北米インビトロ毒性試験市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

5.42 Billion

USD

15.46 Billion

2024

2032

USD

5.42 Billion

USD

15.46 Billion

2024

2032

| 2025 –2032 | |

| USD 5.42 Billion | |

| USD 15.46 Billion | |

| % | |

|

北アメリカの生態学のテストの市場セグメンテーション、プロダクトおよびサービス(消費財、サービス、試金、装置およびソフトウェア)によって、毒性学の終点およびテスト(ADME (吸収、配分、メタボリズム、及び排出)のテスト、Cytotoxicityのテスト、Genotoxicityのテスト、皮膚毒性のテスト、Ocular Toxicityのテスト、Organ Tocityのテスト、皮のIrritation、腐食、感度テストおよび分子検査(分析、分析、分析、分析、分析、分析、分析、分析、分析、分析、分析、分析、分析)。バイオ医薬品企業、診断、食糧、化学薬品、化粧品& 家庭用製品)、流通チャネル(直接入札、小売販売、その他) - 業界動向と予測 2032

北アメリカのIn-Vitroの毒性学のテストの市場のサイズ

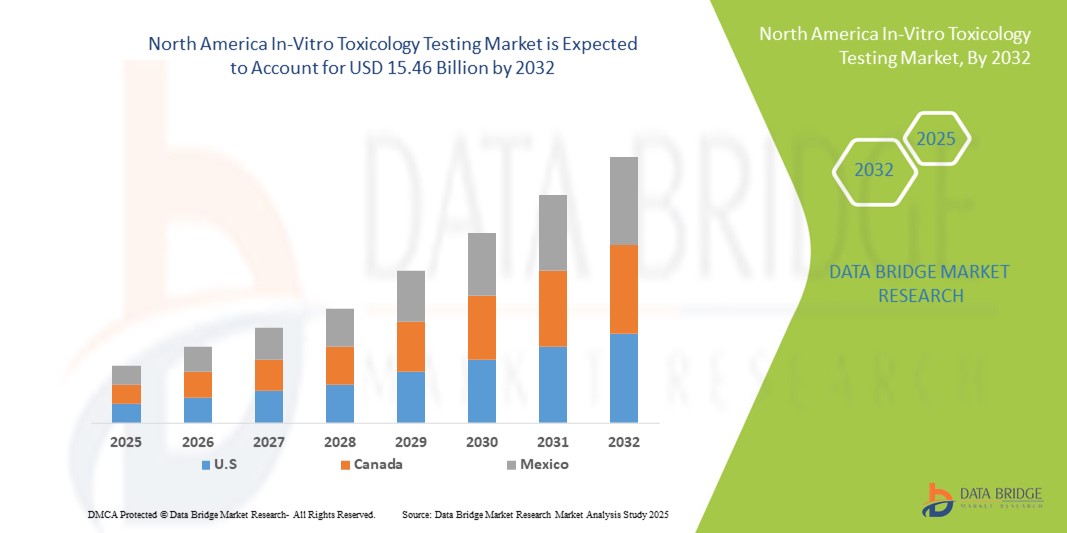

- 北アメリカのinvitroの毒性学のテストの市場のサイズはで評価されました2024年のUSD 5.42億そして到達する予定2032年までに15.46億米ドル, お問い合わせ14.00%のCAGR予報期間中

- 市場成長は、細胞培養技術の進歩、高スループットスクリーニング、予測毒性学モデルによって駆動される、in-vitro毒性試験ソリューション内の成長した採用と技術の進歩によって主に燃料を供給されます。 これらのイノベーションは、動物研究の依存性を減らし、医薬品およびバイオテクノロジー分野における医薬品開発のタイムラインを加速するテスト精度を強化しています。

- さらに、医薬品、化粧品、化学工業の需要増加と組み合わせて、代替試験方法の規制対応を強化し、信頼性、倫理的、費用対効果の高いソリューションとして、in-vitro毒性試験を確立しています。 これらの結合因子は、ウイルス毒性試験ソリューションの摂取量を加速し、その結果、業界の成長を著しく向上しています

