北米外科手術顕微鏡市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

315.76 Million

USD

821.78 Million

2024

2032

USD

315.76 Million

USD

821.78 Million

2024

2032

| 2025 –2032 | |

| USD 315.76 Million | |

| USD 821.78 Million | |

| % | |

|

北米の手術用顕微鏡市場:技術別(拡張現実(AR)および3D可視化、蛍光イメージング、ロボット統合)、タイプ別(キャスター付き、壁掛け、卓上、天井設置)、用途別(眼科、脳神経外科および脊椎外科、耳鼻咽喉科、歯科、形成外科および再建外科、婦人科、泌尿器科、その他の外科)、エンドユーザー別(病院、診療所、その他の環境) - 2032年までの業界動向と予測

北米の外科手術用顕微鏡市場規模

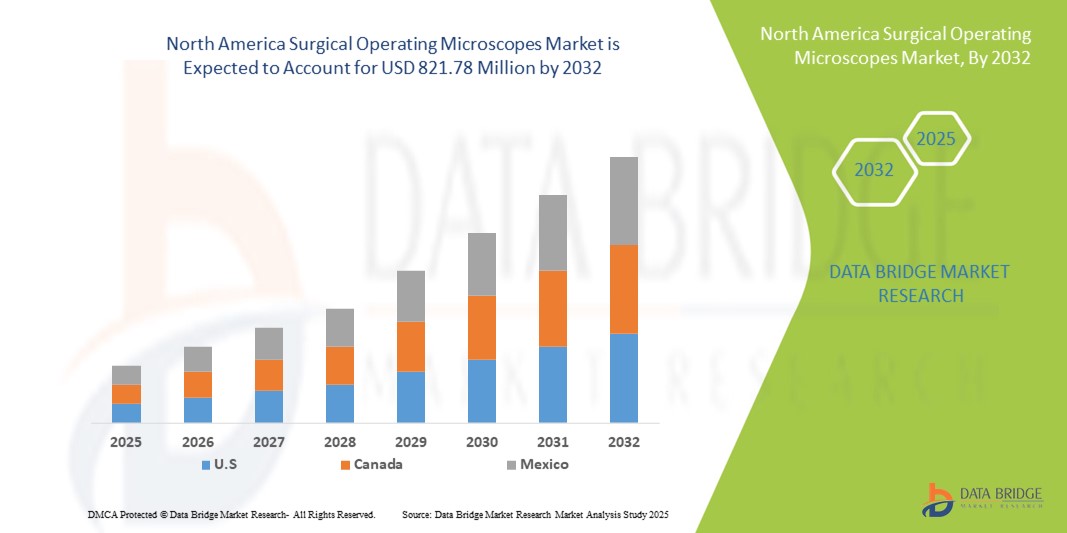

- 北米の外科手術用顕微鏡市場規模は2024年に3億1,576万米ドルと評価され、予測期間中に12.70%のCAGRで成長し、2032年には8億2,178万米ドル に達すると予想されています 。

- 市場の成長は、主に低侵襲手術や精密手術の需要の増加と、 3D視覚化、拡張現実、蛍光イメージングなどの急速な技術進歩によって推進され、脳神経外科、眼科、耳鼻咽喉科の手術における手術結果が向上しています。

- さらに、病院や専門外科センターにおける導入の増加、医療インフラの整備、そして質の高い患者ケアへの関心の高まりにより、手術用顕微鏡は現代の外科手術現場において不可欠なツールとしての地位を確立しつつあります。これらの要因が重なり、高度な手術用顕微鏡の普及が加速し、業界の成長を大きく後押ししています。

北米の外科手術用顕微鏡市場分析

- 手術用顕微鏡は、複雑な手術のための高精度の視覚化を提供し、強化された画像化能力、人間工学に基づいた設計、3D視覚化、拡張現実、蛍光イメージングなどの高度な技術との統合により、脳神経外科、眼科、耳鼻咽喉科、脊椎手術にわたる現代の外科手術においてますます重要なコンポーネントとなっています。

- 手術用顕微鏡の需要の高まりは、主に低侵襲手術の採用の増加、慢性疾患の蔓延、手術精度と患者の転帰の改善に対するニーズの高まりによって促進されています。

- 2024年には、北米の手術用顕微鏡市場で米国が最大の収益シェア87.8%を占め、市場を席巻しました。その特徴は、先進的な医療インフラ、最先端の医療技術の導入率の高さ、そして主要な市場プレーヤーの強力な存在感です。病院や専門手術センターが大幅な成長を牽引し、既存の医療機器メーカーと、強化された画像処理とロボットの統合に重点を置く新興技術プロバイダーの両方によるイノベーションに支えられています。

- カナダは、医療施設への投資の増加、高度な外科的ソリューションに対する意識の高まり、病院や専門クリニックでの高性能手術顕微鏡の導入により、予測期間中に最も急速な成長が見込まれています。

