North America Antiblock Additive Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

1.40 Billion

USD

2.24 Billion

2024

2032

USD

1.40 Billion

USD

2.24 Billion

2024

2032

| 2025 –2032 | |

| USD 1.40 Billion | |

| USD 2.24 Billion | |

| % | |

|

북미 항블록 첨가제 시장 세그먼트, 양식 ( 무기, 유기), 대상 폴리머 (폴리에틸렌 (PE), 폴리 염화 비닐 (PVC), Biaxially-Oriented 폴리프로필렌 (BOPP), 폴리 에틸렌 테레 phthalate (PET), 폴리스티렌 (PS) 및 기타), End-Use Industry (포장, 산업, 농업, 의료 및 헬스 케어, 전자 및 태양, 인쇄 및 광학 및 기타), 국가 (미국, 캐나다, 캐나다, 2032, 2032, 2032, 2032, 2032, 2032, 2032, 2032, 2032, 2032, 2032, 2032, 2032

북미 Antiblock 첨가제 시장 분석

Antiblock 첨가제 시장은 견고한 성장, 플라스틱 포장에 대한 수요 증가로 구동됩니다. 북미 antiblock 첨가제 산업은 지속적으로 확장, 폴리머 포장의 혁신과 발전에 큰 파도가 증가했다. 바이오 기반 항블록 첨가제의 개발 수요가 시장의 기회를 창출하고 있습니다. 시장 역학은 또한 원료 가격을 변동하여 영향을받습니다. 전반적으로, 시장은 혁신과 지속 가능성에 초점을 맞추고, 진화 산업 요구를 충족시키기 위해 계속 확장 할 것으로 예상됩니다.

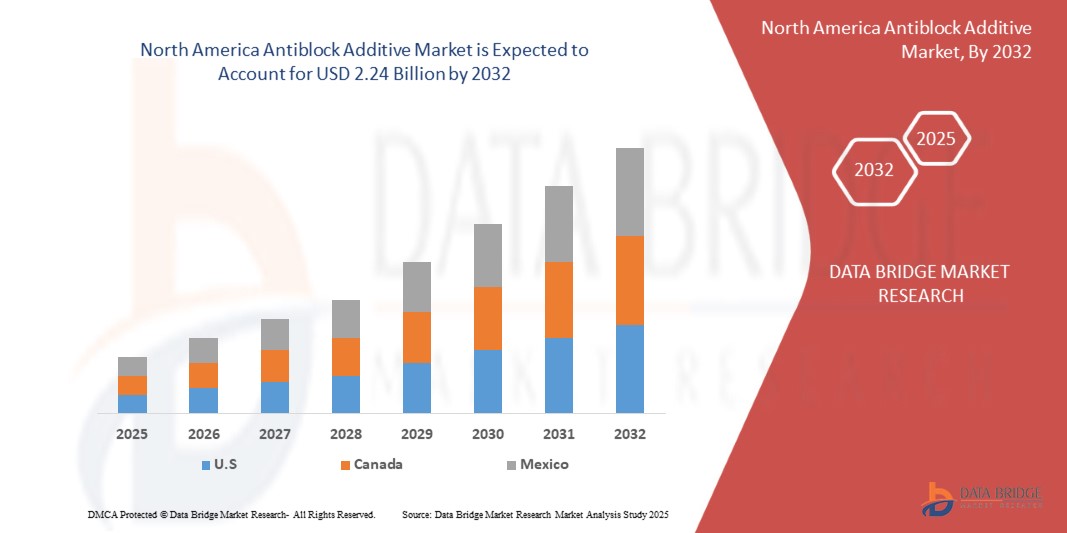

북미 Antiblock 첨가제 시장 크기

북아메리카 antiblock 첨가물 시장 크기는 2024년에 USD 1.40 억에 평가되고 2032년의 예측 기간 도중 5.98%의 CAGR와 더불어 2032년까지 USD 2.24 억에 도달하기 위하여 계획됩니다. 시장 가치, 성장률, 세그먼트, 지리적 범위 및 주요 플레이어와 같은 시장 시나리오에 대한 통찰력 외에도 데이터 브리지 시장 연구에 의해 큐레이터는 심층적 인 전문가 분석, 가격 분석, 브랜드 공유 분석, 소비자 설문 조사, 인구 분석, 공급망 분석, 가치 사슬 분석, 원료/소비자 개요, 공급업체 선택, PESTLE 분석, 포터 분석 및 규제 프레임 워크를 포함합니다.

북미 Antiblock 첨가제 시장연락처

“플라스틱 포장에 대한 수요 성장”

플라스틱 포장을 위한 성장 수요는 북아메리카 antiblock 첨가물 시장을 위한 뜻깊은 운전사입니다. 식품 및 음료, 제약, 소비자 용품 및 전자 상거래 확장과 같은 산업으로 효율적이고 내구성이 뛰어나고 기능성 포장 솔루션이 증가합니다. 플라스틱 포장은, 경량, 비용 효과적이고, 다재다능한, 각종 분야의 맞은편에 선호한 선택이 되었습니다. 플라스틱 포장에 대한 이 증가 된 신뢰성은 플라스틱 재료의 성능을 향상 첨가제에 대한 수요를 구동한다. Antiblock 첨가제는 포장에 사용되는 플라스틱 필름의 처리 및 성능 향상에 중요한 역할을합니다. 이 첨가제는 제조, 취급 및 저장 중에 함께 접합하는 플라스틱 필름의 층을 방지합니다. 반대로 막 대리인 없이, 플레스틱 필름은 생산 문제점, 타협한 포장 무결성 및 불능에 지도하는 것을 다른 것에, 고착할 것입니다. 이러한 문제를 줄이기 위해 안티 블록 첨가제는 부드러운 생산 공정, 높은 품질의 제품 및 더 효율적인 포장 시스템을 보장합니다.

가동 가능한 플라스틱 포장을 위한 수요에 있는 큰 파도는, 특히 식품 산업에서, 더 antiblock 첨가물 시장의 성장을 추진합니다. 소비자가 더 긴 선반 생활을 요구하는 상태에서, 더 나은 제품 보전 및 사용자 친절한 포장은, antiblock 첨가물 플라스틱 포장의 기능과 매력을 개량하기 위하여 공헌합니다. 또한, 지속 가능성은 성장하는 관심사로, 환경 친화적 인 안티 블록 첨가제의 개발은이 추세를 지원, 포장 분야에서 혁신을위한 기회를 제공.

보고서 범위 및 시장 세그먼트

| 관련 기사 | 북미 Antiblock 첨가제이름 *시장 통찰력 |

| Segments 적용 |

|

| 국가 덮음 | 미국, 캐나다, 멕시코 |

| 핵심 시장 선수 | (미국), Ampacet CORPORATION (미국), ALTANA (독일), Dow (미국), Lyondellbasell Industries Holdings B.V. (네덜란드), Astra Polymers (사우디 아라비아), Avient Corporation (미국), BASF (독일), Cargill, Incorporated (미국), Covia Holdings LLC. (미국). (미국). (미국). (미국). (미국). (미국). (미국). (미국). |

| 시장 기회 |

|

| Value 추가 데이터 Infosets | 시장 가치, 성장률, 세그먼트, 지리적 범위 및 주요 플레이어와 같은 시장 시나리오에 대한 통찰력 외에도 데이터 브리지 시장 연구에 의해 큐레이터는 심층적 인 전문가 분석, 가격 분석, 브랜드 공유 분석, 소비자 설문 조사, 인구 분석, 공급망 분석, 가치 사슬 분석, 원료/소비자 개요, 공급업체 선택, PESTLE 분석, 포터 분석 및 규제 프레임 워크를 포함합니다. |

북미 Antiblock 첨가제가격표이름 *

Antiblock 첨가물은 중합체 영화에서, 특히 폴리에틸렌과 폴리프로필렌에서, 영화 층 사이 접착을 감소시키는 화학 화합물입니다. 이 첨가제는 층 사이의 접촉 영역을 최소화하는 마이크로 스코프 거친 표면을 만들기 위해 작업, 함께 스틱에서 그들을 방지. 일반적인 antiblock 대리인은 실리카, talc 및 합성 규산염을 포함합니다. 그들은 포장 영화, 농업 영화 및 산업 신청에서 널리 이용됩니다 취급, 가공 및 machinability를 개량하기 위하여. 블록을 줄이기 위해 이러한 첨가제는 생산성을 향상시키고 필름 분리를 촉진하며 최종 플라스틱 필름 제품의 투명성, 기계적 특성 또는 인쇄성없이 효율적인 포장 작업을 보장합니다.

