世界の澱粉のコーティングの市場規模、共有および傾向の分析のレポート

Market Size in USD Billion

CAGR :

%

USD

237.71 Million

USD

597.03 Million

2024

2032

USD

237.71 Million

USD

597.03 Million

2024

2032

| 2025 –2032 | |

| USD 237.71 Million | |

| USD 597.03 Million | |

| % | |

|

グローバルスターチコーティング市場セグメンテーション、ソース(コーンスターチ、ポテトスターチ、スウィートポテトスターチ、カスサバスターチ、その他)、アプリケーション(フルーツや野菜、肉、鶏肉、魚、乳製品、栄養製品、ベーカリー、菓子など) - 業界動向と予測 2032

澱粉のコーティングの市場のサイズ

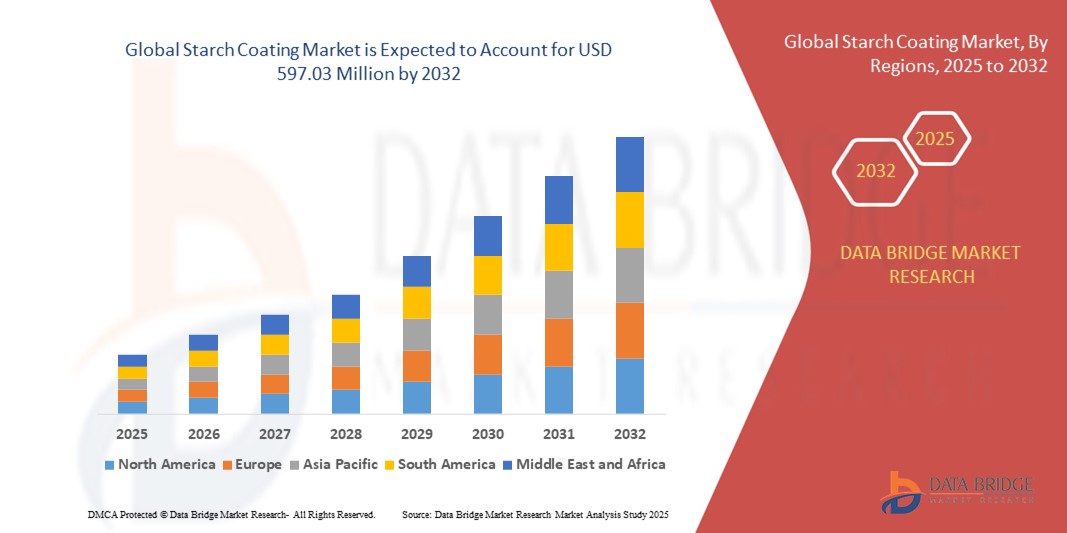

- 世界の澱粉のコーティングの市場のサイズはで評価されました2024年のUSD 237.71百万そして到達する予定米ドル 597.03 百万によって 2032, お問い合わせカリフォルニア 12.2%予報期間中

- 市場成長は包装、織物およびペーパー企業を渡る持続可能な、生物分解性のコーティング材料のための増加された要求によって主に燃料を供給されます

- 石油系および合成コーティングに関する規制規制規制の制限は、産業用途における澱粉ベースの代替の採用をさらに推進しています

スターチコーティング市場分析

- 澱粉のコーティングの市場は包装、織物およびペーパー企業の慣習的なコーティングへの持続可能な、生物分解性および環境に優しい代替品のための増加の要求によって運転される強い成長を、運転しますです

- 合成コーティングに関する厳格な規制に加えて、環境問題の上昇は、コスト効率の高い、再生可能エネルギーであり、幅広いアプリケーションと互換性のある澱粉ベースのソリューションを採用するメーカーをプッシュしています

- 北アメリカは、2024年に39.4%の最大の収益シェアを誇る澱粉コーティング市場を支配し、持続可能性の義務、生分解性パッケージングの強力な要求、および地域は、シングルユースプラスチックを減らすことに重点を置いています

- アジア太平洋地域は、世界最高成長率を目撃する見込み澱粉のコーティング市場、産業化の増加、使い捨ての収入の増加、および新興国全体の持続可能なパッケージの拡大によって主導

