Increasing focus on passenger and crew safety regulations is being identified as a key driver of the global crashworthy aircraft seats market, as aviation authorities continue to strengthen survivability and occupant-protection requirements. Regulatory emphasis on impact attenuation, dynamic load performance, flammability resistance and post-crash evacuation safety has intensified across both commercial and military aviation segments. Crashworthy seating systems have become critical components in meeting updated certification standards, particularly for rotorcraft, military transport aircraft and special-mission platforms operating in high-risk environments.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-crashworthy-aircraft-seats-market

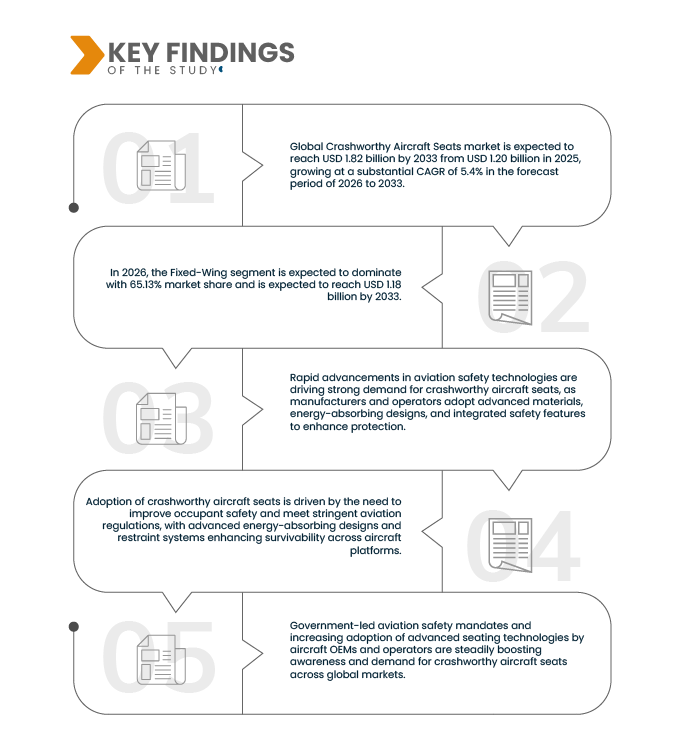

Data Bridge Market Research analyzes that the Global Crashworthy Aircraft Seats Market size was valued at USD 1.20 billion in 2025 and is expected to reach USD 1.82 billion by 2033, at a CAGR of 5.4% during the forecast period of 2026 to 2033.

Key Findings of the Study

Increasing Focus on Passenger and Crew Safety Regulations is Driving Market Growth

Increasing focus on passenger and crew safety regulations is driving demand for crashworthy aircraft seats, as authorities enforce standards for impact attenuation, dynamic load performance, flammability resistance, and post-crash evacuation across commercial and military aviation. Regulatory actions, such as FAA airworthiness directives, seat-dimension transparency rules, and national seatbelt compliance measures, highlight strengthened enforcement and oversight of cabin and cockpit safety. Crashworthy seating systems are critical for compliance with evolving certification standards, particularly for rotorcraft, military transport, and special-mission aircraft operating in high-risk environments. The tightening regulatory environment increases design, certification, and compliance complexity, compelling manufacturers and airlines to adopt advanced seating solutions, thereby supporting sustained market growth. Technological innovations, including energy-absorbing materials, modular seat designs, and integrated safety monitoring systems, are being increasingly incorporated to meet stringent regulations and enhance passenger survivability.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2018-2023)

|

|

Quantitative Units

|

Revenue in USD Millions

|

|

Segments Covered

|

By Platform (Fixed wing and Rotary wing), Fixed Wing Seat Type (Passenger seats, Pilot seats, Troop transport seats and Crew seats) By Fixed Wing Aircraft Type (Commercial aircraft, Military aircraft, General aviation aircraft, Advanced Air Mobility (AAM) vehicles) By Fixed Wing End user By Rotary Wing Seat Type ( Passenger seats, Pilot seats, Crew seats Gunner / observation seats OEM (Original Equipment Manufacturer) MRO (Aftermarket / After-sales), By Rotary Wing Aircraft Type ( Military aircraft, Commercial aircraft, General aviation aircraft, Advanced Air Mobility (AAM) vehicles) By Rotary Wing End User (OEM (Original Equipment Manufacturer) MRO (Aftermarket / After-sales)

|

|

Countries Covered

|

Asia-Pacific China, Japan, South Korea, Taiwan, India, Vietnam, Singapore, Malaysia, Thailand, Philippines, Indonesia, Australia, New Zealand, Rest of Asia-Pacific.., North America, U.S., Canada, Mexico. , Europe, Germany, France, United Kingdom, Italy, Sweden, Netherlands, Switzerland, Spain, Finland, Norway, Denmark, Turkey, Belgium, Russia, Rest of Europe., South America, Brazil, Argentina, Colombia, Chile, Peru, Venezuela, Ecuador, Uruguay, Paraguay, Bolivia, Rest of South America.. Middle East and Africa U.A.E., Saudi Arabia, Israel, South Africa, Egypt, Qatar, Kuwait, Oman, Bahrain, Rest of Middle East and Africa

