自動車向けV2Xの世界市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

4.10 Billion

USD

81.90 Billion

2024

2032

USD

4.10 Billion

USD

81.90 Billion

2024

2032

| 2025 –2032 | |

| USD 4.10 Billion | |

| USD 81.90 Billion | |

| % | |

|

製品タイプ(ハードウェア、ソフトウェア、サービス)、通信タイプ(V2V/車車間、V2I/路車間、V2P/車車間歩行者、V2N/車車間ネットワーク、V2G/車車間グリッド、V2C/車車間クラウド、V2D/車車間デバイス)、車両タイプ(乗用車、小型商用車、大型商用車、その他)、アプリケーション(先進運転支援システム/ADAS、インテリジェント交通システム、緊急車両通知、フリート管理、駐車管理、その他)、テクノロジー(DSRC/専用近距離通信、C-V2X/セルラーV2X、ハイブリッドV2X、その他)、エンドユーザー(個人消費者、フリートオペレーター、政府機関、その他)、販売チャネル(直接販売、流通業者、オンライン小売業) – 2032年までの業界動向と予測

自動車向けV2X市場規模

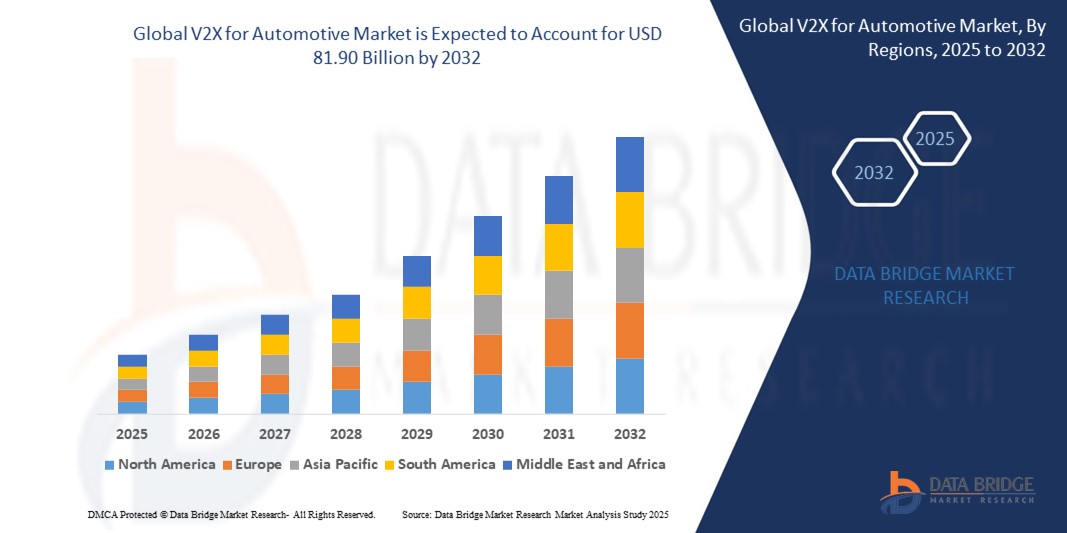

- 世界の自動車向けV2X市場規模は2024年に41億米ドルと評価され、予測期間中に45.4%のCAGRで成長し、2032年には819億米ドル に達すると予想されています。

- この成長は、コネクテッドカー技術の急速な普及、道路安全強化への需要の高まり、そして自動車、スマートシティ、物流分野における高度なV2Xアプリケーションをサポートする5Gネットワークの世界的な展開によって牽引されています。自動運転車開発の急増は、市場の拡大をさらに加速させています。

- 優れた接続性を実現する C-V2X への移行を含む V2X 技術の進歩、車両の安全性に関する政府の義務付け、電気自動車への V2X の統合などが相まって、特に自動車インフラが堅牢な地域で市場の成長が促進されています。

自動車市場向けV2X分析

- V2Xコンポーネントは、車両と他の車両、インフラ、歩行者、そしてネットワークとの通信を可能にする重要なシステムであり、安全性、交通効率、そして自動運転のためのリアルタイムデータ交換を促進します。車載ユニット、路側ユニット、ソフトウェアプラットフォームを含むこれらのコンポーネントは、ADAS、交通管理、フリート最適化といったアプリケーションに不可欠な要素です。

