北米超音波機器市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

3.47 Billion

USD

5.65 Billion

2024

2032

USD

3.47 Billion

USD

5.65 Billion

2024

2032

| 2025 –2032 | |

| USD 3.47 Billion | |

| USD 5.65 Billion | |

| % | |

|

北米超音波装置市場、タイプ別:診断用超音波装置(2D超音波、3D/4D超音波、ドップラー超音波、その他)、治療用超音波装置(高密度焦点式超音波(HIFU)、体外衝撃波結石破砕術(ESWL)、その他)、携帯性別:カート/台車式超音波装置、コンパクト/ハンドヘルド超音波装置、用途別:放射線科/一般画像診断、心臓病学、産婦人科、ポイントオブケア(POC)、泌尿器科、血管科、その他、エンドユーザー別:病院、診断センター、外来手術センター、専門クリニック、その他、国別(米国、カナダ、メキシコ)、2032年までの業界動向と予測

超音波装置市場規模

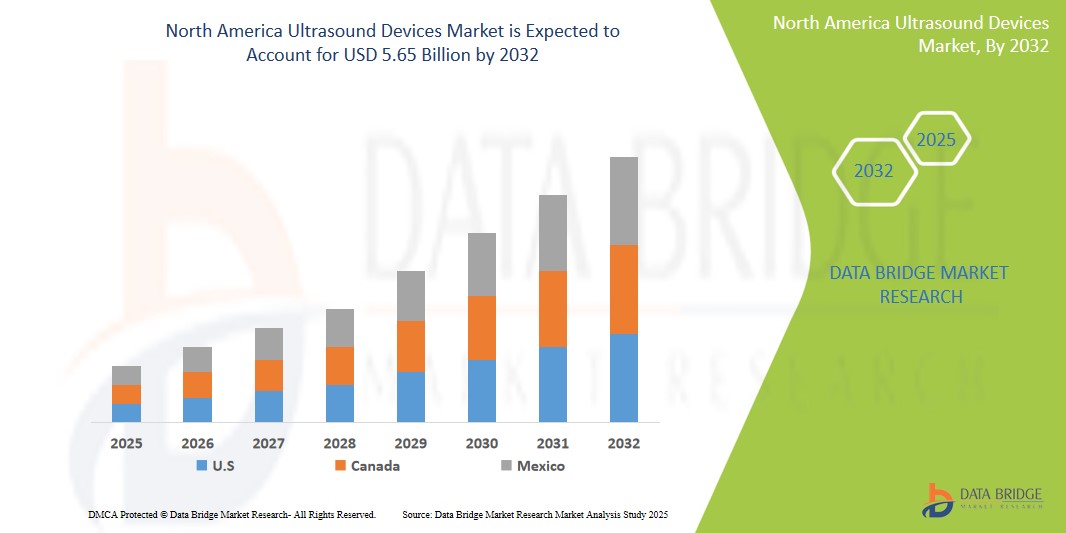

- 北米の超音波装置市場規模は、2024年に34億7,000万米ドルと評価され、2025年から2032年の予測期間中に6.5%のCAGRを示し、2032年までに56億5,000万米ドルに達すると予測されています。

- さらに、早期の診断とモニタリングを必要とする慢性疾患の増加と、非侵襲性の診断手順に対する好みの高まりが相まって、超音波装置は患者のケアと管理における重要なツールとしての地位を確立しています。

- これらの要因が重なり合って超音波機器の導入が加速し、この地域における業界の成長が大きく促進されています。

超音波装置市場分析

- リアルタイム画像、非侵襲性、携帯性を提供する超音波装置は、病気の早期発見、処置のガイド、治療効果のモニタリングを可能にすることから、さまざまな状況における現代の診断および治療ケアのますます重要な要素となっています。

- 超音波装置の需要が急増している主な要因は、人口の高齢化、さまざまな病状の発症率の上昇、そしてより良い臨床結果とより幅広い用途を提供する装置技術の継続的な革新です。

- 米国は、確立された医療インフラ、高い医療費、大手医療機器メーカーの存在により、2024年には超音波装置市場で45.25%という最大の収益シェアを占めることになります。

