北米コンピューティングのトモグラフィデバイス市場規模、株式とトレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

1.67 Billion

USD

2.60 Billion

2024

2032

USD

1.67 Billion

USD

2.60 Billion

2024

2032

| 2025 –2032 | |

| USD 1.67 Billion | |

| USD 2.60 Billion | |

| % | |

|

北アメリカによってコンピューティングされたトモグラフィ装置市場セグメンテーション、製品の種類(低シリズCTスキャナ(64シズ))、アプリケーション(心臓血管アプリケーション、腹部および骨盤アプリケーション、肺血管拡張アプリケーション、脊椎アプリケーション、脳応用、筋骨格応用および腫瘍学)、エンドユーザー(病院および診断センター)および2032の予測

北アメリカの計算されたトモグラフィー装置市場のサイズ

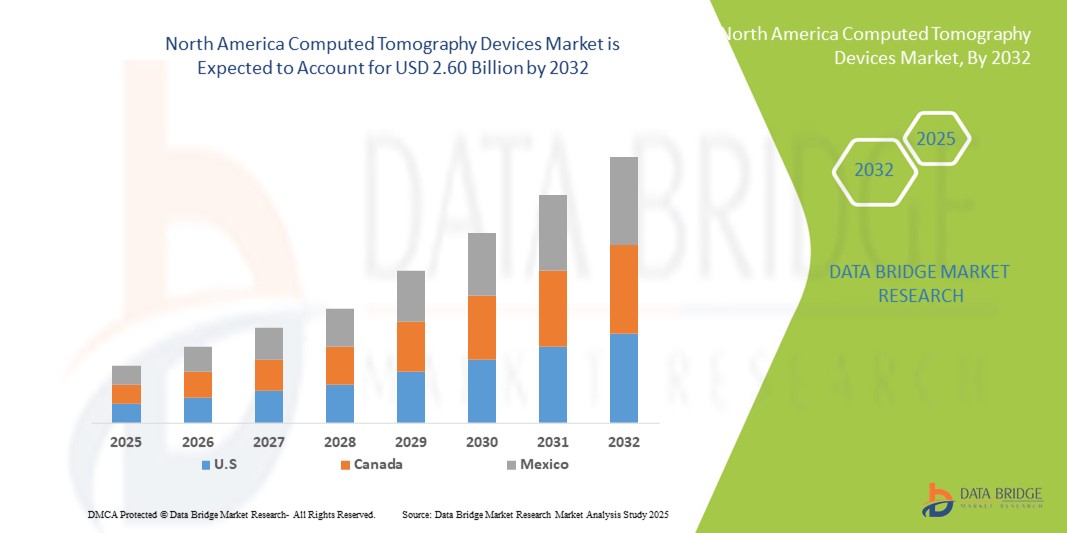

- 北米は、トーモグラフィデバイス市場規模が評価されました2024年のUSD 1.67億そして到達する予定2032年までのUSD 2.60億, お問い合わせ5.65%のCAGR予報期間中

- 市場成長は、主に慢性疾患および生活習慣病の増大、早期および正確な診断イメージングの需要増加、およびAI統合および低線量放射線技術を含むCTイメージングシステムにおける継続的な技術進歩によって駆動されます。

- また、医療インフラの拡充、有利な払い戻し方針の拡充、病院、診断センター、専門医院における先進的なイメージングソリューションの採用拡大は、地域における重要な診断ツールとしてCT装置を配置しています。 これらの組み合わせ要因は、CTシステムの展開を加速し、市場の成長を著しく推進しています

北米コンピューティングのトモグラフィデバイス市場分析

- 計算されたtomography (CT)装置は精密な診断および処置の計画のための断面イメージ投射を提供し、高度のイメージ投射ソフトウェアおよびAI-assisted用具との高度のイメージ投射の正確さ、速度および統合による病院および診断中心の現代医学の診断のますます本質的な部品です

- CT機器の需要は、主に慢性疾患の増大可能性、早期および正確な診断の必要性の増加、および低線量イメージング、AI対応再構築、マルチスライスCTシステムなどの技術進歩によって駆動されます。