- トウモロコシの澱粉の区分は食糧および包装のさまざまなコーティングの塗布のための広い可用性、費用効果が大きい、適性が原因で2024年に最大の収益のシェアを握りました。 トウモロコシの澱粉ベースのコーティングはフィルム形成能力および生物分解性のために非常に好まれ、持続可能な代替のための成長した要求と一直線に並ぶ

レポートスコープとスターチコーティング市場セグメンテーション

| アトリビュート | スターチコーティングキーマーケットインサイト |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

ヨーロッパ

アジアパシフィック

中東・アフリカ

南米

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、データブリッジ市場調査によってキュレーションされた市場レポートには、インポートエクスポート分析、生産能力概要、生産消費分析、価格推移分析、気候変動シナリオ、サプライチェーン分析、バリューチェーン分析、バリューチェーン分析、原材料/消耗品概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークなどがあります。 |

スターチコーティング市場動向

生分解性および環境に優しい包装の解決の拡大の採用

- 世界的な澱粉のコーティングの市場は持続可能な、生物分解性の包装材料の上昇の好みによる要求の急増を経験します。 澱粉ベースのコーティングは石油ベースのプロダクトの代わりとしてますます利用され、企業の規制の承諾に会う間企業の環境の足跡を減らすのを助けます。 このシフトは、成長する循環経済の動きと整列

- 食品・飲料分野を中心に、環境に配慮した包装に関する消費者意識を高め、採用を推進しています。 小売業者やメーカーは、リサイクル性、堆肥性、パッケージング製品の全体的な持続可能性を向上させるために、澱粉コーティングを統合しています。 この傾向は、プラスチック削減を推進する政府の取り組みによってさらに支持される

- 澱粉ベースのコーティングの費用効果が大きいそして多様性はペーパー包装、織物および接着剤のような多様な適用のためにそれらに魅力的です。 メーカーは、合成化学物質の依存性を減らしながら、製品性能を向上させる、再生可能な原材料から恩恵を受ける

- たとえば、2023年に、複数のヨーロッパの紙メーカーは、シングルユースプラスチックを交換するために澱粉コーティング包装を導入しました。これにより、プラスチック廃棄物に関する厳格なEU指令の信頼性とコンプライアンスを強化しました。 これらの取り組みは廃棄物を減らすだけでなく、ブランドの評判と消費者の信頼を高めるだけでなく、

- 澱粉のコーティングは、持続可能な市場で急速に成長していますが、その成功は、加工技術の継続的な革新と成長する世界的な需要に応えるために生産のスケール化に依存しています。 企業はまた長期採用を保障するために費用効率のバランスの性能の特徴に焦点を合わせなければなりません

スターチコーティング市場ダイナミクス

ドライバー

石油ベースのコーティングへの持続可能な代替品の需要の増加

- 環境問題の上昇と規制圧力は、デンタル合成コーティングを澱粉ベースのソリューションなどの生分解性オプションに置き換えるために業界をプッシュしています。 再生可能エネルギーの起源と低炭素の足跡は、持続可能な包装および産業用途に適し、グローバルな気候行動目標と整合します

- 食品および飲料企業は、特に貯蔵寿命を延ばすために澱粉のコーティングを採用し、障壁の特性を高め、単一の使用のプラスチックの全体的な禁止に従うことです。 この移行は、製品の持続可能性を改善し、廃棄物の発生を削減し、毎日のパッケージングにおけるグリーン代替のための消費者の需要に対処することです。

- 研究のコラボレーションと資金調達のイニシアチブは、澱粉コーティング処方の技術的進歩を促進し、耐久性、耐水性、および業界全体の適用性を強化しています。 また、織物、医薬品、建材など、新商品カテゴリーの機会を広げています。

- たとえば、2022年に、複数の北米包装会社は、バイオベースの化学会社と提携し、高性能スターチコーティングを開発し、消費者パッケージングと産業用途の両方をターゲットとしています。 これらのコラボレーションは、商用利用のスケーラビリティを示す一方で、市場競争力を強化しました

- 持続可能な需要は採用を推進していますが、大規模なサプライチェーンの信頼性と競争力のある価格設定は、主流製造に澱粉コーティングの統合を加速するために不可欠です。 業界の利害関係者は、長期的な市場の信頼を築くために、メーカーや消費者を教育することにも注力しなければなりません

