グローバル・イン・ビトロ毒性検査市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

13.93 Billion

USD

35.25 Billion

2024

2032

USD

13.93 Billion

USD

35.25 Billion

2024

2032

| 2025 –2032 | |

| USD 13.93 Billion | |

| USD 35.25 Billion | |

| % | |

|

産品およびサービス(消費財、サービス、試金、装置およびソフトウェア)、毒性学の終点およびテスト(吸収、配分、代謝、及び排出)のテスト、Cytotoxicityのテスト、Genotoxicityのテスト、Dermal Toxicityのテスト、Organ Toxicityのテスト、Organ Toxicityのテスト、Organの皮の苛立ち、腐食、感度テスト、Cytotoxicityテスト、Cytotoxicityの他は、生物化学製品および試験を模倣します。

In-Vitroの毒性学のテストの市場のサイズ

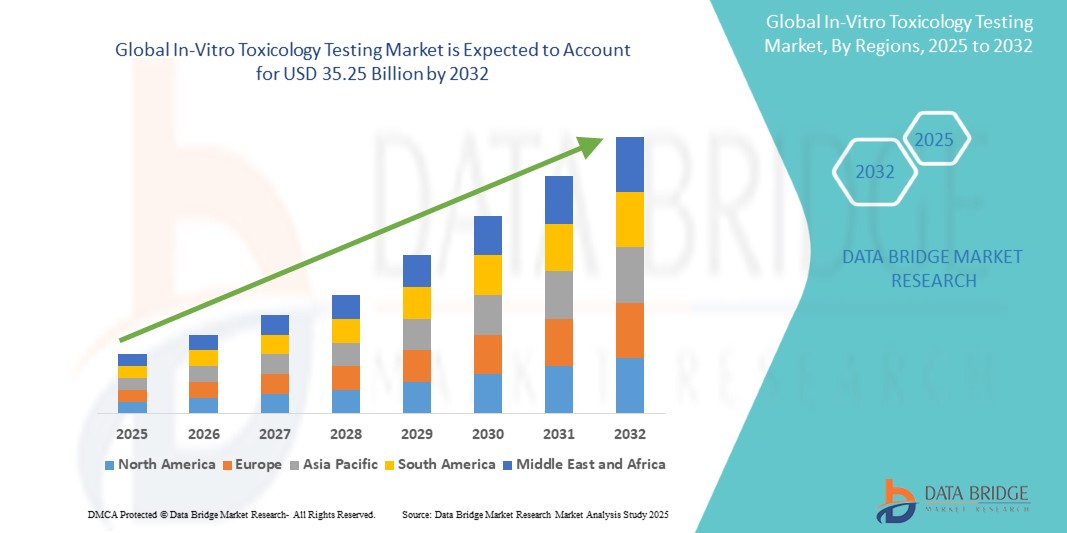

- 世界的なin-vitro毒性試験市場規模が評価されました2024年のUSD 13.93億そして到達する予定2032年までのUSD 35.25億, お問い合わせカリフォルニア 12.30%予報期間中

- 市場成長は高度の細胞ベースのおよび分子アッセイの技術の高められた採用によって主に、高スループットのスクリーニング、自動化された実験室システムおよび予測的な毒性学モデルの技術的な進歩と結合され、薬剤および化学テストの高められた効率そして正確さに導きます

- さらに、より安全で、より速く、そしてより費用効果が大きい代替手段のための上昇の要求は従来の動物テストにinvitroの毒性学テストを薬剤の開発、化学安全評価および規制の承諾の好まれた解決として確立しています。 これらの結合要因は、イン・ビトロ毒性検査ソリューションの採用を加速しています。これにより、業界の成長を大幅に向上させます。

In-Vitro毒性検査市場分析

- ビタミン毒性試験では、化学物質、医薬品、生物学的物質の安全性と毒性を評価するためのラボベースの方法を提供することで、規制の遵守と人間の安全を確保しながら、動物実験の信頼性を削減する能力により、医薬品、化粧品、化学工業にとってますますます重要になっています