북미 Antiblock 첨가제가격표역학

드라이버

- Booming 자동차 및 산업 분야

플라스틱 필름에 주로 사용되는 안티 블록 첨가제는 가공 중에 접합을 방지하기 위해 자동차 및 제조 확장과 같은 산업으로 점점 더 중요합니다. 자동차 분야에서는 포장, 인테리어 및 자동차 부품에 대한 경량, 내구성 및 비용 효율적인 재료에 대한 수요가 증가하고 있습니다. Antiblock 첨가제는 자동차 포장, 보호 코팅 및 복합 재료에 응용 프로그램을 찾을 플라스틱 필름의 생산에 사용됩니다. 북미 차량 생산 증가로 제조 업체는 자동차 플라스틱의 성능과 외관 향상에 초점을 맞추고, 더 안티 블록 첨가제에 대한 필요성을 밀어. 자동차 산업은 더 효율적이고 재상할 수 있으며, 기능성 소재는 시장의 성장에 직접 기여합니다.

마찬가지로, 산업 분야, 포장, 건설 및 기계 등 다양한 응용 프로그램을 우회, 중요한 드라이버입니다. 산업은 포장과 기계장치를 위한 고품질 플레스틱 필름을 수요로, antiblock 첨가물을 위한 필요는 건장했습니다. 포장 산업에서, antiblock 첨가물은 함께 접합에서 필름 층을 방지하기 위해 필수적이며 가공의 용이성을 강화하고 최종 제품의 품질을 향상시킵니다. 또한, antiblock 첨가물은 산업 포장 해결책에, 특히 대량 상품과 과민한 물자 취급에서 근본적입니다.

예를 들어,

- 5 월 2022에서 Squarespace에 의해 출판 된 기사에 따르면 블로그는 자동차 응용 분야의 플라스틱 사용을 탐구하고 이점과 환경 문제를 강조합니다. 플라스틱은 차량 경량, 연료효율 및 customizable 만듭니다, 그러나 유독한 PVC와 빈약한 재생 가능성과 같은 문제점은 환경을 해칠 수 있습니다. 이 문제를 해결하기 위해 더 지속 가능한 폴리머에 대한 기사 호출.

- 5월 2023일, American Chemistry Council, Inc.에 의해 출판된 기사에 따르면 미국 화학위원회 (American Chemistry Council)의 2023 보고서는 자동차의 플라스틱이 2012에서 2021로 증가했습니다. 플라스틱은 연료 효율, 안전 및 성능 향상, 특히 전기 자동차 (EVs), 배터리의 무게를 축소함으로써. 보고서는 지속 가능성과 재활용 노력의 플라스틱 역할을 강조합니다.

두 분야의 비용 절감, 재료 특성 개선, 그리고 지속 가능성은 antiblock 첨가제의 채택을 증가시키기 위해 리드를 보장합니다. 북미 자동차 및 산업 생산이 계속 상승함에 따라 이러한 첨가제에 대한 수요는 소송을 따를 것으로 예상되며 향후 몇 년 동안 안티 블록 첨가제 시장에 대한 긍정적 인 성장 trajectory를 강화 할 것으로 예상됩니다.

- 폴리머 포장의 혁신과 발전

폴리머 포장의 혁신은 두드러지게 antilock 첨가제 시장의 성장에 영향을 미쳤습니다. 포장 재료 및 제품 성능 향상. Antilock 첨가물, 주로 포장에서 사용 하 여 내구성, 안정성, 및 폴리머의 성능 향상, 포장 산업의 진화 요구에 따라 증가된 수요를 보고. 포장 필요조건은 더 지속 가능하고, 능률 적이고 및 고성능 물자로 이동으로, antilock 첨가물은 중합체 정립을 강화하는 핵심 역할을 합니다. 1 차적인 운전사 중 하나는 마찰과 착용에 더 저항하는 중합체를 위한 성장 수요입니다. Antilock 첨가물은 고분자 표면 사이 마찰을 감소시키고, 포장 과정에서 손상의 위험을 최소화하고, 특히 식품 및 제약과 같은 산업 분야에서 제품 무결성가 중요하다. 이 첨가물은 또한 중합체의 가공 특성을 개량하고, 더 매끄러운 생산 과정을 허용하고 포장 물자의 생활을 연장하.

지속 가능성은 중요한 초점이 되고, biodegradable 또는 recyclable 포장 물자를 위한 수요에 있는 상승이 있습니다. Antilock 첨가물은 이 환경 친화적인 중합체를 더 효과적인 시키는 것을 돕고 내구재는, 환경의 손상 없이 잘 실행합니다. Greener Packaging Solution을 향한 이 변화는 마찰을 줄이고 환경에도 안전하지 않는 Antilock 첨가제의 정립에 혁신을 주도했습니다. 또한 전자 상거래의 상승은 북미 운송의 의장을 견딜 수있는 강력한 포장 솔루션을 높이화했습니다. Antilock 첨가제는 폴리머 포장의 성능 향상에 의해이에 기여하고, 그 제품은 포장 실패의 위험을 줄이기 위해 transit 동안에 intact 남아.

예를 들어,

- CarePac에 의해 출판 된 기사에 따르면, 포장 폴리머 가이드는 합성 및 생물 분해성 플라스틱을 포함한 다양한 종류의 폴리머 포장 재료에 대한 자세한 통찰력을 제공합니다. 그것은 폴리에틸렌, PET, 바이오 플라스틱, 응용 프로그램, 혜택, 위험, 환경 영향과 같은 일반적인 폴리머를 탐구하고 포장 산업에서 지속 가능한 환경 친화적 인 대안으로 전환하는 동안.

- 2020 년 Elsevier B.V에 의해 출판 된 기사에 따르면, 이 장은 기존 폴리머, 생소성, 나노폴리머에 초점을 맞춘 식품 포장재를 탐구합니다. 그것은 기존의 고분자에 비 재생성과 같은 생물 분해성-while 해결 도전과 같은 생물 플라스틱의 이점을 강조합니다. 이 연구는 나노 기술과 같은 기술 발전을 통해 포장 솔루션을 개선하고 재료 성능을 향상시킵니다.

- 미시간 주립 대학에 의해 간행된 기사에 따르면, 미시간 주립 대학의 이 문서는 보호, 비용 효과 및 다예 다제와 같은 그것의 이익을 강조하는 플라스틱과 중합체 근거한 포장을 시험합니다. 잠재적인 건강 위험, 마이크로플라스틱 및 환경 영향에 대한 우려가 있으며 지속적인 연구가 포장 재료, 지속 가능성 및 소비자 안전을 개선하기 위해 노력합니다.

- 폴리마트가 발표한 기사에 따르면, PolyMart는 식품 포장에 사용되는 폴리머의 종합적인 개요를 제공하며, 유형, 특성 및 이점을 강조하며 식품을 보호하고 유통 기한을 연장하고 비용 효율적입니다. 이 플랫폼은 신뢰할 수있는 공급 업체와 구매자를 연결하고 실시간 가격 동향을 제공합니다.

고분자 포장의 혁신은, antilock 첨가물에 있는 전진에 의해 몰아지고, 고성능, 지속 가능하고, 튼튼한 포장 해결책을 위한 성장 수요, 따라서 antilock 첨가물 시장의 확장을 촉진하.

