北米超音波画像処理装置市場規模、株式および動向分析レポート

Market Size in USD Billion

CAGR :

%

USD

3.46 Billion

USD

5.64 Billion

2024

2032

USD

3.46 Billion

USD

5.64 Billion

2024

2032

| 2025 –2032 | |

| USD 3.46 Billion | |

| USD 5.64 Billion | |

| % | |

|

北米超音波イメージングデバイス市場セグメンテーション、Arrayフォーマット(Phased Array、リニアアレイ、カーブドリニアアレイ、その他)、デバイスディスプレイ(カラー超音波デバイスと黒と白(B/W)超音波デバイス)、デバイスポータビリティ(Trolley/Cart-Based Ultrasound Device、 Compact/Handheld Ultrasound Device、Stationary Ultrasound Device、Point-of-of-Care Ultrasound Device、Ultrasound Device)、Ultrasound Device、Ultrasound Division(Ultrasound Device)、Ultrasound Divisions、Ultrasound Divisions)、その他

北アメリカの超音波イメージ投射装置市場のサイズ

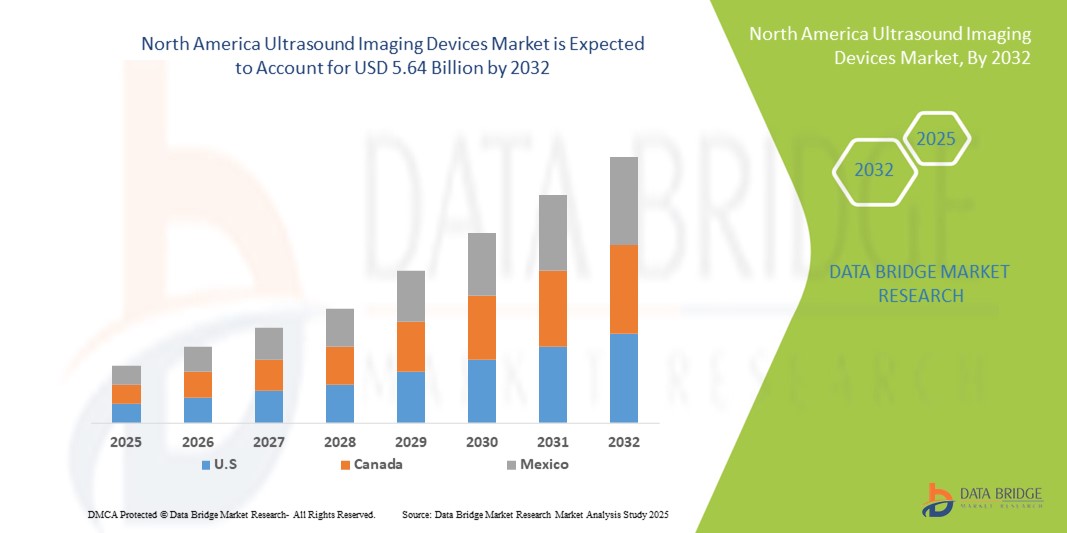

- 北米超音波画像処理装置市場規模は、2024年のUSD 3.46億そして到達する予定2032年までのUSD 5.64億, お問い合わせカリフォルニア 6.30%予報期間中

- 市場成長は、慢性疾患の増加の予防によって大きく燃料を供給され、胃の人口を増加させ、非侵襲的診断イメージングソリューションのための需要が高まっています 病院や診断センター

- また、ポータブル・ワイヤレス超音波装置、AI集積イメージングシステム、強化された3D/4Dイメージング機能などの技術進歩は、臨床・ポイントケアの設定における採用を推進しています。 これらの要因は、医療インフラの拡大と早期疾患の検出の意識の上昇と組み合わせて、超音波画像処理装置の蓄積を加速し、その結果、業界の成長を著しく向上しています

北米超音波イメージングデバイス市場分析

- 超音波イメージング装置は、広範囲の医療条件のための非侵襲的な診断イメージングを提供し、病院、診断センター、およびリアルタイムのイメージング機能、ポータビリティ、および安全プロファイルによるポイント・オブ・ケア施設全体の近代的な医療設定でますますます重要なツールです

- 超音波イメージング装置に対する高需要は、主に慢性疾患の有病率を高め、胃の人口を増加させ、非侵襲的および早期診断ソリューションへのシフト、AIアシストイメージング、ポータブルシステム、および強化された3D/4Dイメージングなどの技術の進歩によって駆動されます。