- 脳神経外科および脊椎手術セグメントは、複雑な外科手術における高精度で高度な画像ソリューションへの高い需要に牽引され、2024年に北米の手術用顕微鏡市場で36.1%の市場シェアを獲得して市場を支配しました。

レポートの範囲と北米の外科手術用顕微鏡市場のセグメンテーション

|

属性 |

北米の外科手術用顕微鏡の主要市場分析 |

|

対象セグメント |

|

|

対象国 |

北米

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

北米の外科手術用顕微鏡市場動向

3DとARの統合による手術精度の向上

- 北米の手術用顕微鏡市場における重要な加速傾向として、3D視覚化、拡張現実(AR)、蛍光イメージングの統合が進み、複雑な手術中の手術精度と視覚化が向上しています。

- 例えば、ZEISS KINEVO 900顕微鏡は3D視覚化とARオーバーレイを統合しており、外科医は精度を向上させ、リアルタイムの解剖学的ガイダンスで脳神経外科手術を行うことができます。

- ARと3Dの統合により、奥行き知覚の強化、組織のより優れた差別化、リアルタイムの手術オーバーレイなどの機能が可能になり、ロボット支援ナビゲーションにより繊細な処置における正確な動きの安定性が確保されます。

- 顕微鏡と画像システム、手術計画ソフトウェアのシームレスな統合により、集中管理と術中意思決定の強化が容易になり、外科医はライブイメージングと術前スキャンを組み合わせてより良い結果を得ることができます。

- よりインテリジェントで直感的、そして相互接続された外科システムへのトレンドは、手術室の機能に対する期待を一変させています。その結果、ライカマイクロシステムズなどの企業は、強化された視覚化、ロボットによる位置決め、デジタル記録機能を備えたAR対応顕微鏡を開発しています。

- 医療機関が患者の安全、精度、低侵襲手術を優先する傾向が強まるにつれ、高度な画像処理とAR統合機能を備えた手術用顕微鏡の需要が病院や専門外科センターで急速に高まっています。

北米の外科手術用顕微鏡市場の動向

ドライバ

外科手術の複雑化と低侵襲手術の増加によるニーズの高まり

- 複雑な手術の増加と低侵襲手術の採用の増加が相まって、手術用顕微鏡の需要が高まっている大きな要因となっている。

- 例えば、2024年3月、ジョンソン・エンド・ジョンソン・メディカル・デバイスは、高精度の画像統合を重視し、脊椎および頭蓋手術用の高度な手術用顕微鏡を病院ネットワーク全体に導入すると発表しました。

- 医療提供者が手術結果と患者の安全性の向上に注力する中、高度な顕微鏡は高解像度の3D視覚化、蛍光イメージング、ロボット支援による位置決めなどの機能を提供し、従来の光学システムよりも魅力的なアップグレードを提供します。

- さらに、専門外科センターや病院への投資の増加により、手術用顕微鏡は他の手術室技術や計画ソフトウェアとのシームレスな統合を可能にする必須機器となっています。

- 手術時間の短縮、視覚化の向上、人間工学の改善により複雑な手術を行える能力は、病院と診療所の両方でこれらの顕微鏡の採用を推進する重要な要因です。

抑制/挑戦

High Cost and Regulatory Compliance Hurdles

- The high initial cost of advanced surgical operating microscopes, combined with strict medical device regulations, poses a significant challenge to broader market penetration

- For instance, High-cost AR-enabled microscopes from ZEISS or Leica can exceed USD 250,000, limiting adoption by smaller hospitals or outpatient centers

- Addressing regulatory requirements, including FDA approvals and ISO certifications, is crucial for market entry, as delays can hinder product launches and adoption in healthcare facilities

- In addition, training surgeons and staff to effectively operate advanced systems requires time and resources, creating further barriers to adoption, especially in facilities with limited budgets

- While costs are gradually decreasing for mid-range systems, the perceived premium for cutting-edge features can still hinder adoption, particularly among price-sensitive clinics or emerging hospitals

- Overcoming these challenges through cost optimization, regulatory support, and training programs will be vital for sustained market growth

North America Surgical Operating Microscopes Market Scope

The market is segmented on the basis of technology, type, application, and end-users.

- By Technology

On the basis of technology, the surgical operating microscopes market is segmented into Augmented Reality (AR) and 3D Visualization, Fluorescence Imaging, and Robotic Integration. The AR and 3D Visualization segment dominated the market with the largest revenue share of 42.5% in 2024, driven by its ability to enhance surgical precision, provide real-time anatomical overlays, and improve spatial awareness during complex procedures. Hospitals prioritize AR-enabled microscopes for neurosurgery and spine surgeries requiring maximum accuracy. Surgeons benefit from multiple viewing angles without repositioning patients, improving workflow efficiency. AR integration allows for preoperative planning and intraoperative guidance simultaneously. Training and simulation programs in teaching hospitals also leverage AR-based microscopes. High adoption rates among top-tier hospitals reinforce the dominance of this segment.

