أدى تزايد حالات العمليات الجراحية، وما يتبعها من دخول وحدات العناية المركزة، إلى زيادة الطلب على مراقبة ديناميكية الدم المتقدمة. غالبًا ما تتطلب التدخلات الجراحية، بدءًا من الإجراءات الروتينية وصولًا إلى الجراحات المعقدة، مراقبة دقيقة لحالة ديناميكية الدم لدى المريض لضمان أفضل النتائج. تتضمن مراقبة ديناميكية الدم تقييمًا مستمرًا لمؤشرات القلب والأوعية الدموية، مثل ضغط الدم، والنتاج القلبي، وحالة السوائل، مما يوفر رؤىً ثاقبة حول جهاز الدورة الدموية لدى المريض أثناء الجراحة وبعدها.

أدى ارتفاع معدلات الأمراض المزمنة، بما في ذلك داء السكري وارتفاع ضغط الدم والسمنة، إلى زيادة الحاجة إلى العمليات الجراحية لإدارة هذه الحالات وعلاجها. على سبيل المثال، قد يحتاج مرضى السكري إلى جراحات مرتبطة بمضاعفات مثل مرض الشرايين الطرفية أو اعتلال الأعصاب السكري.

بالإضافة إلى ذلك، مع تزايد تعقيد التدخلات الجراحية، تزداد الحاجة إلى بيانات دقيقة للديناميكية الدموية، لا سيما في إجراءات مثل جراحات القلب، وزراعة الأعضاء، وجراحات العظام الكبرى. في بيئات الرعاية الحرجة، وخاصةً وحدات العناية المركزة، تُصبح مراقبة الديناميكية الدموية أمرًا بالغ الأهمية لإدارة المرضى الذين يعانون من حالات طبية معقدة أو فترة التعافي بعد الجراحة. على سبيل المثال، وفقًا لمقال NCBI، لم تتغير أساسيات مراقبة الديناميكية الدموية إلا قليلاً في السنوات الأخيرة. ويبقى الهدف الرئيسي من مراقبة الديناميكية الدموية لدى المرضى المصابين بأمراض حرجة هو التقييم الدقيق للجهاز القلبي الوعائي واستجابته لطلب الأنسجة للأكسجين.

يمكنك الوصول إلى التقرير الكامل على https://www.databridgemarketresearch.com/reports/global-hemodynamic-monitoring-market