- 米国は、2024年に最大88.5%の収益シェアを誇る北米複合トーモグラフィデバイス市場を支配し、先進医療インフラ、高ヘルスケア支出、および主要なイメージング機器メーカーの強力な存在によって特徴付けられ、高スライスCTスキャナー(>64スライス)の実質的な採用と、病院および診断センターで、心臓血管、神経管および腫瘍学的画像アプリケーションにおけるイノベーションによってサポートされている

- カナダは、医療インフラへの投資の増加、患者の意識の上昇、先進的な診断ソリューションの需要の増加による予測期間中、北米CTデバイス市場で最速成長国であることが期待されています

- 高スライスCTスキャナ(>64スライス)は、2024年に44.8%の市場シェアを持つ北アメリカCTデバイス市場を支配し、優れたイメージング速度、高分解能、心血管、および病院および診断センター設定の腫瘍学的アプリケーションを横断した汎用性を主導

報告書 スコープと北アメリカ コンピューティング トーソグラフィ デバイス 市場セグメント

| アトリビュート | 北アメリカの計算されたトモグラフィー装置の主要な市場洞察 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

北米コンピューティングトモグラフィデバイス市場動向

AI-Assisted ImagingとマルチスライスCTシステムの開発

- 北アメリカCTデバイス市場における有意で加速傾向は、成長している統合です人工知能(AI) 多枚のCTシステムを搭載し、画像の正確さ、ワークフローの効率および診断機能を高めて下さい

- 例えば、Siemens HealthineersのAI-Rad Companionのインスタンスは、CTスキャンを自動的に分析し、予備診断インサイトを提供し、意思決定における放射線学者を支援します

- CTデバイスにおけるAI統合により、自動画像再構築、異常検知、および予測分析忍耐強い結果のため、スキャンの信頼性を改善し、人間の間違いを減らすため

- マルチスライスCTシステムとAIプラットフォームのシームレスな組み合わせにより、イメージングプロトコルの集中管理、データ共有、および病院ネットワーク間でのレポート作成、より合理化された放射線学ワークフローを実現

- よりインテリジェントで高解像、自動CTシステムに対するこの傾向は、放射線学の期待を再構築しています。 その結果、GEヘルスケアなどの企業は、先進的な再建アルゴリズムと自動心臓と神経管のイメージング解析でAI対応CTスキャナーを開発しています。

- ヘルスケアプロバイダがますますます効率、正確さを優先し、広範囲の診断機能性を先立たせるように、AI-assistedのイメージングおよび高スライス機能を提供するCT装置のための要求は病院および診断中心を渡る急速に成長しています

北米コンピューティング・トモグラフィー・デバイス・マーケット・ダイナミクス

ドライバー

慢性疾患および診断イメージの必要性を育てることによる上昇の要求

- 慢性疾患、がん、心血管疾患の増加の予防、早期および正確な診断の必要性と組み合わせて、CTデバイスに対する高まる要求のための主要なドライバーです

- たとえば、キヤノンメディカルシステムズでは、心臓病の早期発見をサポートするために、強化された心臓イメージング機能を備えた高度な高スライスCTスキャナーを導入しています。

- 医療従事者は、患者の成果と診断精度を向上させることを目指し、CTデバイスは、高解像イメージング、迅速なスキャン時間、AI支援分析などの機能を提供し、従来のイメージングモーダルティに対する説得力のあるアップグレードを提供します。

- さらに、米国とカナダのヘルスケアインフラの拡充と患者意識の高まりは、病院やイメージングセンターにおける診断ワークフローの集積コンポーネントであるCTシステムを構築しています。

- より高速な画像処理、スキャン時間の削減、および一回のセッションで多臓器イメージングを実行する能力の利便性は、臨床設定におけるCTデバイス採用を推進する重要な要因です。 外来イメージングの拡大と高度な診断センターへの傾向は、市場成長に貢献します

