Global Embedded Die Packaging Technology Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

143.53 Million

USD

166.98 Million

2025

2033

USD

143.53 Million

USD

166.98 Million

2025

2033

| 2026 –2033 | |

| USD 143.53 Million | |

| USD 166.98 Million | |

| % | |

|

Global Embedded Die Packaging Technology Market Segmentation, By Platform (Embedded Die in IC Package Substrate, Embedded Die in Rigid Board, and Embedded Die in Flexible Board), Technology (Medical Wearable Devices, Medical implants, Sports/Fitness Devices, Military, Industrial Sensing, and Others), Industry Vertical (Consumer Electronics, IT and Telecommunications, Automotive, Healthcare, and Others)- Industry Trends and Forecast to 2033

Embedded Die Packaging Technology Market Size

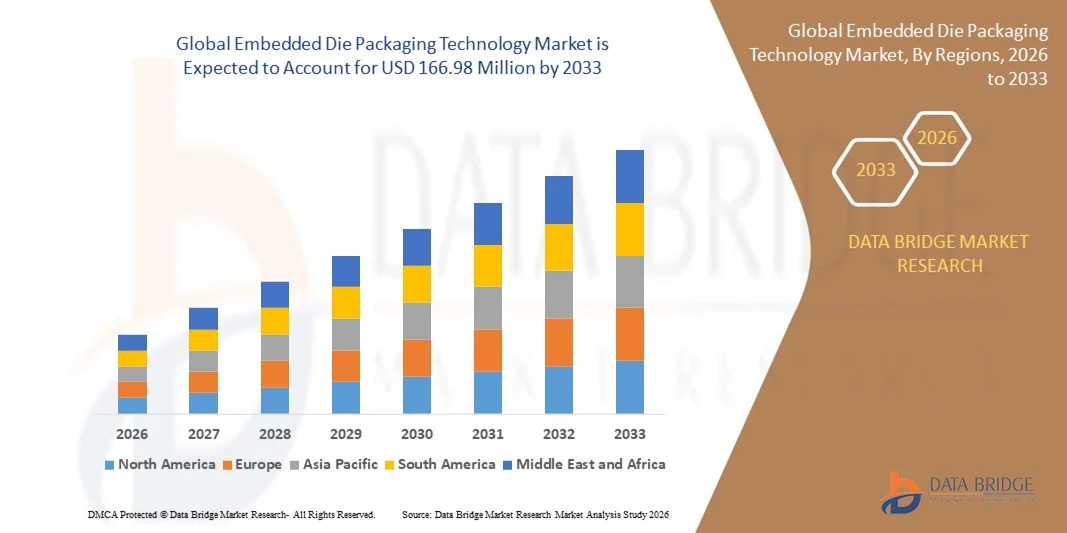

- The global embedded die packaging technology market size was valued at USD 143.53 million in 2025 and is expected to reach USD 166.98 million by 2033, at a CAGR of 1.91% during the forecast period

- The high adoption of autonomous robots for professional services is the major factor accelerating the growth of the embedded die packaging technology market. Furthermore, the growing population and increasing disposable income, developed telecommunication infrastructure and rising adoption of IoT are also expected to drive the growth of the embedded die packaging technology market

- However, the high cost of these chips and high cost restrains the embedded die packaging technology market, whereas, the reduced power loss of the system will challenge market growth

Embedded Die Packaging Technology Market Analysis

- High growth in trend of Internet of Things (IoT) globally and the rise in application in healthcare and automotive devices will create ample opportunities for the embedded die packaging technology market

- Asia-Pacific dominated the embedded die packaging technology market with the largest revenue share of 36.14% in 2025, driven by rapid urbanization, growing consumer electronics demand, and rising semiconductor manufacturing capabilities in countries such as China, Japan, South Korea, and India. Government initiatives supporting electronics innovation and digitalization are driving adoption

- North America region is expected to witness the highest growth rate in the global embedded die packaging technology market, driven by increasing focus on chip miniaturization, expansion of semiconductor fabrication facilities, and strong demand from automotive, aerospace, and high-performance computing sectors