회사연혁

- Bio-Based Antiblock 첨가제의 발전

바이오 기반 안티 블록 첨가제의 개발은 특히 필름 접착과 관련된 도전을 해결하는 폴리머 가공 분야에서 중요한 발전을 나타냅니다. 전통적으로, 실리카 또는 talc와 같은 무기 antiblock 첨가물은 중합체 영화 층의 함께 막는 mitigate에 고용되었습니다. 효과적인 동안, 이 무기 첨가물은 영화의 광학적인 명확성, 특히 더 높은 농도에 타협할 수 있습니다. 대조적으로, bio-based antiblock 첨가물은 지속가능하고 능률적인 대안을, 희생적인 명확성 없이 강화 영화 성과를 제안합니다.

자연적인 아미드에서 파생된 그들과 같은 생물 근거한 antiblock 첨가물은, 중합체 표면에, 영화 층 사이 마찰 계수를 감소시키는 lubricating 층을 형성해서 기능합니다. 이 메커니즘은 차단뿐만 아니라 제품 가시성을 중요 한 식품 포장과 같은 응용 프로그램에 중요 한 영화의 투명도 유지.

바이오 기반 솔루션을 향한 변화는 환경적 고려에 의해 구동된다. 산업은 생태 발자국을 줄이기 위해 노력하고 있습니다. 지속 가능한 첨가제의 수요가 증가했습니다. 바이오 기반 안티 블록 첨가제, 재생 가능 자원에서 파생되고, 이러한 지속 가능성 목표와 일치. Fine Organics와 같은 회사는 Finawax B, 폴리올레핀 기반 영화의 최적의 antiblocking 특성을 제공하는 세련된 야채 기반 behenamide와 같은 제품을 개발했습니다. 적당한 노출량에 무기 antiblock 대리인과 조화하여 사용될 때, 그것은 효과적으로 환경 책임을 가진 성과를 균형을 잡습니다.

예를 들어,

- Cargill에 의해 출판 된 블로그에 따르면, Incorporated, Optislip TM BR (behenamide)은 폴리머 필름에 대한 설계 된 바이오 기반 안티 블록 첨가제입니다. 필름 선명도를 유지하면서 lubricating 표면 층을 형성하여 차단을 감소시킵니다. 각종 중합체를 위해 적당한, 그것은 무기 첨가물에 지속 가능한 대안을 제안하고, 고성능과 환경 친화적인 포장 해결책을 위한 기업 수요로 맞추기.

- Fine Organic Industries Limited에 따르면 Finawax B는 식물성 근거한 behenamide이며 폴리올레핀 필름의 효과적인 바이오 기반 안티 블록 첨가제입니다. 투명성을 유지하면서 필름 접착을 최소화하며 무기 방지제에 대한 신뢰성을 감소시킵니다. 이 지속 가능한 솔루션은 친환경 폴리머 첨가제에 대한 업계의 변화와 패키징 성능을 향상시킵니다.

바이오 기반 안티 블록 첨가제의 개발은 폴리머 첨가제 기술에 대한 비례적인 변화를 나타냅니다. 필름 선명도 및 지원 지속 가능성 이니셔티브를 손상시키지 않는 효과적인 안티 차단 솔루션을 제공함으로써, 이러한 첨가제는 폴리머 필름에 대한 포장 및 기타 산업 의존의 미래에 중요한 역할을 수행 할 수 있습니다.

- E-Commerce Packaging의 온라인 쇼핑 및 성장에 큰 기여

전자 상거래의 급속한 확장은 크게 온라인 쇼핑에서 실질적으로 증가하는 소비자 구매 행동을 변환했습니다. 이 큰 파도는 제품을 지키는 능률 적이고 믿을 수 있는 포장 해결책을 intact와 presentable 전달됩니다. 따라서, 높은 품질의 포장 필름에 대한 고도로 수요가있어 차단과 같은 문제를 방지하는 고품질의 포장 필름이있어 포장 공정을 방해하고 제품 무결성을 준수합니다.

Anti-block 첨가제는 필름 층 사이의 접착을 줄이기 위해 이러한 도전을 해결하는 데 중요한 역할을합니다. 포장 작업의 효율성을 강화하십시오. 이 첨가제는 고분자 필름으로 통합되어 미세 가공 표면, 층 사이의 접촉점과 제조 및 제품 포장 중에 매끄럽게 취급을 촉진합니다.

이 성장은 e-commerce 생태계의 필수적인 구성 요소 인 식품, 음료 및 제약 산업에서 포장 된 상품의 상승 소비에 영향을 미칩니다. 소비자가 구매를 위해 온라인 플랫폼에 점점 의존하므로 제품 품질 및 안전을 유지하는 포장 필름에 대한 수요는 기적이되었습니다.

예를 들어,

- Plastiblends에 따르면, Polyaddit Anti-Block Masterbatches는 층 사이 접촉을 감소시키는 마이크로 가공 표면을 창조하는 정밀한 입자를 소개해서 영화 접착을 막습니다. 이 제품은 식품 포장, 제약 및 소비자 용품과 같은 산업 분야에서 원활한 가공 및 향상된 제품 성능을 보장합니다.

- 3 월 2024, Flex-Pack Engineering, Inc.의 기사에 따르면, 온라인 쇼핑의 큰 파도와 전자 상거래의 성장은 효율적이고 신뢰할 수있는 포장 솔루션에 대한 수요를 크게 증가했습니다. 가동 가능한 플레스틱 필름은 그들의 경량과 방어적인 재산 때문에 포장에서 통용됩니다. 그러나, 이 영화는 함께 찌를 수 있습니다 - "blocking"로 알려진 현상은 포장 공정과 제품 품질에 영향을 줄 수 있습니다. 이 문제점을 해결하기 위하여, 반대로 구획 첨가물은 플라스틱 영화로 통합되어 micro-rough 표면을 창조하고, 영화 층 사이 접착을 감소시키고 더 매끄럽게 취급하고 가공을 facilitating. 이 향상은 전자 상거래에서 전형적인 고속 포장 작업의 효율성을 유지하기위한 것이 중요합니다.

- 2019 년 11 월 Furion Analytics Research & Consulting LLP가 발표 한 기사에 따르면 식품 및 음료, 제약 및 소비자 용품과 같은 분야의 포장 필름에 대한 수요가 포장 필름 시장의 확장의 주요 드라이버가되었습니다. 이 성장은 특히 Polyethylene (PE)와 폴리프로필렌 (PP)와 같은 영화의 취급 그리고 성과를 위해 결정되는 반대로 구획 첨가물을 위한 수요를 증가시켰습니다, 문제점을 막는 prone인.

결론적으로, 온라인 쇼핑에 있는 큰 파도 및 전자 상거래 포장에 있는 consequent 성장은 반대로 구획 첨가물 시장을 위한 pivotal 기회입니다. 전자 상거래 부문은 지속적으로 확장되고, 제품 무결성 및 고객 만족을 보장하는 효과적인 포장 솔루션의 중요성은 포장 산업에서 안티 블록 첨가제의 중요한 역할을 수행하고 있습니다.

스트레인 / 캡enges

- 대체 첨가제 및 솔루션의 가용성

대안 첨가제 및 솔루션의 가용성은 북미 antilock 첨가제 시장에서 상당한 제스처 역할을합니다. 새로운 기술 및 재료가 등장함에 따라 제조 업체는 점점 기존의 antilock 첨가제에 대안을 탐구하고, 종종 비용 효율, 지속 가능성 및 성능 향상에 대한 욕망에 의해 구동됩니다. 이러한 대체 첨가제, 유사한 또는 향상된 특성을 제공 할 수 있습니다, 기존의 안티록 솔루션에 대한 수요를 도전, 기존 제품의 증가 경쟁과 감소 시장 점유율을 선도.

대안의 가용성에 의해 한 키 억제는 친환경 또는 생분해성 첨가제에 대한 이동 환경입니다. 지속 가능성은 많은 산업 분야에서 성장하는 관심사로, 제조업체는 환경 영향을 최소화하는 솔루션을 찾고 있습니다. 전통적인 antilock 첨가물은 자연 근거한 생물 유래 첨가물과 같은 효과적인, 대안입니다 시장 수요에 있는 잠재적인 이동을 창조하는 견인을 얻는 동안. 이러한 대안은 종종 더 환경적으로 책임지고, 기존 화학 첨가물에 대한 선호도를 운전. 또한, 재료 과학의 발전은 전통적인 antilock 첨가물 없이 강화된 마찰 감소 재산을 제공하는 혁신적인 중합체 근거한 해결책의 발달에 지도했습니다. 이 새로운 솔루션은 우수한 성능을 제공 할 수 있으며 첨가제에 대한 신뢰성을 감소시키고, 차례로, antilock 제품에 대한 수요에 영향을 미치는.