- 診断用超音波装置セグメントは、日常的な診断のためのさまざまな医療専門分野での広範な使用と、高度な画像処理機能の継続的な開発により、2025年には58.8%の市場シェアを獲得し、超音波装置市場を支配すると予想されています。

レポートの範囲と超音波装置市場のセグメンテーション

|

属性 |

超音波機器の主要市場分析 |

|

対象セグメント |

|

|

対象国 |

北米

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、専門家による詳細な分析、価格設定分析、ブランドシェア分析、消費者調査、人口統計分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制の枠組みも含まれています。 |

超音波装置市場の動向

「ポイントオブケア超音波(POCUS)の導入拡大」

- 北米の超音波装置市場における重要なトレンドとして、ポイントオブケア超音波(POCUS)の採用が高まっています。これらの装置は、即時診断、患者搬送時間の短縮、患者のベッドサイドでの臨床意思決定の改善といったメリットを提供し、様々な医療従事者による導入が進んでいます。

- たとえば、ポータブルおよびハンドヘルドの超音波デバイスの進歩により、救急治療室、集中治療室、プライマリケアクリニックなど、さまざまな臨床現場で診断および監視できる症状の範囲が拡大しています。

- さらに、超音波システムへのAIを活用した画像診断と解析の統合が急速に進んでいます。これらのシステムは、画質の向上、測定の自動化、診断精度の向上をもたらし、患者の転帰改善と効率性の向上につながる可能性があります。

- 高度な画像技術と電子健康記録 (EHR) および遠隔医療プラットフォームとのシームレスな統合により、超音波検査のアクセシビリティと有用性も向上しています。

超音波機器市場の動向

ドライバ

「技術の進歩と応用の拡大」

- The continuous technological advancements in ultrasound devices, coupled with their expanding range of clinical applications, are significant drivers for the heightened demand in the North America market.

- For instance, innovations such as 3D/4D imaging, elastography, and contrast-enhanced ultrasound provide more detailed and accurate diagnostic information, leading to improved patient management. Similarly, the growing use of ultrasound in interventional procedures, such as guided biopsies and therapeutic ablations, further expands its utility.

- As the capabilities of ultrasound technology continue to evolve, and its applications become more diverse, the demand for a wide range of ultrasound devices is expected to increase substantially.

- Furthermore, the growing awareness among patients and healthcare professionals regarding the non-invasive nature and versatility of ultrasound examinations is contributing to increased adoption rates.

Restraint/Challenge

“High Cost of Advanced Ultrasound Systems and Skilled Workforce Requirements”

- The relatively high cost of some advanced ultrasound devices, particularly those with cutting-edge technologies like 3D/4D capabilities and integrated AI, can pose a significant challenge to broader market access.

- For instance, the acquisition cost of high-end cart-based ultrasound systems can be substantial, potentially limiting their adoption, especially in smaller healthcare facilities or those with stringent budget constraints. Additionally, the need for highly skilled and trained professionals to operate and interpret complex ultrasound examinations can create a bottleneck in wider adoption, particularly in regions facing a shortage of specialized sonographers and radiologists.

- Addressing these cost and workforce challenges through value-based purchasing models, training programs, and the development of more user-friendly interfaces will be crucial for ensuring wider patient access to advanced ultrasound devices.

- While efforts are underway to improve affordability and address workforce needs, these issues remain significant considerations for market growth.

Ultrasound Devices Market Scope

The market is segmented on the basis of type, portability, application, and end-user.

By Type

On the basis of type, the ultrasound devices market can be segmented into diagnostic ultrasound devices (2D ultrasound, 3D/4D ultrasound, Doppler ultrasound, others) and therapeutic ultrasound devices (High-Intensity Focused Ultrasound (HIFU), Extracorporeal Shockwave Lithotripsy (ESWL), others). The diagnostic ultrasound devices segment dominates the largest market revenue share of 58.8% in 2025 due to their widespread and increasing use in a broad range of diagnostic applications across various medical specialties.

The therapeutic ultrasound devices segment is anticipated to witness the fastest growth rate of 13.7% from 2025 to 2032 due to its non-invasive nature, real-time imaging capabilities, and expanding applications across diverse medical fields. Technological advancements, including AI integration and portable point-of-care systems, are enhancing diagnostic accuracy and accessibility.