- 子宮内毒性試験の需要は、主に厳格な政府規制によって駆動され、倫理的なテスト慣行の意識を高め、従来の動物実験方法に対するより速く、より正確で費用対効果の高い代替の必要性が増えています

- 北米は、2024年に最大48.3%の収益シェアを誇る、ベンチャー内毒性試験市場を支配し、先進医療インフラ、高R&D投資、および主要な業界プレーヤーの強力な存在を特徴とする

- アジア・パシフィックは、予測期間中のベンチャー毒性試験市場で最も急速に成長する地域であり、都市化の拡大、使い捨ての収入の増加、医薬品や化粧品産業の拡大、中国、日本、インドなどの国における近代的なラボ技術の導入が期待されています。

- 医薬品およびバイオ医薬品会社セグメントは、2024年に47.8%の最大の市場収益シェアで、インvitro毒性試験市場を支配し、安全性と有効性の検証を必要とする医薬品の発見と開発プログラムの大量に支持

レポートスコープとインビトロ毒性試験市場セグメンテーション

| アトリビュート | In-Vitro毒性学テストキー市場洞察 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

ヨーロッパ

アジアパシフィック

中東・アフリカ

南米

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

In-Vitro毒性検査市場動向

In-Vitro毒性試験における高度化と成長精度

- 世界的な毒性試験市場での重要な傾向は、より正確に人間の生理学的反応を再現する高度なin-vitroモデルの採用の増加です。 これらのモデルは、予測的信頼性を向上させ、動物実験に対する依存性を減らします。これは、世界的な規制および倫理的優先度である

- たとえば、3D細胞培養モデルと臓器オンチップ技術の開発により、研究者が臓器レベルの反応をシミュレートし、より正確な毒性データを提供します。 これらの方法は、医薬品安全評価および化学試験にますます使用されています

- 自動サンプル処理による高スループットスクリーニング(HTS)システムの統合により、精度と再現性を維持しながら、コンパウンドの迅速で大規模なテストが可能になります。 LonzaやCharles Riverなどの企業は、需要増加に対応するHTS機能を拡大しています

- 複数エンドポイントのシト毒性アッセイなど、アッセイ設計における技術革新は、有毒物質に対する細胞応答の包括的な評価を容易にします。 複数のシーケンシャル実験に関連した時間とコストを削減し、データ品質を向上させます。

- 規制遵守の高まりは、標準化されたin-vitroテストプロトコルを採用しています。 組織は、FDA、EMA、OECD ガイドラインに適合し、化学および医薬品安全評価のための検証されたin-vitroプラットフォームを活用しています。

- 初期段階の薬物の故障と悪影響の意識を高めることは、製薬会社が予期せぬin-vitro毒性試験に大きく投資することです。 事前試験の精度の向上により、意思決定を改善し、高価な後期臨床障害を削減

- In-Vitro毒性検査ソリューションの要求は、安全性、効率性、倫理的研究の実践のためのデュアルニーズによって駆動され、医薬品、バイオテクノロジー、および化学業界に急速に拡大しています。 業界関係者間の継続的な研究開発とコラボレーションがさらに加速する市場成長

In-Vitro毒性試験市場ダイナミクス

ドライバー

安全性と規制遵守の要件を高めるための必要性を成長させる

- 医薬品、化粧品、化学工業の厳しい規制と安全基準の高まりに伴い、高度なラボ技術の加速化と相まって、In-Vitro Toxicology Testingの高まる要求のための重要なドライバーです。

- 例えば、2022年、欧州連合のREACH規則(化学物質の登録、評価、認可、制限)および化粧品指令(EC 1223/2009)は、化粧品の動物試験に関する厳格な禁止を強化し、化学物質の厳しい安全評価要件を課しました。 その結果、企業は3Dヒト組織モデル、高コンテンツ画像処理、細胞ベースのアッセイなどの代替無菌毒性法を使用するよう支援しました。 この規制圧力は、InSphero (3D肝臓および心臓モデル)およびCyprotex(予知的in-vitro毒性学アッセイ)などのプロバイダからのソリューションに対する直接の需要増加