拘束/チャレンジ

高い機器コストと規制コンプライアンスハルール

- 高度CTシステムの比較的高い獲得および維持費、特に高いスプライスの走査器は、特により小さい診断中心のためのより広い市場浸透への重要な挑戦をポーズします

- たとえば、Medtronic のインスタンスは、臨床需要にもかかわらず、マルチスライスCTシステムの調達を遅らせる小規模なクリニックでの予算制限を強調しています。

- 資金調達オプション、サービス契約、スケーラブルなソリューションを通じて、これらのコストの懸念に対処することは、市場リーチを拡大するために不可欠です。 また、放射線曝露のための規制遵守と厳格な安全基準は、メーカーやヘルスケアプロバイダのための現在のハードル

- 定期的なソフトウェアの更新の必要性, 放射線学のスタッフの訓練, FDA と健康カナダのガイドラインに従うことは、採用率を遅くすることができます, 特に新しく発売された高スライスの CT システムのため

- コストとコンプライアンスの課題は、革新的な資金調達、モジュラーシステム設計、およびAI主導の自動化によって徐々に管理されていますが、運用上の負担を軽減し、高資本支出と規制の複雑さは、小規模または予算の制約のある医療施設における広範な採用を強化することができます

北アメリカの計算されたトモグラフィー装置市場規模

製品の種類、アプリケーション、エンドユーザーに基づいて市場をセグメント化します。

- 製品タイプ別

製品の種類に基づいて、北米CT機器市場は、低スライスCTスキャナ(<64スライス)、中スライスCTスキャナ(64スライス)、高スライスCTスキャナ(>64スライス)に分けられます。 高いスライスCTスキャナセグメントは、2024年に44.8%の最大の収益シェアで市場を支配し、優れたイメージング速度、高解像能力、および複数の臨床アプリケーション間で汎用性によって駆動しました。 病院および診断センターは、これらのシステムがスキャン時間を削減し、診断の正確さを改善するために、心血管、神経管および腫瘍学のイメージ投射のような複雑なプロシージャのためのhigh-sliceの走査器を好みます。 要求はAIの統合によって更に燃料を供給され、画像の再構成、異常な検出およびワークフローの効率を高めます。 大型病院や専門診断センターでは、高精度・速度が患者の転帰に不可欠であるCTスキャナーを採用しています。 セグメントの優位性は、低線量イメージングや高度なソフトウェアツールなど、継続的な技術革新によってもサポートされています。

低スライスCTスキャナ(<64シズ)セグメントは、2025年から2032年までの最も速い成長率を目撃し、小規模な病院、外来診療所、診断センターの需要が高まっています。 これらの走査器は十分な診断性能の規則的なイメージ投射、バランスをとる有用性のための費用効果が大きい解決を提供します。 低スライスシステムは、予算に配慮した施設や適度な患者の容積を持つ地域に特に適しています。高スライスシステムの高い資本支出なしで重要なイメージング機能を提供します。 より小さなフットプリントとメンテナンスの要件を下げることで、成長する採用にも貢献します。 また、メーカーは、よりコンパクトでユーザーフレンドリーなモデルを開発し、簡単にインストールと操作を可能にし、市場浸透をさらに拡大しています。 このセグメントの成長を加速するために、分散型および外来診断イメージングに対する成長傾向が期待されます。

- 用途別

適用に基づいて、市場は心血管の塗布、腹部および骨盤の塗布、肺の血管の塗布、脊柱適用、musculoskeletal適用および腫瘍学に分けられます。 Oncologyアプリケーションセグメントは、2024年に市場を支配し、がんの増殖と正確な腫瘍検出、ステージング、および治療計画のための重要な必要性による最大の収益分配を占めています。 高分解能およびマルチスライスCTスキャナーは、軟組織の正確なイメージング、生検手順の指導、および治療反応の監視のために腫瘍学で広く使用されています。 AI-assistedイメージングとの統合により、病変検出と体積分析が向上し、診断結果が向上します。 病院および専門にされた癌センターは総合的で、非侵襲的なイメージ投射の解決を提供するように腫瘍学の適用のためのCT装置を好みます。 早期がんの検出と定期的なスクリーニングプロトコルの意識を高めることで、需要も推進されます。