또한, 비용 고려 사항도 역할을합니다. 제조업체는 가격 감도가 높을 지역에서 더 비용 효과적 인 경우 대체 첨가제를 선택할 수 있습니다. 이 가격 중심 교대는 대안 해결책이 더 낮은 비용에 comparable 또는 우량한 성과를 설명하는 경우에 exacerbated 할 수 있었습니다.

예를 들어,

- 2019 년 5 월, 플라스틱 기술에 의해 출판 된 기사에 따르면 DuPont는 Dow Corning AMB-12235 Masterbatch를 출시하여 안티 블록 및 슬립 첨가제를 결합하여 PE 필름 처리를 개선했습니다. 이 실리콘 근거한 정립은 마찰의 낮은 계수를 제공하고, 막는 영화를 막고, 낮게 적재 (4-6%), 흐르는 생산, 복잡한 감소시키고, 공급 사슬에 있는 저축 공간을 감소시킵니다.

- ChemPoint에 의해 간행된 기사에 따르면. Momentive Tospearl 실리콘 구슬은 층 사이 접착을 방지하고 밀어남 도중 마찰의 계수를 감소시키기 위하여 디자인된 polyolefin 영화를 위한 진보된 antiblock 그리고 미끄러짐 첨가물입니다. 이 첨가제는 필름 명확성 및 처리 효율을 개선하고 식품 접촉 응용 및 열으로 최대 400°C의 열 안정을 위해 FDA 승인되고 가동 시간을 단축합니다.

전반적으로, 대안 첨가물 및 해결책의 가용성은 antilock 첨가물 시장의 성장에 도전을, 제조자가 더 지속될지도 모르다 것과 같이, 또는 전통적인 antilock 제품을 위한 시장 잠재력을 제한하는 비용 효율성 선택권을 포위합니다.

- 규제 준수 및 테스트 표준

Antiblock 첨가제 시장은 엄격한 규제 준수 및 테스트 기준에 따라 제품 안전 및 환경 보호를 보장합니다. 미국에서 식품 및 의약품 관리 (FDA)는 포장 재료에 사용되는 antiblock 첨가물을 포함하여 식품 접촉을 위해 예정된 물질을 감독합니다. 제조업체는 이러한 첨가제가 식품 제품에 대한 철저한 평가와 잠재적 마이그레이션을 포함하는 그들의 의도 된 사용에 대한 안전임을 입증해야합니다.

유럽에서는 유럽 화학기구 (ECHA) 및 유럽 식품 안전청 (EFSA)는 항블록 첨가제를 포함한 화학 물질의 안전을 평가하는 역할을합니다. REACH 규정은 제조업체 및 수입업체 등록 화학 물질을 대상으로 한 용도 및 안전 데이터를 포함합니다. 이 엄격한 규제 환경은 음식과의 접촉에 있는 모든 물자는 안전하골 공중 건강을 jeopardize 하지 않습니다.

항블록 첨가제를 둘러싼 규제 프레임 워크는 제품 안전, 환경 보호 및 업계 표준 준수를 보장하기 위해 중요합니다. Antiblock 첨가물은 포장 물자에서 전형적으로, 특히 폴리에틸렌 영화에서, 매우 유용성과 제품 품질을 강화할 수 있는 끈으로 장을 방지하기 위하여 이용됩니다. 그러나, 그들의 광범위하게 사용법은 그들의 사용을 지배하기 위하여 포괄적인 규제 지침의 발달을 necessitated.

다른 국가 및 지역은 규제 지침을 수립했습니다. 예를 들어, 식품 및 의약품 관리 (FDA)는 식품 포장에 사용되는 첨가제를 포함하여 식품과 접촉하도록하기위한 물질의 사용을 감독합니다. FDA는 모든 식품 접촉 물질이 식품 제품에 첨가제의 원료 및 잠재적 마이그레이션의 철저한 검토를 포함하는 의도 한 사용에 안전해야한다.

예를 들어,

- 유럽 식품 안전청 (European Food Safety Authority)이 발표 한 블로그에 따르면, EFSA는 유럽 연합 (EU)의 안전 평가 및 규제 프레임 워크에 중점을 둔 식품 첨가물에 대한 심층 정보를 제공했습니다. 그들의 평가는 항블록 에이전트와 같은 식품 포장에 사용되는 첨가제를 보장하는 데 도움이, 소비자를 위해 안전하고 공공 복지를 보호하기 위해 엄격한 환경 및 건강 기준을 준수.

- 유럽 화학기구 (ECHA)는 식품 접촉을위한 활성 및 지능형 재료에 대한 법률의 포괄적 인 개요를 제공합니다. 이 규정은 포장에 사용되는 antiblock 대리인과 같은 물자의 안전을 지킵니다. ECHA의 프레임 워크는 소비자 건강을 보호하고 식품 안전을위한 EU 표준 준수를 보장합니다.

규제 준수 및 테스트 표준에 대한 견해는 제품 안전, 환경 지속 가능성 및 소비자 건강을 보장하기 위해 안티 블록 첨가제 시장에 필수적입니다. FDA, ECHA 및 EFSA와 같은 당국의 엄격한 감독은 산업 무결성을 유지하고 포장 재료에 첨가제의 더 효과적인 사용을 촉진하는 데 도움이됩니다.

원료 부족 및 배송 지연의 영향 및 현재 시장 시나리오

Data Bridge Market Research는 시장의 높은 수준의 분석을 제공하며, 원료 부족 및 운송 지연의 영향과 현재 시장 환경에 대한 정보를 제공합니다. 이것은 전략적인 가능성을 평가하기 위해 번역, 효과적인 행동 계획을 만들고, 중요한 결정을 내릴 사업.

표준 보고서 외에도, 우리는 또한 예측 된 선박 지연, 지역, 상품 분석, 생산 분석, 가격 매핑 추세, 소싱, 범주 성능 분석, 공급망 위험 관리 솔루션, 고급 벤치 마크 및 조달 및 전략적 지원을위한 기타 서비스에서 조달 수준의 심층 분석도 제공합니다.

제품의 가격과 가용성에 경제 감속의 예상된 영향

경제 활동이 느리면, 산업은 고통을 시작합니다. 제품의 가격 및 접근성에 대한 경제 다운턴의 예측 효과는 DBMR에 의해 제공된 시장 통찰력 보고서 및 인텔리전스 서비스에서 고려됩니다. 이로, 우리의 클라이언트는 전형적으로 그들의 경쟁자, 프로젝트 그들의 판매 및 수익, 및 그들의 이익 및 손실 expenditures의 앞에 1 단계를 지킬 수 있습니다.

북미 Antiblock 첨가제 시장 범위

시장은 유형, 표적 중합체 및 끝 사용 기업의 기초에 세그먼트를 매깁니다. 이러한 세그먼트의 성장은 업계의 meagre 성장 세그먼트를 분석하고 핵심 시장 응용 프로그램을 식별하기위한 전략적 결정을 만드는 데 도움이되는 가치있는 시장 개요 및 시장 통찰력을 가진 사용자에게 제공합니다.

이름 *

- 무기물

- 제품정보

대상 폴리머

- 폴리에틸렌 (PE)

- Polyvinyl 염화물 (PVC)

- 축 방향 폴리프로필렌 (BOPP)

- 폴리에틸렌 테레프탈레이트 (PET)

- 폴리스티렌 (PS)

- 기타

End-Use 기업

- 포장 세부 사항

- 산업 분야

- 주요사업

- 의료 및 의료

- 전자 및 태양

- 인쇄 및 광학

- 기타

북미 Antiblock 첨가제 시장 지역 분석

시장은 분석 및 시장 규모 통찰력 및 추세는 국가, 유형, 타겟 폴리머 및 최종 용도 산업에 의해 위 참조됩니다.