- 米国は、高度医療インフラ、革新的な医療技術の採用、および主要な市場プレーヤーの存在によって支えられた、2024年に79.5%の最大の収益分配で北アメリカ超音波イメージング装置市場を支配しました、そして携帯用およびポイント・オブ・ケアの超音波の配置の実質的な成長の大きい成長と、AI、無線接続およびミニチュア化されたイメージング システムに焦点を合わせる確立された医療機器会社およびスタートアップによって燃料を供給しました

- カナダは、ヘルスケア施設の拡大に伴い、北米超音波イメージング装置市場で最も急速に成長している国であると予想され、診断イメージングの採用のための政府の取り組みの増加、都市および農村地域の先進的なイメージング技術に対する需要の増加

- コンパクト/ハンドヘルド超音波デバイスセグメントは、2024年に約43.8%のシェアを持つ北アメリカ超音波イメージングデバイス市場を支配し、緊急ケア、外来診療所、および農村医療設定における使用、モビリティ、および成長の採用の容易さによって駆動しました

レポートスコープと北米超音波イメージングデバイス市場セグメント

| アトリビュート | 北アメリカの超音波イメージ投射装置の主要な市場洞察 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

北米超音波イメージングデバイス市場動向

AIと3D/4Dイメージングの統合による高度化

- 北アメリカの超音波画像処理装置市場の重要な加速傾向は統合です人工知能(AI)および高度3D/4Dのイメージング技術は、診断の正確さ、イメージの明快さおよびワークフローの効率を高めます、

- たとえば、Butterfly iQ+は、自動測定と画像の最適化のためのAIアルゴリズムを統合し、診断速度を改善し、オペレータの依存性を削減します。 同様に、GEヘルスケアのVolusonシリーズは、高解像3D / 4Dイメージングを提供し、閉塞および心血管用途

- 超音波システムにおけるAIの統合により、異常、予測診断、適応画像強化の自動検出などの機能が可能になります。 たとえば、Philips Lumify は、AI を使用して、ポイント・オブ・ケア・イメージングを支援し、臨床医にリアルタイムのガイダンスを提供し、臨床的意思決定を改善します。

- 病院のPACSシステムとクラウドベースのプラットフォームを備えた超音波デバイスのシームレスな統合により、集中的な画像管理を容易にし、複数の施設間でリモート・コンサルテーションとテレメディシン・サポートが可能

- よりインテリジェントで正確で、コネクテッドなイメージングシステムに対するこの傾向は、臨床的期待を再定義し、Canon Medical Systemsなどの自動車メーカーを運転し、自動化されたワークフローの支援や強化された3D/4D視覚化などの機能を備えたAI対応の超音波装置を開発しています。

- 臨床医がますます効率、正確さを優先し、改善された忍耐強い結果を改善するように、AI搭載の先進的なイメージング超音波装置に対する要求は、病院、診断センター、および外来クリニック間で急速に成長しています

北米超音波イメージングデバイス市場ダイナミクス

ドライバー

慢性疾患の蔓延および非侵襲的な診断による上昇の要求

- 慢性疾患の増大と非侵襲的、リアルタイム診断ソリューションのための成長の必要性は、北アメリカ超音波イメージングデバイス市場の主要なドライバです

- 例えば、2024年3月、Siemens Healthineersは心臓血管監視のためのAI高められた超音波のプラットホームを、早期病気の検出および臨床効率を改善することを目的とした導入しました

- ヘルスケアプロバイダーは早期診断と継続的な監視オプションを求めるため、超音波イメージングデバイスは、リアルタイムイメージング、ポータビリティ、安全性、非イオン化技術などの利点を提供します

- さらに、病院や外来診療所におけるポイント・オブ・ケアおよびベッドサイド超音波の採用は、現代の医療ワークフローに不可欠なこれらのデバイスを構成し、患者管理を強化し、診断遅延を軽減します

- ポータブル、ワイヤレス、AI統合型超音波システムに対する需要が高まっています。臨床医や患者の意識を高めることで、市場成長が著しく向上しています。

- 早期診断、患者中心ケア、および非侵襲的なイメージングソリューションに対する傾向は、病院グレードとポイントオブケア超音波デバイスの両方で革新するメーカーのための機会を拡大しています