- 組織は、動物実験に対するより速く、より正確で倫理的な選択肢を求めるように、In-Vitro Toxicology Testingは、細胞ベースのアッセイ、高スループットスクリーニング、および予測的な毒性学モデルなどの高度な機能を提供し、従来の試験方法よりも優れた利点を提供します

- さらに、パーソナライズされた医薬品、予測分析、および規制遵守に対する成長の焦点は、現代の医薬品開発と安全評価ワークフローの不可欠なコンポーネントをIn-Vitro Toxicology Testingで、より信頼性が高く、人間関連の結果を可能にします

- 自動プラットフォームの利便性、AI主導のデータ分析と統合、人体組織の応答をシミュレートする能力は、医薬品研究開発および化粧品安全評価分野におけるIn-Vitro毒性検査の採用を推進する重要な要因です。 動物実験を削減し、ユーザーフレンドリーなプラットフォームの可用性を高める傾向は、市場成長に貢献します

拘束/チャレンジ

コスト・技術の複雑性に関する懸念

- 高度なIn-Vitro毒性検査システムの高コストと技術的な複雑性を取り巻く懸念は、市場浸透の拡大に大きな課題を提起します。 専門化された装置、訓練の条件および進行中の維持はより小さい実験室および新興市場のための障壁である場合もあります

- たとえば、高度なラボインフラと熟練した人材の必要性を強調するレポートでは、完全に自動化されたインビトロテストソリューションを採用する組織がいくつか行われています。

- 費用対効果の高いモジュラー プラットフォーム、ユーザー フレンドリー ソフトウェア インターフェイスおよび標準化された議定書によってこれらの課題に対処することはより広い採用を奨励するために重要です。 Lonza、Charles River Laboratories、Eurofinsなどの企業は、ワークフローの自動化、規制の遵守、および潜在的なユーザーを安心するために提供するスケーラビリティを強調しています。

- 加えて、価格が徐々に減少している間、高度なIn-Vitro毒性検査システムのための知覚プレミアムは、特に限られた予算で動作する研究施設のための広範な採用を強化することができます

- もう一つの重要な拘束は、アッセイプロトコルと検証要件におけるグローバル標準化の欠如です。 ラボ全体の試験結果の変動と普遍的な規制ベンチマークの欠如は、非vitroメソッドに依存する企業のための不確実性を作成します

- データの再現性と精度の課題は、特にモデルが複雑な人間の生物学的反応を完全に再現できないときに、in-vitroテストの自信を制限します。 これは、従来の動物実験方法から離れることから、結果および不測の組織の規制受諾を遅らせることができます

- 既存のラボのレガシーシステムとの統合に関する懸念も障壁として機能します。 多くの研究施設は、現在のインフラで近代的なin-vitroプラットフォームを揃えることが困難であることを発見し、コストと運用の非効率性を向上

In-Vitro毒性試験市場スコープ

市場はプロダクト及びサービス、毒性学の終点及びテスト、技術、方法、企業および配分チャネルに基づいて区分されます。

- 製品・サービス

製品およびサービスに基づいて、invitroの毒性試験市場は消耗品、サービス、試金、装置およびソフトウェアに分けられます。 消耗品セグメントは、2024年に39.6%の最大の市場収益シェアを占め、試薬、キット、および繰り返し試験手順で要求される文化媒体の一定の要求によって駆動しました。 消耗品は、単価であり、連続補充を必要とするため、毒性学研究に不可欠であり、サプライヤーの定期的な収益を確保します。 異なるアッセイと彼らの手頃な価格と互換性は、学術、研究、および産業研究所でそれらを好む選択肢を作る。 医薬品およびバイオ医薬品パイプラインを成長させることで、ADME、細胞毒性、遺伝子毒性試験の消耗品の使用量を増幅します。 この優位性は、著しく消耗品に依存するin-vitroアッセイの規制の受諾を高めることでさらに支持されます。