시장에서 덮은 국가는 미국, 캐나다, 멕시코입니다.

U.S.는 급속하게 농업 분야를 확장하고 고성능 영화를 위한 수요를 성장하기 때문에 시장을 지배하기 위하여 설치됩니다. 고급 농업 기술, 정부 지원, 지속 가능성 이니셔티브 및 기술 혁신 드라이브 시장 성장, 강화 된 작물 보호, 효율성 및 장기 생산성을 보장합니다.

U.S.는 강력한 농업 발전으로 인해 지역에서 가장 빠르게 성장하고 있으며, 고성능 필름에 대한 수요와 지속 가능한 농업에 대한 정부 지원. 기술 혁신, 정밀 농업에 투자 증가, 농작물 수확량에 초점을 더 드라이브 시장 확장.

보고서의 국가 섹션은 또한 시장의 현재와 미래 추세에 영향을 미치는 시장의 규제에 개별 시장 영향을 미치는 요인과 변화를 제공합니다. 다운스트림 및 업스트림 값 체인 분석, 기술 동향 및 포터의 5 단계 분석과 같은 데이터 포인트는 개별 국가 시장 시나리오를 예측하는 데 사용되는 포인터의 일부입니다. 또한 북미 브랜드의 존재 및 가용성과 현지 및 국내 브랜드의 대형 또는 스카이스 대회로 인해 직면 한 도전, 국내 관세 및 무역 경로의 영향은 국가 데이터의 예측 분석을 제공하면서 고려됩니다.

북미 Antiblock 첨가제 시장 점유율

시장 경쟁력 있는 풍경은 경쟁업체의 세부 정보를 제공합니다. 포함 된 세부 사항은 회사 개요, 회사 재무, 수익 생성, 시장 잠재력, 연구 및 개발 투자, 새로운 시장 이니셔티브, 북미 존재, 생산 사이트 및 시설, 생산 능력, 회사 강점 및 약점, 제품 출시, 제품 폭 및 폭, 응용 도민. 위의 데이터 포인트는 시장과 관련된 회사 초점과 관련이 있습니다.

북미 Antiblock 첨가제시장에서 운영되는 시장 리더:

- Imerys (프랑스)

- Ampacet 기업 (미국)

- ALTANA (독일)

- 도우 (미국)

- Lyondellbasell 산업 홀딩스 B.V. (네덜란드)

- Astra Polymers (사우디 아라비아)

- Avient Corporation (미국)

- BASF (독일)

- Cargill, 전갈 (미국)

- Covia Holdings LLC. (미국)

- Evonik (독일)

- 정밀한 유기 산업 한정판 (India)

- Honeywell International Inc (미국)

- Inerals Technologies Inc. (미국)

- Momentive 성과 물자 (미국)

- 국가 플라스틱 색상, Inc. (미국)

- plasmix pvt (인도)

- SABIC (사우디 아라비아)

- Sukano AG (스위스)

- W. R. Grace & Co.-Conn (미국)

- Wells 플라스틱 (미국)

북미 Antiblock 첨가제 시장의 최신 개발

- 12 월 2024에서 SABIC는 LNP ELCRES CXL 폴리 카보네이트 공중 합체 수지를 도입하여 기동성, 전자, 산업 및 인프라 애플리케이션에 이상적입니다. 이 물자는 개량한 내구성, weatherability 및 저온 충격 저항을 제공합니다. SABIC의 TRUCIRCLE 프로그램의 밑에 생물 재생 가능한 버전에서 유효한, 그들은 열악한 화학 노출의 밑에 조차 지속 가능성에 공헌하고 부분 성과를, 균등하게 강화합니다

- 11월2024일, SABIC는 아시아 (BFA)의 Boao 포럼과 함께 영광의 전략적 파트너십을 갱신했으며, 17년 연속 후원을 수상했습니다. 이 파트너십은 SABIC의 지속 가능한 발전에 대한 헌신을 강조합니다. 이 회사는 BFA를 영향력을 강화하고 북미를 포함한 발전을 주도하는 플랫폼으로 활용합니다.

- 1 월 2025, Evonik Industries AG 및 Fuhua Tongda Chemicals Companyhave는 Leshan, China의 합작 투자를 설립하여 태양 전지 패널, 반도체 및 식품 포장과 같은 응용 분야에 대한 특수 수소 (H2O2)를 생산합니다. 51%와 Fuhua 49%를 보유하는 Evonik로, 벤처는 2026년에 시장을 공급할 것입니다. 이 파트너십은 아시아 태평양 지역의 Evonik의 존재를 강화합니다.

- 6월 2024일, Covia Holdings LLC는 에너지 및 산업 사업의 분리를 두 개의 독립적 인 기업으로 최종화했습니다. Covia Energy, LLC는 독립, 오하이오에 본사를 둔 Woodlands, Texas 및 Covia Solutions Solutions의 본사를두고 있습니다. 이 전략적인 움직임은 각 회사가 각각의 시장 기회에 집중할 수 있도록 합니다.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 소개

1.1 스튜디오의 활동

1.2 시장 결정

1.3 전망

1.4 제한

1.5 시장 덮개

2 시장 세그먼트

2.1 시장 덮개

2.2 GEOGRAPHICAL 가스

2.3 STUDY에 대한 년

2.4 치료 및 포장

2.5 DBMR TRIPOD 자료 가변 모델

2.6 MULTIVARIATE 모형

2.7 중요한 의견 지도를 가진 PRIMARY INTERVIEWS

2.8 DBMR 시장 위치

2.9 DBMR VENDOR 샤인 분석

2.1 시장 적용 커버리지 GRID

2.11 증권

2.12 소개

3 독점 요약

4 프리미엄 INSIGHTS

4.1 PESTEL 분석

4.1.1 화학 FACTORS

4.1.2 생태계

4.1.3 특수 필터

4.1.4 기술적인 모수

4.1.5 환경 발전기

4.1.6 LEGAL 펌프

4.2 PORTER의 FIVE FORCES 분석

4.2.1 새로운 범위의 THREAT

공급의 4.2.2 BARGAINING 힘

구매자의 4.2.3 BARGAINING 힘

4.2.4 이하의 THREAT

4.2.5 인치 가구

4.3 베니어 선택 CRITERIA

4.3.1 품질 및 CONSISTENCY

4.3.2 기술 향상

4.3.3 공급 사슬 믿을 수 있는

4.3.4 호환 및 SUSTAINABILITY

4.3.5 COST와 포장 STRUCTURE

4.3.6 우수한 안정성

4.3.7 융통성과 분류

4.3.8 위험 관리 및 관리 PLANS

5 시장 전망

5.1 드라이버

5.1.1 PLASTIC 포장을 위한 돌리는 DEMAND

5.1.2 BOOMING 자동 및 산업 SECTORS

5.1.3 폴리에스테 패킹에 있는 혁신과 광고

5.1.4 빠른 EXPANDING AGRICULTURAL SECTOR 및 고성능 필름에 대 한 필요

5.2 답글

5.2.1 FLUCTUATING RAW 물자 가격

5.2.2 ALTERNATIVE ADDITIVES 및 솔루션의 이점

5.3 기회

BIO-BASED ANTIBLOCK ADDITIVES에 있는 5.3.1 이점

5.3.2 온라인 쇼핑 및 E-COMMERCE 포장에 있는 성장

5.4 도전

5.4.1 책임과 시험 기준

5.4.2 SHIFTING CONSUMER FOCUS 카드 포장

6 북아메리카 ANTIBLOCK ADDITIVE MARKET, FORM에 의해

6.1 전망

6.2 인치

6.2.1 유형에 의하여 INORGANIC,

6.2.2 INORGANIC, 부분 크기로

6.3 오가닉

6.3.1 ORGANIC, 형식으로

7 북아메리카 ANTIBLOCK ADDITIVE 시장, TARGET POLYMER

7.1 전망

7.2 분말 (PE)

7.2.1 POLYETHYLENE (PE), TARGET POLYMER에 의해

7.3 폴리 비닐 CHLORIDE (PVC)

