The Asia-Pacific healthcare sector is undergoing a profound digital transformation, driven by rapid adoption of healthcare IT systems and steadily rising public and private healthcare expenditure. Governments across APAC are increasingly prioritizing digital health as a core pillar of healthcare modernization, focusing on electronic health records (EHRs), health information exchanges (HIEs), telehealth platforms, national digital health IDs, and data-driven public health systems. This accelerated digitalization has significantly elevated the need for interoperability solutions that enable seamless, secure, and standardized data exchange across fragmented healthcare ecosystems.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-interoperability-market

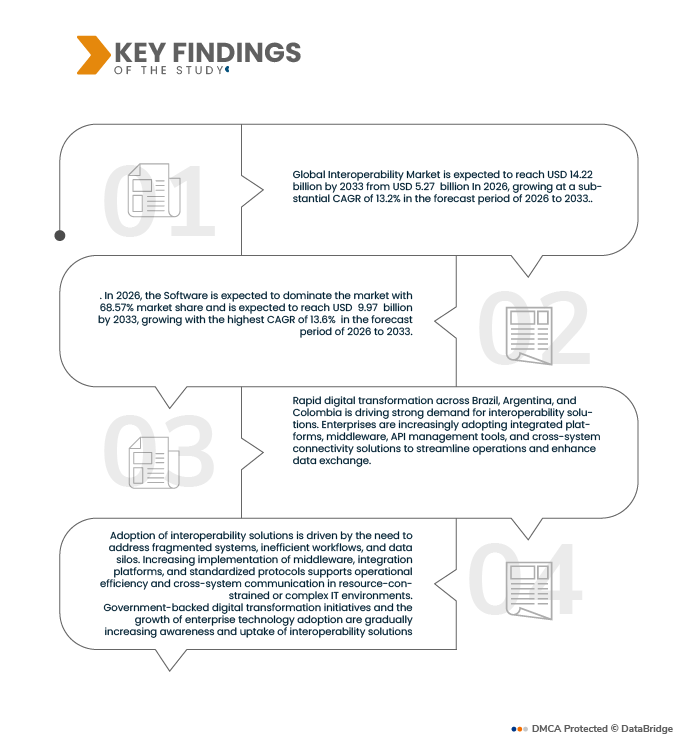

Data Bridge Market Research analyses that the Global Interoperability Market is expected to reach USD 14.22 billion by 2033 from USD 5.27 billion in 2025, growing with a CAGR of 13.2% in the forecast period of 2026 to 2033

Key Findings of the Study

Strong Government Initiatives and National EHR/EMR Programs

Governments across the Asia-Pacific region are playing a pivotal role in accelerating the adoption of healthcare interoperability through large-scale national EHR/EMR programs and digital health policy frameworks. Recognizing health data as critical national infrastructure, public authorities are actively investing in centralized and federated electronic health record systems to improve care continuity, population health management, and system-wide efficiency. These government-led initiatives are significantly increasing demand for interoperability solutions that enable standardized, secure, and real-time data exchange across diverse healthcare stakeholders.

Many APAC countries are implementing nationwide digital health architectures that mandate interoperability across public and private healthcare providers. These programs typically include core components such as unique patient identifiers, standardized clinical data formats, consent management frameworks, and national health information exchanges. As healthcare providers onboard onto these platforms, interoperability becomes a regulatory requirement rather than a discretionary technology choice, positioning integration engines, API frameworks, and standards-compliant middleware as essential enablers of national digital health ecosystems.

Furthermore, governments are increasingly linking EHR/EMR adoption with broader healthcare reforms, including universal health coverage, value-based care, and digital insurance administration. This integration requires seamless data flow between hospitals, clinics, laboratories, pharmacies, payers, and public health authorities—further reinforcing the role of interoperability platforms in ensuring data continuity, compliance, and scalability. Public funding, regulatory mandates, and long-term digital health roadmaps are collectively creating a stable and sustained demand environment for interoperability solutions across APAC.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2018-2024 (Customizable from 2013-2017)

|

|

Quantitative Units

|

Revenue in USD Billion

|

|

Segments Covered

|

Component Type (Software and Services), Interoperability Level (Foundational Interoperability, Structural Interoperability, Organizational Interoperability, and Semantic Interoperability), Deployment Model (On-Premise, Cloud-Based, and Edge & Gateway-Based Deployment), Architecture Model (Hybrid Architecture, Centralized Architecture, and Decentralized Architecture) Application (Clinical Applications, Administrative Applications, Public Health & Population Health, Financial Applications, Digital & Virtual Care, Research & Analytics, and Others) End User (Healthcare Providers, Government & Public Health Bodies, Healthcare Payers, Life Sciences & Research Organizations, Pharmacies & Pharmacy Networks, Patients & Consumer Health Platforms, and Others).