拘束/チャレンジ

高コスト・規制コンプライアンスに関する懸念

- 高度な超音波イメージングシステム、特にAI対応および3D/4D機器の高コストは、ヘルスケア施設の幅広い採用に大きな課題を抱えています

- たとえば、GE HealthcareやPhilipsなどのブランドからハイエンドの超音波デバイスは、基本的なポータブルユニットよりも複数の時間を費やし、より小規模なクリニックや予算を意識したプロバイダのアクセシビリティを制限することができます。

- また、FDA及びその他の保健機関からの規制基準の遵守により、新製品の発売や開発コストの増大、新規参入者や革新的な技術のためのハードルの創出が可能

- 製造業者は、安全、イメージング、およびソフトウェア検証プロトコルの遵守を確実にしなければなりません。これにより、時間とリソース集中的、潜在的な市場成長を遅らせることができます。

- ポータブルおよびポイント・オブ・ケアの超音波システムの価格が次第に減少している間、高度AIおよびイメージ投射の特徴のための報酬は費用感受性のヘルスケアの区分の採用を制限し続けます

- コスト最適化、規制対応、およびAI支援機能の堅牢な検証を通じて、これらの課題を克服することは、北米超音波イメージングデバイス市場における持続的な成長にとって不可欠です。

北米超音波イメージングデバイス市場スコープ

市場は配列のフォーマット、装置の表示、装置可搬性、技術、適用、エンド ユーザーおよび配分チャネルに基づいて区分されます。

- 配列のフォーマットによって

配列のフォーマットに基づいて、北アメリカの超音波画像処理装置は段階的な配列、線形配列、曲げられた線形配列および他に分けられます。 フェーズドアレイセグメントは、2024年に最大の収益シェアで市場を支配し、心臓および血管イメージングで広く使用されている。 病院や心臓ケアユニットは、心臓などの移動構造の高解像度イメージングを提供するため、相続配列システムを好むことが多いです。 高度AIの統合および実時間イメージの処理は診断正確さおよび臨床効率を改善します。 セグメントは、複数のトランスデューサタイプとワークフロー自動化ツールとの互換性から恩恵を受けます。 緊急および重要なケア設定の需要を増加させ、市場優位性を強化し、ハイエンドのヘルスケア施設の好ましい選択をします。

線形配列の区分はmusculoskeletal、管の採用の増加によって燃料を供給される2025から2032への最も速い成長を目撃するために期待されます、および表面的なティッシュのイメージ投射。 線形配列の調査は浅い構造のための優秀な決断を提供しま、それらにoutpatientの医院およびポイント・オブ・ケアの塗布にとって理想的にします。 成長はまた携帯用および手持ち型の超音波システムによって運転されます、それは頻繁にそれらのコンパクト デザインのために線形調査を使用します。 整形外科、血管、および皮膚科のイメージングにおけるライジングの採用は、より速い拡張をサポートしています。 AIによる測定ツールとの統合により、診断の信頼性とワークフローの効率性を高めます。 線形配列装置の使用の多様性そして容易さはそれらをより小さいヘルスケア設備および移動式医学の単位に魅力的にします。

- 装置の表示による

装置の表示に基づいて、北アメリカの超音波イメージ投射装置市場は色の超音波装置および白(B/W)の超音波装置に分けられます。 超音波装置セグメントは、2024年に最大の市場収益シェアを保持し、血流と解剖構造を正確に視覚化する能力を強化しました。 病院および診断センターは心血管、閉塞および管の塗布のための色の超音波を好みます。 AIを用いたフロー解析と3D/4Dイメージング機能により、さらにカラー超音波システムの導入をサポートします。 より高い診断精度と広範囲の臨床ユーティリティは、現代のイメージング部門に不可欠です。 また、病院のPACSとテレメディシンプラットフォームとの統合にもメリットがあります。 カラーイメージングにおける継続的な技術進歩により、持続的な市場優位性を確保します。

B/W超音波装置セグメントは、2025年から2032年まで最速のCAGRを目撃する予定です。 B/W装置は費用効果が大きい、携帯用であり、基礎イメージ投射の必要性、特に農村のヘルスケアの設定のために適しています。 単純性と低いメンテナンス要件は、モバイル医療ユニットやポイントオブケア診断に最適です。 第一次ケアおよび緊急のシナリオで超音波のユーティリティの意識を高めることによって成長は更に運転されます。 B/Wデバイスは、重要な投資なしにイメージングサービスに拡大しようとするクリニックのエントリーポイントとしても機能します。 ハンドヘルドとコンパクトな超音波システムとの統合により、多様なケア設定における採用を強化します。

