北米の流体管理システム市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

4.03 Billion

USD

9.22 Billion

2024

2032

USD

4.03 Billion

USD

9.22 Billion

2024

2032

| 2025 –2032 | |

| USD 4.03 Billion | |

| USD 9.22 Billion | |

| % | |

|

北米の流体管理システム市場セグメンテーション、製品タイプ別(統合型流体管理システム、スタンドアロン型流体管理システム)、使い捨て製品および付属品別(可視化システム、圧力トランスデューサー、バルブ、コネクタ、継手、カテーテル、血液ライン、チューブセット、圧力監視ライン、吸引キャニスター、カニューレ、その他)、用途別(泌尿器科、気管支鏡検査、関節鏡検査、心臓病学、神経学、消化器学、腹腔鏡検査、婦人科/産科、耳鏡検査、歯科、麻酔科、その他)、エンドユーザー別(病院、外来手術センター、美容外科センター、その他) - 2032年までの業界動向と予測

流体管理システム市場規模

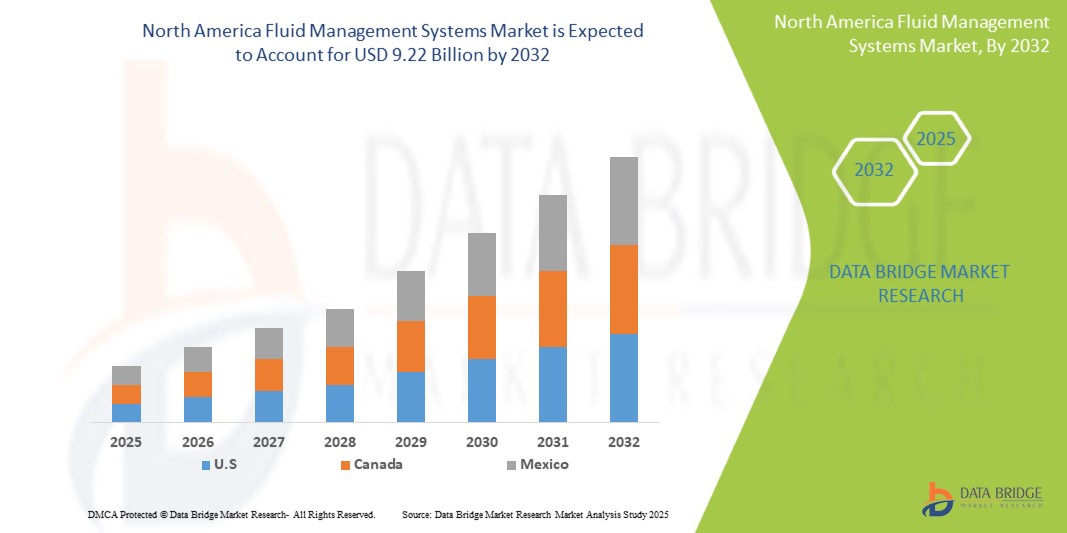

- 北米の流体管理システム市場規模は2024年に40億3000万米ドルと評価され、予測期間中に10.9%のCAGRで成長し、2032年までに92億2000万米ドル に達すると予想されています 。

- 市場の成長は、体液管理を伴う継続的な外科手術や介入処置を必要とする腎不全、心血管疾患、胃腸障害などの慢性疾患の発生率の上昇によって主に促進されています。

- さらに、北米では高齢化が進み、医療介入を必要とする患者数が増加しています。精度の向上、自動化、使い捨て部品の開発など、体液管理システムにおける技術進歩が市場拡大を牽引しています。これらの要因が相まって、体液管理ソリューションの普及が加速し、業界の成長を大きく後押ししています。

流体管理システム市場分析

- 体液管理システム市場は、人体または手術部位における体液の調整・制御を目的とした多様な医療機器と消耗品を網羅しています。これらのシステムは、体液バランスの維持、処置中の灌流・吸引の促進、そして体液廃棄物の管理に不可欠です。主要コンポーネントには、透析器、送気器、吸引・排出・灌流システム、そしてチューブセットやカテーテルなどの様々な消耗品が含まれます。これらのシステムは、泌尿器科、心臓病学、消化器科など、様々な医療専門分野に広く適用されており、透析や低侵襲手術といった処置にも用いられています。市場の成長を牽引しているのは、慢性疾患の増加、低侵襲技術の普及、そして患者ケアと処置の効率性を向上させる継続的な技術進歩です。

- 体液管理システムの需要が急増している主な要因は、低侵襲性外科手術の増加、医療施設における厳格な感染制御プロトコルへの注目の高まり、医療処置中のより安全で効率的な体液処理に対する要望の高まりです。