- 市場は世界的な自動車生産の増加に支えられており、2022年には8,540万台に達すると見込まれ、新車におけるV2Xシステムの需要が高まっています。自動運転車市場は2030年までに300万台に達すると予測されており、V2VおよびV2IアプリケーションにおけるV2Xの需要をさらに押し上げています。

- C-V2Xなどの先進技術の導入により、V2Xのパフォーマンスが向上し、自動車やスマートシティアプリケーションに低遅延通信を提供します。エネルギー管理にV2G通信を必要とする電気自動車の普及は、大きな成長の原動力となっています。

- アジア太平洋地域は、2024年には42.6%という圧倒的な収益シェアで世界のV2X市場をリードする見込みです。これは、堅固な自動車製造エコシステム、高い5G導入率、そして中国、日本、インドにおける政府支援によるものです。中国は、C-V2Xインフラへの大規模な投資によって市場を牽引しています。

- 北米は、規制支援、自律走行車の進歩、米国とカナダにおける大規模な研究開発投資に後押しされ、2025年から2032年にかけて46.2%のCAGRで成長することが予測されており、最も高い成長率が見込まれています。

- 通信タイプの中で、V2Vセグメントは、乗用車および商用車の衝突回避および安全アプリケーションで重要な役割を果たし、道路の安全性の向上を保証することから、2024年に42.01%の最大の市場シェアを占め、17億2,000万米ドルの価値がありました。

自動車市場のセグメンテーションにおけるレポートの範囲とV2X

|

属性 |

自動車向けV2Xの主要市場インサイト |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

自動車市場におけるV2Xの動向

「C-V2X、5G統合、自動運転の進歩」

- 世界のV2X市場の顕著なトレンドは、C-V2Xテクノロジーの広範な採用であり、2023年と2024年の新規導入の60%以上で、低遅延、高帯域幅の車両通信に5Gを活用し、より安全な自動運転が可能になります。

- 優れた接続性を提供する 5G ネットワークの統合が普及しつつあり、2024 年には新しい V2X システムの 35% 以上が、リアルタイム交通管理や V2I 通信などのアプリケーションに 5G を活用することになります。

- 半導体技術の進歩によって推進された V2X ハードウェアの小型化により、小型車両システムでの使用が拡大しており、新しいコンポーネントの 30% がスペースが限られた自動車アプリケーション向けに設計されています。

- ソフトウェア定義の V2X プラットフォームの台頭により、システムの柔軟性が向上し、複数のアプリケーションの動的な更新が可能になり、自動車およびスマート シティ分野での採用率が 20% 増加しています。

- 特に電気自動車向けのエネルギー効率の高い V2X 設計への注目が高まっており、これは持続可能性の目標と一致しており、2024 年の新しいシステムの 25% 以上が V2G アプリケーション向けの低消費電力を特徴としています。

- オンライン流通チャネルの成長により市場アクセスが変革しており、アフターマーケット ソリューションおよび開発者向けの電子商取引プラットフォームの牽引により、V2X コンポーネントのオンライン販売は年間 15% 増加しています。

自動車市場のダイナミクスにおけるV2X

ドライバ

「5Gの拡大、自動運転車の発展、そして安全義務」

- 2028 年までに 25 億件を超える加入が見込まれる 5G ネットワークの世界的な展開が主な推進力となり、コネクテッド ビークルにおける V2V や V2I などの V2X システムの需要が高まり、高速通信が確保されます。

- 2030 年までに世界販売台数が 300 万台に達すると見込まれる自動運転車の普及により、ADAS、V2X 通信、交通管理システムにおける V2X の需要が高まり、安全性と効率性が向上します。

- 電気自動車の普及により、2023年には世界販売台数が1,400万台に達すると予想されており、V2G通信におけるV2Xの需要が高まり、効率的なエネルギー管理とグリッド統合が可能になります。

- スマート シティへの投資が増加し、2023 年には世界支出が 1,890 億米ドルに達すると予想されており、インテリジェントな交通システム、駐車場管理、歩行者安全アプリケーションにおける V2X の需要が高まっています。

- Growing vehicle production, with over 85.4 million units in 2022, is fueling demand for V2X systems for seamless connectivity and safety in passenger cars and commercial vehicles.