- デバイスポータビリティ

デバイスポータビリティに基づき、北米超音波イメージングデバイス市場は、トロリー/カートベース、コンパクト/ハンドヘルド、固定装置、ポイントオブケア超音波装置に分けられます。 コンパクト/ハンドヘルド超音波デバイスセグメントは、病院、緊急部門、外来診療所、およびリモートヘルスケア設定における採用の増加による43.8%の市場シェアで2024年に市場を支配しました。 これらのデバイスは、患者のベッドサイドでリアルタイムイメージングを提供し、集中型イメージング施設の依存性を減らし、診断ターンアラウンド時間を改善します。 高度なAI統合、ワイヤレス接続、クラウドベースのストレージにより、臨床ユーティリティが向上します。 これらのデバイスのポータビリティ、使いやすさ、コスト効率性は、幅広いヘルスケアプロバイダーに魅力的です。 継続的な革新とポイント・オブ・ケア診断の需要増加は、市場優位性を強化します。

トロリー/カートベースの超音波デバイスセグメントは、2025年から2032年までの最速の成長を目撃し、大規模な病院や診断センターで高性能な画像要件によって駆動されます。 これらのシステムは、心臓学、放射線学、および産科の包括的なワークフローに優先されます。 複数のトランスデューサーの両立性、大きい表示スクリーンおよび高度のイメージ投射機能は複雑な検査のためにそれらに適します。 病院や手術センターは、長期にわたる信頼性とPACSとの統合のために、これらのシステムに引き続き投資します。 さらなる成長は、AI対応のイメージングツールと自動測定により、臨床の効率性を高めています。 多専門部門の採用の増加により、セグメントの拡大が加速します。

- テクノロジー

技術に基づいて、北米超音波イメージング装置市場は、診断超音波および治療超音波に分けられます。 診断超音波セグメントは、心臓学、閉塞、放射線学、およびその他の特産品を渡る非侵襲的イメージングの需要を増加させ、2024年に支配しました。 病院およびイメージングセンターは、定期的な検査、高度な臨床応用、早期疾患検出のための診断装置に依存しています。 AI対応のイメージングソリューションは、精度を高め、オペレータの依存性を減らし、リアルタイム解析を容易にします。 病院情報システムとPACSとの統合により、臨床機能を強化 診断超音波装置の高い信頼性、安全および汎用性は彼らの市場のリーダーシップを維持します。 臨床医と非侵襲的イメージングの利点に関する患者の意識を高めることで、継続的な採用をサポートします。

治療用超音波セグメントは、2025年から2032年までの最速成長を目撃する予定で、理学療法、痛み管理、および標的薬の配信における適用を拡大することによって燃料を供給されます。 リハビリテーションや外来ケアセンターの採用の増加が要求されます。 集中された超音波療法の進歩はmusculoskeletalおよび柔らかいティッシュの無秩序のための精密な処置を可能にします。 クリニックやホームケア設定のポータブル治療システムの使用は、より速い市場成長をサポートしています。 超音波療法の継続的な革新と臨床受諾の増加は、セグメントの拡大に貢献します。 最小限の副作用による非侵襲的治療の可能性は、採用を促します。

- 用途別

アプリケーションに基づいて、北米超音波イメージングデバイス市場は、放射線学/一般イメージング、産科および婦人科、心血管、消化器、血管、泌尿器科、整形外科および筋骨格、疼痛管理、緊急部、クリティカルケアなどに分かれています。 放射線学/一般画像セグメントは、病院や診断センターを横断する定期的な診断および多臓器評価の広範な使用のために2024年に支配しました。 ラジオロジストは、汎用性、信頼性、および高度なイメージングワークフローとの統合のためにこれらのデバイスを好む。 高い忍耐強いスループットおよび正確な診断のための必要性は区分の優位性を補強します。 AIによるイメージングとクラウドベースのソリューションにより、ワークフローの効率化を実現します。 継続的な技術革新と早期疾患検出のための需要は、市場リーダーシップを強化します。.