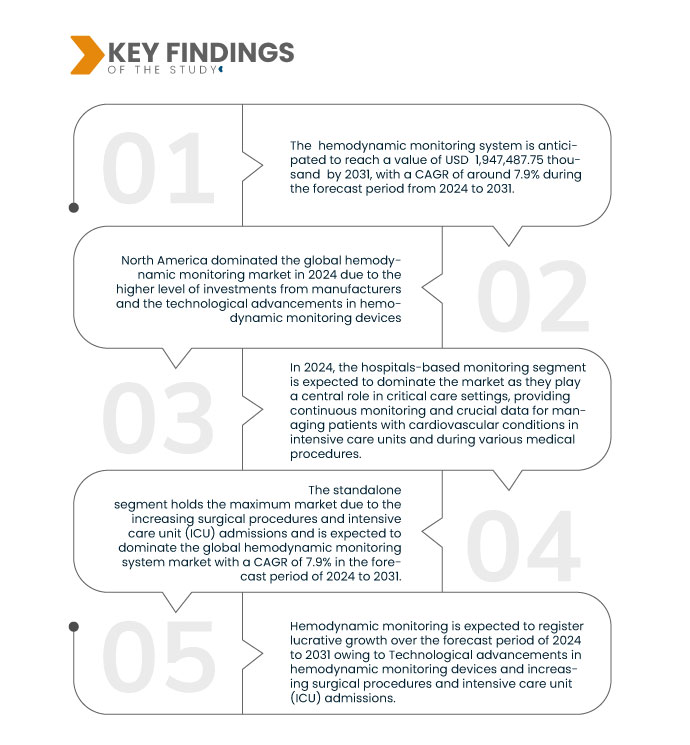

تحلل شركة Data Bridge Market Research أن سوق مراقبة الدورة الدموية العالمية من المتوقع أن ينمو بمعدل نمو سنوي مركب قدره 7.2٪ في الفترة المتوقعة من 2024 إلى 2031، ومن المتوقع أن يصل إلى 3،839،125.07 ألف دولار أمريكي بحلول عام 2031. في عام 2024، من المتوقع أن يهيمن قطاع أنظمة مراقبة الدورة الدموية على السوق بسبب ارتفاع حالات اضطرابات القلب والأوعية الدموية.

النتائج الرئيسية للدراسة

دمج مراقبة الدورة الدموية مع الطب عن بعد

يُمثل دمج مراقبة الدورة الدموية مع التطبيب عن بُعد نقلة نوعية في مجال الرعاية الصحية، لا سيما في سياق مراقبة الدورة الدموية. ويُمثل دمج مراقبة الدورة الدموية مع التطبيب عن بُعد نهجًا تحويليًا لتقديم الرعاية الصحية، مستفيدًا من التكنولوجيا لتوفير تقييم فوري وتدخلات طبية لتحسين صحة القلب والأوعية الدموية للمرضى.

إن التكامل مع الطب عن بعد يعيد تشكيل الرعاية الصحية،

على سبيل المثال،

التقاط البيانات في الوقت الحقيقي:

تتضمن مراقبة ديناميكية الدم قياسًا مستمرًا لمؤشرات القلب والأوعية الدموية، مثل ضغط الدم ومعدل ضربات القلب وتشبع الأكسجين. تلتقط الأجهزة القابلة للارتداء والمزودة بأجهزة استشعار هذه البيانات آنيًا، مما يوفر صورة شاملة لحالة القلب والأوعية الدموية للمريض.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

من 2024 إلى 2031

|

سنة الأساس

|

2023

|

السنوات التاريخية

|

2022 (قابلة للتخصيص حتى 2016-2021)

|

الوحدات الكمية

|

الإيرادات بالألف دولار أمريكي

|

القطاعات المغطاة

|

المنتج (أنظمة مراقبة الدورة الدموية، أجهزة مراقبة العلامات الحيوية، أجهزة قياس التأكسج النبضي ، القسطرة والمواد الاستهلاكية والملحقات)، النوع (مراقبة الدورة الدموية غير الجراحية، مراقبة الدورة الدموية طفيفة التوغل ومراقبة الدورة الدموية الجراحية)، الوسيلة (مستقلة، سطح الطاولة، محمولة، يمكن ارتداؤها وغيرها)، التطبيق (مراقبة في المستشفيات، مراقبة في المختبرات ومراقبة منزلية)، التكوين (آلي ويدوي)، الفئة العمرية (بالغ، كبار السن، وطب الأطفال)، المستخدم النهائي (المستشفيات، مراكز الجراحة الخارجية ، مختبرات القسطرة، دور التمريض، الرعاية المنزلية، المؤسسات الطبية، مراكز إعادة التأهيل، وغيرها)، قناة التوزيع (غير متصلة بالإنترنت وعبر الإنترنت)

|

الدول المغطاة

|

الولايات المتحدة الأمريكية، كندا، المكسيك، ألمانيا، المملكة المتحدة، فرنسا، روسيا، إيطاليا، إسبانيا، تركيا، بولندا، بلجيكا، هولندا، سويسرا، الدنمارك، السويد، النرويج، فنلندا، بقية أوروبا، الصين، اليابان، الهند، أستراليا، كوريا الجنوبية، نيوزيلندا، سنغافورة، تايلاند، الفلبين، ماليزيا، إندونيسيا، فيتنام، تايوان، بقية دول آسيا والمحيط الهادئ، البرازيل، الأرجنتين، بقية دول أمريكا الجنوبية، المملكة العربية السعودية، الإمارات العربية المتحدة، جنوب أفريقيا، مصر، قطر، الكويت، عُمان، البحرين، وبقية دول الشرق الأوسط وأفريقيا