拘束/チャレンジ

合成物と比較して高い生産コストと性能制限

- 環境に優しい魅力にもかかわらず、澱粉ベースのコーティングは、多くの場合、より高い生産と加工コストを伴います。 スケールの経済性を達成することができないことは、より安価な石油ベースのコーティングとコストに敏感な市場への永続的な挑戦を競います

- 合成代替品と比較して、低水抵抗や機械的強度などの性能上の懸念、また、広範な使用を妨げる。 添加物か化学処置と無修正、澱粉のコーティングは産業包装および高い湿気の環境のようなデマンドが高い適用で不足するかもしれません

- サプライチェーンの一貫性、特に限られた澱粉の生産の地域では、原材料の継続的な可用性を制限することができます。 これは、輸入に関する信頼性を作成します。, メーカーを価格変動にさらします。, 全体的なコストを増加させる, グローバル市場で競争力に影響を与える

- たとえば、2023年、アジア・パシフィックのパッケージング会社では、原料コストが高いため、澱粉コーティングを採用し、湿った条件で製品性能に関する懸念を報告した。 これらの要因は、強力な規制のプッシュにもかかわらず、すぐに大規模な採用を開示しました

- 変更技術の革新は、パフォーマンスギャップに取り組む一方で、コストを削減し、一貫したスケーラビリティを確保することで、世界的な市場におけるスターチコーティングの完全成長の可能性を最大限に引き出します。 R&Dおよびローカライズされた生産能力に投資する会社は競争の端を得るために本当です

澱粉のコーティングの市場規模

市場は、ソースとアプリケーションに基づいてセグメント化されます。

- ソース

ソースに基づいて、スターチコーティング市場はコーンスターチ、ポテトスターチ、サツマイモスターチ、カサバスターチなどに分かれています。 トウモロコシの澱粉の区分は食糧および包装のさまざまなコーティングの塗布のための広い可用性、費用効果が大きい、適性が原因で2024年に最大の収益のシェアを握りました。 トウモロコシデンプンベースのコーティングは、フィルム成形能力と生分解性のために非常に有利であり、持続可能な代替のための成長した需要と整列しています。

カッサバの澱粉の区分は2025年から2032年までの最も速い成長率を目撃し、高いアミラーズの内容、強いフィルム形成の特性によって運転され、新興経済の採用を拡大すると期待されます。 Cassavaの澱粉のコーティングは障壁の特性および環境に優しい解決を改善する食糧保存および包装の適用で普及しています優先順位付けされます。

- 用途別

適用に基づいて、澱粉のコーティングの市場はフルーツおよび野菜、肉、家禽および魚、酪農場プロダクト、栄養製品、パン屋および製菓、等に分けられます。 2024年の最大の収益分配のために考慮した果物や野菜のセグメントは、棚の寿命を延ばし、鮮度を維持し、ポストハーベストの損失を減らす天然コーティングの消費者需要の増加によってサポートされています。 食品廃棄物の低減に注力し、グローバルに成長を続ける。

ベーカリーと菓子のセグメントは、2025年から2032年までの最も速い成長率を目撃する見込みで、食用コーティングの需要が増加し、質感を高め、水分保持を改善し、きれいなラベル製品開発をサポートします。 菓子の艶出しやベーカリー包装の澱粉コーティングの上昇使用は、このセグメントで強力な機会を作成することが期待されます。

スターチコーティング市場地域分析

- 北アメリカは、2024年に39.4%の最大の収益シェアを誇る澱粉コーティング市場を支配し、持続可能性の義務、生分解性パッケージングの強力な要求、および地域は、シングルユースプラスチックを減らすことに重点を置いています

- 食品および飲料の製造業者は棚の生命を改善し、環境に優しい標準に従うために澱粉ベースのコーティングを採用しますの最前線にあります

- 豊富な原材料の可用性、高度な加工技術、およびデンプンコーティング処方の革新をサポートする強力な研究開発能力の領域の利点。 また、グリーンとリサイクル可能なパッケージングの消費者の嗜好が高まっています。

