北アメリカのPreclinicalのイメージ投射の市場のサイズ、共有および傾向の分析のレポート

Market Size in USD Billion

CAGR :

%

USD

1.38 Billion

USD

2.32 Billion

2024

2032

USD

1.38 Billion

USD

2.32 Billion

2024

2032

| 2025 –2032 | |

| USD 1.38 Billion | |

| USD 2.32 Billion | |

| % | |

|

北アメリカの Preclinical のイメージ投射の市場区分、プロダクトによって(システムおよびサービス)、試薬(Preclinical の光学イメージ投射の試薬、Preclinical の核イメージ投射試薬、Preclinical MRI の対照の代理店、Preclinical の超音波の対照の代理店、および Preclinical CT の対照の代理店)、適用(研究開発、薬剤の発見、生物検出、癌細胞の検出、生物マーカー、生物標識者および他の研究は、研究および研究に終わります。

北アメリカのPreclinicalイメージ投射の市場のサイズ

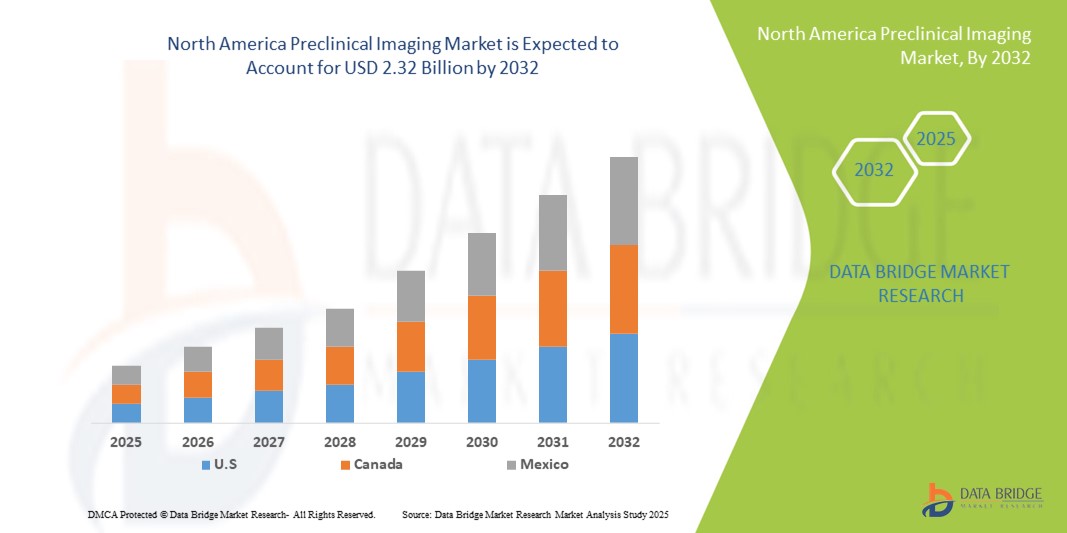

- 北米非臨床イメージング市場規模は、2024年のUSD 1.38億そして到達する予定2032年までのUSD 2.32億, お問い合わせ6.70%のCAGR予報期間中

- 市場成長は、医薬品の発見と開発への投資の増加によって主に駆動されます, などの高度な画像のモダリティの上昇の採用と相まってMRIについて、ペット、CTおよび前臨床研究のための光学イメージ投射

- さらに、動物モデルにおける疾患の進行状況を監視するための翻訳研究、パーソナライズド医薬品、非侵襲的イメージング技術に重点を置いています。 これらの要因は、主に前臨床イメージングソリューションの採用を強化し、市場の成長を著しく推進しています。

北アメリカの Preclinical のイメージ投射の市場分析

- MRI、PET、CT、光学イメージングなどの高度なイメージングシステムを網羅し、現代の創薬と翻訳研究において、動物モデルにおける非侵襲的、リアルタイムのインサイトを疾患の進行、治療の有効性、および生物学的メカニズムに提供する能力がますますます重要になっています。

- 前臨床イメージングのエスカレート要求は、主に医薬品の投資を成長させることで燃料を供給しています。バイオテクノロジー高度のイメージ投射のモダリティの研究開発、上昇の採用およびより速く、より正確な薬剤の開発のパイプラインのための増加の必要性