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

|

Segment Analysis

The market is segmented into seven notable segments which are based on platform, fixed-wing seat type, fixed-wing aircraft type, fixed-wing end user, rotary-wing seat type, rotary-wing aircraft type and rotary-wing end user.

- On the basis of platform, the market is segmented into fixed-wing and rotary-wing.

In 2026, the fixed wing segment is expected to dominate the market

In 2026, the fixed-wing segment is expected to dominate the crashworthy aircraft seats market with a 65.13% share. This is driven by higher demand in commercial and military aircraft, where passenger and crew safety is a top priority. The segment benefits from widespread adoption of advanced crashworthy seating technologies and regulatory compliance requirements. Its leading position is reinforced by continued investments in safety innovations and retrofit programs across fixed-wing fleets

- On the basis of fixed-wing seat type, the market is segmented into passenger seats, pilot seats, troop transport seats, crew seats, and gunner / observation seats

In 2026, the passenger seats segment is expected to dominate the market

In 2026, the passenger seats segment is expected to dominate with a 53.00% market share. This growth is driven by increasing demand for enhanced passenger safety and compliance with stringent aviation regulations. Widespread adoption of advanced crashworthy seating technologies in commercial aircraft further supports the segment’s leading position.

- On the basis of fixed-wing aircraft type, the market is segmented into commercial aircraft, military aircraft, general aviation aircraft, and advanced air mobility (AAM) vehicles. In 2026, the Commercial aircraft segment is expected to dominate with a 61.19% market share. This growth is driven by increasing air passenger traffic, rising demand for enhanced safety features, and strict regulatory compliance requirements. Widespread adoption of advanced crashworthy seating solutions in commercial fleets further supports the segment’s leading position.

- On the basis of fixed-wing end user, the market is segmented into OEM (Original Equipment Manufacturer) and MRO (Aftermarket / After-sales). In 2026, the OEM segment is expected to dominate with a 63.69% market share. This growth is driven by increasing aircraft production, stringent regulatory requirements, and the need for integrated crashworthy seating solutions during manufacturing. Widespread adoption of advanced seat technologies by OEMs ensures compliance and enhances passenger and crew safety, supporting the segment’s leading position.

- On the basis of rotary-wing seat type, the market is segmented into passenger seats, pilot seats, troop transport seats, crew seats, and gunner / observation seats. In 2026, the passenger seats segment is expected to dominate with a 40.99%% market share. This growth is driven by increasing demand for enhanced passenger safety in helicopters and other rotorcraft. Regulatory compliance requirements and adoption of advanced crashworthy seating technologies further support the segment’s leading position. Expansion of commercial, military, and emergency service rotorcraft operations also contributes to market growth.

- On the basis of rotary-wing aircraft type, the market is segmented into commercial aircraft, military aircraft, general aviation aircraft, and advanced air mobility (AAM) vehicles. In 2026, the military aircraft segment is expected to dominate with a 61.19%% market share. This growth is driven by increasing demand for enhanced crew and troop safety in military helicopters. Rising defense budgets, stringent regulatory safety requirements, and adoption of advanced crashworthy seating technologies further support the segment’s leading position.

- On the basis of rotary-wing end user, the market is segmented into OEM (Original Equipment Manufacturer) and MRO (Aftermarket / After-sales). In 2026, the OEM segment is expected to dominate with a 70.22%% market share. This growth is driven by increasing production of rotary-wing aircraft and the demand for factory-installed, crashworthy seating solutions. OEMs are investing in advanced seat designs that meet stringent safety regulations and enhance occupant protection. Rising adoption of these solutions across military, commercial, and emergency rotorcraft further supports the segment’s leading position

Major Players

Collins Aerospace (U.S.), Safran (France), Martin-Baker Aircraft Co. Ltd (U.K.), Recaro Aircraft Seating GmbH & Co. KG (Germany), Jamco Corporation (Japan), Acro Aircraft Seating (U.K.), Airgo Design (Singapore), Airbus (France), Autoflug GmbH (Germany), Aviation Traders Limited – ATL (U.K.), Aviointeriors S.p.A. (Italy), Bombardier (Canada), East/West Industries, Inc. (U.S.), Expliseat (France), Futureflite, Inc. (U.S.), Geven S.p.A. (Italy), Ipeco Holdings Ltd. (U.K.), Israel Aerospace Industries Ltd. (Israel), LifePort (U.S.), MBA S.A. Argentina (Argentina), MESAG-System AG (Switzerland), and Mirus Aircraft Seating (U.K.) are the major players dealing in the market.