7.4 BIAXIALLY-ORIENTED 폴리 프로필렌 (BOPP)

7.5 POLYETHYLENE TEREPHTHALATE (애완 동물)

7.6 폴리스티렌 (PS)

7.7 다른

8 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET, END 사용 산업에 의해

8.1 전망

8.2 포장

8.3 산업

8.4 위치

8.5 의학과 건강 관리

8.6 전기와 태양

8.7 인쇄 및 OPTICS

8.8 기타

9 북아메리카 ANTIBLOCK ADDITIVE 시장, REGION에 의하여

9.1 북아메리카

9.1.1 미국

9.1.2 캐나다

9.1.3 멕시코

10 북아메리카 ANTIBLOCK ADDITIVE 시장: 회사 LANDSCAPE

10.1 회사 샤인 분석 : NORTH AMERICA

11 SWOT 분석

12 회사소개

12.1 아이머

12.1.1 회사 SNAPSHOT

12.1.2 REVENUE 분석

12.1.3 회사 ANALYSIS

12.1.4 제품포트폴리오

12.1.5 수익률

12.2 AMPACET 기업

12.2.1 회사 SNAPSHOT

12.2.2 회사 ANALYSIS

12.2.3 제품포장

12.2.4 수익 창출

12.3 아타나

12.3.1 회사 SNAPSHOT

12.3.2 회사 ANALYSIS

12.3.3 제품포장

12.3.4 수익률

12.4 문

12.4.1 회사 SNAPSHOT

12.4.2 REVENUE 분석

12.4.3 회사 ANALYSIS

12.4.4 제품 PORTFOLIO

12.4.5 유지 보수

12.5 LYONDELLBASELL 산업 HOLDINGS B.V.

12.5.1 회사 SNAPSHOT

12.5.2 REVENUE 분석

12.5.3 회사 SHARE ANALYSIS

12.5.4 제품 PORTFOLIO

12.5.5 수익 창출

12.6 에어리어

12.6.1 회사 SNAPSHOT

12.6.2 제품/BRAND PORTFOLIO

12.6.3 수익률

12.7 AVIENT 기업

12.7.1 회사 SNAPSHOT

12.7.2 REVENUE 분석

12.7.3 제품포트폴리오

12.7.4 수익률

12.8 바스

12.8.1 회사 SNAPSHOT

12.8.2 REVENUE 분석

12.8.3 제품포장

12.8.4 수익률

12.9 CARGILL, 구성

12.9.1 회사 SNAPSHOT

12.9.2 제품포트폴리오

12.9.3 수익 창출

12.1 코비아홀딩스

12.10.1 회사 SNAPSHOT

12.10.2 제품포장

12.10.3 수익률

12.11 은

12.11.1 회사 SNAPSHOT

12.11.2 REVENUE 분석

12.11.3 제품포트폴리오

12.11.4 수익률

12.12 FINE ORGANIC 산업 제한

12.12.1 회사 SNAPSHOT

12.12.2 REVENUE 분석

12.12.3 제품포트폴리오

12.12.4 수익률

12.13 HONEYWELL 국제 INC

12.13.1 회사 SNAPSHOT

12.13.2 REVENUE 분석

12.13.3 제품포트폴리오

12.13.4 수익률

12.14 INERALS 기술 INC.

12.14.1 회사 SNAPSHOT

12.14.2 REVENUE 분석

12.14.3 제품포트폴리오

12.14.4 수익률

12.15 MOMENTIVE 성능 재료

12.15.1 회사 SNAPSHOT

12.15.2 제품포트폴리오

12.15.3 수익률

12.16 NATIONAL PLASTICS 컬러, INC.

12.16.1 회사 SNAPSHOT

12.16.2 제품포트폴리오

12.16.3 수익률

12.17 플릭스 PVT LTD

12.17.1 회사 SNAPSHOT

12.17.2 제품포장

12.17.3 수익률

12.18 사비

12.18.1 회사 SNAPSHOT

12.18.2 리베니아 분석

12.18.3 제품포장

12.18.4 비용 절감

12.19 스칸소 AG

12.19.1 회사 SNAPSHOT

12.19.2 제품/BRAND PORTFOLIO

12.19.3 수익률

12.2 W. R. GRACE 및 CO.-CONN

12.20.1 회사 SNAPSHOT

12.20.2 제품포트폴리오

12.20.3 수익률

12.21 웰스 플레스틱

12.21.1 회사 SNAPSHOT

12.21.2 제품 PORTFOLIO

12.21.3 수익률

13 질문

14 관련 보고서

표 목록

TABLE 1 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

TABLE 2 NORTH 아메리카 ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (TONS)

TABLE 3 NORTH AMERICA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, REGION에 의해, 2018-2032 (USD THOUSAND)

TABLE 4 NORTH AMERICA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, 2018-2032, (TONS)

테이블 5 NORTH AMERICA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (USD THOUSAND)

TABLE 6 NORTH AMERICA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)

테이블 7 NORTH AMERICA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, PARTICLE 크기, 2018-2032 (USD THOUSAND)

TABLE 8 NORTH AMERICA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, PARTICLE 크기, 2018-2032 (TONS)

테이블 9 NORTH AMERICA ORGANIC IN ANTIBLOCK ADDITIVE MARKET, REGION, 2018-2032 (USD THOUSAND)

TABLE 10 NORTH AMERICA ORGANIC IN ANTIBLOCK ADDITIVE MARKET, 2018-2032, (TONS)

테이블 11 NORTH AMERICA ORGANIC IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 12 NORTH AMERICA ORGANIC IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 13 NORTH 아메리카 ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (USD THOUSAND)

TABLE 14 NORTH 아메리카 ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (TONS)

TABLE 15 NORTH AMERICA POLYETHYLENE (PE) IN ANTIBLOCK ADDITIVE MARKET, REGION에 의해, 2018-2032 (USD THOUSAND)

16 NORTH AMERICA POLYETHYLENE (PE) REGION, 2018-2032, (TONS)에 의해 ANTIBLOCK ADDITIVE 시장,

17 NORTH AMERICA POLYETHYLENE (PE) ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (USD THOUSAND)

18 NORTH AMERICA POLYETHYLENE (PE) ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (TONS)

19 NORTH AMERICA POLYVINYL CHLORIDE (PVC) REGION, 2018-2032 (USD THOUSAND)에 의해 ANTIBLOCK ADDITIVE MARKET에,

케이블 20 NORTH AMERICA POLYVINYL CHLORIDE (PVC) REGION, 2018-2032, (TONS)

케이블 21 NORTH AMERICA BIAXIALLY-ORIENTED POLYPROPYLENE (BOPP) ANTIBLOCK ADDITIVE MARKET에서, 2018-2032 (USD THOUSAND)

TABLE 22 NORTH AMERICA BIAXIALLY-ORIENTED POLYPROPYLENE (BOPP) IN ANTIBLOCK ADDITIVE MARKET, 2018-2032, (TONS)

테이블 23 NORTH AMERICA POLYETHYLENE TEREPHTHALATE (PET) IN ANTIBLOCK ADDITIVE MARKET, 2018-2032 (USD THOUSAND)

케이블 24 NORTH 아메리카 POLYETHYLENE TEREPHTHALATE (PET) IN ANTIBLOCK ADDITIVE MARKET, 2018-2032, (TONS)

TABLE 25 NORTH AMERICA POLYSTYRENE (PS) IN ANTIBLOCK ADDITIVE MARKET, REGION에 의해, 2018-2032 (USD THOUSAND)

TABLE 26 NORTH AMERICA POLYSTYRENE (PS) REGION, 2018-2032, (톤)

테이블 27 NORTH AMERICA 다른, REGION에 의해, 2018-2032 (USD THOUSAND)

TABLE 28 NORTH AMERICA OTHERS IN ANTIBLOCK ADDITIVE MARKET, 2018-2032 (톤)

TABLE 29 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET, END 사용 산업에 의해, 2018-2032 (USD THOUSAND)

TABLE 30 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET, END 사용 산업에 의해, 2018-2032 (TONS)

