北米血管造影装置市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

3.75 Billion

USD

10.50 Billion

2024

2032

USD

3.75 Billion

USD

10.50 Billion

2024

2032

| 2025 –2032 | |

| USD 3.75 Billion | |

| USD 10.50 Billion | |

| % | |

|

北米血管造影装置市場のセグメンテーション、製品別(血管造影システム、血管造影剤、血管閉鎖装置、血管造影用バルーン、血管造影用カテーテル、血管造影用ガイドワイヤー、血管造影用アクセサリ)、技術別(X線血管造影、CT血管造影、MRA血管造影、その他)、手順別(冠動脈造影、血管内血管造影、神経血管造影、腫瘍血管造影、その他)、適応症別(冠動脈疾患、弁膜症、先天性心疾患、うっ血性心不全、その他)、用途別(診断、治療)、エンドユーザー別(病院、診療所、診断・画像診断センター、研究機関) - 2032年までの業界動向と予測

血管造影装置市場規模

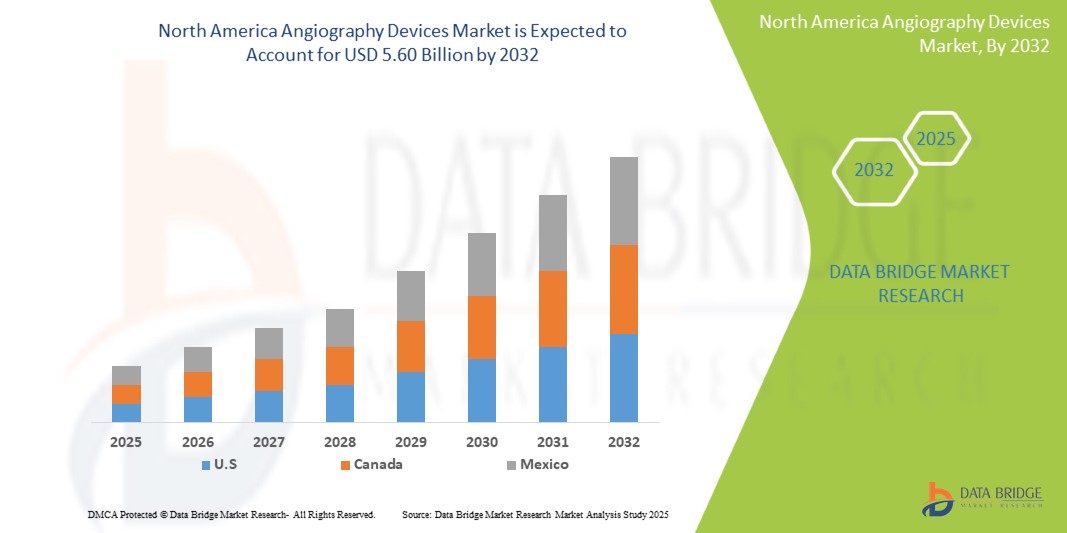

- 北米の血管造影装置市場規模は2024年に37億5000万米ドルと評価され、予測期間中に5.8%のCAGRで成長し、2032年には56億米ドル に達すると予想されています。

- 市場の成長は、心血管疾患の発生率の上昇、高齢化の進行、血管疾患の早期かつ正確な診断に対する需要の高まりによって主に促進されています。

- さらに、3Dイメージング機能や高度なナビゲーションシステムといった血管造影システムの技術進歩が市場拡大を牽引しています。これらの要因が相まって、様々な医療用途における血管造影装置の導入が加速し、業界の成長を大きく後押ししています。

血管造影装置市場分析

- 血管造影装置市場は、血管や臓器を画像化するために用いられる幅広い医療用画像機器と消耗品を網羅しています。これには、血管造影システム(Cアーム、カテーテルラボ)、カテーテル、ガイドワイヤ、造影剤インジェクター、その他の付属品が含まれます。これらの装置は、様々な心血管疾患、神経疾患、末梢血管疾患の診断と治療に不可欠です。この市場は、心血管疾患の有病率の増加、画像診断技術の進歩、そして低侵襲手術への需要の高まりによって牽引されています。

- 血管造影装置の需要の高まりは、主に、心臓病学および放射線学における介入処置の増加、低侵襲技術の採用の増加、血管疾患の早期診断と介入の利点に対する認識の高まりによって促進されています。

