تُعدّ غرسات العظام، بما فيها غرسات الأسنان، أجهزة طبية بالغة الأهمية. فهي تُعيد الحركة ونوعية الحياة للمرضى الذين يعانون من مشاكل في المفاصل أو كسور أو فقدان الأسنان. تتميز هذه الغرسات بمواد متوافقة حيويًا تتكامل مع أنسجة الجسم، مما يضمن ثباتها ومتانتها. تُستخدم في جراحات العظام، مثل استبدال المفاصل وتثبيت الكسور. تُوفر غرسات الأسنان حلاً طويل الأمد للأسنان المفقودة، مما يُحسّن وظيفة الفم وجماله. بشكل عام، تُحسّن غرسات العظام صحة المرضى بشكل كبير من خلال استعادة الحركة الجسدية وصحة الأسنان.

احصل على التقرير الكامل على الرابط التالي: https://www.databridgemarketresearch.com/reports/mena-and-gcc-orthopedic-implants-including-dental-implants-market

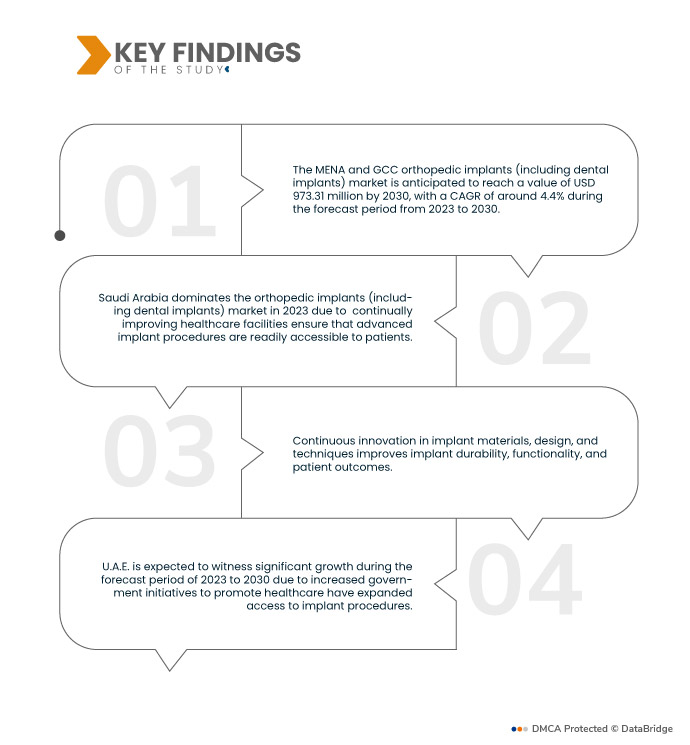

تشير تحليلات شركة داتا بريدج لأبحاث السوق إلى أن قيمة سوق زراعة العظام (بما في ذلك زراعة الأسنان) في منطقة الشرق الأوسط وشمال أفريقيا ودول مجلس التعاون الخليجي بلغت 689.67 مليون دولار أمريكي في عام 2022، ومن المتوقع أن تصل إلى 973.31 مليون دولار أمريكي بحلول عام 2030، مسجلةً معدل نمو سنوي مركب قدره 4.4% خلال الفترة المتوقعة من 2023 إلى 2030. ويعاني كبار السن من مشاكل العظام والأسنان، مثل تنكس المفاصل وفقدان الأسنان. ويعزز هذا التوجه الديموغرافي الطلب على زراعة العظام والأسنان كحلول فعالة لمعالجة هذه المشاكل الصحية المرتبطة بالعمر، مما يدفع عجلة نمو سوق زراعة الأسنان.

النتائج الرئيسية للدراسة

من المتوقع أن يؤدي الوعي بصحة الأسنان إلى دفع معدل نمو السوق

يُعدّ تزايد الوعي بصحة الأسنان وفوائد زراعة الأسنان كخيار دائم لاستبدال الأسنان عاملاً رئيسياً في نمو السوق. يبحث المرضى عن حلول طويلة الأمد تُحاكي الأسنان الطبيعية وتُحسّن صحتهم الفموية بشكل عام. يُشجع هذا الوعي المزيد من الناس على التفكير في زراعة الأسنان بدلاً من الخيارات التقليدية، مثل أطقم الأسنان أو الجسور. ونتيجةً لذلك، يستمر الطلب على زراعة الأسنان في الارتفاع، حيث يُولي المرضى أهميةً كبيرةً لصحة أسنانهم وجودة حياتهم.