北米インビトロ毒性試験市場分析

- 人体外に化学物質、薬および他の物質の安全性と潜在的な毒性を評価することを含むin-vitro毒性試験は、動物実験の信頼性を低下させ、精度を高め、規制遵守を改善するために、現代の医薬品開発と化学安全評価の重要な成分となっています

- ウイルス毒性試験の需要は、主に規制圧力を増加させ、医薬品の動物検査、研究開発活動の上昇を最小限にし、迅速で費用対効果の高いテストソリューションのための成長の必要性

- 米国は、2024年に最大87.53%の収益シェアを誇るベンチャー内毒性試験市場を支配し、先進医療インフラ、強力な政府の取り組み、医薬品およびバイオテクノロジー企業の存在を支持しました。 また、堅牢な規制枠組みや、セルベースのアッセイ、高スループットスクリーニング、およびオーガン・オン・チップ技術による継続的な技術進歩により、市場規模の拡大を促進

- カナダは、予測期間中に、子宮内毒性試験市場で最も急速に成長している国であることが期待され、ヘルスケア投資を増加させ、先進的なテスト技術の導入、および動物実験の代替を促進する政府の取り組みの増加が増加しています。 医薬品研究の分野を拡大し、学術機関と業界関係者の連携が高まっています。

- 医薬品・バイオ医薬品事業会社セグメント北アメリカのinvitroの毒性学のテストの市場を支配しました2024年の45.8%の市場収益シェア、非法的な薬物検査の大量に燃料を供給し、規制安全基準の順守の必要性、および先進の非vitro毒性プラットフォームの採用

レポートスコープとインビトロ毒性試験市場セグメンテーション

| アトリビュート | In-Vitro毒性学テストキー市場洞察 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

北アメリカのIn-Vitroの毒性学のテストの市場の傾向

高度のテスト プラットホームによる高められた便利

- 北米内毒性試験市場での有意で加速傾向は、先進的な高スループットスクリーニング(HTS)プラットフォームおよび自動テスト技術の導入です。 これらのイノベーションは、毒性のワークフローを合理化し、手動介入を減らし、より迅速で信頼性の高い結果を提供します。

- たとえば、従来の2D文化よりも、人体生理学を的確に再現し、毒性評価の予測値を高める3D細胞培養技術を導入しています。 同様に、microfluidicベースのシステムは、再現性とスケーラビリティを向上させるために、毒性試験ワークフローに統合されています

- ウイルス毒性試験の自動化により、ラボでは、バリビリティとエラーを最小限に抑えながら、大量のサンプルボリュームを処理することができます。 たとえば、複数の新しいシステムでは、自動液体処理、高度なイメージング、および統合データ分析を可能にし、医薬品と化学安全テストの両方のスループットと効率を大幅に改善

- さらに、先進的なイメージング技術やAIを活用した分析(消費者向けアプリケーションではなく、毒性データセットに特化)を組み込むことで、研究者が細胞の反応、バイオマーカー、線量応答関係に深い洞察を得ることができます。 これは、より包括的な毒性プロファイルを高精度で配信するのに役立ちます

- ラボ情報管理システム(LIMS)を備えた、非vitro 毒性プラットフォームのシームレスな統合により、集中化されたデータ収集、規制遵守、およびリサーチセンターおよび製薬会社全体の標準化レポートを容易にします。 1つのインターフェイスを通して、研究所は他の研究開発活動と共にテスト プロセスを管理し、薬物発見および化学安全評価のための統一されたワークフローを作成できます

- より高度化、自動化、および生物学的に関連した毒性試験システムに対するこの傾向は、医薬品開発および化学安全評価における期待を根本的に再構築しています。 その結果、Eurofins ScientificやCharles River Laboratoriesなどの企業は、高度のin-vitroモデルに大きく投資し、正確で倫理的、スケーラブルな毒性学ソリューションの需要に応える