心血管系アプリケーションセグメントは、2025~2032年の間に最速の成長率を目撃する見込みで、心疾患の上昇と正確な心臓イメージングの要求によって燃料を供給しました。 マルチスライスCTスキャナは、冠動脈イメージング、カルシウムスコーリング、およびプレ手術計画のためにますます採用され、迅速で正確な評価を提供します。 心臓イメージングにおけるAIの統合は、アーティファクトを減らし、画像の品質を最適化し、複雑な心血管構造の自動化分析を可能にします。 病院と診断センターの双方の採用を成長させ、早期心臓血管疾患の検出の意識を高めるとともに、急速な市場拡大を促進することが期待されています。 また、このセグメントの成長に最小限の侵襲的および非patient心臓画像処理が貢献しています。

- エンドユーザーによる

エンド ユーザーに基づいて、北アメリカ CT 装置市場は病院および診断中心に分けられます。 病院の区分は高度のインフラ、大きい忍耐強い容積の可用性および多様な臨床適用を扱うことができる高切れ目および多目的CTシステムのための強い好みによる2024年に市場を支配しました。 病院は、定期的な診断、緊急ケア、腫瘍学、心血管検査、多用途で高性能なCT機器の運転要求のためのCTイメージングに依存しています。 主要なイメージング機器メーカーの存在と技術の専門知識の可用性は、さらに病院のCTデバイスの採用をサポートしています。

診断センターのセグメントは、2025から2032までの最速の成長率を目撃し、外来患者の診断、予防的な健康診断、および専門的なイメージングセンターの上昇傾向によって駆動する見込みです。 診断センターは、中型および低スライスCTスキャナーに投資し、費用対効果の高い高品質のイメージングサービスを提供します。 便利で、非病院ベースの診断サービスのための成長している忍耐強い好みおよびoutpatientイメージのための保険の適用範囲の拡大はこの区分の市場成長を更に加速します。 製造業者はまた、コンパクトで簡単なCTソリューションでこのセグメントをターゲットにしています。

北米コンピューティングのトモグラフィデバイス市場地域分析

- 米国は、2024年に88.5%の最大の収益シェアを持つ北アメリカのCTデバイス市場を支配しました。先進医療インフラ、高ヘルスケアの支出、および主要なイメージング機器メーカーの強力な存在によって特徴付けられ、高スライスCTスキャナー(>64スライス)の実質的な採用と病院および診断センターで、心臓血管、神経管および腫瘍学的アプリケーションにおけるイノベーションによってサポートされています。

- 地域におけるヘルスケアプロバイダは、高精度、速度、および高スライスおよびAI集積CTスキャナが提供するマルチアプリケーション機能を大切にし、正確な診断と患者の結果を改善します。

- この広範囲にわたる採用は、先進医療インフラ、高医療費、および主要なイメージング機器メーカーの存在によってさらに支持され、CT装置を病院や診断センターの重要なツールとして確立します。

U.S. Computed Tomography Device マーケットインサイト

米国のCTデバイス市場は、先進的な診断イメージングを必要とする慢性疾患、癌、心血管疾患の上昇の蔓延によって駆動され、北アメリカの2024で最大の収益シェアを撮影しました。 病院や診断センターは、イメージングの精度、速度、および患者の成果を改善するために、ハイスライムおよびAI統合CTスキャナーを優先しています。 複数のスライスCTシステムを採用し、AIによる再構築と自動解析と組み合わせ、市場成長を促進します。 また、先進医療インフラ、高医療費、および主要なイメージング機器メーカーの存在により、CTシステムの迅速な導入をサポートし、米国での利点があります。 外来イメージングセンターや予防健康診断の傾向は、市場拡大にも貢献しています。

カナダ・コンピューティング・トモグラフィー・デバイス・マーケット・インサイト

カナダCTデバイス市場は、予報期間中に相当するCAGRで成長すると予想され、ヘルスケアインフラへの投資の増加と早期疾患の検出の意識の高まりが期待されます。 カナダの病院および診断センターは心血管、腫瘍学および神経管のイメージ投射のための臨床要求を満たすために媒体およびハイ スライスCTの走査器を採用します。 医療の近代化を推進し、診断サービスへのアクセスを改善するための政府の取り組みは、CTデバイスのインストールの拡大を支援しています。 また、外来診断センターや予防ケアの焦点は、全国の採用を加速しています。 AIと先進的なイメージングソフトウェアの統合は、カナダの医療施設におけるCTシステムの実用性をさらに高めています。