- 米国は、2024年に最大82.5%の収益シェアを誇る北アメリカの非臨床イメージング市場を廃止し、高R&D投資、主要なイメージング機器メーカーの強力な存在、および最先端のイメージング技術の早期採用によって特徴付けられ、製薬企業や学術研究機関を横断し、高解像MRIおよびマルチモーダルイメージングシステムにおけるイノベーションによって駆動する非臨床イメージング施設の実質的な成長を著しく

- カナダは、ライフサイエンス研究の投資拡大、バイオテクノロジーのスタートアップの成長、および翻訳およびパーソナライズド医療の焦点の増加による予測期間中、北米非公開イメージング市場で最速成長国であることが期待されています

- システムセグメントは、2024年に49.5%の市場シェアで、医薬品の発見、高解像イメージング能力、医薬品、バイオテクノロジー、学術研究施設全体における幅広い採用の重要な役割を担っています。

報告書 スコープと北米の臨床イメージング市場セグメント

| アトリビュート | 北アメリカのPreclinicalのイメージ投射のキー マーケットの洞察 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

北アメリカのPreclinicalのイメージ投射の市場の傾向

マルチモーダルとAI強化イメージングの高度化

- 北米非臨床イメージング市場における有意で加速的な傾向は、AI主導の解析ソフトウェアとマルチモーダルイメージングシステムの増大の統合であり、疾患モデルのより正確で高解像度の視覚化と治療応答を可能にします

- たとえば、MRI-PETイメージングプラットフォームの組み合わせにより、研究者は分析的および機能的なデータを同時にキャプチャし、前臨床研究の質を高め、医薬品開発のタイムラインを加速することができます。

- イメージングシステムにおけるAI統合により、自動異常検知、治療結果の予測分析、および最適化されたイメージングプロトコルなどの機能により、より優れたスループットを実現します。 たとえば、Vevo LAZR-X システムによっては、AI が画像再構築の精度を高め、縦方向の学習のための予測的なインサイトを提供します。

- イメージングモダリティとAIによるデータ分析のシームレスな組み合わせにより、イメージングワークフローの集中管理が容易になり、研究者が複数のデータセットを単一のプラットフォームから分析し、生物学的プロセスに包括的な洞察を得ることができます。

- この傾向は、よりインテリジェントで自動化され、統合されたイメージングソリューションは、根本的に非臨床研究効率の期待を再構築することです。 その結果、ブルーカーやパーキンエルマーなどの企業は、自動セグメンテーション、予測モデリング、および強化された解像度などの機能を備えたAI対応のpreclinical Imagingシステムを開発しています。

- 多様化するAI主導の非臨床イメージングプラットフォームの需要は、医薬品および学術的研究施設全体で急速に高まっています。これにより、ステークホルダーは、精度、スピード、および包括的な分析能力が向上します。

北アメリカの Preclinical のイメージ投射の市場 動的

ドライバー

R&D投資・医薬品開発活動による需要増加

- 医薬品やバイオテクノロジーの研究開発への投資の増加、迅速でより正確な医薬品開発の必要性と相まって、前臨床イメージングシステムに対する高まる要求の重要なドライバーです。

- たとえば、2024年3月、ブルーカーは、腫瘍学と神経学前臨床研究を加速し、先進的なイメージングプラットフォームの成長産業の採用を促すように設計された新しい高スループットMRI-PETイメージングソリューションを開始しました

- 研究者は、翻訳研究と精密医学に焦点を合わせ、前臨床イメージングは、薬物の有効性、安全性、病気の進行に重要な洞察を提供し、従来の評価方法よりも説得力のある利点を提供します

- さらに、米国におけるバイオテクノロジーのスタートアップやCROの拡大は、初期研究の積分的な部分を予測し、複数の研究でスケーラブルで標準化されたイメージングソリューションを提供します。

- 非侵襲的な縦方向研究を実施し、バイオマーカー式を監視し、AI分析と画像データを統合する能力は、医薬品および学術研究施設の採用を推進する重要な要因です。 高スループットのpreclinicalイメージ投射および自動化されたワークフローへの傾向は更に市場成長に貢献します

拘束/チャレンジ

コストと規制遵守のハードル

- 高度なイメージングシステムのための高資本支出を取り巻く懸念, 厳格な規制と検証要件と相まって, より広範な市場浸透に重要な課題をポーズ. preclinicalのイメージ投射装置がGLP/GMPの標準に専門にされた操作そして付着力を必要とするので、小さいbiotech会社は採用の障壁に直面します