- Government initiatives, such as China’s C-V2X mandates and the U.S. FCC’s spectrum allocation, are promoting V2X technology development, supporting market growth through regulatory and funding incentives.

Restraint/Challenge

“High Costs, Cybersecurity Risks, and Interoperability Issues”

- The high cost of advanced V2X systems, particularly those using C-V2X and 5G technologies, poses a challenge to adoption in cost-sensitive markets, limiting scalability for smaller manufacturers and regions.

- Cybersecurity risks, including hacking and data breaches, have impacted V2X adoption, leading to increased costs, with the V2X cybersecurity market growing at a CAGR of 19.1% to address threats.

- Technical complexities in designing and integrating V2X systems for autonomous vehicles require specialized expertise and advanced processes, increasing development costs and time-to-market.

- Stringent regulatory requirements, such as NHTSA standards in the U.S. and EU safety certifications, increase compliance costs and complexity for V2X manufacturers, particularly in automotive sectors.

- Interoperability issues between DSRC and C-V2X technologies pose a challenge to V2X adoption, particularly in regions with mixed infrastructure, requiring standardized protocols.

- The need for continuous innovation to meet evolving 5G and autonomous driving standards, coupled with rapid technological obsolescence, creates pressure on manufacturers to invest heavily in R&D, limiting profitability for smaller players.

V2X for Automotive Market Scope

The global RF components market is segmented on the basis of product type, component, application, technology, end-user, and sales channel.

- By Product Type

On the basis of product type, the market is segmented into hardware, software, and services. The hardware segment dominated the market with a commanding revenue share of 62.4% in 2024, valued at USD 2.56 billion, driven by its critical role in onboard and roadside units for V2X communication.

The software segment is anticipated to witness the fastest CAGR of 50.2% from 2025 to 2032, fueled by its use in IoT-enabled analytics and 5G platforms.

- By Communication Type

On the basis of communication type, the market is segmented into V2V, V2I, V2P, V2N, V2G, V2C, and V2D. The V2V segment held the largest market revenue share of 42.01% in 2024, valued at USD 1.72 billion, driven by its widespread use in collision avoidance and safety applications.

The V2I segment is expected to witness the fastest CAGR of 47.8% from 2025 to 2032, fueled by the rise of intelligent traffic systems.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into passenger cars, light commercial vehicles, heavy commercial vehicles, and others. The passenger cars segment accounted for the largest market revenue share of 68.5% in 2024, driven by high vehicle ownership and safety demands. The heavy commercial vehicles segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by logistics and fleet management needs.

- By Application

On the basis of application, the market is segmented into ADAS, intelligent traffic systems, emergency vehicle notifications, fleet management, parking management, and others. The ADAS segment accounted for the largest market revenue share of 38.2% in 2024, driven by its role in autonomous driving. The intelligent traffic systems segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by smart city initiatives.

- By Sales Channel

On the basis of sales channel, the market is segmented into direct sales, distributors, and online retail. The direct sales segment held the largest share of 65.6% in 2024, driven by B2B contracts with automakers and fleet operators. The online retail segment is expected to grow at the fastest CAGR from 2025 to 2032, fueled by e-commerce growth for aftermarket solutions.

- By Technology

On the basis of technology, the market is segmented into DSRC, C-V2X, Hybrid V2X, and others. The C-V2X segment held a significant share of 60.2% in 2024, driven by its 5G compatibility and reliability. This segment is expected to grow at the fastest CAGR from 2025 to 2032, fueled by its adoption in autonomous and connected vehicles.

- By End-User

On the basis of end-user, the market is segmented into individual consumers, fleet operators, government agencies, and others. The individual consumers segment dominated with a 55.3% revenue share in 2024, driven by high demand in passenger cars. The fleet operators segment is expected to grow at the fastest CAGR from 2025 to 2032, fueled by logistics and fleet management applications.