- 北米の体液管理システム市場は、米国が2025年に81.45%という最大の収益シェアで市場をリードする見込みです。これは、医療インフラの整備、外科手術件数の増加、そして先進的な体液管理技術の早期導入によるものです。集中治療室や手術室における体液バランスへの高い意識と、多額の医療費支出が相まって、この国の主導的地位を強固なものにしています。

- 北米の体液管理システム市場において、米国は予測期間中に最も急速に成長する国になると予想されています。その原動力となっているのは、腎不全や心血管疾患といった慢性疾患の発生率増加と、体液調節が極めて重要な低侵襲手術の需要増加です。バクスター、ストライカー、フレゼニウスといった主要企業の存在も、イノベーションとアクセス性の向上に貢献しています。

- スタンドアロン型体液管理システムは、その高い精度、画像システムとの統合機能、そして内視鏡、整形外科、婦人科手術における高い有用性により、2025年には北米の体液管理システム市場において46.9%の市場シェアを獲得し、市場を席巻すると予想されています。病院や外来手術センターにおける導入拡大は、ユーザーフレンドリーなインターフェースとリアルタイムの体液モニタリング機能によってさらに加速しています。

レポートの範囲と流体管理システム市場のセグメンテーション

|

属性 |

流体管理システムの主要市場分析 |

|

対象セグメント |

|

|

対象国 |

北米

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

流体管理システム市場動向

「低侵襲手術の導入拡大」

- 低侵襲手術と使い捨てコンポーネントの採用拡大:北米の体液管理システム市場において、重要な加速トレンドとして、高精度な体液コントロールが求められる低侵襲手術(MIS)の採用拡大が挙げられます。このトレンドは、使い捨ての体液管理デバイスおよびコンポーネントの使用増加への顕著なシフトと相まって進んでいます。

- 例えば、高度なロボットシステムを用いて行われることが多いMIS(人工心肺システム)手術では、手術部位の正確な灌流、吸引、そして明瞭な視界を確保するために、高度な体液管理システムが求められます。MISは、回復の迅速化や入院期間の短縮といったメリットを背景に人気が高まっており、こうしたシステムの需要を直接的に押し上げています。

- 同時に、チューブセット、吸引キャニスター、カテーテルといった使い捨ての体液管理機器の需要も高まっています。この変化は、主に交差汚染への懸念の高まり、滅菌コストの削減の必要性、そして医療施設における厳格な感染管理要件によって推進されています。

- 技術の進歩もまた重要なトレンドであり、企業は高粘性流体の噴射など、精度と汎用性を向上させる分野で革新を起こしています。IoT、機械学習、クラウドコンピューティングの統合により、治療成果を向上させる予測モデルの開発が可能になっています。

- より効率的で安全、かつ技術的に統合された体液管理ソリューションへのこの傾向は、北米全域で外科手術および患者ケアの実践を根本的に変えるものとなっています。

流体管理システム市場の動向

ドライバ

「慢性疾患の発生率の上昇と低侵襲手術」

- The increasing prevalence of chronic illnesses, such as kidney failure, cardiovascular diseases, gastrointestinal diseases, and urological conditions, is a significant driver for the heightened demand for fluid management systems in North America. These conditions often necessitate ongoing surgical or interventional procedures that rely heavily on precise fluid control.

- For instance, the rising rate of urological diseases, including benign prostatic hyperplasia (BPH) and kidney stones, requires increased use of endoscopy in procedures like cystoscopy and transurethral resection, which in turn boosts the need for advanced fluid management systems.

- The growing number of minimally invasive surgical procedures being performed is a primary catalyst, as these techniques require specialized fluid management for optimal visibility and reduced blood loss.

- The increasing geriatric population in North America is more susceptible to these chronic conditions, further accelerating the demand for fluid management solutions.

- Additionally, stringent infection control protocols mandated by regulatory bodies encourage the adoption of advanced fluid management systems, including closed-loop systems and disposable components, to minimize cross-contamination risks monitoring

Restraint/Challenge

“High Costs and Supply Chain Disruptions”

- The high initial investment costs associated with advanced fluid management systems, coupled with potential disruptions in global supply chains, present significant challenges to widespread market adoption, particularly for smaller healthcare facilities and those with budget constraints.

- For instance, the capital expenditure for sophisticated fluid management equipment can be substantial. Healthcare providers may face increased costs if manufacturers pass on higher production expenses due to tariffs or trade conflicts, impacting purchasing decisions.