|

الجهات الفاعلة في السوق المغطاة

|

Icumedical (الولايات المتحدة)، Teleflex Incorporated (الولايات المتحدة)، Koninklijke Philips NV (هولندا)، GE HealthCare (الولايات المتحدة)، Edwards Lifesciences Corporation (الولايات المتحدة)، Masimo (الولايات المتحدة)، Baxter (الولايات المتحدة)، Getinge AB (السويد)، CONTEC MEDICAL SYSTEMS CO.,LTD (الصين)، Nihon Kohden Corporation (اليابان)، Merit Medical Systems (الولايات المتحدة)، Drägerwerk AG & Co. KGaA (ألمانيا)، OSYPKA MEDICAL (ألمانيا)، Deltex Medical (الولايات المتحدة)، SC، Schwarzer Cardiotek (ألمانيا)، Caretaker LLC. (الولايات المتحدة)، Uscom (أستراليا)، NI-Medical (إسرائيل)، CNSystems Medizintechnik GmbH (النمسا)، وArgon Medical Devices (الولايات المتحدة)، وغيرها.

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، فإن تقارير السوق التي تم تنظيمها بواسطة Data Bridge Market Research تتضمن أيضًا تحليلًا متعمقًا من الخبراء وعلم الأوبئة للمرضى وتحليل خطوط الأنابيب وتحليل التسعير والإطار التنظيمي.

|

تحليل القطاعات

يتم تصنيف سوق مراقبة الدورة الدموية العالمية إلى ثمانية قطاعات بارزة بناءً على المنتج والنوع والوسيلة والتطبيق والتكوين والفئة العمرية والمستخدم النهائي وقناة التوزيع.

- على أساس المنتج، يتم تقسيم السوق إلى أنظمة مراقبة الدورة الدموية، وأجهزة مراقبة العلامات الحيوية، وأجهزة قياس التأكسج النبضي، والقسطرة، والمواد الاستهلاكية والملحقات

في عام 2024، من المتوقع أن يهيمن قطاع مراقبة الدورة الدموية على السوق

ومن المتوقع أن تهيمن أنظمة مراقبة الدورة الدموية على السوق في عام 2024 بحصة سوقية تبلغ 48.50% بسبب ارتفاع معدل الإصابة باضطرابات القلب والأوعية الدموية.

- على أساس النوع، يتم تقسيم السوق إلى مراقبة ديناميكية الدم غير الجراحية، ومراقبة ديناميكية الدم طفيفة التوغل، ومراقبة ديناميكية الدم الجراحية

في عام 2024، من المتوقع أن يهيمن قطاع مراقبة الدورة الدموية غير الجراحية على السوق

من المتوقع أن تهيمن شريحة مراقبة الدورة الدموية غير الجراحية على السوق في عام 2024 بحصة سوقية تبلغ 61.13% بسبب التقدم التكنولوجي في أجهزة مراقبة الدورة الدموية.

- بناءً على طريقة الاستخدام، يُقسّم السوق إلى أجهزة مستقلة، وأجهزة مكتبية، وأجهزة محمولة، وأجهزة قابلة للارتداء، وغيرها. في عام ٢٠٢٤، من المتوقع أن يهيمن قطاع الأجهزة المستقلة على السوق بحصة سوقية تبلغ ٤٧.٩٢٪.

- بناءً على التطبيق، يُقسّم السوق إلى مراقبة المستشفيات، ومراقبة المختبرات، ومراقبة المنازل. في عام ٢٠٢٤، من المتوقع أن يهيمن قطاع مراقبة المستشفيات على السوق بحصة سوقية تبلغ ٧٤.٨٢٪.