- 高度のin-vitroの毒性試験プラットフォームの需要は、予測精度、コスト効率を優先し、進化する規制枠組みとの整合性における動物実験の信頼性を削減する組織として、医薬品とバイオテクノロジーの両方の分野で急速に成長しています

北アメリカのIn-Vitroの毒性学のテスト マーケットの動的

ドライバー

安全上の懸念と規制の遵守による成長の必要性

- ヒトの安全性、動物検査に関する倫理的問題、および化学物質および医薬品検査の厳しいグローバル規制に対する懸念の増加は、In-Vitro Toxicology Testingの要求を満たす主要な要因です。

- たとえば、2024年4月、Charles River Laboratoriesは、高度な3D細胞培養モデルを安全性試験ポートフォリオに統合することにより、そのウイルス毒性能力の拡大を発表しました。 大手企業によるそのような戦略的取り組みは、予測期間中にイン・ビトロ毒性検査市場の成長を加速することが期待されています

- 業界、特に医薬品、バイオテクノロジー、および化学物質として、表面強化された規制スカルチニ、in-vitroテスト方法は、伝統的な動物研究に科学的に堅牢で倫理的に健全な代替手段を提供します。 これらの方法は、研究における動物使用を減らすためのグローバルな努力と整合しながら、正確な毒性データを提供します

- さらに、臓器オンチッププラットフォーム、幹細胞由来モデル、自動高スループットスクリーニングシステムなどの先端技術の高度化が、現代の安全評価枠の中央コンポーネントを実証しています。

- より速い結果、より大きい再現性、およびより多くの人間関連性データを提供するためにinvitroの毒性学のプラットホームの能力は薬物開発、化学安全評価および化粧品のテストのための必要な用具としてそれらを置きます。 また、費用対効果の高い、倫理的、効率的なソリューションの需要の高まりは、開発および新興市場での採用を拡大し続けています。

拘束/チャレンジ

コスト・技術制限に関する懸念

- 彼らの成長している人気にもかかわらず、in-vitro毒性法は、高度なテストプラットフォームと特定の技術的な制限の高いコストに関連する課題に直面しています。 3D臓器モデルやマイクロ流体デバイスなどの革新的なシステムが価値あるインサイトを提供しますが、その採用は、特に小規模な研究施設やコスト感度の高い市場において、重要な先行投資要件によって妨げられます。

- たとえば、in-vitroモデルが強力な予測値を提供しているが、高プロファイルの研究では、彼らはまだ完全に組織全体の応答の複雑さを再現することはできません。特定のケースで補完的なテスト方法と一緒に使用する必要があります

- さらなる技術革新、より広範な標準化、および規制の受諾を通じて、これらの制限に対処することは、in-vitroメソッドの自信を高めるために不可欠です。 ユーロフィンズ科学とラボコープなどの企業は、コストバリアを削減するために、新しい試金を有効活用し、手頃な価格のテストサービスを拡張するために積極的に取り組んでいます

- また、機器、消耗品、専門的専門知識に必要な高い投資は、開発地域における採用を開示することができます。 技術の進歩により、コストが徐々に低下する一方で、プレミアムサービスとしてのウイルス毒性の認識は、低所得市場での浸透を遅らせる可能性があります。

- 業界のコラボレーション、トレーニングのイニシアチブ、および継続的なイノベーションを通じたこれらの課題を克服することは、持続可能な成長と世界的なインビトロ毒性試験の受け入れを確保することが重要となります