サービスセグメントは、2025年から2032年までの12.8%の最速のCAGRを目撃し、費用対効果の高い試験ソリューションを求める製薬および化粧品企業間のアウトソーシングトレンドによって燃料を供給する見込みです。 サービスプロバイダは、社内チームへの負担を軽減する専門的専門知識、高度なラボインフラストラクチャ、および迅速な納期を提供します。 また、CRO(Contract Research Organization)は、エンドツーエンドの前処理サービスの一環として、毒性試験をグローバルに展開しています。 安全試験の複雑性を高め、厳しいグローバル規制と組み合わせることで、アウトソーシングの企業が増えています。 このシフトは、予測期間中にサービスセグメントの急速な成長を著しくサポートします。

- 毒性学エンドポイントとテスト

毒性学の終点及びテストに基づいて、invitroの毒性学のテストの市場はADME (吸収、配分、Metabolismおよび排泄物)のテスト、cytotoxicityのテスト、genotoxicityのテスト、皮膚毒性のテスト、Ocularの毒性テスト、有機性毒性テスト、皮の苛立ち、腐食及び感度テスト、光毒性テストおよび他の毒性試験に分けられます。 ADMEテストセグメントは、2024年に31.4%の最大の市場収益シェアを占めています。これは、臨床試験の前に薬理学的および薬物候補の評価において重要な役割を果たしています。 医薬品およびバイオ医薬品会社がADMEアッセイに大きく依存し、段階的な故障を最小限に抑え、安全性と有効性を保証します。 薬物検出プロジェクトの増加に伴い、ADMEテストは初期段階研究パイプラインの不可欠な部分を残しています。 広範囲にわたる採用は、規制機関が非異常な試験方法を奨励することによってもサポートされています。 精密医学および個人化された療法のための増加された要求はさらにADMEのテストの重要性を高めます。

細胞毒性試験セグメントは、2025年から2032年までの13.5%の最速のCAGRを目撃し、細胞損傷効果の潜在的な化学化合物、医薬品、化粧品成分をスクリーニングすることに重要な役割を担っています。 Cytotoxicity アッセイは非常に費用効果が大きい、速い結果を提供して、それらを高スループットのテスト環境のために必要としました。 複数の地域で化粧品の動物実験に関する禁止は、シト毒性アッセイの信頼性と倫理的代替手段として加速しました。 また、食品・環境分野における化学物質暴露に関する懸念が高まっています。 セルベースのモデルおよびアッセイ感度における高度化により、予測期間におけるこのセグメントの採用をさらに加速します。

- テクノロジー

テクノロジーをベースに、細胞培養技術、高スループット技術、分子イメージング、オミクス技術にインvitro毒性試験市場を分けています。 細胞培養技術セグメントは、2024年に最大36.7%の市場収益シェアを占め、最も有望な毒性学研究の基盤として機能しています。 細胞培養システムは、研究者が人間の生物学的条件を複製し、薬物の有効性、毒性、行動のメカニズムに正確な洞察を提供することを可能にします。 それらは人間生理学を模倣する能力のためにADME、cytotoxicityおよび器官の毒性テストのために広く採用されます。 このセグメントの優位性は、より予測的で信頼性の高いデータを提供する3D細胞培養と臓器オンチップモデルの継続的な進歩によってさらにサポートされています。 また、医薬品およびバイオ医薬品会社は、医薬品開発コストとタイムラインを最小限に抑えるために、細胞培養ベースのアッセイに大きく投資し、さらにセグメントの市場位置を強化します。