نطاق التقرير وتقسيم السوق

مقياس التقرير

|

تفاصيل

|

فترة التنبؤ

|

من 2023 إلى 2030

|

سنة الأساس

|

2022

|

السنوات التاريخية

|

2021 (قابلة للتخصيص حتى 2015-2020)

|

الوحدات الكمية

|

الإيرادات بالملايين من الدولارات الأمريكية، والحجم بالوحدات، والتسعير بالدولار الأمريكي

|

القطاعات المغطاة

|

المنتجات (استبدال المفاصل الترميمية، زراعة العمود الفقري ، الصدمات وجراحة الوجه والفكين، زراعة الأسنان، الأجهزة الحيوية التقويمية)، نوع الأجهزة (أجهزة التثبيت الداخلية وأجهزة التثبيت الخارجية)، المواد الحيوية ( المواد الحيوية المعدنية ، المواد الحيوية البوليمرية، المواد الحيوية الخزفية، المواد الحيوية الطبيعية وغيرها)، الإجراءات (الجراحة المفتوحة والجراحة طفيفة التوغل)، المستخدم النهائي (المستشفيات، مراكز الرعاية الخارجية، العيادات المتخصصة، مراكز العظام وغيرها)، الملكية (الحكومية والخاصة)

|

الدول المغطاة

|

المملكة العربية السعودية والكويت والإمارات العربية المتحدة وقطر والبحرين وعمان

|

الجهات الفاعلة في السوق المغطاة

|

3M (الولايات المتحدة)، B. Braun Melsungen AG (ألمانيا)، Integra LifeSciences (الولايات المتحدة)، Depuy Synthes (شركة تابعة لـ JnJ) Inc. (الولايات المتحدة)، Zimmer Biomet (الولايات المتحدة)، Smith & Nephew plc (المملكة المتحدة)، Medtronic (أيرلندا)، Stryker (الولايات المتحدة)، Changzhou Waston Medical Appliance Co., Ltd. (الولايات المتحدة)، Narang Medical Limited (الهند)، WL Gore & Associates, Inc. (الولايات المتحدة)، Arthrex, Inc. (الولايات المتحدة)، GE HEALTHCARE (الولايات المتحدة)، DJO, LLC (شركة تابعة لـ Colfax Corporation) (الصين)، Curex (الولايات المتحدة)، Samay Surgical (الهند)، Dongguan Traumed Technology Co., Ltd. (الصين)، Abou Hamela Group (مصر)

|

نقاط البيانات التي يغطيها التقرير

|

بالإضافة إلى الرؤى حول سيناريوهات السوق مثل القيمة السوقية ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، تتضمن تقارير السوق التي أعدتها Data Bridge Market Research أيضًا تحليلًا متعمقًا من الخبراء وعلم الأوبئة للمرضى وتحليل خط الأنابيب وتحليل التسعير والإطار التنظيمي.

|

تحليل القطاعات:

يتم تقسيم سوق زراعة العظام (بما في ذلك زراعة الأسنان) في منطقة الشرق الأوسط وشمال أفريقيا ودول مجلس التعاون الخليجي على أساس المنتجات ونوع الأجهزة والمواد الحيوية والإجراءات والمستخدم النهائي والملكية.

- بناءً على المنتجات، يُقسّم سوق غرسات العظام (بما في ذلك غرسات الأسنان) إلى بدائل المفاصل الترميمية، وغرسات العمود الفقري، وغرسات الصدمات والوجه والفكين، وغرسات الأسنان، والغرسات الحيوية التقويمية. في عام 2023، يهيمن قطاع بدائل المفاصل الترميمية على سوق غرسات العظام (بما في ذلك غرسات الأسنان) بمعدل نمو سنوي مركب قدره 5.1% خلال الفترة المتوقعة من 2023 إلى 2030، مع تزايد شيخوخة السكان، وانتشار الأمراض المتعلقة بالمفاصل مثل هشاشة العظام.