北アメリカのIn-Vitroの毒性学のテストの市場規模

市場はプロダクトおよびサービス、毒性学の終点およびテスト、技術、方法、企業および配分チャネルに基づいて区分されます。

- 製品・サービス

製品およびサービスに基づいて、北アメリカのinvitroの毒性検査の市場は消耗品、サービス、試金、装置およびソフトウェアに分けられます。 消耗部品セグメントは、2024年に最大39.5%の市場収益シェアを占め、試薬、キット、および文化媒体の定期的な毒性試験ワークフローに対する再発要求によって駆動しました。 消耗品は、日々の研究室の業務に不可欠であり、サプライヤーにとって一貫した収益源となっています。 再現性、精度、納期の短縮に重点を置き、医薬品、バイオテクノロジー、化学業界における高品質の消耗品の需要が高まっています。 また、臓器毒性などの複雑な毒性エンドポイントのための高度な3D細胞培養消耗品および専門アッセイキットの上昇使用は、このセグメントの優位性を強化しています。 消耗品の新製品の発売と継続的な革新により、セグメントは市場の角質を維持します。

ソフトウェアセグメントは、2025年から2032年までの12.8%の最速のCAGRを目撃し、データ分析、予測モデリング、および毒性試験における規制遵守のためのデジタルプラットフォームの採用の増加によって推進されています。 研究者は、高スループットスクリーニング、OMICS技術、およびサイリコモデルの複雑なデータセットを統合し、意思決定を加速し、実験的なエラーを減らすことができます。 正確なドキュメンテーションのための規制要件を成長させ、医薬品開発における高度な予測分析の必要性は、ソフトウェアの採用を強化しています。 クラウドベースのプラットフォームとAI対応ツールは、毒性学研究のためのスケーラブルで自動化された、そして協調的なソリューションを提供することで、さらに効率性を高めています。 研究所がデジタルトランスフォーメーションに向けて進むにつれて、ソフトウェアセグメントは急速に拡大し、全体的なテストエコシステムを再構築することが期待されます。

- 毒性学エンドポイントと テスト

毒性学の終点およびテストに基づいて、北アメリカのinvitroの毒性学のテストの市場はADME (吸収、配分、Metabolism及び排泄)のテスト、cytotoxicityのテスト、genotoxicityのテスト、皮膚毒性のテスト、ocularの毒性テスト、器官の毒性テスト、皮の苛立ち、腐食及び感度テスト、光毒性テストおよび他のエンドポイントテストに分けられます。 ADMEテストセグメントは、2024年に41.2%の最大の市場収益シェアを占め、前臨床開発における薬物動態プロファイルの評価に重要な役割を果たしました。 ADMEの研究は、規制の提出のためにピボタルである吸収効率、バイオアベイラビリティ、代謝安定性、および除去経路に重要な洞察を提供します。 高スループットのスクリーニングプラットフォーム、自動化、および予測モデルの採用がさらに強化されました。 医薬品およびバイオ医薬品会社は、開発サイクルで早期に薬の候補を削減し、早期に薬の候補を最適化するためにADMEテストにますます頼っています。 microfluidicシステム、3D肝モデルおよび共同培養アッセイの継続的な改善により、ADMEテストの精度とスループットが向上しました。

細胞毒性試験セグメントは、2025年から2032年までの13.4%の最速のCAGRを目撃すると予想され、新しい化学組織、生物学的、化粧品原料の安全評価に重点を置いています。 Cytotoxicityアッセイは、毒性化合物の早期識別を可能にし、臨床試験における副作用のリスクを最小限に抑えます。 契約研究機関(CRO)や規制機関から規格化・再現性シート毒性データに対する需要の増加が加速する。 自動イメージングシステム、高コンテンツスクリーニング、および3D細胞培養モデルの採用は、細胞毒性アッセイの範囲と信頼性を拡大しています。 また、動物実験を3R(置換、減衰、精製)ラインで削減する規制の奨励は、ウイルス性膀胱毒性プラットフォームの採用を推進しています。