医薬品、化粧品、化学工業の化合物の迅速で大規模なスクリーニングの必要性によって駆動され、2025から2032までの最速のCAGRを目撃する高スループット技術セグメントが期待されます。 これらの技術は、数千の化合物の同時テストを可能にし、安全性評価に関連する時間とコストを大幅に削減します。 自動化機能、強化された精度、AI主導の分析との互換性により、高スループットスクリーニングがますます支持されます。 さらに、規制機関は、データ生成を加速しながら動物実験の要件を減らすため、採用をサポートしています。 薬の発見および化学テストのR & Dの活動の上昇は区分の急速な成長のtrajectoryを強く支えます。

- 方法によって

方法に基づいて、in-vitro毒性試験市場は、細胞アッセイ、生化学アッセイ、ex-vivoモデル、およびsilicoモデルに分けられます。 セルラーアッセイセグメントは、2024年に42.1%の最大の市場収益シェアを占め、生物学的環境を再現し、有毒な経路に価値ある洞察を提供する能力を支持しています。 細胞アッセイは、医薬品、化粧品、食品業界において、細胞毒性、遺伝子毒性、臓器毒性試験に幅広く使用されています。 それらの採用は、非異常な試験方法の要求によって強く駆動され、グローバル規制フレームワークと整列します。 また、生細胞イメージングおよび3D培養システムの進歩により、細胞アッセイの信頼性と予測精度が向上します。 これらの要因は、細胞アッセイを細胞内毒性学研究の礎石として集合的に確立します。

2025年から2032年にかけて最も速いCAGRを目撃するシリコモデルセグメントは、計算生物学、機械学習、予測毒性学の進歩によって推進される。 サイリコモデルでは、研究者は、既存の生物学的および化学的データを使用して有毒な効果をシミュレートし、予測し、物理的実験の必要性を減らすことができます。 コスト効率とスピードは、初期段階の薬物スクリーニングとリスク評価のための魅力的な選択肢となります。 また、シリコモデルでは、毒性試験の支援ツールとして規制を受けており、さらなる導入を推進しています。 予測期間中にAIアルゴリズムと大きな毒性データベースとの統合が大幅に増加すると予想されます。

- 業界別

業界では、インvitro毒性試験市場は、医薬品およびバイオ医薬品会社、診断、食品、化学物質、化粧品および家庭用製品に分けられます。 医薬品およびバイオ医薬品会社セグメントは、2024年に47.8%の最大の市場収益シェアを占め、安全性と有効性の検証を必要とする医薬品の発見と開発プログラムの高容量でサポートしました。 これらの会社は、後期の臨床障害のリスクを最小限に抑え、厳格な規制要件を遵守するために、in-vitro毒性試験に大きく依存します。 3Dセルモデルや高スループットアッセイなど、先進的なインビトロ法の採用は、R&Dの意思決定とコストダウンを高速化できるため、このセグメントでは特に高くなっています。 革新的な医薬品とバイオロジックの世界的なパイプラインは、このセグメントのリーダーシップポジションを強化します。

化粧品および家庭用製品セグメントは、2025年から2032年までの最も速いCAGRを目撃し、化粧品の動物検査の世界的な禁止によって推進され、残酷フリー製品に対する消費者需要が高まります。 化粧品会社は、皮膚刺激、皮膚毒性、および安全と倫理基準を満たす光毒性アッセイなどのビタミンモデルを急速に採用しています。 また、製品安全に関する消費者の意識を高めることは、高度な毒性試験方法に投資するメーカーを説得しています。 予測性の高い皮膚や楕円モデルの可用性は、この業界での急速な採用をサポートしています。 この規制および消費者主導のプッシュは、予測期間中に最も急速に成長しているセクターとして、化粧品および家庭用製品セグメントを置きます。

- 流通チャネル

分布チャネルに基づいて、in-vitro毒性試験市場は、直接入札、小売販売などに分けられます。 直接入札セグメントは、主に病院、研究機関、製薬会社によるバルク調達のために、2024年に51.3%の最大の市場収益分配を支配しました。 直接入札者は、コスト優位性を提供し、サプライチェーンの信頼性を確保し、サプライヤーとエンドユーザー間の長期契約を確立します。 政府や大規模な医療機関も、透明性と品質保証を維持するための直接入札を好む。 このチャネルの優位性は、大規模な研究と臨床設定における消耗品、アッセイ、サービスの需要の増加によって強化されます。