- 北米の血管造影装置市場は、米国が2025年に87.45%という最大の収益シェアを占め、市場をリードしています。これは、確立された医療インフラ、低侵襲手術の導入率の高さ、心血管疾患の有病率の上昇、そしてインターベンション心臓学への積極的な投資によるものです。大手メーカーの存在と多額の研究開発費も、市場の成長を支えています。

- 米国は、高齢化人口の増加、有利な保険償還政策、そしてフラットパネルディテクタや3D回転血管造影システムといった先端技術を搭載した機器への需要増加により、北米の血管造影装置市場において最も急速に成長する国になると予想されています。また、主要企業間の継続的な臨床的進歩と戦略的提携も市場拡大に貢献しています。

- 血管造影カテーテルは、血管の状態を正確に画像化し、冠動脈および末梢血管造影手順に幅広く適用でき、また、低侵襲性と臨床的有効性により診断および介入心臓学の両方で採用が増えているため、2025年には38.2%の市場シェアを獲得し、北米の血管造影装置市場を支配すると予想されています。

レポートの範囲と血管造影装置市場のセグメンテーション

|

属性 |

血管造影装置の主要な市場洞察 |

|

対象セグメント |

|

|

対象国 |

北米

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

血管造影装置市場の動向

「3Dイメージングと高度なナビゲーションシステムの統合」

- 先進的な画像技術とナビゲーション技術の統合:北米の血管造影装置市場における重要なトレンドは、先進的な画像技術とナビゲーション技術の統合が進んでいることです。この融合により、複雑なインターベンション手技における診断精度、手技効率、そして患者の安全性が大幅に向上しています。

- 例えば、最新の血管造影システムは、2D透視と3D画像撮影機能(CTのような画像撮影や回転血管造影など)を組み合わせることで、包括的な解剖学的画像を提供します。これにより、臨床医は複雑な血管構造を視覚化し、より正確な処置計画を立てることができます。

- ロボット支援血管造影や電磁トラッキングなどの高度なナビゲーションシステムの開発により、カテーテルの操作性が向上し、患者と医師の双方の放射線被ばくが軽減されています。さらに、患者データ管理システム(PACS/HIS)とのシームレスな統合により、ワークフローが効率化され、リアルタイムの意思決定が容易になります。

- よりインテリジェントで統合性に優れ、高精度な血管造影システムへのトレンドは、インターベンション心臓学および放射線医学の診療を根本的に変革しつつあります。そのため、企業は自動化とリアルタイムガイダンス機能を強化した次世代の血管造影プラットフォームの開発に多額の研究開発投資を行っています。

- 臨床医が患者の転帰の最適化と処置の効率を優先するにつれ、高度な画像診断とナビゲーションのシームレスな統合を提供する血管造影装置の需要が病院や専門の心臓血管センター全体で急速に高まっています。

血管造影装置市場の動向

ドライバ

「心血管疾患の発生率の上昇」

- 北米における心血管疾患 (CVD) の発生率の増加は、血管造影装置市場の成長の主な原動力となっています。

- 例えば、米国心臓協会によると、CVDは依然として米国における罹患率と死亡率の主要な原因であり、多くの診断および介入処置を必要としています。血管造影は、冠動脈疾患、末梢動脈疾患、その他の血管疾患の診断、および介入治療の指針策定において重要な役割を果たしています。

- The aging population, coupled with lifestyle factors such as obesity, diabetes, and hypertension, contributes to the rising burden of CVDs, thereby increasing the demand for angiography procedures.

- Furthermore, advancements in interventional techniques and the growing preference for minimally invasive procedures are fueling the adoption of advanced angiography devices.

- Increasing awareness about early diagnosis and treatment of vascular diseases is also driving market growth

Restraint/Challenge

“High Cost of Angiography Systems and Reimbursement Issues”

- The high cost of advanced angiography systems and the complexities associated with reimbursement pose a significant challenge to broader market adoption, particularly for smaller healthcare facilities and those with budget constraints.

- For instance, a state-of-the-art angiography system can cost several million dollars, representing a substantial capital investment for hospitals and diagnostic centers. This high initial cost can limit access to advanced angiography technologies, especially in underserved areas.

- The need for specialized infrastructure, such as dedicated cath labs, and highly trained personnel (interventional cardiologists, radiologists, and technologists) further adds to the operational burden.

- Additionally, variations in reimbursement policies across different healthcare systems and insurance providers can create financial uncertainty, potentially limiting the volume of procedures performed.