|

|

Countries Covered

|

U.S., Canada and Mexico in North America, Germany, U.K., France, Spain, Belgium, Russia, Netherlands, Italy, Turkey, Switzerland, Sweden, Denmark, Norway, Finland, and Rest of Europe in Europe, India, China, Japan, Australia, South Korea, Singapore, Thailand, Indonesia, Taiwan, Hong Kong, Malaysia, New Zealand, Philippines, and Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), U.A.E, Saudi Arabia, South Africa, Egypt, Qatar, Kuwait, Bahrain, Oman, Israel, and Rest of Middle East and Africa as a part of Middle East and Africa (MEA), Brazil, Argentina and rest of South America

|

|

Market Players Covered

|

Major companies in the market are Epic Systems Corporation (U.S.), Oracle (U.S.), InterSystems Corporation (U.S.), Microsoft Corporation (U.S.), Amazon Web Services (AWS) (U.S.), NextGen Healthcare (U.S.), Infor (U.S.), Allscripts Healthcare Solutions (U.S.), MEDITECH (U.S.), McKesson Corporation (U.S.), Athenahealth (U.S.), Orion Health (New Zealand), Philips Healthcare (Netherlands), Siemens Healthineers (Germany), GE Healthcare (U.S.), IBM Corporation (U.S.), Health Catalyst (U.S.), CareEvolution (USA), Capsule Technologies (USA), Interfaceware (Canada), Smile CDR (Canada), 1upHealth (U.S.), Health Gorilla (U.S.), TriNetX (U.S.), Verato (U.S.), Surescripts (U.S.), CitiusTech Inc. (India), NextGen HealthCare (U.S.), Intersystems (U.S.), Epic Systems (U.S.), and others.

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework..

|

Segment Analysis

The global interoperability market is segmented into six notable segments, which are based on component type, interoperability level, deployment model, architecture model, application, and end user.

- On the basis of component, the global interoperability market is segmented into software and services.

In 2026, the software segment is expected to dominate the global interoperability market

In 2026, the software is expected to dominate the market with 68.57% market share and is expected to reach USD 9.97 billion by 2033, growing with the highest CAGR of 13.6% in the forecast period of 2026 to 2033.

- On the basis of interoperability level, the global interoperability market is segmented into foundational interoperability, structural interoperability, semantic interoperability, and organizational interoperability.

In 2026, the foundational interoperability segment is expected to dominate the global interoperability market

In 2026, the foundational interoperability segment is expected to dominate the market with 35.34% market share and is expected to reach USD 134.810 billion by 2032, growing with the highest CAGR of 6.9% in the forecast period of 2026 to 2033.

- On the basis of deployment model, the global interoperability market is segmented into on-premise, cloud-based, and edge & gateway-based deployment. In 2026, the on-premise segment is expected to dominate the market with 44.89% market share and is expected to reach USD 6.36 billion by 2033, growing with the highest CAGR of 13.2% in the forecast period of 2026 to 2033.

- On the basis of architecture model, the global interoperability market is segmented into centralized architecture, decentralized architecture, and hybrid architecture. In 2026, the hybrid architecture segment is expected to dominate the market with 39.39% market share and is expected to reach USD 5.275 billion by 2033, growing with the highest CAGR of 12.3% in the forecast period of 2026 to 2033.

- On the basis of application, the global interoperability market is segmented into clinical applications, administrative applications, financial applications, public health & population health, digital & virtual care, and research & analytics. In 2026, the Clinical Applications segment is expected to dominate the market with 33.28% market share and is expected to reach USD 4.77 billion by 2033, growing with the highest CAGR of 13.4% in the forecast period of 2026 to 2033.

- On the basis of end user, the Global Interoperability Market is segmented into Healthcare Providers, Healthcare Payers, Pharmacies & Pharmacy Networks, Government & Public Health Bodies, Life Sciences & Research Organizations, and Patients & Consumer Health Platforms. In 2026, the Healthcare Providers segment is expected to dominate the market with 34.26% market share and is expected to reach USD 4.99 billion by 2033, growing with the highest CAGR of 13.6%in the forecast period of 2026 to 2033.

Major Players

Data Bridge Market Research analyzes some of the major market players operating in the market, such as Epic Systems Corporation (U.S.), Oracle (U.S.), InterSystems Corporation (U.S.), Microsoft Corporation (U.S.), Amazon Web Services (AWS) (U.S.), NextGen Healthcare (U.S.), Infor (U.S.), Allscripts Healthcare Solutions (U.S.), MEDITECH (U.S.), McKesson Corporation (U.S.), Athenahealth (U.S.), Orion Health (New Zealand), Philips Healthcare (Netherlands), Siemens Healthineers (Germany), GE Healthcare (U.S.), IBM Corporation (U.S.), Health Catalyst (U.S.), CareEvolution (U.S.), Capsule Technologies (U.S.), Interfaceware (Canada), Smile CDR (Canada), 1upHealth (U.S.), Health Gorilla (U.S.), TriNetX (U.S.), Verato (U.S.), Surescripts (U.S.), CitiusTech Inc. (India), NextGen HealthCare (U.S.), Intersystems (U.S.), Epic Systems (U.S.), and others.