緊急部門は、2025年から2032年までの最も速い成長を目撃し、外傷、心臓のでき事および重大な心配の状態の急速な診断のためのポイント・オブ・ケアおよび携帯用超音波システムの使用の増加によって運転されると期待されます。 AI対応のイメージングにより、時間感度の高いシナリオで自動測定と意思決定をサポートします。 ハンドヘルドデバイスとモバイルカートとの統合により、ベッドサイド診断が容易になります。 重要なケアユニットの採用と予備病院の設定でさらなる燃料成長を促進します。 政府のイニシアチブや病院の投資から緊急ケア能力を向上させるセグメントの利点。 ポータブル、高速、および正確なイメージングソリューションは、このセグメントの急速な市場拡大を促進します。

- エンドユーザーによる

エンドユーザーに基づいて、北米超音波イメージングデバイス市場は、病院、手術センター、研究およびアカデミー、マタニティセンター、アンブレーサーケアセンター、診断センター、その他に分けられます。 病院の区分は2024年に、高度の忍耐強い流出、高度のイメージ投射の条件および最新式の超音波システムへの投資によって支えました。 病院は複数の部門の適用のための統合された、AI によってアシストされる超音波装置を好む。 大量のイメージングワークフローを管理する能力は、市場優位性を高めます。 大規模な医療施設は、PACSおよび医療プラットフォームとの統合にも役立ちます。 継続的な交換サイクルと病院のアップグレードは、収益成長を維持します。

2025年から2032年までの最も速い成長を目撃するために、血管内科のクリニックや診断センターが急速で費用対効果が大きい、非侵襲的なイメージングソリューションに焦点を当てた増加数で燃料を供給する、血管内ケアセンターのセグメントが期待されています。 これらのセンターは、ポータブルでコンパクトなデバイスを採用し、効率的な診断を実現します。 テレメディシンの採用とAI対応のイメージングツールにより、さらなる成長をサポートします。ポイントオブケア超音波ソリューションは、患者のスループットと満足度を向上させます。 病院と比較して投資要件を下げると、アンブレーラセンターはメーカーにとって魅力的なターゲットになります。 ヘルスケアの分散化と外来ケアの需要増加によるセグメントメリット

- 流通チャネル

配布チャネルに基づいて、北米超音波イメージングデバイス市場は、直接入札、サードパーティのディストリビューター、および小売販売に分けられます。 直接入札セグメントは、病院、政府機関、および大規模な診断チェーンによるバルク調達によって運転され、コスト効率、サービス契約、および長期的なサポートを確実にするために2024年に市場を支配しました。 大規模な医療施設は、多くの場合、デバイスカスタマイズ、トレーニング、メンテナンス契約の直接調達を好む。 このチャネルは供給の信頼性そして継続を保障します。 病院ネットワークとPACSとの統合も、直接入札契約により容易になります。 価値の高い契約と政府の取り組みは、さらなる優位性を強化します。

サードパーティのディストリビューターのセグメントは、2025年から2032年まで最速のCAGRを目撃し、メーカーと地域のディストリビューター間のパートナーシップを強化し、より小規模なクリニック、農村医療施設、新興医療センターでの市場進出を拡大する見込みです。 ディストリビューターヘルプメーカーは、ローカライズされたサポート、トレーニング、メンテナンスサービスを提供しています。 tier-2 および tier-3 の都市の拡大はこのチャネルを通して採用を運転します。 ディストリビューターとのパートナーシップにより、新規プレイヤーのエントリー障壁が減少します。 小さなクリニックの中で超音波ユーティリティの意識を高め、成長を加速します。 柔軟な調達オプションとアフターサービスの改善によるセグメントメリット

北米超音波イメージングデバイス市場地域分析

- 米国は、先進医療インフラ、革新的な医療技術の採用、および主要な市場プレーヤーの存在によって支えられた2024年に79.5%の最大の収益分配を持つ北アメリカ超音波イメージングデバイス市場を支配しました

- 地域におけるヘルスケアプロバイダーは、病院PACS、AI支援ツール、およびポイント・オブ・ケア診断用のポータブルシステムを備えた超音波機器の精度、リアルタイムイメージング機能、および統合を高く評価しています。

- 高度医療インフラ、医療技術の高投資、および主要な企業のプレーヤーの強い存在によって、超音のイメージ投射装置を病院、診断センターおよび外来の心配設備を渡る好まれた選択として確立するこの広範な採用は更に支えられます

