世界の静脈血採取装置市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

6.84 Billion

USD

11.13 Billion

2024

2032

USD

6.84 Billion

USD

11.13 Billion

2024

2032

| 2025 –2032 | |

| USD 6.84 Billion | |

| USD 11.13 Billion | |

| % | |

|

世界の静脈血採取装置市場のセグメンテーション、タイプ別(採血管、針、真空採血システム、マイクロ流体システムなど)、材質別(プラスチック、ガラス、ステンレス鋼など)、用途別(静脈血ガスサンプリング、術中血液回収)、エンドユーザー別(病院・診療所、ポイントオブケア、献血センター、診断センターなど) - 2032年までの業界動向と予測

静脈血採取装置市場規模

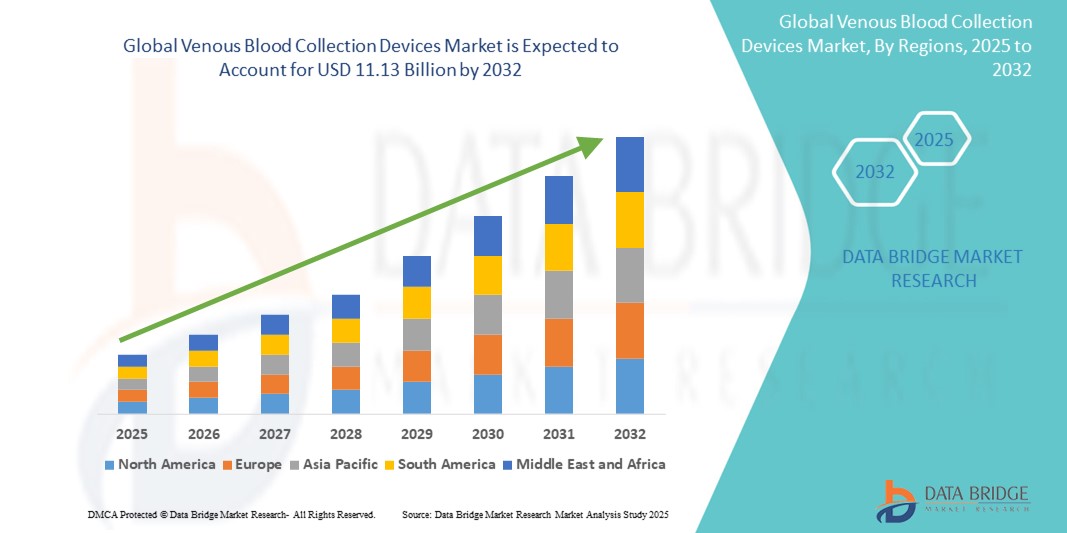

- 世界の静脈血採取装置市場規模は2024年に68億4000万米ドルと評価され、予測期間中に6.27%のCAGRで成長し、2032年には111億3000万米ドルに達すると予想されています。

- この成長は、診断検査の需要の増加、慢性疾患の増加、医療技術の進歩、早期の病気発見の重要性に対する意識の高まりなどの要因によって推進されています。

静脈血採取装置市場分析

- 静脈血採取器具は、臨床および診断現場において、様々な検査や治療のための血液サンプルを採取するために不可欠な器具です。針、注射器、採血管などのこれらの器具は、日常的な血液検査、輸血、慢性疾患の診断などの処置に不可欠です。

- 静脈採血装置の需要は、糖尿病、心血管疾患、癌などの慢性疾患の増加、および予防医療と早期疾患検出の重要性の高まりによって大きく推進されています。

- 北米は、高度な医療インフラ、高い医療費、そして診断検査需要の増加により、静脈採血装置市場において約75.5%の最大の市場シェアを占めると予想されています。また、この地域は、多数の医療施設と確立された償還制度の恩恵を受けています。

- アジア太平洋地域は、医療へのアクセスの向上、血液関連の診断検査に関する意識の高まり、中国やインドなどの国における医療インフラの拡大により、予測期間中に静脈採血装置市場で最も急速に成長する地域になると予測されています。

- プラスチックセグメントは、ガラス製の代替品と比較して製造・購入コストが比較的安価であることから、約88.5%の最大の市場シェアを占め、市場を席巻すると予想されています。また、プラスチック製の採血器具は破損しにくく、取り扱いや輸送中の怪我のリスクを軽減するため、より安全で耐久性に優れています。

レポートの範囲と静脈血採取装置市場のセグメンテーション

|

属性 |

静脈血採取装置に関する主要な市場洞察 |

|

対象セグメント |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

Data Bridge Market Research がまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、患者の疫学、パイプライン分析、価格分析、規制の枠組みも含まれています。 |

静脈血採取装置市場動向

「静脈血採取装置の技術的進歩」

- 静脈採血装置市場における顕著なトレンドの一つは、採血処置中の効率、安全性、患者の快適性を高めるための先進技術の統合である。

- これらの革新には、針刺し事故のリスクを最小限に抑える格納式針などの安全工学装置の開発や、血流制御を改善して患者の不快感を軽減し、全体的な採取プロセスを改善する装置の開発が含まれる。