By Portability

On the basis of portability, the market is segmented into cart/trolley-based ultrasound devices and compact/handheld ultrasound devices. The cart/trolley-based ultrasound devices segment dominates the largest market revenue share in 2025 due to their increasing adoption in point-of-care settings, emergency medicine, and remote diagnostics, offering enhanced convenience and accessibility.

The compact/handheld ultrasound devices segment is expected to witness the fastest CAGR from 2025 to 2032 due to their portability, ease of use, and affordability. These devices enable point-of-care diagnostics, making ultrasound imaging more accessible in remote or underserved areas.

By Application

On the basis of application, the market is segmented into radiology/general imaging, cardiology, obstetrics/gynecology, point of care (POC), urology, vascular, and others. The radiology/general imaging segment dominates the largest market revenue share in 2025 due to the growing emphasis on immediate diagnosis and intervention across diverse clinical environments, from emergency rooms to remote clinics.

The cardiology segment is expected to witness the fastest CAGR from 2025 to 2032 due to the increasing prevalence of cardiovascular diseases and the demand for non-invasive diagnostic tools. Ultrasound imaging, especially echocardiography, is widely used in assessing heart conditions, including valve disorders, heart failure, and coronary artery disease.

By End-user

On the basis of end-user, the market is segmented into hospitals, diagnostic centers, ambulatory surgical centers, specialty clinics, and others. The hospitals segment dominates the largest market revenue share in 2025 due to the high volume of patient admissions, comprehensive range of diagnostic services, and significant investment in advanced medical equipment.

The diagnostic centers segment is expected to witness the fastest CAGR from 2025 to 2032 due to their ability to offer specialized, accessible, and cost-effective imaging services outside hospital settings. These centers provide shorter wait times, faster reporting, and a wide range of advanced imaging modalities, driving higher patient volumes.

Ultrasound Devices Market Regional Analysis

- The U.S. dominates the Ultrasound Devices market with the largest revenue share of 45.25% in 2024, driven by a large and aging population, high prevalence of chronic diseases, and well-established healthcare infrastructure with favorable reimbursement policies.

- この強力な市場地位は、大手医療機器企業の存在と機器技術の継続的な進歩によってさらに支えられています。

カナダの超音波機器市場に関する洞察

カナダの超音波装置市場は、人口の高齢化と非侵襲性画像診断の利点に対する意識の高まりを背景に、2025年には北米で大きな収益シェアを獲得しました。医療アクセスの向上を目指す政府の取り組みと、疾患の早期発見に対する需要の高まりが、市場拡大に貢献しています。

メキシコの超音波機器市場の洞察

メキシコの超音波装置市場は、医療費の増加と高度な診断ソリューションへの意識の高まりにより、2025年には北米で顕著な収益シェアを獲得しました。慢性疾患の発生率の上昇と医療インフラの改善の必要性が、超音波装置の需要を押し上げています。

超音波装置の市場シェア

超音波装置業界は、主に次のような定評ある企業によって牽引されています。

- GEヘルスケア(米国)

- フィリップス ヘルスケア(オランダ)

- シーメンス・ヘルシニアーズ(ドイツ)

- キヤノンメディカルシステムズ株式会社(日本)

- サムスンメディソン(韓国)

- 富士フイルムホールディングス株式会社(日本)

- ミンドレイ・メディカル・インターナショナル・リミテッド(中国)

- 日立製作所(日本)

- Esaote SpA(イタリア)

- コニカミノルタ株式会社(日本)

- ホロジック社(米国)

- ストライカー(米国)

- ソノサイト社(米国)

- アルピニオンメディカルシステムズ株式会社(韓国)

- BKメディカル(米国)

北米超音波機器市場の最新動向

- 2025年4月、北米の大手医療技術企業が、心臓画像の精度向上を目的としたAI搭載の新型超音波システムの発売を発表しました。このシステムは、自動駆出率測定とストレイン解析のための高度なアルゴリズムを統合し、心臓専門医の診断精度と効率性の向上を目指しています。

- 2025年2月、大手メーカーが、筋骨格系アプリケーション向けに画質を向上させた、コンパクトなワイヤレスハンドヘルド超音波装置のFDA承認を取得しました。この開発により、スポーツ傷害や整形外科疾患のPOC診断が大幅に向上すると期待されています。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。