- たとえば、スタートアップや小規模な学術機関の資金調達は、高解像MRI、PET、マルチモーダルイメージングシステムへのアクセスを制限でき、全体的な市場占有率を低下させる

- モジュラーシステムの提供、柔軟なリースオプション、および規制サポートを通じてこれらの課題に対処することは、より広範な採用を可能にするために不可欠です。 PerkinElmerやMILabsなどの企業は、潜在的な買い手間の信頼を築くためのスケーラブルなソリューションとコンプライアンスのサポートを強調しています。 また、継続的なメンテナンス、ソフトウェアのアップデート、および訓練された人事要件は、ユーザーの運用コストを増加させ、より小規模な施設の採用をより複雑にしています。

- 一部の企業は、費用対効果の高いベンチトップまたはコンパクトなイメージングシステムを導入していますが、ハイエンドのAI対応マルチモーダルプラットフォームのプレミアムは、特に初期段階のバイオテクノロジーと学術ラボの採用のためのハードルを維持しています

- コストの最適化、規制ガイダンス、およびトレーニングプログラムを通じてこれらの課題を克服することは、北米非公式イメージングにおける持続的な市場成長にとって不可欠です。

北アメリカのPreclinicalのイメージ投射の市場規模

市場は、製品、試薬、アプリケーション、エンドユーザーに基づいてセグメント化されます。

- 製品情報

製品のベースでは、北米非臨床イメージング市場はシステムとサービスに分けられます。 システムセグメントは、医薬品の発見と翻訳研究におけるMRI、PET、CT、光学系などのイメージングプラットフォームの重要な役割を担って、2024年に最大49.5%の収益シェアで市場を支配しました。 動物モデルにおける疾患の進行状況を監視し、治療の有効性を評価するための高解像、非侵襲的イメージングクリティカルを提供します。 製薬会社、バイオテクノロジー会社、学術研究機関によるこれらのシステムの強力な採用は、市場収益に著しく貢献します。 また、AIによる分析とマルチモーダルイメージングソリューションの両立性により、研究の効率化を図っています。 さらに、米国における政府の資金調達と研究開発のインセンティブがさらなるサポート体制を採用しています。

サービスセグメントは、2025年から2032年までの最速成長を目撃する見込みで、契約研究機関(CRO)に対する前方イメージング研究のアウトソーシングを増加させています。 小規模なバイオテクノロジー企業や学術ラボは、高資本支出なしで高度なイメージング機能にアクセスすることができます。 成長は、データ分析、縦方向研究、およびイメージングプロトコルの最適化を含むエンドツーエンドのイメージングソリューションの需要によってさらに燃料を供給されます。 サービス提供のスケーラビリティと柔軟性により、費用対効果の高い非臨床研究支援を求める組織に魅力的にすることができます。

- 試薬による

試薬に基づいて、北アメリカのpreclinicalイメージ投射の市場はプレクライニングのMRIの対照の代理店、前臨床光学イメージ投射の試薬、前臨床核画像の試薬、前臨床超音波の対照の代理店および前臨床CTの対照の代理店に分けられます。 プレクライニング MRI コントラスト エージェント セグメントは、高解像分析および機能的イメージングのための前方研究における MRI システムの広範な使用による 2024 年に市場を支配しました。 MRIの対照の代理店はティッシュおよび器官の可視性を高め、病気の進行および治療効果の詳細な評価を可能にします。 研究者は、正確なデータを提供しながら、動物使用量を削減する非侵襲的、縦方向の研究のためにMRIの対照代理店を好む。 また、このセグメントは、腫瘍学、神経学、心臓血管研究における適用可能性を拡大する継続的な技術改善と規制の承認から恩恵を受けています。 米国の医薬品および学術研究機関の強力な採用により、安定した市場優位性が保証されます。

プレクリンジカルオプティカルイメージング試薬セグメントは、予測期間における最速の成長を目撃し、リアルタイムで非侵襲的なモニタリングと、生きた動物モデルにおける分子および細胞プロセスのモニタリングを増加させることが期待されています。 光学イメージング試薬は、その感度、費用効率性、および高スループットイメージングプラットフォームとの互換性のために、薬物発見およびバイオマーカー研究で広く使用されています。 蛍光プローブとバイオ発光試薬のイノベーションにより、画像の品質と研究効率が向上します。 また、がん研究、生体流通研究、標的療法の開発に重点を置いたことで、成長も支援しています。