The Fluorescence Imaging segment is anticipated to witness the fastest growth rate of 14.8% from 2025 to 2030, fueled by rising demand for tissue differentiation, tumor detection, and minimally invasive procedures. Fluorescence microscopes help surgeons distinguish critical structures such as blood vessels, nerves, and tumors in real time. Hospitals and specialty surgical centers are investing in these systems for enhanced precision. Integration with AR and robotic-assisted navigation improves surgical outcomes. Growing awareness among surgeons about better post-surgery recovery is driving adoption. The segment’s growth is further supported by rising research in fluorescence-guided surgery.

- By Type

On the basis of type, the surgical operating microscopes market is segmented into on casters, wall mounted, table top, and ceiling mounted. The Ceiling-Mounted Systems segment dominated the market with the largest revenue share of 39.7% in 2024, due to their stability, flexibility, and suitability for high-volume operating rooms. Hospitals prefer these systems as they occupy minimal floor space and provide optimal positioning. They support a wide range of procedures including neurosurgery, ophthalmology, and ENT. Advanced models integrate lighting, imaging, and AR functionalities. Ceiling-mounted systems are durable, cost-effective, and require less maintenance. Their installation across North American hospitals reinforces their market dominance.

The On-Casters (Mobile) Systems segment is anticipated to witness the fastest growth rate of 15.3% from 2025 to 2030, due to portability and multi-room usage. These systems are popular in specialty clinics and smaller hospitals where flexibility is critical. Surgeons can reposition the microscope quickly without permanent installation. Mobile systems increasingly integrate AR and imaging features for improved outcomes. Growth in outpatient surgical centers contributes to adoption. Their adaptability across multiple surgical setups is driving demand.

- By Application

On the basis of application, the surgical operating microscopes market is segmented into ophthalmology, neurosurgery and spine surgery, ENT surgery, dentistry, plastic and reconstructive surgeries, gynaecology, urology, and other surgeries. The Neurosurgery & Spine Surgery segment dominated the market with the largest revenue share of 36.1% in 2024, driven by high demand for precision and advanced imaging technologies. Complex procedures require accurate positioning, AR overlays, and robotic assistance. Hospitals invest in high-end microscopes to reduce operative time and improve patient outcomes. Teaching hospitals leverage these systems for surgeon training. Integration with fluorescence imaging supports tumor and tissue differentiation. Increasing neurological disorder cases further reinforce the segment’s dominance.

The Ophthalmology segment is anticipated to witness the fastest growth rate of 16.1% from 2025 to 2030, due to rising prevalence of eye disorders and demand for minimally invasive surgeries. Procedures such as cataract, retinal, and corneal surgeries require high magnification and illumination. 3D visualization and AR integration improve surgical efficiency. Clinics adopt compact, ergonomic microscopes for outpatient procedures. Technological innovations enhance accuracy and outcomes in eye surgeries. Patient preference for advanced treatments is driving growth.

- By End-Users

On the basis of end-users, the surgical operating microscopes market is segmented into hospital, physician clinics, and other settings. The Hospitals segment dominated the market with the largest revenue share of 81.5% in 2024, due to their capacity to perform high-volume, complex surgeries. Neurosurgery, spine, and ophthalmology departments rely on advanced microscopes for precision. Ceiling-mounted and robotic-integrated systems improve patient outcomes. Hospitals have the budget and trained staff to adopt high-end systems. Teaching hospitals further drive demand through training programs. Hospitals’ consistent investments reinforce market dominance.

The Physician Clinics and Specialty Centers segment is anticipated to witness the fastest growth rate of 13.9% from 2025 to 2030, due to increasing outpatient procedures and minimally invasive surgeries. Mobile and compact microscopes are preferred in these settings. Surgeons benefit from ergonomic and technologically advanced systems. Clinics performing cosmetic, ENT, ophthalmology, and dental procedures drive adoption. Cost-effective, portable solutions support growth. Expanding outpatient facilities further accelerate demand.