米国スターチコーティング市場インサイト

米国のスターチコーティング市場は、2024年に北米で優勢なシェアを捕捉し、プラスチックの厳しい政府規制と、包装会社から再生可能エネルギー材料への強力なプッシュによって推進しました。 食品および農業業界は、澱粉ベースのコーティングに投資し、性能と持続可能性を向上させます。 バイオベースの化学会社とパッケージングプロデューサーのコラボレーションにより、さらには商品化を推進しています。

ヨーロッパの澱粉のコーティングの市場洞察

欧州の澱粉のコーティングの市場は生物分解性の代わりのための厳密な環境の規則そして消費者要求によって燃料を供給される2025から2032までの最も速い成長率を目撃するために期待されます。 欧州の企業は、食品包装、酪農、ベーカリー業界における澱粉ベースのコーティングを採用し、持続可能性目標と整合しています。 地域はまた、コーティングの耐久性とバリア特性の革新を促進する高度な研究エコシステムから恩恵を受けます。

ドイツ スターチ コーティング マーケット インサイト

ドイツの澱粉のコーティングの市場は強い包装および食品加工の企業によって支えられる2025から2032までの最も速い成長率を目撃するために期待されます。 国の規制枠組みは、循環経済を強調し、持続可能なイノベーションへのコミットメントは、澱粉コーティングの採用を加速しています。 新鮮な農産物および酪農場の包装の拡大の塗布は更に地域市場でのリーダーシップを補強します。

U.K.スターチコーティングマーケットインサイト

米国の澱粉のコーティングの市場は食糧および小売セクターを渡る生物分解性のコーティングの採用の増加によって運転される2025から2032までの最も速い成長率を目撃する期待されます。 消費者の意識を高め、プラスチック使用に関する政府の制限と組み合わせ、澱粉ベースのソリューションにシフトする業界を奨励しています。 U.K.のダイナミックな小売と電子商取引環境は、パッケージングイノベーションのさらなる燃料供給です。

アジア・パシフィック・スターチ・コーティング・マーケット・インサイト

アジア・パシフィック・スターチ・コーティング・マーケットは、2025年から2032年にかけて最も速い成長率を目撃し、急速な産業成長によって支えられ、プラスチック廃棄物を削減し、政府主導の取り組みを増加させました。 中国、日本、インドなどの国々は、食品加工業界や大型スターチ生産能力に強い採用されています。

中国スターチコーティング市場洞察

中国スターチコーティング市場は、その堅牢な国内製造拠点と環境に優しい材料のための政府のプッシュによって駆動され、2024年にアジアパシフィックで最大の収益シェアを獲得しました。 成長を続けるパッケージング部門と、持続可能な製品に対する強いミドルクラスの要求により、スターチコーティングは、消費者と産業用途の両方で急速に主流となっています。

ジャパンスターチコーティングマーケットインサイト

日本スターチコーティング市場は、2025年から2032年にかけて最も速い成長率を目撃する見込みで、国の先進食品包装部門の燃料供給と、持続可能な高品質の製品に対する高い消費者の嗜好が期待されています。 澱粉のコーティングを前向きに統合し、利便性の高い食品包装が高まっています。 さらに、日本のイノベーション主導のエコシステムでは、スターチコーティングのパフォーマンス、貯蔵寿命の延長、および環境効率性の継続的な改善をサポートしています。

スターチコーティング市場シェア

澱粉のコーティングの企業は主に下記のものを含んでいます:

- カルギル株式会社(米国)

- ADM(米国)

- Ingredion Incorporated(米国)

- テートとライル PLC (U.K.)

- Agrana Beteiligungs-AG(オーストリア)

- 穀物加工株式会社(米国)

- Roquette Frères(フランス)

- テレオスグループ(フランス)

- ロイヤル・コサン(オランダ)

- Altia 産業サービス(フィンランド)

- Everest Starch Pvt. Ltd.(インド)

- グリーンテックインダストリーズ株式会社(インド)

- バンコクスターチ工業株式会社(タイ)

- Sahyadri Starch and Industries Pvt. Ltd.(インド)

- ノバ・トランスファー株式会社(インド)

- サンスターバイオポリマー株式会社(インド)

- タンティア農薬プライベートリミテッド(インド)

- SPACスターチ製品株式会社(インド)

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。