- テクノロジー

テクノロジーをベースに、北米における毒性試験市場は、細胞培養技術、高スループット技術、分子イメージング、OMICS技術に分けられます。 細胞培養技術セグメントは、2024年に38.7%の最大の市場収益シェアを占め、予測毒性試験および薬物安全評価における幅広い用途に匹敵しました。 2Dおよび3D細胞培養モデル、臓器オンチップおよび球状培養を含む、臓器固有の毒性、細胞毒性、および機械的研究を評価するために広く使用されています。 セグメントは、パーソナライズされた医薬品への傾向の増加、アッセイの再現性の向上、および動物実験の減少に寄与します。 特殊な細胞ライン、共同培養システム、および血清フリーメディアの可用性の向上により、高度な細胞培養技術が求められます。

OMICS技術セグメントは、毒性の分子バイオマーカーを識別するために、ゲノム、プロテオミクス、およびメタボロミクスプラットフォームの拡大使用によって駆動され、2025年から2032年までの最も速いCAGRを目撃する予定です。 OMICSは、分子レベルでの薬物効果の包括的なプロファイリングを可能にし、予測精度と安全評価を強化します。 製薬会社は、前臨床的研究を加速し、厳格な規制基準を満たすため、バイオトロモデルでOMICSデータをます統合しています。 次世代シーケンシング、質量分析、バイオインフォマティクスの技術開発は、医薬品、化学、化粧品業界におけるOMICS技術の採用を拡大しています。

- 方法によって

方法に基づいて、北アメリカのinvitroの毒性試験市場は細胞アッセイ、生化学アッセイ、ex-vivoモデルおよびsilicoモデルに分けられます。 セルラーアッセイセグメントは、2024年に42.5%の最大の市場収益シェアを占め、細胞の生存性、細胞毒性、臓器特異的な毒性、および薬理的反応を評価するための広範な適用性による。 セルラーアッセイは、より速いターンアラウンド、再現性、高スループットスクリーニングとの互換性を提供するため、広く好まれています。 動物実験を置き換える規制圧力が増加し、人間関連モデルの採用がこのセグメントをさらに推進しています。 高度なイメージング、自動解析、および3D細胞培養技術は、効率性と精度を発揮します。

2025年から2032年にかけて最も速いCAGRを目撃するシリコモデルセグメントは、計算的な毒性と予測モデリングによって駆動されます。 silico では、毒性リスクの評価、オフターゲット効果の特定、実験コストの削減に役立ちます。 セグメントは、AI主導の予測アルゴリズム、機械学習統合、および代替テスト戦略のための規制サポートから恩恵を受けています。 これらのモデルは実験的なデータを補完し、動物実験に関する信頼性の早期意思決定と削減を可能にします。 また、公共の毒性データベースやオープンソースモデリングツールの普及可能性が高まっています。 ソフトウェア開発者、研究機関、規制機関とのコラボレーションを強化し、モデルの精度と規制当局の受け入れを強化しています。

- 業界別

業界に基づいて、北アメリカのinvitroの毒性検査の市場は医薬品及びバイオ医薬品会社、診断、食品、化学物質、化粧品および家庭用製品に分けられます。 医薬品およびバイオ医薬品会社セグメントは、2024年に45.8%の最大の市場収益シェアを占め、前処理薬試験の大量処理、規制安全基準の順守の必要性、および先進のウイルス毒性プラットフォームの採用によって燃料を供給しました。 これらの会社は、潜伏障害の可能性を削減しながら、自分の薬候補の安全性と有効性プロファイルを強化するために、in-vitroテストを利用しています。 高スループットスクリーニング、オーガナオンチップモデル、自動プラットフォームを統合する傾向は、セグメントの優位性を強化しています。

化粧品および家庭用製品セグメントは、2025から2032までの最速のCAGRを目撃し、規制の義務によって運転され、動物実験を削減し、より安全な消費者製品に対する需要の増加を期待しています。 企業はますます国際安全規格に従うためにinvitroのcytotoxicity、genotoxicityおよび皮の感受性の試金を採用します。 3Dの皮膚モデル、再建されたヒトの表皮およびorganotypicの試金の技術革新はこのセクターの急速な成長を支えます。 また、残酷フリーで環境に優しい製品に対する消費者の嗜好が高まっています。 化粧品メーカー、バイオテクノロジー会社、規制機関とのコラボレーションは、試金精度を高め、製品テストのタイムラインを加速しています。