米国超音波イメージングデバイス市場インサイト

米国超音波イメージングデバイス市場は、北米で2024年に最大の収益シェアをキャプチャし、慢性疾患の増大と非侵襲的診断ソリューションの需要の増加によって燃料を供給しました。 病院および診断センターは改善された臨床効率のための携帯用、手持ち型およびAIによって統合される装置を含む高度の超音波システムの採用を、優先します。 3D/4Dイメージングやリアルタイム分析、市場成長などの技術革新と相まって、ポイント・オブ・ケア・イメージングのトレンドが高まっています。 また、医療インフラを支える政府の取り組みや、臨床医のヘルスケアの普及や認知度を高め、市場拡大に大きく貢献しています。

カナダ超音波イメージングデバイス市場情報

カナダの超音波画像処理装置市場は、主にヘルスケアインフラへの投資の増加と高度な診断イメージングの需要の増加によって駆動、予測期間中に実質的なCAGRで成長するために計画されています。 政府の払い戻し方針と組み合わされ、国の発達した医療システムが、病院、出産センター、外来診療所における超音波システムの採用を促進します。 カナダのヘルスケアプロバイダーは、AI対応とポータブル超音波デバイスを統合し、診断精度とワークフローの効率性を高めています。 また、早期病態の検出に関する高齢化人口や高齢化の意識が高まっています。

メキシコ超音波イメージングデバイス市場洞察

メキシコの超音波イメージングデバイス市場は、予測期間中に注目すべきCAGRで成長することを期待しています, 増加する医療意識と都市および半都市地域の診断施設の拡大によって駆動. 慢性疾患および母体の健康監視の要件の普及は、超音波イメージングシステムの導入を促進しています。 政府の取り組みにより、診断サービスや医療のアクセシビリティを改善し、市場成長をさらに支援しています。 ポータブルおよびポイント・オブ・ケア装置の統合は、タイムリーな診断を提供するためにますます一般的になっています。 メキシコの民間医療分野は、市場拡大にも大きく貢献しています。

北米超音波イメージングデバイス市場シェア

北アメリカの超音波イメージ投射装置工業は主に下記のものを含んでいる十分に確立された会社によって、導きます:

- GE HealthCare(アメリカ)

- Koninklijke フィリップス N.V. (米国)

- サムスンヘルスケア(韓国)

- テラソン(アメリカ)

- オトネクサスメディカルテクノロジーズ株式会社(米国)

- ボストンイメージング(米国)

- Medtronic(アイルランド)

- Aidoc.(イスラエル)

- 株式会社アクミン(カナダ)

- アメテック株式会社(米国)

- Sofwave Medical Ltd.(イスラエル)

- カプサヘルスケア(米国)

- NAIイメージングシステムズ株式会社(米国)

- Avante Health Solutions(米国)

- 株式会社ホロジック(米国)

- キャノンメディカルシステムズ株式会社(米国)

- 日立ハイテック株式会社(米国)

- シンセンMindrayの生物医学の電子工学Co.、株式会社(中国)

- Esaote SPA(アメリカ)

北米超音波イメージングデバイス市場における最近の発展は何ですか?

- 2025年8月、GE HealthCareは、Vvidのパイオニア、最も先進的な心臓血管超音波システムを導入し、2D、4D、およびカラーフローのイメージングで臨床医を支援しました。 ワークフローを合理化し、診断の自信を高める

- 2025年8月、Esaote North AmericaとEpica Internationalは、米国病院および専門慣行の広範な拠点に到達することを目指し、ヒトおよび獣医MRIおよび超音波システムのポートフォリオを拡大するための戦略的パートナーシップを発表しました

- 2025年7月、MAUI Imagingは、骨、ガス、脂肪、手術工具などの障壁を視覚化することができる超音波技術を進めるために、シリーズDの資金調達で14百万米ドルを調達しました。 会社は、特に外傷のシナリオで診断イメージングを高めることを目指しています

- 2025年5月、心臓不整脈治療のグローバルリーダーであるジョンソン&ジョンソン・メドテックは、心臓血管疾患(ICE)画像処理のためのSOUNDSTAR CRYSTAL超音波カテーテルの米国発売を発表

- 2024年12月には、AIを活用した健康情報とRadNet社の完全子会社であるシーメンス・ヘルスケア社とDeepHealth社のグローバルリーダーであるDeepHealth社が、ワークフローやイメージング・ハードウェアにおけるAIを活用した健康情報の提供を通じて、超音波操作の変革に向けた戦略的コラボレーションを発表しました。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。