North America Surgical Operating Microscopes Market Regional Analysis

- The United States dominated the North America surgical operating microscopes market with the largest revenue share of 87.8% in 2024, characterized by advanced healthcare infrastructure, high adoption of cutting-edge medical technologies, and a strong presence of key market players

- Hospitals and specialty surgical centers in the U.S. highly value features such as 3D visualization, augmented reality (AR) overlays, fluorescence imaging, and robotic integration, which enhance surgical precision and improve patient outcomes

- This widespread adoption is further supported by high healthcare expenditure, presence of leading medical device manufacturers, skilled surgical professionals, and rising awareness of advanced surgical solutions, establishing surgical operating microscopes as essential tools in modern operating rooms

U.S. North America Surgical Operating Microscopes Market Insight

The U.S. surgical operating microscopes market captured the largest revenue share in 2024 within North America, fueled by the swift adoption of advanced surgical technologies and the growing trend of minimally invasive and precision surgeries. Hospitals and specialty surgical centers increasingly prioritize features such as 3D visualization, augmented reality (AR) overlays, fluorescence imaging, and robotic integration to enhance surgical outcomes. The growing preference for high-precision procedures, combined with a strong presence of skilled surgeons and cutting-edge hospitals, further propels the market. Moreover, the integration of surgical microscopes with imaging systems and planning software is significantly contributing to the market's expansion.

Canada Surgical Operating Microscopes Market Insight

カナダの手術用顕微鏡市場は、予測期間を通じて大幅なCAGRで拡大すると予測されています。これは主に、医療インフラへの投資の増加と、病院や専門クリニックにおける先進的な手術機器の導入増加に牽引されています。手術精度、患者の安全性、そして手術結果の向上への重点が、手術用顕微鏡の導入を促進しています。カナダの病院やクリニックでは、新規手術室や改修プロジェクトにこれらのシステムを導入しています。外科医や医療管理者の間で低侵襲手術に対する意識が高まっていることも、導入を後押ししています。医療の近代化を支援する政府の取り組みも、市場の成長をさらに促進しています。

メキシコの外科手術用顕微鏡市場の洞察

メキシコの手術用顕微鏡市場は、民間医療施設の拡大と高度な外科ソリューションへの需要増加に牽引され、予測期間中に注目すべきCAGRで成長すると予想されています。メキシコの病院や専門センターは、手術成績の向上を目指し、AR、3D可視化、蛍光イメージング機能を備えた顕微鏡への投資を増やしています。精密手術を必要とする慢性疾患や複雑な疾患の増加も、顕微鏡の導入を促進しています。メキシコでは、都市部の医療インフラの発展と病院の技術水準の向上が市場の成長を支えています。外科医向けの研修プログラムも、高度な顕微鏡の普及に貢献しています。

北米の外科手術用顕微鏡市場シェア

北米の外科手術用顕微鏡業界は、主に次のような定評ある企業によって牽引されています。

- ライカマイクロシステムズ(ドイツ)

- カールツァイスAG(ドイツ)

- オリンパス株式会社(日本)

- トプコン株式会社(日本)

- アルコンビジョンLLC(米国)

- ハーグ通り(スイス)

- カール・ストルツ(ドイツ)

- ストライカー(米国)

- メドトロニック(アイルランド)

- スミス・アンド・ネフュー(英国)

- ジョンソン・エンド・ジョンソンおよびその関連会社(米国)

- ボシュロム(米国)

- キヤノンメディカルシステムズ株式会社(日本)

- ペンタックスメディカルカンパニー(日本)

- ブレインラボSE(ドイツ)

- マイクロサージカルテクノロジー(米国)

- シナプティブメディカル(カナダ)

- Motic Instruments Inc.(カナダ)

北米の外科手術用顕微鏡市場の最近の動向は何ですか?

- 2025年7月、デューク大学の研究者らは、ライトフィールド技術を用いて高精度な3D画像を提供する手術用顕微鏡「FiLM-Scope」を発表しました。この装置は48枚の多視点画像を同時に撮影し、手術中の奥行き知覚と精度を向上させます。

- 2024年10月、Beyeonicsは、拡張現実(AR)ベースのヘッドセットと目に見えない赤外線照明を搭載した初の完全デジタル眼科用内視鏡「Beyeonics One」を発表しました。この革新は、眼科手術における手術精度と患者の快適性の向上を目指しています。

- 2024年3月、ZEISSは、視覚化機能を強化した3Dヘッドアップ式眼科顕微鏡「ARTEVO 850」を発売しました。このシステムは、手術中の奥行き知覚と鮮明度を向上させることで、眼科手術に革命をもたらすことを目指しています。

- ライカマイクロシステムズは2024年1月、脳神経外科用デジタル可視化顕微鏡ARveo 8の進化版を発表しました。この新バージョンは、3Dビューと拡張現実(AR)蛍光技術を統合しています。同社によると、これにより手術の可視化が向上し、脳腫瘍や血管手術において外科医により包括的な情報を提供します。

- 2022年9月、オリンパス株式会社、ソニー、ソニー・オリンパスメディカルソリューションズは、新たな4K外科用内視鏡システムの開発を発表しました。「VISERA ELITE III」と名付けられたこのシステムは、4K、3D、赤外線(IR)画像に対応し、内視鏡手術の視認性向上に重点を置いています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。