TABLE 31 NORTH AMERICA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, 2018-2032, (USD THOUSAND)

테이블 32 NORTH AMERICA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, REGION, 2018-2032 (TONS)

테이블 33 NORTH AMERICA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

테이블 34 NORTH AMERICA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)

35 NORTH AMERICA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

테이블 36 NORTH AMERICA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 37 NORTH AMERICA 산업, REGION, 2018-2032, (USD THOUSAND)

케이블 38 NORTH AMERICA 산업 ANTIBLOCK ADDITIVE 시장, 2018-2032 (TONS)

TABLE 39 NORTH AMERICA 산업 IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

케이블 40 NORTH AMERICA 산업 ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)

케이블 41 NORTH AMERICA 산업 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 42 NORTH AMERICA 산업 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

테이블 43 NORTH AMERICA AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, REGION, 2018-2032, (USD THOUSAND)

테이블 44 NORTH AMERICA AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, 2018-2032 (TONS)

ABLE 45 NORTH AMERICA AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)에 의해

테이블 46 NORTH AMERICA AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 47 NORTH 아메리카 MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, REGION, 2018-2032, (USD THOUSAND)

TABLE 48 NORTH 아메리카 MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, REGION, 2018-2032 (TONS)

ABLE 49 NORTH 아메리카 MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

ABLE 50 NORTH 아메리카 MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 51 NORTH AMERICA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, REGION, 2018-2032, (USD THOUSAND)

TABLE 52 NORTH AMERICA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, REGION, 2018-2032 (TONS)

TABLE 53 NORTH AMERICA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

케이블 54 NORTH AMERICA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (TONS)

TABLE 55 NORTH AMERICA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

TABLE 56 NORTH AMERICA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 57 NORTH AMERICA PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, 2018-2032, (USD THOUSAND)

58 NORTH AMERICA PRINTING 및 ANTIBLOCK ADDITIVE MARKET의 OPTICS, 2018-2032 (TONS)

TABLE 59 NORTH AMERICA PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 60 NORTH AMERICA PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (TONS)

TABLE 61 NORTH AMERICA PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

케이블 62 NORTH AMERICA 인쇄 및 ANTIBLOCK ADDITIVE MARKET의 OPTICS, FORM, 2018-2032 (TONS)

TABLE 63 NORTH AMERICA OTHERS IN ANTIBLOCK ADDITIVE MARKET, 2018-2032, (USD THOUSAND)

테이블 64 NORTH AMERICA 다른, REGION에 의해, 2018-2032 (TONS)

ABLE 65 NORTH AMERICA OTHERS IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

ABLE 66 NORTH AMERICA OTHERS IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

테이블 67 NORTH 아메리카 ANTIBLOCK ADDITIVE MARKET, COUNTRY, 2018-2032 (USD THOUSAND)

테이블 68 NORTH 아메리카 ANTIBLOCK ADDITIVE MARKET, COUNTRY에 의해, 2018-2032 (TONS)

테이블 69 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

TABLE 70 북아메리카 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

테이블 71 NORTH AMERICA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, 으로 TYPE, 2018-2032 (USD THOUSAND)

케이블 72 NORTH AMERICA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)

테이블 73 NORTH AMERICA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY PARTICLE SHAPE, 2018-2032 (USD THOUSAND)

테이블 74 NORTH AMERICA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY PARTICLE SHAPE, 2018-2032 (TONS)

케이블 75 NORTH AMERICA ORGANIC IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

테이블 76 NORTH 아메리카 ORGANIC IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 77 NORTH 아메리카 ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (USD THOUSAND)

테이블 78 NORTH 아메리카 ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (TONS)

케이블 79 NORTH AMERICA POLYETHYLENE (PE)은 TARGET POLYMER, 2018-2032 (USD THOUSAND)의 상표를 붙입니다

케이블 80 NORTH 아메리카 POLYETHYLENE (PE) ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (TONS)

TABLE 81 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET, END 사용 산업에 의해, 2018-2032 (USD THOUSAND)

케이블 82 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET, END 사용 산업, 2018-2032 (TONS)

83 NORTH AMERICA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 84 NORTH AMERICA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, 으로 TYPE, 2018-2032 (TONS)

ABLE 85 NORTH AMERICA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

ABLE 86 NORTH AMERICA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (TONS)

케이블 87 NORTH AMERICA 산업 ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (USD THOUSAND)

케이블 88 NORTH AMERICA 산업 ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)

케이블 89 NORTH AMERICA 산업 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 90 NORTH AMERICA 산업 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

테이블 91 NORTH AMERICA AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 92 NORTH AMERICA AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

ABLE 93 NORTH 아메리카 MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 94 NORTH AMERICA MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

테이블 95 NORTH AMERICA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, 으로 TYPE, 2018-2032 (USD THOUSAND)

케이블 96 NORTH AMERICA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, 으로 TYPE, 2018-2032 (TONS)

케이블 97 NORTH AMERICA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 98 NORTH AMERICA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

99 NORTH AMERICA 인쇄 및 ANTIBLOCK ADDITIVE MARKET의 OPTICS, TYPE, 2018-2032 (USD THOUSAND)

TABLE 100 NORTH AMERICA PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (TONS)

TABLE 101 NORTH AMERICA PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

케이블 102 NORTH AMERICA 인쇄 및 ANTIBLOCK ADDITIVE MARKET의 OPTICS, FORM, 2018-2032 (TONS)

TABLE 103 NORTH AMERICA OTHERS IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

TABLE 104 NORTH AMERICA OTHERS IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

케이블 105 미국 ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

케이블 106 미국 ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (TONS)

케이블 107 미국 ANTIBLOCK ADDITIVE MARKET의 INORGANIC, TYPE, 2018-2032 (USD THOUSAND)

케이블 108 미국 ANTIBLOCK ADDITIVE MARKET의 INORGANIC, TYPE, 2018-2032 (TONS)

TABLE 109 미국 ANTIBLOCK ADDITIVE MARKET의 INORGANIC, PARTICLE SHAPE, 2018-2032 (USD THOUSAND)

케이블 110 미국 ANTIBLOCK ADDITIVE MARKET의 INORGANIC, PARTICLE SHAPE, 2018-2032 (TONS)

TABLE 111 미국 ORGANIC IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 112 미국 ORGANIC IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 113 미국 ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (USD THOUSAND)

TABLE 114 미국 ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (TONS)

TABLE 115 미국 POLYETHYLENE (PE) IN ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (USD THOUSAND)

TABLE 116 미국 POLYETHYLENE (PE), 2018-2032 (TONS)

TABLE 117 미국 ANTIBLOCK ADDITIVE MARKET, END USE INDUSTRY에 의해, 2018-2032 (USD THOUSAND)

TABLE 118 미국 ANTIBLOCK ADDITIVE MARKET, 2018-2032 (TONS)

TABLE 119 U.S. PACKAGING IN ANTIBLOCK ADDITIVE MARKET, 으로 TYPE, 2018-2032 (USD THOUSAND)

TABLE 120 미국 ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)에 포장

TABLE 121 미국 ANTIBLOCK ADDITIVE MARKET의 패키지, FORM, 2018-2032 (USD THOUSAND)

케이블 122 미국 ANTIBLOCK ADDITIVE MARKET에 포장, FORM, 2018-2032 (TONS)

TABLE 123 미국 산업 IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

케이블 124 미국 산업 ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)

케이블 125 미국 산업 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 126 미국 산업 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 127 미국 ANTIBLOCK ADDITIVE MARKET의 AGRICULTURE, FORM, 2018-2032 (USD THOUSAND)

케이블 128 미국 ANTIBLOCK ADDITIVE MARKET의 AGRICULTURE, FORM, 2018-2032 (TONS)

TABLE 129 미국 MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

TABLE 130 U.S. MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 131 U.S. 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 132 U.S. 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (TONS)

TABLE 133 미국 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

TABLE 134 미국 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 135 U.S. ANTIBLOCK ADDITIVE MARKET의 PRINTING 및 OPTICS, TYPE, 2018-2032 (USD THOUSAND)