- The Embedded Die in IC Package Substrate segment dominated the market with the largest revenue share of 45.3% in 2025, driven by its widespread adoption in semiconductor manufacturing and high-performance electronic devices. Its advantages include improved thermal management, enhanced electrical performance, and compatibility with advanced packaging methods, making it the preferred choice for integrated circuits in consumer electronics, automotive, and industrial applications

Report Scope and Embedded Die Packaging Technology Market Segmentation

|

Attributes |

Embedded Die Packaging Technology Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Embedded Die Packaging Technology Market Trends

Rising Demand For Miniaturized, High-Performance Electronics

- The growing focus on compact, high-performance, and energy-efficient electronic devices is significantly shaping the embedded die packaging technology market, as manufacturers increasingly adopt packaging solutions that reduce form factor while enhancing thermal management and reliability. Embedded die solutions are gaining traction across consumer electronics, automotive, healthcare, and industrial sensing applications, encouraging innovation in packaging design and materials

- Increasing awareness around device performance, durability, and energy efficiency has accelerated the adoption of embedded die technology in semiconductors, wearables, medical devices, and IoT systems. Manufacturers are prioritizing packaging solutions that support high-density integration, miniaturization, and improved thermal and electrical performance, prompting collaborations between semiconductor companies and packaging solution providers

- Advanced packaging and sustainability trends are influencing purchasing and design decisions, with companies emphasizing reliability, energy efficiency, and cost-effective manufacturing processes. These factors help businesses differentiate products in a competitive market while ensuring scalability, reducing energy consumption, and supporting environmental compliance

- For instance, in 2024, ASE Technology in Taiwan and Amkor Technology in the U.S. expanded their embedded die packaging offerings for ICs in consumer electronics and wearable devices. These initiatives were introduced to meet rising demand for miniaturized, high-performance, and energy-efficient solutions, with distribution across global semiconductor supply chains. The developments also support faster time-to-market and improved device performance

- While adoption of embedded die packaging is growing, sustained market expansion depends on continuous R&D, process innovation, and cost optimization. Manufacturers are also focusing on improving production scalability, supply chain reliability, and developing advanced packaging solutions that balance performance, cost, and sustainability for broader application

Embedded Die Packaging Technology Market Dynamics

Driver

Growing Demand For Miniaturized, High-Performance Electronics

- Rising demand for compact, energy-efficient, and high-performance electronics is a major driver for the embedded die packaging technology market. Manufacturers are increasingly integrating dies directly into substrates or boards to reduce size, improve thermal management, and enhance overall device performance. This trend also drives R&D in new packaging materials and technologies, supporting product diversification

- Expanding applications in consumer electronics, automotive electronics, medical devices, wearables, and industrial sensing are fueling market growth. Embedded die packaging improves reliability, performance, and device longevity, enabling manufacturers to meet industry and consumer expectations for advanced electronics

- Semiconductor companies are actively promoting embedded die solutions through innovation, collaboration, and marketing initiatives. These efforts are supported by the rising need for miniaturized, high-performance, and sustainable solutions across multiple industries, and they also encourage partnerships to improve packaging efficiency and reduce environmental footprint

- For instance, in 2023, Amkor Technology in the U.S. and JCET Group in China reported increased deployment of embedded die packaging for ICs in wearables and automotive electronics. This adoption followed higher demand for miniaturized, reliable, and energy-efficient devices, driving product differentiation and repeat orders. Both companies emphasized process reliability, scalability, and quality compliance in marketing campaigns to strengthen customer trust

- Although rising miniaturization and high-performance trends support growth, wider adoption depends on cost management, material availability, and scalable manufacturing processes. Investment in supply chain efficiency, advanced materials, and process innovation will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Cost And Complex Manufacturing Processes

- The relatively higher cost of embedded die packaging compared to conventional packaging methods remains a key challenge, limiting adoption among cost-sensitive manufacturers. Complex processes, precision requirements, and advanced materials contribute to elevated production costs. In addition, fluctuating supply of high-quality substrates or boards can impact cost stability and market penetration

- Awareness of advanced packaging benefits remains uneven, particularly among small and medium enterprises in developing regions. Limited understanding of technical advantages restricts adoption across certain segments and slows innovation uptake in emerging markets

- Supply chain and production challenges also affect market growth, as embedded die packaging requires advanced manufacturing capabilities, stringent quality control, and specialized equipment. Logistical complexities, yield management, and process optimization add to operational costs. Companies must invest in high-precision machinery, skilled workforce, and quality monitoring to maintain performance