- 流通チャネル

配布チャネルに基づいて、北米のinvitro毒性試験市場は、直接入札、小売販売などに分かれています。 直接入札セグメントは、2024年に41.3%の最大の市場収益シェアを支配し、医薬品およびバイオテクノロジー企業が定期的な毒性試験を実施しました。 サプライヤーとの長期契約は、一貫した品質、納期厳守、規制基準の遵守を保証します。 直接入札契約は、組織が価格交渉、運用コストの削減、および消耗品、機器、ソフトウェアの信頼できるサプライチェーンの確保を可能にします。

小売販売部門は、2025年から2032年の最も速いCAGRを目撃し、小規模なラボ、学術研究機関、およびキット、試薬、および小規模な機器の個々の購入を必要とする契約研究機関の需要の増加によって燃料を供給することが期待されます。 スタートアップ・リサーチ・センター・専門ラボは、小売チャネルを通じた成長をサポートし、小規模な運用に柔軟かつ利便性をもたらします。 また、eコマースプラットフォームやオンラインサイエンスマーケットプレイスの上昇は、重要な消耗品や機器への容易なアクセスを促進しています。 小売業者が提供するアフターサポート、トレーニング、およびバンドルされたソリューションを強化し、より小規模な機関間のさらなるドライブ導入を実現します。

北アメリカのIn-Vitroの毒性学のテストの市場地域分析

- 米国は、2024年に最大87.53%の収益シェアを誇るベンチャー内毒性試験市場を支配し、先進医療インフラ、強力な政府の取り組み、医薬品およびバイオテクノロジー企業の存在を支持しました。 また、堅牢な規制枠組みや、セルベースのアッセイ、高スループットスクリーニング、およびオーガン・オン・チップ技術による継続的な技術進歩により、市場規模の拡大を促進

- カナダは、予測期間中に、子宮内毒性試験市場で最も急速に成長している国であることが期待され、ヘルスケア投資を増加させ、先進的なテスト技術の導入、および動物実験の代替を促進する政府の取り組みの増加が増加しています。 医薬品研究の分野を拡大し、学術機関と業界関係者の連携が高まっています。

U.S. In-Vitro毒性試験市場洞察

米国内毒性試験市場は、2024年に最大87.53%の収益分配で、先進医療インフラ、強力な政府の取り組み、および主要な医薬品およびバイオテクノロジー企業の存在によって支持され、ウイルス毒性試験市場を支配しました。 国は、細胞ベースのアッセイ、高スループットスクリーニング、および分子イメージングプラットフォームを含む技術革新の最前線にあり、有意に毒性学研究を強化しています。 また、医薬品の発見、厳格な規制要件への投資の増加、およびより予測モデルで動物実験を交換することに対する成長の重点は、市場成長を促進しています。 これらの要因は、北米市場での明確なリーダーとして米国を集約的に確立します。

カナダ In-Vitro毒性学試験市場 Insight

カナダのin-vitro毒性試験市場は、予測期間中にIn-Vitro毒性検査市場で最も急速に成長している国であることが期待され、ヘルスケア投資の増加と動物実験に対する倫理的で持続可能な選択肢を促進する政府の取り組みが主導しています。 医薬品研究分野を拡充し、生体モデル、シリコ法、臓器毒性試験などの先端技術の普及が著しい機会を創出しています。 大学、研究機関、民間企業とのコラボレーションにより、イノベーションをさらに支援し、支持的な規制枠組みが近代的な試験モデルへの移行を強化しています。 これらのダイナミクスは、北米における高機能成長市場としてカナダに位置します。