- For instance, advancements in needle design and the introduction of smart blood collection tubes with digital tracking systems enable real-time data collection and improve sample integrity, streamlining the diagnostic process

- These advancements are transforming blood collection practices, improving patient safety and comfort, and driving the demand for next-generation blood collection devices with enhanced features

Venous Blood Collection Devices Market Dynamics

Driver

“Growing Demand Due to Increasing Chronic Diseases”

- The rising prevalence of chronic diseases such as diabetes, cardiovascular conditions, and obesity is significantly contributing to the increased demand for venous blood collection devices

- As the global population ages and lifestyle diseases continue to rise, there is an increasing need for regular diagnostic testing, which in turn drives the demand for efficient and reliable blood collection methods

- As more individuals undergo routine blood tests for monitoring and managing these chronic conditions, the need for advanced blood collection devices grows, ensuring better diagnosis, treatment, and monitoring

For instance,

- In 2022, the World Health Organization (WHO) reported that the global prevalence of diabetes is expected to rise significantly, with an estimated 700 million people living with the disease by 2045. This increase is directly contributing to the growing need for blood collection devices to monitor diabetes and other chronic diseases

- As a result of the rising incidence of chronic diseases, there is a significant increase in the demand for venous blood collection devices, driving market growth and the adoption of advanced technologies for improved healthcare outcomes

Opportunity

“Expanding Role of Digital Health and AI in Blood Collection”

- The integration of digital health technologies and artificial intelligence (AI) into venous blood collection systems presents a significant market opportunity by enhancing the accuracy, traceability, and efficiency of blood sample management

- AI-driven tools can assist in optimizing vein detection, reducing errors in collection, and improving the overall patient experience, particularly in difficult venous access cases or pediatric and elderly patients

- Smart blood collection devices with connectivity features can automatically log and track samples, integrate with electronic health records (EHRs), and support remote patient monitoring and data analytics

For instance,

- In 2023, multiple healthcare innovators began piloting AI-powered vein visualization and digital labeling systems to reduce human error and streamline pre-analytical processes, contributing to faster diagnostics and improved clinical outcomes

- The integration of AI and digital tools in venous blood collection can lead to increased operational efficiency, reduced sample misidentification, and enhanced diagnostic accuracy—creating new growth avenues in both hospital and home-care settings

Restraint/Challenge

“Risk of Contamination and Needlestick Injuries Hindering Market Growth”

- The risk of bloodborne pathogen transmission and needlestick injuries remains a significant challenge in the venous blood collection devices market, particularly impacting healthcare worker safety and regulatory compliance

- Despite advancements in safety-engineered devices, improper handling, lack of training, and insufficient use of protective technologies in certain regions increase the likelihood of accidents and infections

- These safety concerns can lead to higher liability for healthcare institutions, increased operational costs, and hesitance in adopting new blood collection systems without proven safety records

For instance,

- According to a 2023 report by the World Health Organization (WHO), over 2 million healthcare workers globally experience needlestick injuries annually, with a considerable percentage related to blood collection procedures. This has heightened the demand for strict safety protocols and advanced protective equipment

- Consequently, safety risks and infection concerns act as barriers to wider adoption, particularly in under-resourced healthcare systems, hindering the growth of the global venous blood collection devices market

Venous Blood Collection Devices Market Scope

The market is segmented on the basis of type, material, application, and end users

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Material |

|

|

By Application |

|

|

By End users |

|

In 2025, the plastic is projected to dominate the market with a largest share in material segment

The plastic segment is expected to dominate the venous blood collection devices market with the largest share of approximately 88.5%, due to the cost-effectiveness of plastic, which makes it more affordable to produce and purchase compared to glass alternatives. Plastic blood collection devices are also safer and more durable, as they are less prone to breakage, reducing the risk of injury during handling and transportation

The hospitals and clinics is expected to account for the largest share during the forecast period in end users segment

In 2025, the hospitals and clinics segment is expected to dominate the market with the largest market share of approximately 34.2%, due to the high volume of diagnostic tests and increased blood transfusion needs associated with surgeries and chronic conditions. Hospitals and clinics serve as primary centers for patient care, encompassing a wide range of services from routine check-ups to complex surgical procedures, thereby driving the demand for venous blood collection devices

Venous Blood Collection Devices Market Regional Analysis

“North America Holds the Largest Share in the Venous Blood Collection Devices Market”

- North America dominates the venous blood collection devices market with largest market share of approximately 75.5%, driven by a well-established healthcare infrastructure, high healthcare spending, and early adoption of advanced diagnostic technologies

- The U.S. holds a significant share of 28.7%, due to the increasing number of diagnostic tests, strong presence of key players such as Becton, Dickinson and Company, and favorable reimbursement policies that support the widespread use of modern blood collection devices