メキシコのコンピューティング・トモグラフィー・デバイス・マーケット・インサイト

メキシコ CT デバイス市場は、予測期間中に注目すべき CAGR で成長することを期待しています。, 医療投資の増加と病院や専門センターでの診断イメージングの需要の増加によって駆動. コスト効果の高い低・中スライスCTスキャナの採用により、都市部や半都市部のトラクションが楽しめます。 早期疾病診断の意識を高め、医療アクセスを支援する政府プログラムと組み合わせ、CTシステムの展開を奨励しています。 メキシコの民間医療分野を拡大し、主要なイメージング機器メーカーとのパートナーシップを結び、市場成長に貢献しています。 また、腫瘍学、心臓血管、神経血管系アプリケーションにおける多用途イメージング機能の需要が高まり、現代のCTデバイスの採用をサポートしています。

北米コンピューティングのトモグラフィデバイス市場シェア

北アメリカの計算されたトモグラフィー装置工業は主に下記のものを含む確立された会社によって、導きます:

- GEヘルスケア(米国)

- Siemens Healthineers AG(ドイツ)

- Koninklijke Philips N.V.(オランダ)

- キャノンメディカルシステムズ株式会社(日本)

- ネロロジカ株式会社(米国)

- リョーイアメリカ(アメリカ)

- PrizMedイメージング(米国)

- ノーススターイメージング株式会社(米国)

- ユナイテッドイメージングヘルスケア株式会社(米国)

- Xoran Technologies, LLC.(米国)

- CurveBeam(アメリカ)

- ストライカー(アメリカ)

- 正確なメトロロジー(米国)

- ピナクルX線ソリューション(米国)

- 応用技術サービス株式会社(米国)

- Jesse Garant Metrology Center(カナダ)

- マイクロX(オーストラリア)

- サーモフィッシャーサイエンス株式会社(米国)

- PerkinElmer(アメリカ)

- ブルーカー(アメリカ)

北米計算トモグラフィデバイス市場における最近の発展は何ですか?

- 2025年5月、GE HealthCareは、新しいハイブリッドイメージングシステム用のFDA 510(k)クリアランスを受け取り、オーロラは、統合されたディープラーニングソフトウェアと共に、DLをクリアします。 この核医学のSPECT/CTの走査器は単一のphotonの放出の計算されたtomography (SPECT)を結合し、複雑なtomography (CT)の技術は臨床専門を渡るより精密なイメージ投射を渡すために鋭く、提供します

- Siemens Healthineersは2025年3月、Neotom Alphaのフォトンカウント計算式トーモグラフィ(CT)スキャナーがFDAのクリアランスを受けました。 この製品クラスには、Naeotom Alphaが含まれています。 Pro、第2のデュアルソースCTスキャナー、Neotom Alpha。 世界初のCT技術を搭載した世界初のシングルソーススキャナ

- 2024年12月、ユナイテッド・イメージング・ヘルスケアは、完全に統合されたZ検知器と0.3秒の高速回転速度を備えた160枚のスライスCTスキャナーを発表しました。 システムでは、低線量のイメージング機能で優れた診断を提供することを目指しています

- 2023年11月、キヤノンメディカルシステムズでは、Aquilion ONE / GENESIS Edition CTスキャナを導入。 このシステムは高度のAI高められた復興の技術、改善されたイメージの質および減らされた放射線線量を提供します特色にします

- 2021年11月、GEヘルスケアは、回転1回あたりの0.23秒の世界で最も速いガントリー回転時間および19.5ミリ秒の有効な一時的な決断を特色にする革命Apex CTのプラットホームを進水させました。 このモジュール式でスケーラブルなシステムは、心臓イメージング機能を強化し、ワークフローの効率性を向上させることを目指しています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。