- For instance, in 2024, semiconductor manufacturers in India and Southeast Asia reported slower adoption of embedded die packaging due to higher costs and limited technical expertise. Complex production requirements and stringent quality standards were additional barriers, affecting supply chain efficiency and project timelines

- Overcoming these challenges will require cost-efficient production techniques, expanded technical training, and strategic partnerships between packaging providers and semiconductor companies. Developing scalable, reliable, and cost-competitive embedded die solutions, while promoting awareness of functional and performance benefits, will be essential for widespread adoption

Embedded Die Packaging Technology Market Scope

The market is segmented on the basis of platform, technology, and industry vertical.

- By Platform

On the basis of platform, the embedded die packaging technology market is segmented into Embedded Die in IC Package Substrate, Embedded Die in Rigid Board, and Embedded Die in Flexible Board. The Embedded Die in IC Package Substrate segment dominated the market with the largest revenue share of 45.3% in 2025, driven by its widespread adoption in semiconductor manufacturing and high-performance electronic devices. Its advantages include improved thermal management, enhanced electrical performance, and compatibility with advanced packaging methods, making it the preferred choice for integrated circuits in consumer electronics, automotive, and industrial applications.

The Embedded Die in Flexible Board segment is expected to witness the fastest growth rate from 2026 to 2033, propelled by the growing demand for lightweight, bendable, and compact electronic devices such as wearable sensors, flexible medical devices, and IoT-enabled smart products. Flexibility, portability, and miniaturization are key factors driving this segment’s rapid growth across diverse applications.

- By Technology

On the basis of technology, the embedded die packaging technology market is segmented into Medical Wearable Devices, Medical Implants, Sports/Fitness Devices, Military, Industrial Sensing, and Others. The Medical Wearable Devices segment held the largest revenue share of 38.7% in 2025, fueled by the rising adoption of health monitoring solutions, wearable sensors, and connected devices that require reliable embedded die solutions for compact and accurate performance. This segment benefits from increasing consumer health awareness, aging populations, and integration with smartphones and cloud platforms.

The Sports/Fitness Devices segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the surge in fitness-conscious consumers, smartwatches, and wearable trackers that require low-power, miniaturized, and highly integrated embedded die technology. Continuous innovation in wearable tech and performance monitoring devices is further propelling this growth trajectory.

- By Industry Vertical

On the basis of industry vertical, the embedded die packaging technology market is segmented into Consumer Electronics, IT and Telecommunications, Automotive, Healthcare, and Others. The Consumer Electronics segment dominated the market with the largest revenue share of 41.6% in 2025, largely due to the proliferation of smartphones, tablets, laptops, smart home devices, and portable electronics that demand miniaturized, high-performance embedded die solutions. Its dominance is reinforced by strong R&D investments and the consumer preference for compact, energy-efficient devices.

The Automotive segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the rapid adoption of electric vehicles, autonomous driving technologies, advanced driver-assistance systems (ADAS), and connected car solutions. Embedded die solutions in automotive electronics enhance reliability, thermal stability, and integration, driving growth in this vertical across global markets.

Embedded Die Packaging Technology Market Regional Analysis

- Asia-Pacific dominated the embedded die packaging technology market with the largest revenue share of 38.5% in 2025, driven by rapid urbanization, growing consumer electronics demand, and rising semiconductor manufacturing capabilities in countries such as China, Japan, South Korea, and India. Government initiatives supporting electronics innovation and digitalization are driving adoption

- Furthermore, the region’s emergence as a manufacturing hub for advanced packaging solutions is making embedded die technology more accessible and cost-effective for a broader consumer and industrial base

Japan Embedded Die Packaging Technology Market Insight

The Japan embedded die packaging technology market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s high-tech culture, advanced semiconductor ecosystem, and rising adoption of wearable electronics and medical devices. Japanese manufacturers emphasize compact, high-performance, and reliable packaging solutions. Integration with IoT devices, smart sensors, and robotics is fueling growth. Moreover, Japan’s aging population is likely to drive demand for healthcare and medical wearable devices, increasing adoption of embedded die packaging solutions in both consumer and professional sectors.