في عام 2023، يهيمن قطاع استبدال المفاصل الترميمي على سوق الغرسات العظمية (بما في ذلك الغرسات السنية) بمعدل نمو سنوي مركب قدره 5.1% خلال الفترة المتوقعة من 2023 إلى 2030

في عام ٢٠٢٣، يهيمن قطاع استبدال المفاصل الترميمي على سوق غرسات العظام (بما في ذلك غرسات الأسنان) بمعدل نمو سنوي مركب قدره ٥.١٪ خلال الفترة المتوقعة من ٢٠٢٣ إلى ٢٠٣٠، حيث تُقدم جراحات استبدال المفاصل الترميمية، مثل جراحات استبدال مفصل الورك والركبة، حلولاً فعّالة لاستعادة الحركة وتخفيف الألم. وقد أدى التقدم التكنولوجي إلى تصميمات غرسات متينة ومبتكرة، مما حسّن نتائج المرضى. بالإضافة إلى ذلك، أصبحت هذه الإجراءات أكثر سهولة، مع تحسين التقنيات الجراحية وتقصير فترات التعافي.

- بناءً على نوع الأجهزة، يُقسّم سوق غرسات العظام (بما في ذلك غرسات الأسنان) إلى أجهزة تثبيت داخلية وأجهزة تثبيت خارجية. في عام 2023، يهيمن قطاع أجهزة التثبيت الداخلية على سوق غرسات العظام (بما في ذلك غرسات الأسنان) بمعدل نمو سنوي مركب قدره 4.5% خلال الفترة المتوقعة من 2023 إلى 2030، حيث تُعدّ هذه الأجهزة، بما في ذلك البراغي والصفائح والمسامير، أساسيةً لتثبيت الكسور وتسهيل التئام العظام.

- بناءً على المواد الحيوية، يُقسّم سوق غرسات العظام (بما في ذلك غرسات الأسنان) إلى مواد حيوية معدنية، ومواد حيوية بوليمرية، ومواد حيوية سيراميكية، ومواد حيوية طبيعية ، وغيرها. في عام 2023، سيهيمن قطاع المواد الحيوية المعدنية على سوق غرسات العظام (بما في ذلك غرسات الأسنان) بمعدل نمو سنوي مركب قدره 4.7% خلال الفترة المتوقعة من 2023 إلى 2030، حيث تُعدّ المواد الحيوية المعدنية، مثل التيتانيوم والفولاذ المقاوم للصدأ، ذات قيمة عالية لقوتها ومتانتها وتوافقها الحيوي، مما يجعلها مثالية لغرسات العظام مثل استبدال المفاصل وأجهزة العمود الفقري.

- بناءً على الإجراءات، يُقسّم سوق غرسات العظام (بما في ذلك غرسات الأسنان) إلى جراحات مفتوحة وجراحة طفيفة التوغل . في عام 2023، سيهيمن قطاع الجراحة المفتوحة على سوق غرسات العظام (بما في ذلك غرسات الأسنان) بمعدل نمو سنوي مركب قدره 4.5% خلال الفترة المتوقعة من 2023 إلى 2030، حيث توفر إجراءات الجراحة المفتوحة التقليدية رؤية مباشرة وردود فعل لمسية لجراحي العظام، مما يسمح بتركيب دقيق للغرسات، خاصةً في الحالات المعقدة.

- بناءً على المستخدم النهائي، يُقسّم سوق غرسات العظام (بما في ذلك غرسات الأسنان) إلى مستشفيات، ومراكز رعاية طبية خارجية، وعيادات متخصصة، ومراكز عظام، وغيرها. في عام 2023، يهيمن قطاع المستشفيات على سوق غرسات العظام (بما في ذلك غرسات الأسنان) بمعدل نمو سنوي مركب قدره 4.8% خلال الفترة المتوقعة من 2023 إلى 2030، حيث تُعدّ المستشفيات مراكز رئيسية للإجراءات الجراحية، بما في ذلك جراحات العظام.