Market Developments

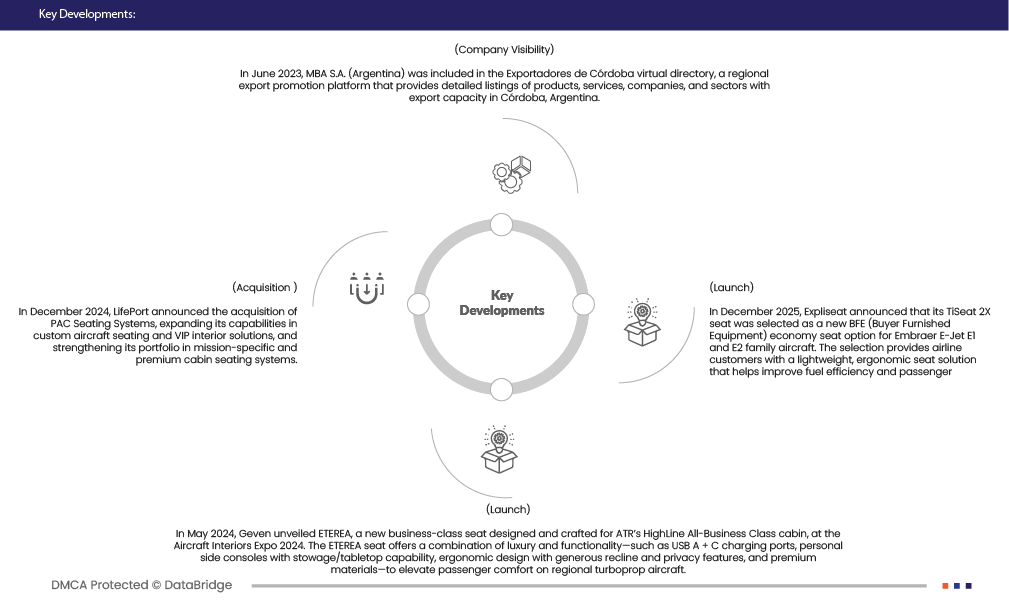

- In June 2023, MBA S.A. (Argentina) was included in the Exportadores de Córdoba virtual directory, a regional export promotion platform that provides detailed listings of products, services, companies, and sectors with export capacity in Córdoba, Argentina. This listing increases visibility for MBA’s aerospace and defence products, including ejection seats and survival systems, among international buyers and supports the company’s export-oriented market development.

- In December 2024, LifePort announced the acquisition of PAC Seating Systems, expanding its capabilities in custom aircraft seating and VIP interior solutions, and strengthening its portfolio in mission-specific and premium cabin seating systems.

- In May 2024, Geven unveiled ETEREA, a new business-class seat designed and crafted for ATR’s HighLine All-Business Class cabin, at the Aircraft Interiors Expo 2024. The ETEREA seat offers a combination of luxury and functionality—such as USB A + C charging ports, personal side consoles with stowage/tabletop capability, ergonomic design with generous recline and privacy features, and premium materials—to elevate passenger comfort on regional turboprop aircraft. This seat is now offered as part of the ATR HighLine All-Business Class configuration on ATR aircraft, supporting airlines seeking enhanced premium cabin solutions in the regional aviation market.

- In December 2025, Expliseat announced that its TiSeat 2X seat was selected as a new BFE (Buyer Furnished Equipment) economy seat option for Embraer E-Jet E1 and E2 family aircraft. The selection provides airline customers with a lightweight, ergonomic seat solution that helps improve fuel efficiency and passenger comfort on regional jet operations.

Regional Analysis

Geographically, the countries covered in the global crashworthy aircraft seats market report are North America, Europe, Asia-Pacific, Middle East and Africa, South America.

The North America crashworthy aircraft seats market accounted for a significant share of 37.36% within the global in 2025. This growth is driven by rapid expansion of commercial and military aviation, increasing focus on passenger and crew safety, and stringent regulatory compliance requirements. Rising investments in fleet modernization, adoption of advanced crashworthy seating technologies, and growth in rotorcraft and urban air mobility operations further support the market. Strong government initiatives to enhance aviation safety standards also contribute to global leading position.

As per Data Bridge Market Research analysis:

For more detailed information about the global crashworthy aircraft seats market report, click here – https://www.databridgemarketresearch.com/reports/global-crashworthy-aircraft-seats-market