- Addressing these challenges requires efforts to reduce manufacturing costs, develop more cost-effective solutions, and advocate for favorable reimbursement policies to ensure wider accessibility of angiography procedures

Angiography Devices Market Scope

The market is segmented on the basis product, technology, procedure, indication, application and end user.

- By Product

On the basis of product, the North America angiography devices market is segmented into angiography systems, angiography contrast media, vascular closure devices, angiography balloons, angiography catheters, angiography guidewires and angiography accessories. The Angiography Catheters segment dominates the largest market revenue share of 38.2% in 2025, driven by high demand for advanced imaging platforms that provide precise visualization of vascular structures. These systems are integral in both diagnostic and interventional procedures and are continually evolving with innovations such as flat-panel detectors, rotational angiography, and hybrid OR integration.

The vascular closure devices segment is anticipated to witness the fastest growth rate of 9.6% from 2025 to 2032, due to the growing shift toward minimally invasive procedures. These devices enable rapid hemostasis and early ambulation, reducing patient discomfort and improving hospital workflow efficiency.

- By technology

On the basis of technology, the market is segmented into X-ray angiography, CT angiography, and MRA angiography and other. X-ray angiography is further segmented into image Intensifiers and flat-panel detectors. X-ray angiography segment held the largest market revenue share in 2025, due to its established use in coronary and peripheral vascular assessments, and its compatibility with catheter-based procedures. It remains the backbone of interventional cardiology owing to its real-time visualization capabilities and precision.

The CT angiography segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by advancements in multi-slice CT systems, increased preference for non-invasive imaging, and broader applications in detecting aortic aneurysms, pulmonary embolism, and peripheral artery disease.

- By Procedure

On the basis of procedure, the market segmented into coronary angiography, endovascular angiography, neurovascular angiography, onco-angiography and other. The Coronary angiography segment accounted for the largest market revenue share in 2025, owing to the high burden of coronary artery disease in the region and the growing demand for timely diagnosis and treatment. This procedure remains a critical diagnostic step before interventions such as angioplasty or stenting.

The Neurovascular angiography segment is projected to witness the fastest CAGR from 2025 to 2032, attributed to increasing incidence of stroke and cerebrovascular anomalies, along with expanding access to specialized neurological centers and interventional neuroradiology capabilities.

- By Indication

On the basis of Indication, the market segmented into coronary artery disease, valvular heart disease, congenital heart disease, congestive heart failure, and other indications. The Coronary artery disease segment accounted for the largest market revenue share in 2025, driven by lifestyle-related risk factors, an aging population, and widespread screening initiatives across North America.

The Congestive heart failure segment is projected to witness the fastest CAGR from 2025 to 2032, as angiography increasingly supports both diagnosis and interventional planning in patients with complex heart failure conditions, particularly in the elderly.

- By Application

On the basis of Application, the market segmented into diagnostics and therapeutics. The diagnostics segment accounted for the largest market revenue share in 2025, as angiography remains the cornerstone for identifying vascular obstructions, aneurysms, and structural anomalies. Its high sensitivity and ability to guide subsequent interventions support its leading role.

The therapeutics segment is projected to witness the fastest CAGR from 2025 to 2032, reflecting the rise in image-guided procedures such as angioplasty, stenting, and embolization therapies—supported by hybrid ORs and improved device compatibility.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, diagnostic and imaging centers and research institutes. The Hospitals and clinics segment holds the largest market revenue share in 2025, due to their capacity to perform complex angiographic procedures, access to high-end imaging systems, and multidisciplinary expertise. These facilities are central to both routine diagnostics and emergency cardiovascular care.

The Diagnostic and imaging centers segment is expected to witness the fastest growth from 2025 to 2032, driven by the increasing preference for outpatient diagnostics, shorter patient wait times, and cost-effectiveness. Technological advancements enabling high-quality non-invasive angiographic imaging also support this trend.

Angiography Devices Market Regional Analysis

- U.S. dominates the Angiography Devices market with the largest revenue share of 87.45% in 2024, primarily driven by a high burden of cardiovascular diseases, robust diagnostic infrastructure, and strong reimbursement frameworks.

- The widespread adoption of advanced imaging systems—including digital flat-panel detectors and AI-assisted angiography platforms—continues to enhance procedural accuracy and clinical outcomes.