- بناءً على التكوين، يُقسّم السوق إلى آلي ويدوي. في عام ٢٠٢٤، من المتوقع أن يهيمن القطاع الآلي على السوق بحصة سوقية تبلغ ٧٣.٦٣٪.

- بناءً على الفئات العمرية، يُقسّم السوق إلى فئات للبالغين، وكبار السن، والأطفال. في عام ٢٠٢٤، من المتوقع أن تهيمن شريحة النساء على السوق بحصة سوقية تبلغ ٦٦.٥١٪.

- بناءً على المستخدم النهائي، يُقسّم السوق إلى مستشفيات، ومراكز جراحة متنقلة، ومختبرات قسطرة، ودور رعاية مسنين، وخدمات رعاية منزلية، ومؤسسات طبية، ومراكز إعادة تأهيل، وغيرها. وفي عام ٢٠٢٤، من المتوقع أن يهيمن قطاع المستشفيات والعيادات على السوق بحصة سوقية تبلغ ٦٦.٦٤٪.

- بناءً على قنوات التوزيع، يُقسّم السوق إلى سوقين: سوق غير متصل بالإنترنت وسوق عبر الإنترنت. في عام ٢٠٢٤، من المتوقع أن يهيمن قطاع المناقصات المباشرة على السوق بحصة سوقية تبلغ ٨٤.٠٤٪.

اللاعبون الرئيسيون

تقوم شركة Data Bridge Market Research بتحليل شركات Edwards Lifesciences Corporation (الولايات المتحدة)، وMasimo (الولايات المتحدة)، وGettinge AB (السويد)، وBaxter (الولايات المتحدة)، وTeleflex Incorporated (الولايات المتحدة) باعتبارها الشركات الرئيسية في سوق مراقبة الدورة الدموية العالمية.