في عام 2023، يهيمن قطاع المستشفيات على سوق غرسات العظام (بما في ذلك غرسات الأسنان) بمعدل نمو سنوي مركب قدره 4.8% خلال الفترة المتوقعة من 2023 إلى 2030

في عام ٢٠٢٣، سيهيمن قطاع المستشفيات على سوق زراعة العظام (بما في ذلك زراعة الأسنان) بمعدل نمو سنوي مركب قدره ٤.٨٪ خلال الفترة المتوقعة من ٢٠٢٣ إلى ٢٠٣٠، بفضل توفر معدات متطورة وجراحين ذوي خبرة ومرافق رعاية شاملة للمرضى، مما يجعلها الخيار الأمثل لإجراءات زراعة العظام المعقدة. علاوة على ذلك، غالبًا ما تتلقى المستشفيات إحالات لحالات عظام متخصصة، مما يعزز هيمنتها في هذا السوق. مع تزايد أعمار سكان العالم وانتشار مشاكل العظام، يستمر الطلب على إجراءات زراعة العظام في المستشفيات في الارتفاع، مما يعزز مكانة قطاع المستشفيات الرائدة في نمو السوق.

- بناءً على الملكية، يُقسّم سوق زراعة العظام (بما في ذلك زراعة الأسنان) إلى قطاعين حكومي وخاص. في عام 2023، سيهيمن القطاع الحكومي على سوق زراعة العظام (بما في ذلك زراعة الأسنان) بمعدل نمو سنوي مركب قدره 4.7% خلال الفترة المتوقعة من 2023 إلى 2030، نظرًا لدوره المحوري في تنظيم وتمويل أنظمة الرعاية الصحية.

اللاعبون الرئيسيون

تعترف شركة Data Bridge Market Research بالشركات التالية باعتبارها اللاعبين الرئيسيين في سوق زراعة العظام (بما في ذلك زراعة الأسنان) في منطقة الشرق الأوسط وشمال إفريقيا ودول مجلس التعاون الخليجي في سوق زراعة العظام (بما في ذلك زراعة الأسنان) وهي: 3M (الولايات المتحدة)، B. Braun Melsungen AG (ألمانيا)، Integra LifeSciences (الولايات المتحدة)، Depuy Synthes (شركة تابعة لشركة JnJ) Inc. (الولايات المتحدة)، Zimmer Biomet (الولايات المتحدة)، Smith & Nephew plc (المملكة المتحدة)، Medtronic (أيرلندا)، Stryker (الولايات المتحدة)، Changzhou Waston Medical Appliance Co.، Ltd. (الولايات المتحدة).

تطورات السوق

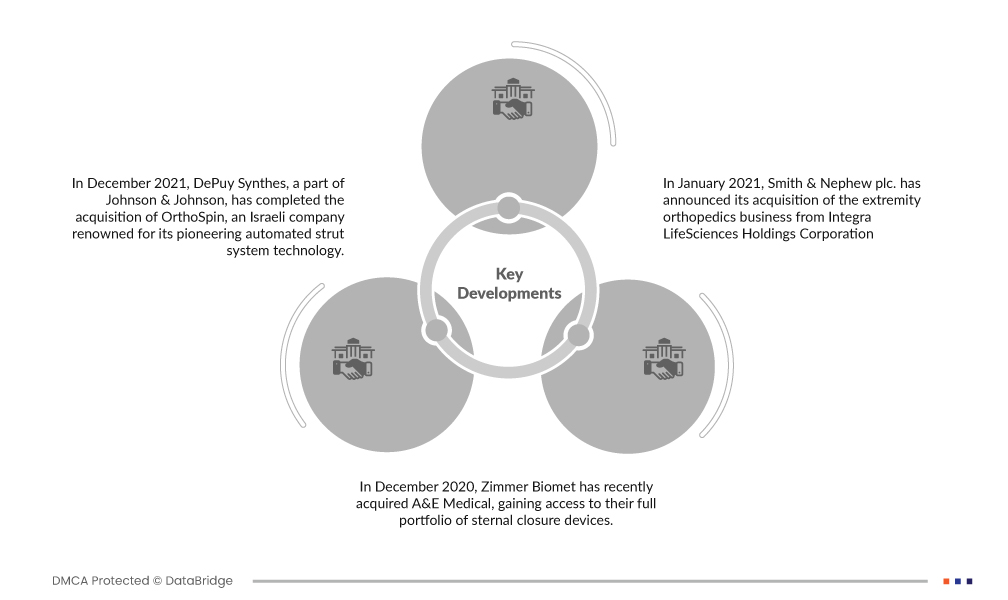

- في ديسمبر 2021، استحوذت شركة ديبوي سينثس، التابعة لشركة جونسون آند جونسون، على شركة أورثوسبين، وهي شركة إسرائيلية تشتهر بتقنيتها الرائدة في أنظمة الدعامات الآلية. يُكمّل هذا النظام المبتكر نظام ماكسفرام متعدد المحاور للتصحيح من ديبوي سينثس، وهو نظام تثبيت حلقي خارجي، مما يُعزز قدرات الشركة في مجال الابتكار الطبي.