小売販売部門は、2025年から2032年までの11.6%の最速のCAGRを目撃すると予想され、オンラインプラットフォーム、電子商取引チャネル、およびサードパーティのディストリビューターの増加による燃料を供給しました。 小売販売は、調達の柔軟性を必要とする小規模な研究所、学術機関、化粧品会社にとって特に魅力的です。 注文、競争力のある価格設定、および幅広い製品へのアクセスの容易さは、小売販売は、エンドユーザーが利便性を求めるために好ましい選択肢になります。 また、調達プロセスの高度化と専門ディストリビューターの拡大は、このセグメントの成長に著しく貢献します。

In-Vitro毒性検査市場地域分析

- 北米は、2024年に最大48.3%の収益シェアを誇るベンチャー内毒性試験市場を占め、先進医療インフラ、高R&Dの支出、および主要なグローバルプレーヤーの強力な存在によって特徴付けられました

- 地域は、特に医薬品や化粧品の動物実験の減少を奨励する厳格な規則から恩恵を受けており、信頼性の高いin-vitroモデルの燃料需要があります

- AI主導の予測毒性および自動化された高スループットシステムの採用は成長を加速していますが、医薬品の発見、化学的安全性、化粧品製品試験におけるインビトロ法の増大応用は、北米の世界的な市場における主要な位置を統合しています

U.S. In-Vitro毒性試験市場洞察

米国内毒性試験市場は、医薬品研究および先進的なバイオテクノロジーのリーダーシップを反映し、北米で2024年に最大の収益シェアを獲得しました。 市場の拡大は、医薬品開発パイプラインの代替テスト技術の急速なアップテークによって駆動され、企業はますます安全性と規制遵守を優先します。 臓器オンチップ技術、細胞ベースのアッセイ、計算モデルの革新と相まって、研究室で動物の使用を減らすための強力な政府支援は、さらなる採用を加速しています。 また、化粧品、化学物質、環境研究における予測毒性学の需要が高まっています。この分野における米国の役割を強化しています。

ヨーロッパ In-Vitro毒性学試験市場 洞察

欧州のinvitro毒性試験市場は、厳格なEU指令によって支持され、化粧品の動物検査を禁止し、複数の業界にわたってより安全な代替を促進するために着実に成長するように計画されています。 地域が誇る医薬品分野、持続可能な試験方法の需要増加、バイオテクノロジー研究の継続的な投資は、主要な成長コントリビューターです。 また、学術機関と民間企業が連携し、細胞培養技術と分子イメージングのイノベーションを推進しています。 ドイツ、フランス、イギリスなどの国々は、この変革の最前線に立ち向かう国で、イン・ビトロ・テスト・モデルの採用に強いエコシステムを作り出しています。

U.K. In-Vitro毒性試験市場インサイト

英国内毒性試験市場は、国の強力な研究インフラ、繁栄するバイオテクノロジー業界、および動物実験の減少と整合された規制ポリシーによって駆動される注目すべきCAGRで成長することを期待しています。 医薬品、薬品、化粧品業界における研究開発活動は、インビトロモデルの採用に大きなチャンスを創出しています。 また、AIベースの毒性学予測における米国の進展は、支援型イノベーションエコシステムと組み合わせ、複数の業界における採用を加速しています。

ドイツ In-Vitro毒性試験市場 洞察

ドイツ・イン・ビトロ毒性試験市場は、先進の医薬品・化学産業に支えられたかなりのペースで拡大し、技術革新に重点を置いています。 環境に優しい、持続可能な試験方法の普及は、臓器オンチップシステム、3D細胞培養、および分子イメージングソリューションの採用を推進しています。 ドイツは、バイオテクノロジーとラボオートメーションのグローバルリーダーとしての地位を強化し、高度な毒性試験を提供する能力を強化し、より安全で効率的な試験フレームワークの長期ビジョンと整列します。