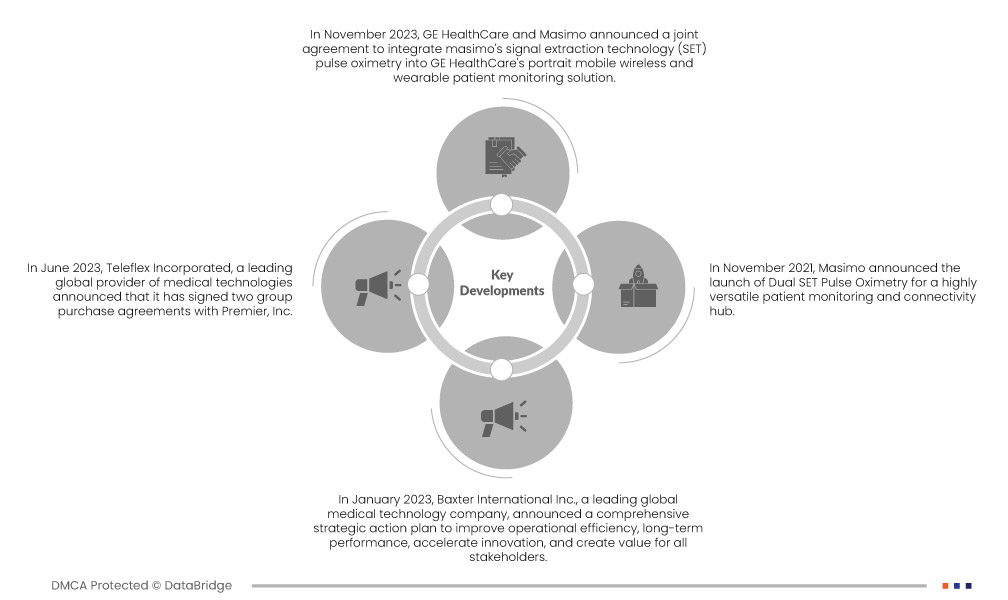

تطورات السوق

- في مايو 2024، أعلنت شركة بريستول مايرز سكويب (المدرجة في بورصة نيويورك تحت الرمز: BMY) بالشراكة مع شركة جانسن للأدوية، إحدى شركات جانسن للأدوية التابعة لشركة جونسون آند جونسون (جانسن)، أن جميع المؤشرات الثلاثة المحتملة لدواء ميلفيكسيان، وهو مثبط فموي تجريبي لعامل التخثر الحادي عشر (FXIa)، قد حصلت الآن على تصنيف المسار السريع من إدارة الغذاء والدواء الأمريكية (FDA). تشمل الأسماء جميع التجارب الثلاث التي تسعى إلى مؤشرات في برنامج تطوير ليبركسيا للمرحلة الثالثة (ليبركسيا لمراقبة ديناميكية الدم، وليبركسيا ACS، وليبركسيا AF)، وجميعها للمرضى الذين تلقوا جرعات. يُعد برنامج ليبركسيا برنامجًا فريدًا من نوعه للتطوير السريري الشامل لعامل التخثر الحادي عشر، حيث يوفر بيانات شاملة من ما يقرب من 50,000 مريض. وهذا يفتح الباب أمام مجموعة جديدة تمامًا من المرضى المهملين حاليًا بسبب خطر النزيف.

- في يناير 2024، أعلنت شركة بينومبرا، وهي شركة عالمية للرعاية الصحية تُركز على العلاجات المبتكرة، عن موافقة إدارة الغذاء والدواء الأمريكية (FDA) على إطلاق جهاز Lightning Flash، وهو أحدث وأقوى نظام ميكانيكي لاستئصال الخثرة في السوق. يتميز Lightning Flash بتقنية Lightning Intelligent Aspiration الجديدة من بينومبرا، والتي تحتوي الآن على خوارزميتين للكشف عن الجلطات. وبدمجه مع تقنية القسطرة المبتكرة، صُمم Lightning Flash لإزالة جلطات الدم الكبيرة من الجسم بسرعة، بما في ذلك الانسداد الوريدي والانسداد الرئوي. سيساعد هذا الإطلاق الشركة على توسيع محفظة منتجاتها بفضل النتائج المتقدمة لهذه التقنية الجديدة التي يمكن تتبعها بشكل استثنائي، فضلًا عن قدرتها الفريدة على التمييز بين الدم المتدفق والجلطات.

- في يوليو 2024، أعلنت شركة روش عن شراكة جديدة مع شركة ألنيلام لتطوير وتسويق زيليبسير، وهو علاج تجريبي بتقنية تداخل الحمض النووي الريبوزي (RNAi) في مرحلته الثانية لعلاج ارتفاع ضغط الدم. يجمع هذا التعاون بين خبرة ألنيلام المثبتة في علاج تداخل الحمض النووي الريبوزي (RNAi) ونطاق روش التجاري العالمي، والتزامها بالابتكار، ورغبتها في تغيير واقع مرضى أمراض القلب والأوعية الدموية الشديدة.

- في فبراير 2021، حصل دواء بلافيكس (كلوبيدوجريل) من شركة سانوفي على موافقة المفوضية الأوروبية لاستخدامه مع الأسبرين لدى المرضى البالغين المصابين بنوبة إقفارية عابرة متوسطة أو عالية الخطورة (TIA) (درجة ABCD2 ≥ 4) أو بمراقبة ديناميكية دموية إقفارية خفيفة (IS). يتم ذلك خلال أربع وعشرين ساعة من حدوث نوبة إقفارية عابرة أو نوبة إقفارية خفيفة. في هذا المؤشر الجديد، يمكن الاستمرار في الاستخدام لمدة 21 يومًا، متبوعًا بعلاج طويل الأمد بمضاد صفيحات واحد. يستند المؤشر الإضافي إلى نتائج دراسة من المرحلة الثالثة، مزدوجة التعمية، عشوائية، خاضعة للتحكم الوهمي، بدأها باحثان، وشملت أكثر من 10000 مريض. أظهرت الدراسات أن الجمع بين كلوبيدوجريل والأسبرين، الذي بدأ في غضون 24 ساعة، أفضل من الأسبرين في تقليل خطر مراقبة ديناميكية الدم اللاحقة، وله ملف تعريف أمان مقبول بشكل عام. تُظهر هذه الموافقة الجديدة التزام الشركات الراسخ بتطوير رعاية القلب والأوعية الدموية.