- Trade conflicts and tariffs can disrupt global supply chains, leading to delays in production, longer lead times, and scarcity of essential components (e.g., OEM parts, electronics), which can affect the upgrade or maintenance of existing equipment.

- Additionally, the need for skilled technicians for installation, operation, and maintenance of these complex systems adds to the operational burden. The temporary reduction in elective surgeries during events like the COVID-19 pandemic also highlighted vulnerabilities in market growth.

Fluid Management Systems Market Scope

The market is segmented on the basis product type, disposables and Accessories and Application and end user.

- By Product

On the basis of Product, the Fluid Management Systems market is into Integrated Fluid Management Systems and Standalone Fluid Management Systems. Standalone Fluid Management Systems dominate the market with the largest revenue share of 46.9% in 2025, driven by their adaptability across a wide range of minimally invasive surgical procedures such as endoscopy, urology, and gynecology. These systems are favored for their precision control, ease of integration with existing surgical equipment, and growing use in ambulatory surgical centers. Technological advancements such as digital flow regulation and user-friendly touchscreen interfaces are contributing to widespread adoption.

The Integrated Fluid Management Systems segment is anticipated to witness the fastest growth rate of 5.8% from 2025 to 2032, due to the increasing demand for unified platforms that combine irrigation, suction, and visualization functions. These systems streamline procedural workflow, reduce clutter in operating rooms, and enhance surgical safety—making them highly desirable in high-volume hospitals and tertiary care centers.

- By Disposables and Accessories

On the basis of application, the Fluid Management Systems market is segmented into Visualization Systems, Pressure Transducers, Valves, Connectors and Fittings, Catheters, Bloodlines, Tubing Sets, Pressure Monitoring Lines, Suction Canisters, Cannulas, and Others. The Tubing Sets held the largest market revenue share in 2025, owing to their indispensable role in maintaining fluid pathways during diagnostic and surgical procedures. These sets are vital for safe and sterile fluid delivery and drainage, and their use spans across multiple specialties including gastroenterology, urology, and cardiology. The segment benefits from high replacement rates and widespread use in single-use sterile applications.

The Visualization Systems is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing reliance on high-definition endoscopic visualization during fluid-intensive surgeries. Innovations in HD imaging, light management, and integration with fluid control modules are boosting demand across both inpatient and outpatient settings.

- By Applications

On the basis of application, the Fluid Management Systems market is segmented into Urology, Bronchoscopy, Arthroscopy, Cardiology, Neurology, Gastroenterology, Laparoscopy, Gynecology/Obstetrics, Otoscopy, Dentistry, Anesthesiology, and Others. The Urology segment driven by the high prevalence of kidney stones, prostate disorders, and bladder conditions requiring procedures like TURP and cystoscopy. Demand for advanced irrigation and suction systems in endourological surgeries is contributing to segment dominance.

The Laparoscopy segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the growing adoption of minimally invasive surgeries for bariatric, gynecological, and gastrointestinal conditions. The need for precise fluid regulation and clear visualization in closed-body cavity procedures supports rising demand for laparoscopy-specific fluid management solutions.

- By End User

On the basis of end user, the Fluid Management Systems market is segmented into Hospitals, Ambulatory Surgical Centers (ASCs), Cosmetic Surgical Centers, and Others. The Hospitals segment is projected to dominate the market with the largest revenue share in 2025, driven by the high volume of complex surgical procedures requiring precise fluid control, such as urology, laparoscopy, and cardiology. Hospitals benefit from comprehensive infrastructure, integrated operating rooms, and higher budgets for advanced fluid management systems—both standalone and integrated. Additionally, hospitals are the primary settings for procedures involving critically ill patients and emergency cases where effective fluid balance is vital to clinical outcomes.

The Ambulatory Surgical Centers (ASCs) segment is expected to register the fastest CAGR from 2025 to 2032, owing to the rising demand for same-day surgeries and cost-effective healthcare delivery. ASCs are increasingly adopting compact, portable, and easy-to-operate fluid management systems to support minimally invasive procedures across specialties like arthroscopy, gynecology, and gastroenterology. The segment's growth is further supported by favorable reimbursement structures and the shift of elective procedures from hospitals to outpatient settings.

Fluid Management Systems Market Regional Analysis

- U.S. dominates the Fluid Management Systems market with the largest revenue share of 81.45% in 2025, driven by the increasing number of minimally invasive surgical procedures, advancements in surgical visualization, and a strong clinical preference for integrated and automated fluid control systems.

- The presence of a highly advanced healthcare infrastructure, along with the growing demand for precision and safety in surgeries such as urology, laparoscopy, and endoscopy, supports rapid adoption of fluid management technologies.