- Government initiatives such as the Million Hearts program and the American Heart Association’s screening campaigns have led to greater uptake of preventive and diagnostic cardiovascular imaging, boosting demand for angiography procedures.

- The presence of major industry players like GE HealthCare, Siemens Healthineers, and Philips, along with aggressive investments in R&D and product innovation, strengthens the U.S. market.

- Additionally, the shift toward minimally invasive and outpatient-based interventions—supported by ambulatory surgical centers—is accelerating the use of catheter-based angiography devices across multiple clinical settings.

Canada Angiography Devices Market Insight

The Canada Angiography Devices market is projected to expand at a substantial CAGR throughout the forecast period, driven by the growing incidence of breast cancer and increased investments in public health diagnostics. Canada’s national health strategy emphasizes early cancer detection, and provinces have rolled out organized breast screening programs (such as Ontario Breast Screening Program), boosting demand for advanced biopsy systems. Additionally, rising awareness about the benefits of minimally invasive biopsies over surgical alternatives and the growing availability of MRI-guided and stereotactic-guided techniques in diagnostic centers are contributing to market expansion. Strong regulatory standards set by Health Canada and increasing collaborations with U.S.-based device companies further support the growth of innovative biopsy technologies in the Canadian market

Mexico Angiography Devices Market Insight

メキシコの血管造影装置市場は、医療インフラの継続的な改善と、心血管の健康に対する政府の重点化を背景に、予測期間中に顕著なCAGRで成長すると予想されています。過体重、肥満、糖尿病の予防と管理に関する国家戦略などの取り組みにより、血管造影を含む心血管診断の需要が高まっています。高度な介入システムへのアクセスは依然として都市部の三次医療センターに限られていますが、官民連携や国際協力により、二次医療や地方医療の現場への技術浸透が徐々に進んでいます。早期心血管リスクスクリーニングへの意識の高まりと、心臓専門医および放射線科医向けの研修プログラムの改善が相まって、カテーテルを用いた血管造影とCT/MR血管造影の両方の普及を後押ししています。

血管造影装置の市場シェア

血管造影装置業界は、主に次のような定評ある企業によって牽引されています。

- シーメンス・ヘルシニアーズ(ドイツ)

- GEヘルスケア(米国)

- フィリップス ヘルスケア(オランダ)

- キヤノンメディカルシステムズ株式会社(日本)

- ボストン・サイエンティフィック・コーポレーション(米国)

- メドトロニック(アイルランド)

- アボットラボラトリーズ(米国)

- テルモ株式会社(日本)

- コーディス(米国)

- 島津製作所(日本)

北米血管造影装置市場の最新動向

- シーメンス・ヘルスシナーズは2024年3月、高度な3DイメージングとAIを活用した画像処理を特徴とする次世代血管造影システムを発表しました。このシステムは、複雑な血管構造の可視化を向上させ、特に神経血管および末梢血管手術における診断精度と介入計画を向上させます。また、高度な治療環境において、リアルタイムの意思決定と最適化されたワークフローによって医師をサポートします。

- GEヘルスケアは2024年2月、優れた操縦性と困難な解剖学的部位へのアクセスを実現する革新的な血管造影カテーテルを発表しました。末梢血管介入におけるナビゲーションを改善するように設計されたこのカテーテルは、臨床精度の向上、手技時間の短縮、そして複雑な血管病変の治療成績の向上に貢献します。

- フィリップス ヘルスケアは2024年1月、ロボット手術のリーディングカンパニーと戦略的提携を締結し、ロボット支援血管造影システムを共同開発することを発表しました。この提携は、フィリップスの画像診断技術とロボットの高精度な低侵襲血管介入技術を融合させ、神経血管手術におけるカテーテルナビゲーションの精度と制御性を向上させることを目指しています。

- ボストン・サイエンティフィックは2023年12月、潤滑性の向上と先端の柔軟性を高めた最新のガイドワイヤーのFDA承認を取得しました。複雑な冠動脈構造をナビゲートできるよう設計されたこのデバイスは、高リスク冠動脈インターベンションにおける手技の成功率向上と合併症率の低減を目指しています。

- メドトロニックは2023年11月、次世代の投与量管理と患者情報システムとの完全な統合を実現する新しい造影剤インジェクターシステムを発表しました。ワークフローの効率性を高め、造影剤の使用を最適化するように設計されたこのシステムは、診断およびインターベンション血管造影における画像の安全性と精度の向上をサポートします。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。