- في سبتمبر 2020، أعلنت شركة دايتشي سانكيو المحدودة عن تقديمها طلبًا إضافيًا في اليابان للحصول على موافقة مُوسّعة على دواء إيدوكسابان (هيدرات بنزوات إيدوكسابان) المُضاد للتخثر لعلاج المرضى المسنين المُصابين بقصور غير صمامي ومُعرّضين لخطر نزيف حاد. يستند هذا الطلب إلى نتائج تجربة سريرية يابانية من المرحلة الثالثة (تجربة ELDERCARE-AF) أُجريت على 984 مريضًا مُصابًا بالرجفان الأذيني غير الصمامي، والذين تبلغ أعمارهم 80 عامًا على الأقل، والذين يُعانون من خطر نزيف مرتفع، وغير مُلائمين لعلاجات التخثر الأخرى المُتاحة. تُخطط دايتشي سانكيو للمساهمة في علاج المرضى المسنين المُصابين بالرجفان الأذيني غير الصمامي من خلال تقديم خيار علاجي جديد.

التحليل الإقليمي

جغرافيًا، البلدان التي يغطيها تقرير سوق مراقبة الدورة الدموية العالمية هي الولايات المتحدة وكندا والمكسيك وألمانيا والمملكة المتحدة وفرنسا وروسيا وإيطاليا وإسبانيا وتركيا وبولندا وبلجيكا وهولندا وسويسرا والدنمارك والسويد والنرويج وفنلندا وبقية أوروبا والصين واليابان والهند وأستراليا وكوريا الجنوبية ونيوزيلندا وسنغافورة وتايلاند والفلبين وماليزيا وإندونيسيا وفيتنام وتايوان وبقية دول آسيا والمحيط الهادئ والبرازيل والأرجنتين وبقية دول أمريكا الجنوبية والمملكة العربية السعودية والإمارات العربية المتحدة وجنوب إفريقيا ومصر وقطر والكويت وعمان والبحرين وبقية دول الشرق الأوسط وأفريقيا وفقًا لتحليل أبحاث سوق Data Bridge:

من المتوقع أن تهيمن أمريكا الشمالية على سوق مراقبة الدورة الدموية العالمية

من المتوقع أن تُهيمن أمريكا الشمالية على السوق نظرًا للطلب المرتفع على أجهزة مراقبة الدورة الدموية في المنطقة وارتفاع نفقات الرعاية الصحية. وستواصل أمريكا الشمالية هيمنتها على سوق أجهزة مراقبة الدورة الدموية من حيث الحصة السوقية والإيرادات، وستواصل تعزيز هيمنتها خلال فترة التوقعات.

من المتوقع أن تكون منطقة آسيا والمحيط الهادئ هي المنطقة الأسرع نموًا في سوق مراقبة الدورة الدموية العالمية

ومن المتوقع أن تكون منطقة آسيا والمحيط الهادئ أسرع المناطق نمواً في السوق خلال فترة التوقعات، وذلك بسبب التبني المتزايد للتكنولوجيا المتقدمة وإطلاق منتجات جديدة في هذه المنطقة.

لمزيد من المعلومات التفصيلية حول تقرير سوق مراقبة الدورة الدموية العالمية، انقر هنا - https://www.databridgemarketresearch.com/reports/global-hemodynamic-monitoring-market