北米 In-Vitro毒性試験市場シェア

In-vitro の毒性学のテストの企業は主に下記のものを含む十分に確立された会社によって、導きます:

- サーモフィッシャーサイエンス株式会社(米国)

- Labcorp(アメリカ)

- メルク・カーガ(ドイツ)

- チャールズ・リバー研究所(米国)

- ロンザ(スイス)

- バイオロード研究所(米国)

- 株式会社カタレント(米国)

- SGS Société Générale de Surveillance SA(スイス)

- インターテックグループ plc(イギリス)

- ユーロフィンズ科学(Luxembourg)

- 株式会社プロメガ(米国)

- アラーゲンライフサイエンス株式会社(インド)

- Cyprotex Plc(イギリス)

- 上海メディシロン株式会社(中国)

- クリエイティブ・バイオラボ(米国)

- BioIVT(米国)

- AATバイオクエスト株式会社(米国)

- Gentronix(イギリス)

- IONTOX(アメリカ)

- InSphero (スイス)

- MB研究機関(米国)

- クリエイティブ・バイオアレイ(米国)

- 優先セルシステム(米国)

北アメリカのIn-Vitroの毒性学のテスト マーケットの最も最近の開発

- 2023年3月には、実験機器や試薬のリーディングプロバイダであるサーモフィッシャー科学株式会社が、新たな高スループットのインvitro毒性試験プラットフォームの発売を発表しました。 このプラットフォームは、高度な細胞培養技術と自動スクリーニング機能を統合し、研究者がより効率的かつ正確に潜在的な毒性効果を評価することを可能にします。 打ち上げは、サーモフィッシャーが、薬物開発における規制遵守をサポートし、in-vitro毒性試験方法論を強化するためのコミットメントを強調

- 2024年6月、チャールズ・リバー・ラボラトリーズ(Charles River Laboratories)は、著名な契約研究機関であるチャールズ・リバー・ラボラトリーズ(Charles River Laboratories)が、そのイン・ビトロ・毒性試験サービスを拡大し、ダーマおよびオキュラ・毒性に焦点を当てた新しいアッセイのスイートを導入しました。 これらの試金は再建された人間の上皮および皮および目の刺激の可能性のより正確な予測を提供するために皮および皮モデルを利用します。 拡大は、動物モデルの信頼性を低下させ、世界的な規制動向と整列する代替試験方法に対する成長した需要を満たすことを目指しています

- 2024年9月、ラボコープ医薬品開発は、先進の3D細胞培養モデルに加え、その強化されたin-vitro毒性試験能力を発表しました。 これらのモデルは、特に臓器固有の効果のコンテキストで、薬物誘発毒性を評価するためのより生理学的に関連した環境を提供します。 3D細胞培養システムの統合により、Labcorpの最先端ソリューションを提供し、毒性評価の予測可能性と関連性を向上させる

- 2024年12月、ライフサイエンス研究と臨床診断のグローバルリーダーであるBio-Rad Laboratoriesは、高スループットスクリーニングアプリケーション用に設計されたin-vitro毒性試験キットの新しいラインを開始しました。 これらのキットは、膀胱毒性と性毒性を検出し、迅速かつ信頼性の高い毒性評価を促進するために、蛍光ベースのアッセイを組み込んでいます。 これらのキットの導入は、テストの効率を高めながら、厳しい安全基準を満たした医薬品および化粧品業界をサポートすることを目指しています

- 2025年2月、ドイツ・ダームシュタット(Merck KGaA)は、米国に拠点を置くバイオテクノロジー社との戦略的パートナーシップを発表しました。 コラボレーションは、より包括的かつ予測的な毒性データを提供するために、先進的なinvitroモデルとオミクス技術の統合に焦点を当てています。 このパートナーシップは、革新とコラボレーションによるin-vitro毒性試験の分野を発展させるためにメルクKGaAのコミットメントを強調しています

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。