- 用途別

応用に基づき、北米非臨床イメージング市場は研究開発、医薬品の発見、バイオ流通、がん細胞の検出、バイオマーカーなどの分野に分けられます。 医薬品のディスカバリー部門は、医薬品の有効性、安全性、および臨床試験前の薬理学を評価するために不可欠であるため、2024年に市場を支配しました。 高解像イメージングは、細胞および組織レベルの効果にインサイトを提供し、研究開発パイプラインにおける迅速かつより正確な意思決定を可能にします。 医薬品会社やCROは、早期の故障を削減し、医薬品開発のタイムラインを加速するために、前臨床イメージングに大きく依存しています。 導入はまた、非侵襲的な動物研究のための規制奨励によって運転され、倫理的なコンプライアンスを最適化します。 創薬ワークフローにおけるAIとマルチモーダルイメージングの統合により、生産性と分析精度が向上します。

バイオマーカーのセグメントは、予測期間中の予測期間中に最速の成長を目撃すると予想され、高精度医学とパーソナライズされた治療に焦点を当てて燃料を供給しました。 イメージングベースのバイオマーカーの検出により、研究者は、疾患の進行と治療の応答をバイボで追跡し、翻訳研究を支援することができます。 成長は、バイオテクノロジー企業と学術機関とのコラボレーションの拡大により、腫瘍学、神経学、免疫学に関する新たなバイオマーカーを特定し、さらに強化されます。 また、高感度イメージングプローブやAIを用いたデータ解析における技術の進歩にもメリットがあります。

- エンドユーザーによる

エンドユーザーに基づいて、北米非臨床イメージング市場は、契約研究機関(CROS)、医薬品・バイオテクノロジー企業、学術・政府研究機関、診断センター、その他に分けられます。 医薬品&バイオテクノロジー企業セグメントは、2024年に医薬品開発を加速する高スループットイメージングソリューションの必要性で重要な投資による市場を支配しました。 これらの企業は、高度なイメージングシステムと試薬を活用して、薬物の有効性、安全性、およびバイオディストリビューションを評価します。 米国とカナダの大手製薬研究開発拠点、およびイメージングソリューションプロバイダーとのパートナーシップにより、優位性が認められています。 マルチモーダルイメージングシステムとAI強化分析の採用により、市場シェアを強化。

CROs セグメントは、2025 から 2032 までの最速の成長を目撃する見込みで、非推奨のイメージングにより、より小規模なバイオテクノロジー企業や学術ラボが、重大資本投資なしで高度なイメージング機能にアクセスできるようになります。 CROsは、イメージング、データ分析、規制対応などのスケーラブルでエンドツーエンドのサービスを提供しています。 成長は、柔軟性と費用対効果の高い非臨床研究ソリューション、米国におけるCROネットワークの拡大、製薬会社と専門サービスプロバイダ間のコラボレーションの増加に対する需要の増加によって促進されます。

北アメリカのPreclinicalイメージ投射の市場地域分析

- 米国は、2024年に最大82.5%の収益シェアを誇る北アメリカの非臨床イメージング市場を支配し、高研究開発投資、主要なイメージング機器メーカーの強力な存在によって特徴付けられました

- 領域内の研究者や組織は、疾患の進行、薬物の有効性、およびバイオマーカーの識別の効率的な監視を可能にする、非侵襲的イメージングシステムの精度、高解像能力、および非侵襲的な性質を高く評価しています。

- この広範囲にわたる採用は、バイオテクノロジー企業と学術研究機関とのコラボレーション、および翻訳およびパーソナライズされた医薬品に焦点を当て、現代の創薬および開発ワークフローの重要なコンポーネントとして、前方イメージングを確立し、強力な研究開発インフラによってさらにサポートされています。

U.S. Preclinical Imaging Market のインサイト

米国非臨床イメージング市場は、医薬品およびバイオテクノロジー研究開発および主要なイメージング機器メーカーの実質的な投資によって燃料を供給し、北米で2024年に最大の収益シェアを占めています。 研究者や組織は、疾患の進行、薬物の有効性、およびバイオマーカーの発見を監視するために、高解像、非侵襲的イメージングシステムを優先しています。 マルチモーダルイメージングの普及とAI・AI市場をさらに推進する分析を支援しました。 また、製薬会社、バイオテクノロジー企業、学術機関とのコラボレーションは、特に腫瘍学、神経学、心臓研究に大きく貢献しています。