Asia Pacific In-Vitro毒性試験市場 Insight

アジア・パシフィック・イン・ビトロ毒性試験市場は、イン・ビトロ毒性試験市場で最も急速に成長する地域であることが予想され、予測期間中に最高のCAGRで拡大する予定です。 成長は、中国、日本、インドのより安全で費用対効果の高い試験ソリューションの医薬品および化粧品産業の急速な発展、ヘルスケア投資の増加および増加の需要によって運転されます。 近代的なラボ技術を推進する動物実験や政府の取り組みに対する代替案の普及は、さらなる成長を促進しています。 また、APACのポジションと製造ハブと相まって、より広いコンシューマーベースへのアクセスを拡大し、市場浸透を加速しています。

ジャパン・イン・ビトロ毒性試験市場 Insight

強固な医療・バイオテクノロジー分野から、日本における毒性試験市場が勢いを増大し、技術革新の高度化に貢献しています。 より速く、より安全な薬剤の開発のための要求によって運転される予測的な毒性学モデルの国の採用は市場成長に著しく貢献します。 また、日本の高齢化人口は、安全性の高い医薬品の高度化の必要性を生み出しています。これにより、正確で先進的な検査ソリューションに対する信頼性が高まります。 実験におけるAI搭載ツールと分子イメージングの統合により、日本がこの市場で増加するリーダーとして位置づけています。

中国In-Vitro毒性検査市場洞察

2024年にアジア・パシフィックで最大の収益シェアを占める中国内毒性試験市場は、拡大する製薬産業、動物実験の代替策を促進する政府政策によって支えられています。 急速な都市化、使い捨て収入の増加、および強い国内製造能力は、業界横断のinvitroテストの採用を加速しています。 中国は、バイオテクノロジー投資とラボ機器の生産のための重要なハブとしての役割は、その位置を強化し、その地域の急成長に重要な貢献します。

In-Vitro毒性試験市場シェア

invitro の毒性学のテストの企業は主に下記のものを含む十分に確立された会社によって、導きます:

- サーモフィッシャーサイエンス株式会社(米国)

- Labcorp(アメリカ)

- メルク・カーガ(ドイツ)

- チャールズ・リバー研究所(米国)

- ロンザ(スイス)

- バイオロード研究所(米国)

- 株式会社カタレント(米国)

- SGS Société Générale de Surveillance SA(スイス)

- QIAGEN(オランダ)

- インターテックグループ plc. (イギリス)

- ユーロフィンズ科学(フランス)

- 株式会社プロメガ(米国)

- アラーゲンライフサイエンス株式会社(インド)

- Cyprotex Plc. (イギリス)

- 上海メディシロン株式会社(中国)

- クリエイティブ・バイオラボ(米国)

- BioIVT(米国)

- AATバイオクエスト株式会社(米国)

- Gentronix(イギリス)

- IONTOX(アメリカ)

- InSphero (スイス)

- MB研究機関(米国)

- クリエイティブ・バイオアレイ(米国)

- 優先セルシステム(米国)

グローバル・イン・ビトロ毒性試験市場の最新動向

- 2025年4月、米国食品医薬品局は、特定の医薬品クラスの必須動物検査の要件を段階的にフェーズアウトすることを意図し、臓器オンチップやAIベースの予測毒性システムなどの高度な新アプローチ方法論に対する規制強化のサポートをマークしました。

- 2025年5月、AstuteAnalyticaは、176の新しい非動物性毒性プロトコルが1月2022日から12月2023日までの市場検証パイプラインに参入したと報告しました。臓器チップやマイクロ流体システムなどの非vitro方法論のイノベーションを拡大する明確な兆候

- Quris-AIは2023年9月、Merck KGaA(Darmstadt)とのコラボレーションを拡張し、薬物毒性を予測できるAIを搭載したモデルを拡張し、計算された予測ツールとの統合を強化

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。