しました

- 2020年9月、ExxonMobilは、高容積食品や飲料、産業、自動車包装用途向けの手頃な価格で持続可能なソリューションとして設計された、発泡Achieve Advanced Polypropyleneを導入しました。 このイノベーションは、環境負荷の低減で、軽量素材の需要が高まっています。 性能を損なうことなく、資源の効率性を向上させることで、開発は、次世代樹脂ソリューションの推進におけるExxonMobilの役割を強化し、費用対効果の高い持続可能なパッケージング技術に対する広範な業界動向をサポート

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。