カナダ Preclinical Imaging Market Insight

カナダの非臨床イメージング市場は、主にライフサイエンス研究とバイオテクノロジーの政府や民間投資の増加によって推進され、予測期間全体で実質的なCAGRで拡大する予定です。 CROとバイオテクノロジーのスタートアップの立ち上がりは採用を促進していますが、翻訳とパーソナライズされた医学研究の需要が増えています。 カナダの研究機関は、高度なイメージングシステムを活用して、創薬パイプラインを最適化しています。 効率と分析精度を向上させるAIとイメージングソフトウェアの統合は、市場成長を加速しています。 また、米国を拠点とする製薬会社とのコラボレーションにより、最先端のイメージング技術の知識の伝達と採用を支援

メキシコの臨床イメージング市場動向

メキシコの非臨床イメージング市場は、医薬品およびバイオテクノロジーの研究活動の増加と学術および政府研究機関の拡大によって推進され、安定した成長を目撃しています。 米国と欧州の製薬会社との研究開発およびコラボレーションにおける投資の拡大は、先進的なイメージングシステムの導入を支援しています。 高精度イメージングサービスを提供するCROsの存在は、高解像度MRI、PET、CT、光学イメージングプラットフォームへのアクセスを促進しています。 バイオテクノロジーのイノベーションとライフサイエンスの研究を推進する政府の取り組みは、市場をさらに高めています。 メキシコは、研究インフラの改善と熟練した人材の育成に注力し、非臨床イメージングシステムの採用を強化しています。

北アメリカのPreclinicalイメージ投射の市場シェア

北アメリカのpreclinicalのイメージ投射工業は主に下記のものを含んでいる十分に確立された会社によって、導きます:

- ブルーカー(アメリカ)

- PerkinElmer(アメリカ)

- Trifoil Imaging LLC(米国)

- 株式会社メディソ(ハンガリー)

- MILabs B.V.(オランダ)

- MRソリューションズ(英国)

- アスペクトイメージング株式会社(イスラエル)

- 株式会社ビジュアルソニックス(カナダ)

- 株式会社LI-COR(米国)

- 富士フイルムホールディングス株式会社(日本)

- カブレサ株式会社(カナダ)

- スカンコメディカルAG(スイス)

- サーモフィッシャーサイエンス株式会社(米国)

- リガクホールディングス株式会社(日本)

- アジレントテクノロジーズ株式会社(米国)

- モレキューブ(ベルギー)

- 上海ユナイテッドイメージングヘルスケア株式会社(中国)

北米臨床イメージング市場における最近の発展は何ですか?

- 2025年9月、Revityはノースカロライナ州のIn Vivo Imaging Center of Excellenceを設立しました。 次世代計測器、光学イメージングシステム、X線CT、マルチモーダルAI解析ソフトウェア、超音波システムなど、次世代の計測機器の開発を目指します。 現在、Revvityの主要イノベーションには、IVIS光学イメージングシステム、Quantum GX3 microCTシステム、Vega自動前方超音波システム、VivoJect Image-Guidedインジェクションシステムなどが含まれます。

- 2025年8月、ユナイテッド・イメージングは、そのuMR UltraおよびuOmniscanシステムのFDAクリアランスを発表しました。 これらのシステムは、高解像イメージング機能を提供するように設計されており、疾患メカニズムの研究と小さな動物モデルにおける治療介入を強化します

- ユナイテッド・イメージングは、2025年5月、ISMRMアニュアル・サイエンティフィック・ミーティングで先進的なイメージング技術を紹介しました。 当社は、磁気共鳴イメージング(MRI)システムにおけるイノベーションを強調し、差別化された技術を重視しています。 ユナイテッド・イメージングの参加は、前臨床研究用途におけるイメージングソリューションの推進に取り組みます。

- 2024年2月、大手の科学機器会社であるブルーカー株式会社がSpectral Instruments Imaging LLCを買収 本買収は、インビブオ光学イメージングシステムのポートフォリオを拡大することにより、ブルーカーバイオスピンのPreclinical Imaging(PCI)部門を強化することを目的としています。 動きは病気の研究の Bruker の機能を高め、競争のpreclinical のイメージ投射の市場の位置を補強しました

- 以前はPerkinElmerとして知られるRevvity, Inc.は、2023年9月に、科学的発見を加速するように設計された次世代の非臨床イメージング技術のシリーズを発表しました。 このポートフォリオ拡張には、IVIS Spectrum 2とIVIS SpectrumCT 2システムが搭載され、より感度と汎用性が向上しました。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。