- في ديسمبر 2020، استحوذت شركة زيمر بيوميت مؤخرًا على شركة A&E Medical، مما أتاح لها الوصول إلى محفظتها الكاملة من أجهزة إغلاق القص. يُوسّع هذا الاستحواذ الاستراتيجي محفظة زيمر بيوميت من أجهزة تقويم العظام بشكل كبير، مما يُهيئ الشركة لزيادة المبيعات وزيادة الطلب في السوق. ومن المتوقع أن تُسهم هذه الخطوة في نمو إيرادات زيمر بيوميت مستقبلًا.

- في يناير 2021، أعلنت شركة سميث آند نيفيو بي إل سي عن استحواذها على قسم جراحة العظام للأطراف من شركة إنتيغرا لايف ساينسز هولدينجز كوربوريشن. وقد ساهمت هذه الخطوة الاستراتيجية في توسيع محفظة منتجات الشركة بشكل فعال.

التحليل الإقليمي

جغرافيًا، الدول التي يغطيها تقرير سوق زراعة العظام (بما في ذلك زراعة الأسنان) في منطقة الشرق الأوسط وشمال إفريقيا ودول مجلس التعاون الخليجي هي المملكة العربية السعودية والكويت والإمارات العربية المتحدة وقطر والبحرين وعمان.

وفقًا لتحليل Data Bridge Market Research:

تهيمن المملكة العربية السعودية على سوق زراعة العظام (بما في ذلك زراعة الأسنان) في منطقة الشرق الأوسط وشمال أفريقيا ودول مجلس التعاون الخليجي خلال الفترة المتوقعة 2023 - 2030

في عام ٢٠٢٣، ستهيمن المملكة العربية السعودية على سوق زراعة العظام (بما في ذلك زراعة الأسنان) في منطقة الشرق الأوسط وشمال إفريقيا ودول مجلس التعاون الخليجي، بفضل الحضور القوي لكبار اللاعبين في هذا المجال، مما يُحفّز الابتكار والمنافسة، ويعزز جودة وتنوع الغرسات المتاحة. علاوة على ذلك، تدعم البنية التحتية المتميزة للرعاية الصحية في المناطق المتقدمة التكامل السلس لهذه الغرسات. وأخيرًا، يُسهم العدد الكبير من السكان الذين يعانون من الإصابات والعمليات الجراحية، وخاصةً في شريحة سكانية متقدمة في السن، في نمو السوق المستدام، حيث تُصبح الغرسات حلولاً حيوية لاستعادة القدرة على الحركة وتحسين جودة الحياة.

من المتوقع أن تشهد دولة الإمارات العربية المتحدة نموًا كبيرًا خلال الفترة المتوقعة من 2023 إلى 2030

في عام ٢٠٢٣، من المتوقع أن تشهد دولة الإمارات العربية المتحدة نموًا ملحوظًا بفضل تزايد الوعي العام بفوائد زراعة الأسنان والخيارات الجراحية المتقدمة، مما أدى إلى زيادة طلب المرضى عليها. ثالثًا، أدى تزايد عدد السكان، إلى جانب الحاجة المتزايدة إلى رعاية صحية عالية الجودة، إلى خلق سوق واسعة لهذه التقنيات الطبية المتقدمة. باختصار، تجتمع هذه العوامل لتدعم توسع سوق زراعة العظام استجابةً لتزايد الوعي والطلب على الرعاية الصحية.

لمزيد من المعلومات التفصيلية حول تقرير سوق زراعة العظام (بما في ذلك زراعة الأسنان) ، انقر هنا - https://www.databridgemarketresearch.com/reports/mena-and-gcc-orthopedic-implants-including-dental-implants-market