China Embedded Die Packaging Technology Market Insight

The China embedded die packaging technology market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding electronics manufacturing base, rapid urbanization, and high rates of technological adoption. China represents one of the largest markets for consumer electronics, automotive electronics, and industrial sensing applications. The push toward smart factories, IoT integration, and availability of cost-effective packaging solutions, alongside strong domestic players, are key factors propelling market growth in China.

North America Embedded Die Packaging Technology Market Insight

North America is expected to witness the fastest growth rate from 2026 to 2033, driven by high adoption of advanced electronics, strong semiconductor manufacturing infrastructure, and increasing demand for miniaturized, high-performance devices. Consumers and manufacturers in the region highly value the reliability, integration capability, and performance benefits offered by embedded die packaging in applications such as consumer electronics, automotive, and industrial sensing. This widespread adoption is further supported by high R&D investment, a technologically advanced workforce, and the growing demand for compact and energy-efficient electronic components, establishing embedded die packaging as a preferred solution across multiple industries.

U.S. Embedded Die Packaging Technology Market Insight

The U.S. embedded die packaging technology market captured the largest revenue share in 2025 within North America, fueled by strong demand for high-density integrated circuits in consumer electronics, automotive, and healthcare devices. Manufacturers are increasingly prioritizing embedded die solutions for enhanced performance, reduced form factor, and improved thermal management. The growing adoption of advanced packaging in IoT devices, wearable electronics, and industrial applications, combined with significant R&D investments, further propels market growth. Moreover, integration with AI-enabled electronics and next-generation semiconductor technologies is significantly contributing to market expansion.

Europe Embedded Die Packaging Technology Market Insight

The Europe embedded die packaging technology market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing industrial automation, rising adoption of medical and wearable electronics, and stringent quality standards for electronic components. Urbanization and the demand for high-performance, energy-efficient solutions are fostering adoption. Growth spans across automotive, industrial sensing, and healthcare applications, with embedded die solutions being integrated into both new product designs and next-generation electronics.

U.K. Embedded Die Packaging Technology Market Insight

The U.K. embedded die packaging technology market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for miniaturized electronics, high-performance ICs, and wearable medical devices. Increased focus on innovation and technological advancements, combined with government support for semiconductor research, is encouraging adoption. The U.K.’s growing electronics manufacturing base and strong R&D ecosystem are expected to continue to stimulate market growth.

Germany Embedded Die Packaging Technology Market Insight

The Germany embedded die packaging technology market is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising awareness of advanced packaging benefits, high adoption of industrial automation, and demand for compact, reliable electronics. Germany’s well-developed semiconductor and automotive industries, along with a focus on sustainable and high-efficiency technologies, promote adoption of embedded die solutions. Integration with smart industrial equipment, automotive electronics, and medical devices is increasingly prevalent, aligning with local industry and consumer expectations.

Embedded Die Packaging Technology Market Share

The Embedded Die Packaging Technology industry is primarily led by well-established companies, including:

- Amkor Technology (U.S.)

- ASE Group (Taiwan)

- Microsemi (U.S.)

- STMicroelectronics (Switzerland)

- AT & S Austria Technologie & Systemtechnik Aktiengesellschaft (Austria)

- TOSHIBA CORPORATION (Japan)

- FUJITSU (Japan)

- Taiwan Semiconductor Manufacturing Company, Ltd. (Taiwan)

- General Electric (U.S.)

- Infineon Technologies AG (Germany)

- Fujikura Ltd. (Japan)

- TDK Electronics AG (Germany)

Latest Developments in Global Embedded Die Packaging Technology Market

- In June 2022, Advanced Semiconductor Engineering, Inc. (ASE), a member of ASE Technology Holding Co., Ltd., launched VIPack, an advanced packaging platform enabling vertically integrated package solutions. VIPack™ represents ASE’s next-generation 3D heterogeneous integration architecture, extending design rules while achieving ultra-high density and enhanced performance, marking a major technological milestone for the company

- In February 2022, Microsemi Corporation, a computing-in-memory innovator, addressed speech processing challenges at the edge by leveraging analog embedded SuperFlash technology. This solution highlights Microsemi’s continued focus on high-performance, energy-efficient embedded die technologies, providing a robust edge computing capability

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.