- Favorable reimbursement policies, coupled with rising investments in ambulatory surgical centers and outpatient facilities, contribute to expanded usage across a broad range of specialties. Major U.S.-based players such as Stryker, Baxter, and Zimmer Biomet continue to innovate and launch advanced fluid irrigation and suction systems integrated with high-definition imaging platforms.

- Furthermore, the increasing implementation of digital ORs (operating rooms) and growing preference for disposable fluid management accessories to reduce infection risk are supporting long-term market growth.

Canada Fluid Management Systems Market Insight

カナダの体液管理システム市場は、低侵襲手術の導入増加、デジタルヘルスインフラへの国家投資、そして公立・私立医療施設における手術環境の近代化を背景に、予測期間を通じて着実に拡大すると予測されています。カナダの医療制度は感染管理と患者の安全を重視しており、吸引キャニスター、チューブセット、使い捨てバルブといった高品質な体液管理アクセサリーの需要を促進しています。泌尿器科、婦人科、整形外科における手術件数の増加は、病院の資金援助や外科研修プログラムの改善に支えられ、導入を後押ししています。さらに、米国に拠点を置く医療機器企業との提携により、最先端システムへのアクセスが確保されています。カナダ保健省の堅牢な規制枠組みにより、非常に効果的で安全な機器のみが市場に投入されることが保証されており、外科医や調達の意思決定者の間で信頼が高まっています。

メキシコの流体管理システム市場に関する洞察

メキシコの体液管理システム市場は、進行中の医療改革、インフラ整備、公立・私立病院両方における低侵襲外科手術の普及拡大に支えられ、2025~2032年の間に顕著なCAGRで成長すると予想されています。政府主導の健康キャンペーン、医療ツーリズムの成長、特に腹腔鏡検査、内視鏡検査、婦人科における手術件数の増加が、市場拡大を牽引する主な要因です。高度なシステムへのアクセスは依然として都市部や私立の医療センターに集中していますが、官民パートナーシップや医療機器分野への外国直接投資により、より広範な地域でのシステムの可用性が向上しています。特に体液制御処置や感染予防プロトコルに関する医療従事者向けのトレーニングイニシアチブも、需要をさらに加速させています。費用対効果の高いスタンドアロンシステムや再利用可能なアクセサリの採用が一般的ですが、患者の安全基準に対する意識が高まるにつれて、使い捨て製品の使用も徐々に増加しています。

流体管理システムの市場シェア

流体管理システム業界は、主に次のような定評のある企業によって牽引されています。

- カーディナルヘルス社(米国)

- ジョンソン・エンド・ジョンソン・サービス社(米国)

- メドトロニックplc(アイルランド)

- Fresenius Medical Care AG & Co. KGaA(ドイツ

- ベクトン・ディキンソン・アンド・カンパニー(米国)

- ストライカーコーポレーション(米国)

- バクスターインターナショナル社(米国)

- エコラボ社(米国)

- B. ブラウン メルズンゲン AG (ドイツ)

- ジマー・バイオメット・ホールディングス(米国)

- オリンパス株式会社(日本)

- ホロジック社(米国)

- アートレックス社(米国)

- メリットメディカルシステムズ社(米国)

- コンメッドコーポレーション(米国)

- リチャード・ウルフGmbH(ドイツ)

- アンジオダイナミクス社(米国)

- スミス・アンド・ネフュー(英国)

- スミスメディカル社(米国)

- テレフレックス・インコーポレーテッド(米国)

- CRバード(米国)

- 3M社(米国)

北米の流体管理システム市場の最新動向

- 2024 年 11 月、Megnajet Ltd. は、高粘度の流体を噴射する際の課題に対処し、さまざまな用途にわたって信頼性の高い流体調整を保証するように設計された OmniFlo 流体管理システムを発売しました。

- 2023年8月、米国食品医薬品局は、在宅透析における体液管理を強化し、患者と介護者に在宅セッションをガイドするフレゼニウスの透析ソフトウェアを承認しました。

- 2020年12月、Cantel Medical CorpとCensis Technologiesは、Cantelの感染予防内視鏡再処理ワークフローポートフォリオとCensisの外科用資産管理および器具追跡ソリューションを組み合わせる新たな長期パートナーシップを発表しました。

- 2018 年 11 月、CrystalView Pro 灌漑システムは FDA より製品の販売承認を取得しました。

- 2018年10月、ENDOMAT SELECT子宮鏡体液管理ポンプが米国FDAの承認を取得しました。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。