- The growing burden of chronic diseases such as diabetes, cardiovascular conditions, and cancer continues to drive demand for frequent blood tests, further boosting the market in the region

- The presence of regulatory bodies like the FDA that enforce safety and quality standards also encourages innovation and deployment of advanced, safety-engineered blood collection devices

“Asia-Pacific is Projected to Register the Highest CAGR in the Venous Blood Collection Devices Market”

- The Asia-Pacific region is expected to witness the highest growth rate in the venous blood collection devices market, fueled by the rapid expansion of healthcare infrastructure and increasing investments in healthcare modernization

- Countries such as China, India, and Japan are emerging as key contributors, supported by large patient populations, rising prevalence of lifestyle diseases, and growing demand for improved diagnostic services

- Japan leads in technology adoption, while China and India are seeing rising public and private sector investments to expand diagnostic capabilities, particularly in rural and underserved areas

- Government initiatives promoting early disease detection, coupled with improving access to healthcare services, are accelerating the adoption of venous blood collection devices across the region

Venous Blood Collection Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- BD (US)

- Haematonics (US)

- Terumo BCT (US)

- Fresenius Kabi AG (Germany)

- Grifols, S.A. (Spain)

- Nipro Medical Corporation (Japan)

- Greiner Holding (Austria)

- Quest Diagnostics (US)

- SARSTEDT AG & Co. (Germany)

- Macopharma (France)

- Smiths Medical (US)

- Cardinal Health (US)

- Retractable Technologies (US)

- Liuyang Sanli Medical Technology Development (China)

- F.L. Medical S.R.L (Italy)

- AB Medical (South Korea)

- APTCA SPA (Italy)

- Jiangsu Micsafe Medical Technology CO., LTD. (China)

- Disera Tibbi Malzeme Lojistik Sanayi Ve Ticaret A.Þ (トルコ)

- アジョシャ バイオ テクニク Pvt. Ltd.(インド)

- Preq Systems(インド)

- CMLバイオテック(インド)

- Lmb Technologie GmbH(ドイツ)

- ミトラ・インダストリーズ・プライベート・リミテッド(インド)

- ネオメディック・リミテッド(英国)

世界の静脈血採取装置市場の最新動向

- 2020年8月、Greiner Bio-OneとHaematologic Technologiesは、体外診断(IVD)および臨床診断機器開発者のニーズに合わせた採血管の包括的なエンドツーエンド開発およびカスタム製造サービスを提供する戦略的提携を発表しました。この提携により、採血管製造におけるイノベーションとカスタマイズが促進され、高まる精密診断の需要に対応します。市場がより専門的で高性能な診断ソリューションへと移行する中で、このような戦略的提携は製品品質の向上と市場投入までの時間の短縮に重要な役割を果たし、最終的には静脈採血機器の世界的な拡大と技術進歩を支えることになります。

- マグノリア・メディカルは2020年7月、特に血管系に障害のある患者における血液サンプル採取の精度を高めるために設計された一体型シリンジを備えたSteripath Gen2初期検体分流装置を発表しました。Steripath Gen2の発売は、より正確で患者中心の血液採取ソリューションへの市場の継続的な移行を反映しています。特に脆弱な患者層における診断の信頼性に対する需要が高まる中、このような技術的に高度なデバイスは臨床結果の向上に貢献し、世界的な市場成長を促進する上でのイノベーションの重要性を改めて認識させます。

- 2022年3月、Vivasure Medicalは、次世代デバイス「PerQseal+」を評価する米国における早期実現可能性調査に最初の患者が登録されたことを発表しました。PerQseal+は経皮経カテーテル大動脈弁置換術(TAVR)用に設計されており、血管閉鎖技術における大きな進歩を表しています。これらの進歩は、静脈アクセスと採血のより広範なエコシステムを補完し、安全性、使いやすさ、そして患者転帰の改善を重視しており、これらは静脈採血デバイス市場の成長を促進する要因でもあります。

- 2022年2月、ロシュのファウンデーション・メディシンは、血漿中の循環腫瘍DNA(ctDNA)を検出する検査の承認を取得しました。FDAの画期的医薬品指定を受けたこの検査は、がん治療後の患者における分子生物学的残存病変(MRD)の検出を目的としています。ctDNA検査の承認は、個別化医療における非侵襲性血液診断技術の重要性の高まりを浮き彫りにしています。この傾向は、信頼性の高い診断結果を得るために正確なサンプル採取と取り扱いが不可欠であるため、高度な採血機器の需要の高まりと一致しています。

- 2024年2月、Tasso社は、事前スクリーニングプログラムの効率向上を目的とした包括的なエンドツーエンドのサービスソリューション「Tasso Care for Prescreening」を発表しました。Tasso Care for Prescreeningの導入は、臨床試験における革新的な採血ソリューションの需要の高まりを浮き彫りにしています。遠隔採血機能を統合することで、Tassoは、よりアクセスしやすく効率的な医療サービスへの移行に貢献し、高度な静脈採血デバイスのニーズを高めています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。