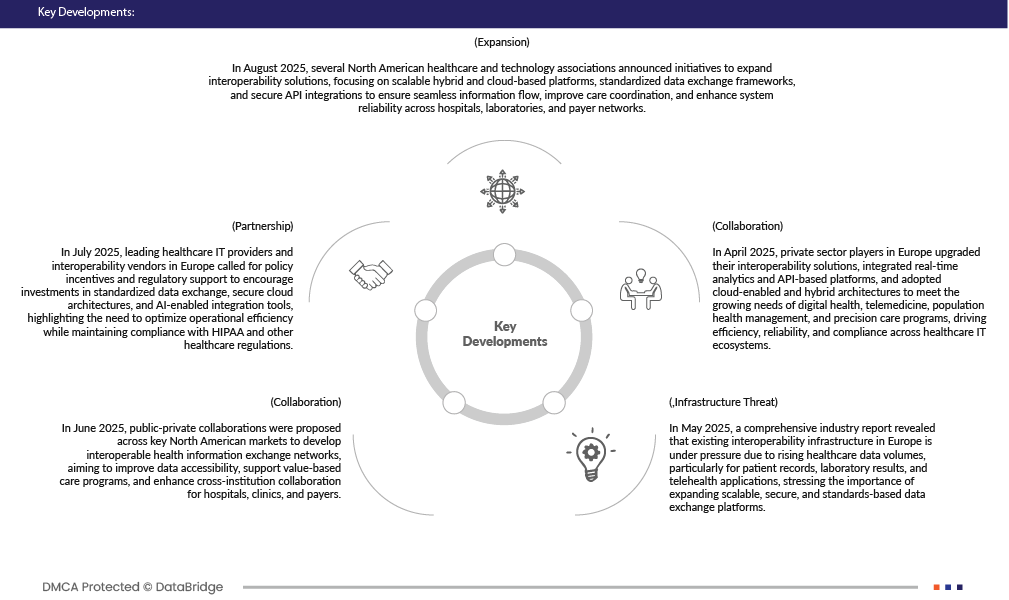

Market Developments

- In November 2025, Oracle Health Information Network Inc., a subsidiary of Oracle, was designated as a Qualified Health Information Network (QHIN) as a part of the Trusted Exchange Framework and Common Agreement (TEFCA). Building on a long legacy of paving the way for interoperability across the healthcare industry.

- In September 2023, St. Peter’s Health transitioned to a new Electronic Health Record (EHR) called Epic. The switch enhances Epic's dominance in healthcare IT, as widespread use.

- In November 2025, InterSystems announced the launch of InterSystems HealthShare AI Assistant, a new generative AI capability designed to assist clinicians, case managers, and administrators in accessing and understanding patient information faster and more intuitively.

- In November 2025, InterSystems, a global leader in data management and healthcare information systems, today announced the launch of InterSystems Public Sector Corporation (IPSC), a new subsidiary dedicated to serving the unique needs of government agencies at the federal, state, and local levels.

- In November 2025, AWS expanded its AI Competency program with new Agentic AI categories for partners, including tools, applications, and consulting, enhancing the ecosystem for autonomous AI systems under AWS certification and support.

Regional Analysis

Geographically, the country covered in the global interoperability market report is U.S., Canada and Mexico in North America, Germany, U.K., France, Spain, Belgium, Russia, Netherlands, Italy, Turkey, Switzerland, Sweden, Denmark, Norway, Finland, and Rest of Europe in Europe, India, China, Japan, Australia, South Korea, Singapore, Thailand, Indonesia, Taiwan, Hong Kong, Malaysia, New Zealand, Philippines, and Rest of Asia-Pacific (APAC) in the Asia-Pacific (APAC), U.A.E, Saudi Arabia, South Africa, Egypt, Qatar, Kuwait, Bahrain, Oman, Israel, and Rest of Middle East and Africa as a part of Middle East and Africa (MEA), Brazil, Argentina and rest of South America.

As per Data Bridge Market Research analysis:

North America is the dominant region in the global interoperability market

North America leads the global interoperability market due to its advanced healthcare infrastructure, including widespread adoption of electronic health records (EHRs) and digital health platforms.

Asia Pacific is estimated to be the fastest-growing region in the global interoperability market

Asia Pacific is expected to be the fastest-growing region in the global interoperability market from 2026 to 2033, driven by accelerating digitization of healthcare systems across countries like China, Japan, and India, alongside robust government initiatives establishing national health information exchanges.

For more detailed information about the Global Interoperability market, click here – https://www.databridgemarketresearch.com/reports/global-interoperability-market