TABLE 136 U.S. ANTIBLOCK ADDITIVE MARKET의 PRINTING 및 OPTICS, TYPE, 2018-2032 (TONS)

TABLE 137 미국 ANTIBLOCK ADDITIVE MARKET의 PRINTING 및 OPTICS, FORM, 2018-2032 (USD THOUSAND)

TABLE 138 미국 ANTIBLOCK ADDITIVE MARKET의 PRINTING 및 OPTICS, FORM, 2018-2032 (TONS)

TABLE 139 미국 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

TABLE 140 미국 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 141 캐나다 ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

TABLE 142 캐나다 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 143 CANADA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

케이블 144 CANADA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (TONS)

테이블 145 캐나다 INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY PARTICLE SHAPE, 2018-2032 (USD THOUSAND)

테이블 146 캐나다 INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY PARTICLE SHAPE, 2018-2032 (TONS)

케이블 147 CANADA ORGANIC IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 148 캐나다 ORGANIC IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 149 캐나다 ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (USD THOUSAND)

TABLE 150 캐나다 ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (TONS)

TABLE 151 캐나다 POLYETHYLENE (PE) IN ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (USD THOUSAND)

TABLE 152 캐나다 POLYETHYLENE (PE) IN ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (TONS)

TABLE 153 캐나다 ANTIBLOCK ADDITIVE MARKET, END USE 산업에 의해, 2018-2032 (USD THOUSAND)

TABLE 154 캐나다 ANTIBLOCK ADDITIVE MARKET, END 사용 산업, 2018-2032 (TONS)

TABLE 155 CANADA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 156 CANADA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (TONS)

TABLE 157 CANADA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

ABLE 158 CANADA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (TONS)

TABLE 159 CANADA 산업 ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (USD THOUSAND)

ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)의 휴대용 160 캐나다 산업

TABLE 161 CANADA 산업용 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 162 CANADA 산업용 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 163 CANADA 플랫폼, 2018-2032 (USD THOUSAND)

케이블 164 CANADA AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

ABLE 165 CANADA MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

TABLE 166 CANADA MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (TONS)

TABLE 167 CANADA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (USD THOUSAND)

TABLE 168 캐나다 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)

케이블 169 CANADA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 170 CANADA 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 171 CANADA PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 172 CANADA PRINTING 및 OPTICS IN ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)

173 CANADA PRINTING 및 OPTICS IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

TABLE 174 CANADA PRINTING 및 OPTICS IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

ABLE 175 CANADA 기타 ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

TABLE 176 CANADA 기타 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 177 멕시코 ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

TABLE 178 MEXICO ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (TONS)

TABLE 179 MEXICO INORGANIC in ANTIBLOCK ADDITIVE MARKET, 으로 유형, 2018-2032 (USD THOUSAND)

TABLE 180 MEXICO INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (TONS)

TABLE 181 MEXICO INORGANIC in ANTIBLOCK ADDITIVE MARKET, BY PARTICLE SHAPE, 2018-2032 (USD THOUSAND)

테이블 182 MEXICO INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY PARTICLE SHAPE, 2018-2032 (TONS)

케이블 183 MEXICO ORGANIC IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

케이블 184 MEXICO ORGANIC IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 185 MEXICO ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER에 의해, 2018-2032 (USD THOUSAND)

TABLE 186 멕시코 ANTIBLOCK ADDITIVE MARKET, TARGET POLYMER, 2018-2032 (TONS)

TABLE 187 MEXICO POLYETHYLENE (PE)는 TARGET POLYMER, 2018-2032 (USD THOUSAND)에 의해 상표를 붙입니다

TABLE 188 MEXICO POLYETHYLENE (PE), 2018-2032 (TONS)

TABLE 189 MEXICO ANTIBLOCK ADDITIVE MARKET, END USE 산업에 의해, 2018-2032 (USD THOUSAND)

TABLE 190 MEXICO ANTIBLOCK ADDITIVE MARKET, END 사용 산업, 2018-2032 (TONS)

TABLE 191 MEXICO PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

ABLE 192 MEXICO PACKAGING IN ANTIBLOCK ADDITIVE MARKET, 으로 유형, 2018-2032 (TONS)

TABLE 193 MEXICO PACKAGING IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

194 MEXICO 패키지 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 195 MEXICO 산업 IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

196 MEXICO 산업 ANTIBLOCK ADDITIVE MARKET, TYPE, 2018-2032 (TONS)

197 MEXICO 산업 ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

198 MEXICO 산업 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 199 MEXICO AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

TABLE 200 MEXICO AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (TONS)

ABLE 201 MEXICO MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

케이블 202 MEXICO MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 203 MEXICO 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 204 MEXICO 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, BY TYPE, 2018-2032 (TONS)

TABLE 205 MEXICO 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

TABLE 206 MEXICO 전기 및 SOLAR IN ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

TABLE 207 MEXICO PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, 으로 TYPE, 2018-2032 (USD THOUSAND)

TABLE 208 MEXICO PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, 으로 TYPE, 2018-2032 (TONS)

TABLE 209 MEXICO PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (USD THOUSAND)

ABLE 210 MEXICO PRINTING AND OPTICS IN ANTIBLOCK ADDITIVE MARKET, FORM에 의해, 2018-2032 (TONS)

ABLE 211 MEXICO 기타 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (USD THOUSAND)

ABLE 212 MEXICO 기타 ANTIBLOCK ADDITIVE MARKET, FORM, 2018-2032 (TONS)

그림 목록

FIGURE 1 북아메리카 ANTIBLOCK 완전한 시장

FIGURE 2 북아메리카 ANTIBLOCK ADDITIVE 시장: DATA 지구

FIGURE 3 북아메리카 ANTIBLOCK 보조 시장: DROC ANALYSIS

FIGURE 4 NORTH AMERICA ANTIBLOCK ADDITIVE 시장: REGIONAL 시장 분석

FIGURE 5 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET : 회사 연혁

FIGURE 6 북아메리카 ANTIBLOCK ADDITIVE 시장: MULTIVARIATE 모형

FIGURE 7 북아메리카 ANTIBLOCK ADDITIVE 시장: DEMOGRAPHICS를 검토하십시오

FIGURE 8 NORTH AMERICA ANTIBLOCK ADDITIVE 시장: DBMR 시장 위치 GRID

FIGURE 9 NORTH AMERICA ANTIBLOCK ADDITIVE 시장: VENDOR SHARE ANALYSIS

FIGURE 10 북아메리카 ANTIBLOCK ADDITIVE 시장: 세그먼트

FIGURE 11 TWO SEGMENTS NORTH AMERICA ANTIBLOCK ADDITIVE MARKET, FORM (2024)

FIGURE 12 NORTH AMERICA ANTIBLOCK ADDITIVE 시장: 독점 제안

FIGURE 13 북아메리카 ANTIBLOCK 완전한 시장: STRATEGIC 차원

플라스틱 포장 NORTH AMERICA를 위한 FIGURE 14 GROWING DEMAND는 FORECAST PERIOD (2025-2032)에 있는 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET를 몰기 위하여 전형적으로 입니다

FIGURE 15 INORGANIC SEGMENT는 2025년과 2032년 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET의 리그 몫을 위한 계정으로 경쟁됩니다

FIGURE 16 호텔 ANALYSIS

FIGURE 17 PORTER의 FIVE FORCES 분석

FIGURE 18 VENDOR 선택 CRITERIA

FIGURE 19 DRIVERS, RESTRAINTS, OPPORTUNITIES, NORTH AMERICA ANTIBLOCK에 대한 도전

FIGURE 20 NORTH AMERICA ANTIBLOCK ADDITIVE 시장: FORM, 2024년

FIGURE 21 북아메리카 ANTIBLOCK ADDITIVE 시장: TARGET POLYMER, 2024년

FIGURE 22 NORTH AMERICA ANTIBLOCK ADDITIVE 시장: END 사용 기업에 의해, 2024

FIGURE 23 북아메리카 ANTIBLOCK 완전한 시장: SNAPSHOT (2024)

FIGURE 24 NORTH AMERICA ANTIBLOCK ADDITIVE MARKET : 회사 SHARE 2024 (%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.