V2X for Automotive Market Regional Analysis

North America

North America is poised to grow at the fastest CAGR of approximately 46.2% from 2025 to 2032, driven by regulatory support, advancements in autonomous vehicles, and R&D investments. The U.S. accounted for 78.6% of the regional market in 2024, supported by FCC’s C-V2X spectrum allocation and strong demand for connected vehicle solutions.

U.S. V2X for Automotive Market Insight

The United States is expected to dominate the North American market, driven by its leadership in automotive innovation, autonomous vehicle development, and 5G infrastructure. The adoption of C-V2X in V2V and V2I applications, coupled with players like Qualcomm, supports market growth.

Europe V2X for Automotive Market Insight

Europe held a significant share in 2024, driven by its focus on safety regulations and smart city initiatives. Countries like Germany, the U.K., and France are key contributors, with growth fueled by the adoption of V2X in autonomous vehicles and intelligent traffic systems.

U.K. V2X for Automotive Market Insight

The United Kingdom is anticipated to grow steadily, driven by its strong automotive sector and investments in 5G and smart city technologies. Government initiatives like the U.K.’s Connected and Autonomous Vehicles program are boosting demand for V2X systems.

Germany V2X for Automotive Market Insight

Germany’s market is expected to grow at a considerable CAGR, fueled by its leadership in automotive manufacturing and smart mobility. The adoption of V2X in premium vehicles and smart highways, supported by players like Continental AG, drives market expansion.

Asia-Pacific V2X for Automotive Market Insight

Asia-Pacific dominated the global V2X market with a revenue share of 42.6% in 2024, driven by its robust automotive manufacturing ecosystem, high 5G adoption rates, and significant investments in smart city infrastructure. The passenger cars segment accounted for the largest vehicle type share of 65.4% in 2024, driven by high ownership. The heavy commercial vehicles segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by logistics growth.

Japan V2X for Automotive Market Insight

Japan’s market is expanding at a notable CAGR, fueled by its advanced automotive industry and focus on C-V2X and 5G applications. The presence of key players like DENSO and investments in autonomous vehicles drive market growth.

China V2X for Automotive Market Insight

China captured the largest revenue share of 48.2% within Asia-Pacific in 2024, driven by its leadership in C-V2X infrastructure, with over 500,000 5G-connected vehicles deployed by 2023, and a thriving electric vehicle market. Government initiatives like the Intelligent and Connected Vehicles Plan support V2X development through R&D funding and infrastructure incentives.

V2X for Automotive Market Share

- The V2X for Automotive industry is primarily led by well-established companies, including:

- Qualcomm Technologies, Inc. (U.S.)

- Continental AG (Germany)

- Robert Bosch GmbH (Germany)

- NXP Semiconductors N.V. (Netherlands)

- Autotalks Ltd. (Israel)

- Harman International (U.S.)

- Huawei Technologies Co., Ltd. (China)

- DENSO Corporation (Japan)

- Cohda Wireless (Australia)

- Infineon Technologies AG (Germany)

- Savari, Inc. (U.S.)

- Commsignia Ltd. (Hungary)

- Danlaw, Inc. (U.S.)

- Hitachi Solutions, Ltd. (Japan)

- Unex Technology Corp. (Taiwan)

- TDK Corporation (Japan)

Latest Developments in Global V2X for Automotive Market

- In March 2023, Qualcomm Technologies launched the Snapdragon Auto 5G Modem, a C-V2X solution with enhanced V2V capabilities, improving safety by 20% for autonomous vehicles, adopted by over 50 automakers globally.

- In January 2024, Continental AG introduced a new line of C-V2X onboard units for V2I communication, offering 25% improved latency, deployed in over 200 smart city projects in North America and Asia-Pacific.

- In April 2024, DENSO Corporation unveiled a compact V2X software platform for fleet management, reducing processing time by 30%, gaining traction in logistics markets in Japan and Europe.

- In February 2024, NXP Semiconductors launched an integrated V2X chipset for autonomous vehicles, enhancing signal reliability for V2P communication, with adoption by major automakers in Europe and the U.S.

- In June 2023, Huawei Technologies introduced a 5G-V2X module for smart traffic systems, supporting multi-band operations and reducing system complexity, adopted in over 100 smart city projects in China.

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。